Quick Navigation

Report Overview

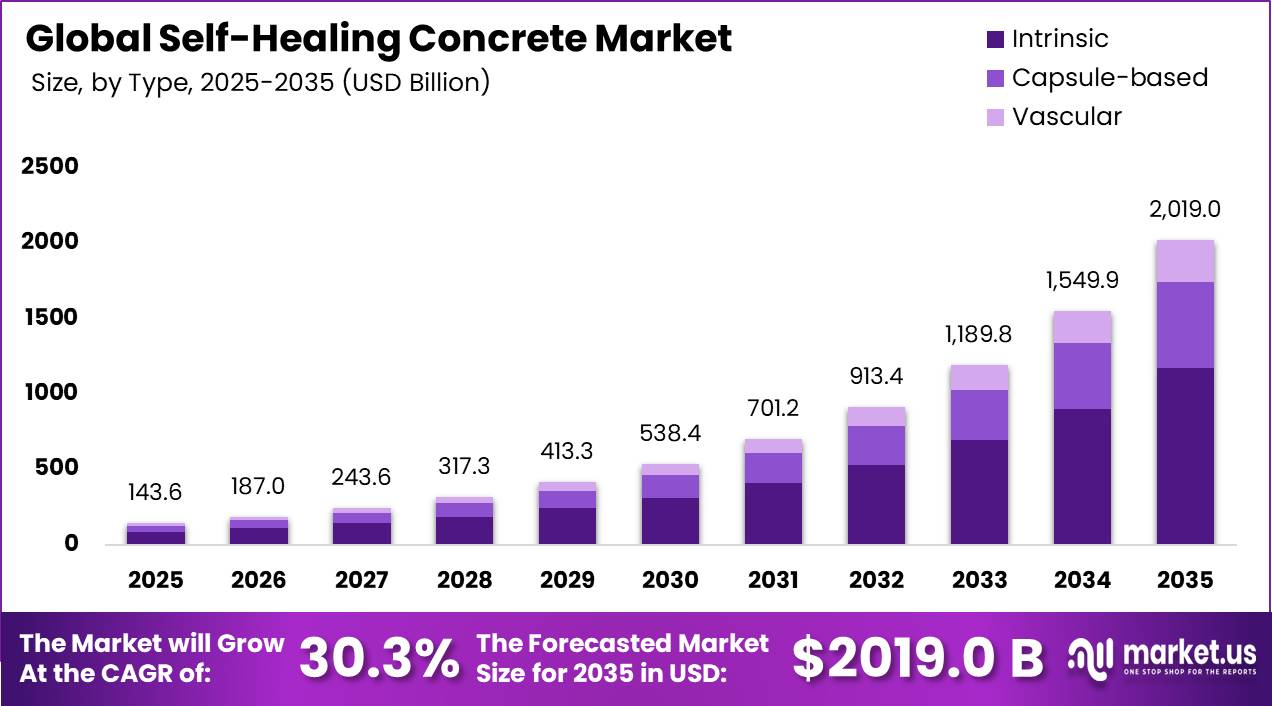

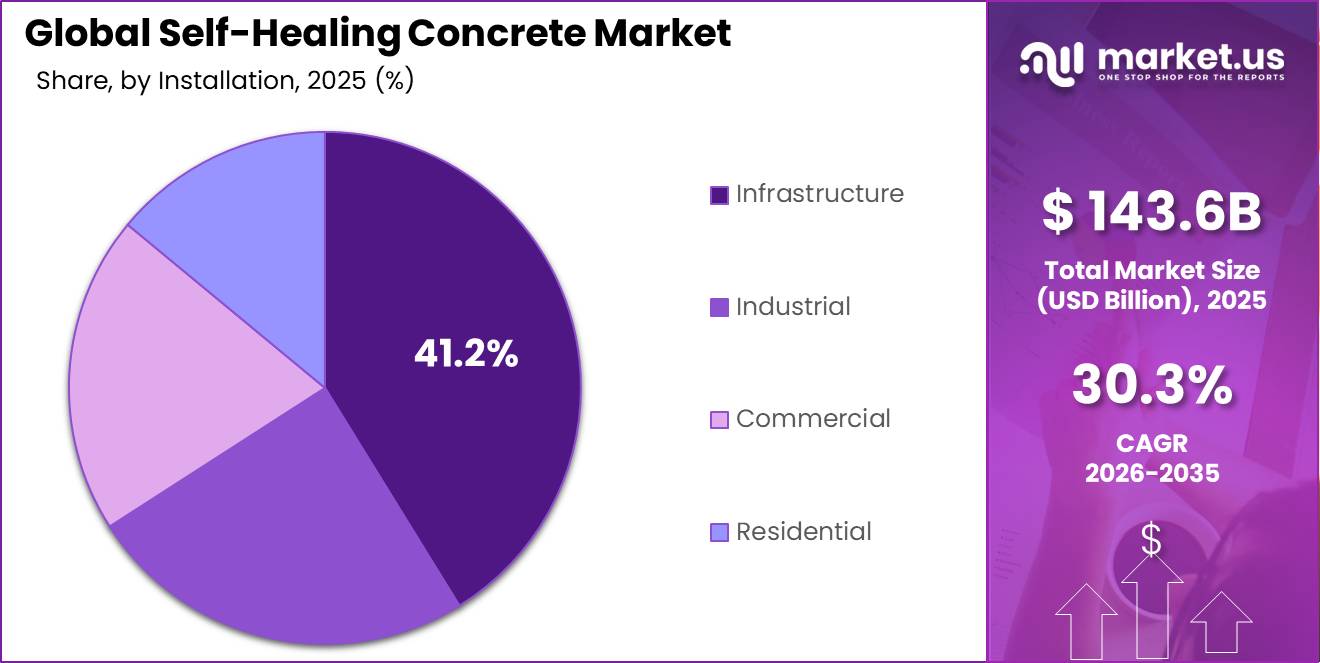

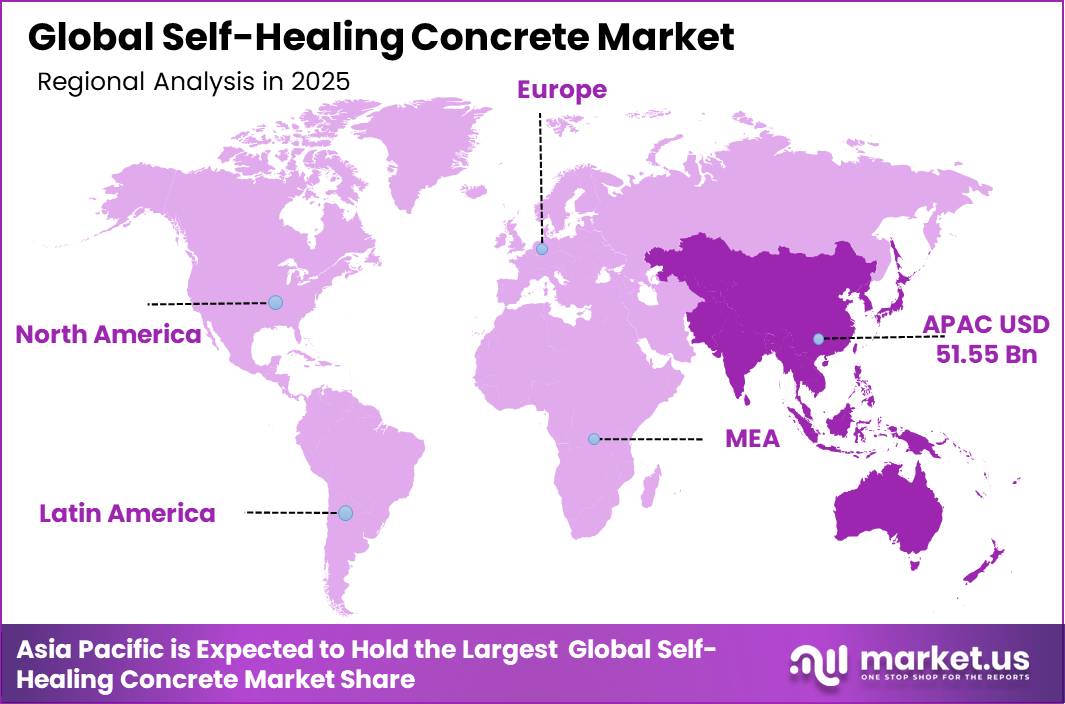

The Global Self-Healing Concrete Market was valued at US$143.6 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 30.3%, reaching about US$2019.0 billion by 2035. Asia Pacific held a dominant market position, capturing more than a 35.9% share, holding USD 51.55 billion in revenue.

Self-healing concrete is an advanced construction material designed to autonomously repair microcracks through mechanisms such as bacterial mineralization, encapsulated healing agents, or continued cement hydration. The technology is gaining attention across infrastructure, commercial, and industrial construction due to its ability to improve durability, extend asset life, and reduce maintenance requirements.

- Self-healing concrete has demonstrated 85–95% crack-closure efficiency for cracks up to 0.8 mm, helping to reduce deterioration caused by moisture penetration, corrosion, and environmental stress. These performance benefits make the material particularly suitable for bridges, tunnels, marine structures, and water infrastructure projects.

The industrial landscape is being shaped by increasing investments in infrastructure modernization, sustainable construction practices, and durable building materials. Conventional concrete repair methods often provide service lives of only 10–15 years, encouraging infrastructure owners to adopt advanced materials that enhance structural longevity.

Future growth opportunities are expected to arise from smart city developments, climate-resilient infrastructure, and sustainable construction initiatives. Studies indicate that self-healing concrete can reduce long-term maintenance costs by approximately 50% over a 50-year service life, supporting its increasing adoption among asset owners focused on lifecycle performance and total cost optimization.

Key Takeaways

- The global self-healing concrete market was valued at USD 143.6 billion in 2025.

- The global self-healing concrete market is projected to grow at a CAGR of 30.3% and is estimated to reach USD 2019.0 billion by 2035.

- On the basis of type, the intrinsic segment dominated the market, constituting 58.1% of the total market share.

- Based on installation, the infrastructure segment dominated the self-healing concrete market, with a substantial market share of around 41.2%.

- Based on component, bridges and tunnels led the market, comprising 35.4% of the total market.

- Among the technologies, bacterial-based self-healing concrete is the most considerable within the market, accounting for around 48.3% of the revenue.

- In 2025, Asia Pacific was the most dominant region in the self-healing concrete market, accounting for 35.9% of the total global consumption.

Type Analysis

Intrinsic self-healing concrete holds the largest share in the market

Intrinsic self-healing concrete holds the largest share in the market at 58.1%. Unlike other forms that rely on externally added healing agents or complex delivery systems, intrinsic self-healing concrete achieves its repair capability through the inherent chemical properties of the concrete mix itself. When cracks form, the unhydrated cement particles within the mix react with water and air to produce calcium carbonate crystals that naturally fill and seal the damage from within.

The remaining segments, capsule-based (28.2%) and vascular (13.7%), offer distinct but important capabilities within the self-healing concrete market. Capsule-based systems operate through microcapsules embedded in the concrete matrix that rupture upon crack formation, releasing healing agents that autonomously seal the damage.

This approach is widely used in high-value structures such as bridges, tunnels, and marine infrastructure where crack prevention is critical for safety and durability. Vascular self-healing concrete represents a more advanced system, using internal channel networks to continuously supply healing agents to damaged areas. This enables repeated healing over the structure’s lifespan and is gaining attention for long-term critical infrastructure applications.

Installation Analysis

Infrastructure Emerges as the Largest Installation Segment

Infrastructure accounts for the largest installation share at 41.2%, and this dominance reflects a very simple reality. No other construction category puts concrete under more stress or faces higher consequences when that concrete fails.

Bridges, tunnels, roads, dams, airports, and power stations are constantly exposed to heavy traffic loads, extreme weather conditions, chemical exposure, and mechanical stress that cause cracking far more rapidly and severely than in any other built environment.The cost of repairing or replacing these structures using conventional methods is enormous, and the disruption caused to communities and economies during repair works adds another layer of urgency.

Self-healing concrete addresses this problem directly by reducing the frequency and scale of maintenance interventions needed over the lifespan of an infrastructure asset, making it an increasingly attractive material choice for government agencies and engineering firms responsible for building and maintaining public infrastructure.

Component Analysis

Bridges and Tunnels Emerge as the Dominant Component Segment

Bridges and tunnels account for 35.4% of the self-healing concrete market by component, making them the single largest area of application, and the reasons are deeply practical. These structures operate under some of the most punishing conditions of any built asset, carrying enormous loads, enduring constant vibration from traffic, and facing continuous exposure to moisture, de-icing salts, and temperature extremes that accelerate concrete cracking and corrosion of steel reinforcement.

The consequences of structural failure in a bridge or tunnel are severe, not just in financial terms but in human safety terms, which is why engineers and infrastructure authorities are increasingly willing to specify premium materials like self-healing concrete that can demonstrably extend structural integrity and reduce the risk of dangerous crack propagation between maintenance cycles.

The global push to rebuild and upgrade aging bridge and tunnel networks across North America, Europe, and Asia is creating a large and sustained pipeline of projects where self-healing concrete is becoming a standard specification rather than an experimental choice.

Technology Analysis

Bacterial-Based Self-Healing Concrete Emerges as the Dominant Technology Segment

Bacterial-based self-healing concrete holds the largest technology share at 48.3%, and this leadership position reflects both the effectiveness of the technology and the growing importance of sustainability credentials in construction material procurement decisions.

In bacterial-based systems, specially selected dormant bacteria, typically from the Bacillus genus, are embedded within the concrete mix along with a nutrient source. When cracks form and allow water and oxygen to enter, the bacteria activate, metabolise the nutrients, and produce calcium carbonate as a byproduct, which fills and seals the crack naturally and permanently.

The healing process produces no harmful chemical residues; the bacteria remain dormant and harmless within the concrete until activated, and the calcium carbonate produced is chemically identical to the mineral compounds already present in the concrete matrix.

Key Market Segments

By Type

- Intrinsic

- Capsule-based

- Vascular

By Installation

- Infrastructure

- Industrial

- Commercial

- Residential

By Component

- Bridges & Tunnels

- Buildings

- Roads & Highways

- Marine Structures

By Technology

- Microcapsule-based

- Bacterial-based

- Polymer-based

- Others

Challenges

Input cost volatility remains a major restraint for the self-healing concrete market because the technology depends on an energy-intensive cement and admixture supply chain. Cement production costs still carry approximately 30%–40% energy exposure, while self-healing concrete typically commands a 25%–40% cost premium over conventional concrete due to healing agents and specialized manufacturing processes. These factors contribute to an estimated −1.0 percentage point drag on potential market CAGR in 2026.

Fluctuations in electricity, clinker, polymers, encapsulation materials, and freight costs continue to pressure supplier margins, often forcing quotation validity periods down to 15–30 days and increasing bidding selectivity for long-cycle infrastructure projects. The challenge is particularly pronounced where reimbursement timelines are uncertain, and cost recovery mechanisms are limited.

To mitigate these pressures, producers are increasingly regionalizing healing-agent production, adopting dual-source procurement strategies, and incorporating escalation clauses into contracts. Adoption is also being focused on marine infrastructure, basements, and water-retaining structures, where a 5%–10% upfront premium can be justified by 20%–40% lower maintenance and intervention requirements over the asset life.

| Challenge | (~) % CAGR Friction | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Performance Validation Gaps | −1.4% | EU innovation corridors, North America core, Japan, South Korea | Medium term (2–4 years) |

| Healing Agent Durability Drift | −1.2% | Hot-arid MENA, freeze-thaw Europe, coastal APAC, North America | Long term (≥ 4 years) |

| Input Cost Volatility | −1.0% | Europe, import-dependent Asia, urban megaproject hubs | Medium term (2–4 years) |

| Carbon Data Compliance Burden | −0.8% | EU regulatory hubs, UK-aligned spec markets, premium public procurement zones | Medium term (2–4 years) |

| SCM Availability Rebalancing | −0.9% | North America, Europe, China transition belts | Long term (≥ 4 years) |

| Specialized Installation Skills Deficit | −1.1% | Europe core, U.S. infrastructure states, advanced APAC metros | Long term (≥ 4 years) |

Opportunity

Offshore energy infrastructure represents a significant opportunity for self-healing concrete, particularly in offshore wind foundations, floating platforms, coastal protection systems, and geothermal facilities. While adoption is currently limited to high-value pilot projects, research has demonstrated maintenance-free performance of up to 50 years in marine and energy-related applications, improving long-term asset economics for operators managing difficult-to-access structures.

The opportunity is supported by projections of approximately USD 25 trillion in cumulative energy infrastructure investment and USD 50 trillion in transportation investment by 2050, with Asia-Pacific accounting for more than 52% of total spending. Even a modest 0.15%–0.25% specification penetration into marine and energy-related concrete applications could create a multi-hundred-million-dollar revenue opportunity for self-healing concrete by the early 2030s.

The business case is strengthened by lifecycle benefits, including up to 60% lower steel reinforcement requirements and 25% fewer patch repairs in suitable designs. This allows suppliers to move beyond product sales toward durability-focused service models, potentially generating 400–700 basis points of gross-margin improvement compared with conventional admixture offerings.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Offshore energy concrete systems | +2.4% | EU, North Sea, East Asia, GCC | Medium term |

| Water utility retrofit lining | +1.9% | EU, India, MENA, North America | Short term |

| Repair-to-performance service model | +1.6% | North America core, EU, Australia | Short term |

| Precast tunnel and transit segments | +1.8% | India, China, EU, Middle East | Medium term |

| Code-ready crystalline admixture scale-up | +1.4% | EU, UK, North America | Short term |

| Roll-up of niche IP and applicators | +2.1% | EU, North America, Japan | Medium term |

Drivers

Aging bridge and transport infrastructure is emerging as a major demand driver for self-healing concrete because asset owners are increasingly prioritizing rehabilitation over full replacement. In the United States, the ASCE estimates a USD 373 billion bridge funding gap over the next 10 years, while FHWA bridge-condition reporting continues to highlight the scale of ongoing maintenance and preservation needs across existing transport networks.

This environment increases the value of materials that can slow chloride ingress, rebar corrosion, and crack propagation. Self-healing concrete is particularly attractive for bridge decks, tunnels, retaining walls, and underpasses, where traffic disruption, labor access, and recurring repair costs can outweigh the material premium.

As a result, procurement decisions are increasingly shifting from lowest upfront material cost toward minimizing total lifecycle intervention costs over 20–50-year operating periods, supporting broader adoption of self-healing concrete in infrastructure renewal projects.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging bridge and transport asset renewal | +2.4% | North America core, EU, Japan, Korea | Short term (≤ 2 years) |

| Carbon disclosure and low-carbon procurement in construction products | +2.1% | EU core, UK, Nordics, spill-over to APAC exporters | Short term (≤ 2 years) |

| Lifecycle cost savings over replacement-heavy maintenance models | +1.8% | North America, Western Europe, Gulf infrastructure hubs | Medium term (2–4 years) |

| Commercial maturation of bacterial and capsule-based healing systems | +1.6% | EU innovation clusters, Japan, Singapore, China pilot corridors | Medium term (2–4 years) |

| Climate resilience needs in tunnels, underpasses, marine and water assets | +1.5% | EU lowland regions, coastal APAC, Middle East, North America | Medium term (2–4 years) |

| Material-efficiency and reinforcement optimization in premium concrete systems | +1.2% | EU, advanced APAC, selective Middle East projects | Long term (≥ 4 years) |

Restraints

Code and certification gaps remain a significant barrier to self-healing concrete adoption because the industry still lacks harmonized design and acceptance frameworks across ASTM, EN, and project-specification standards. Different approaches, including autogenous healing, encapsulation-based systems, and bacterial mechanisms, continue to require project-specific validation rather than benefiting from universally recognized structural design guidance.

This results in prolonged qualification cycles, duplicate testing requirements, and additional engineering approvals that can extend pre-specification timelines by 6–18 months. The challenge is further intensified by Europe’s revised Construction Products Regulation, which entered into force in January 2025 and became more broadly applicable from January 2026, increasing requirements for technical and environmental documentation.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High system cost | −2.4% | EU, North America core, APAC premium projects | Short term (≤ 2 years) |

| Code/certification lag | −1.9% | EU, North America core, Japan, GCC | Medium term (2–4 years) |

| Specialty input volatility | −1.5% | EU, North America, import-reliant APAC | Short term (≤ 2 years) |

| Low-carbon mix conflict | −1.3% | EU core, UK, North America public works | Medium term (2–4 years) |

| Field execution risk | −1.2% | India, Southeast Asia, MENA, LATAM | Short term (≤ 2 years) |

| Proof-of-life data gap | −1.0% | Global | Long term (≥ 4 years) |

Geopolitical Impact Analysis

The self-healing concrete market is increasingly influenced by geopolitical factors, often more than is immediately visible within the construction industry. Many critical raw materials such as specialty polymers, bacterial nutrients, encapsulation agents, and chemical healing compounds are concentrated in a limited number of supplying countries, with China playing a key role in several upstream inputs.

As a result, any trade restrictions, export controls, or diplomatic tensions can quickly disrupt supply chains, leading to material shortages and higher production costs for manufacturers in regions such as North America and Europe. In response, companies are gradually shifting toward diversified sourcing strategies, although this transition is both time-consuming and cost-intensive in the short term.

At the same time, the Russia–Ukraine conflict has further strained global construction supply networks by impacting cement, steel reinforcement, and chemical additive flows, particularly across Eastern Europe. This disruption has also redirected public spending in parts of Europe toward defence and emergency infrastructure, temporarily slowing the adoption of advanced construction materials like self-healing concrete.

Regional Analysis

Asia Pacific dominates the global self-healing concrete market

Asia Pacific dominates the global self-healing concrete market with a 35.9% share, driven by the region’s massive and fast-growing construction activity, rapid urbanisation, and strong government commitment to building smarter and more durable public infrastructure. Countries like China, India, Japan, and the emerging economies of Southeast Asia are investing heavily in highways, tunnels, bridges, smart cities, and large-scale commercial developments, all of which are ideal application environments for self-healing concrete.

Government policies actively supporting green construction, combined with rising awareness of long-term maintenance cost savings, are pushing developers and infrastructure authorities across the region to increasingly specify advanced construction materials. China alone leads the Asia Pacific segment, backed by its enormous infrastructure development pipeline and government support for innovative construction technologies.

Europe is supported by strong sustainability regulations and deep-rooted research activity in bio-concrete technology, with Germany, the UK, and the Netherlands leading adoption driven by green building certification requirements and tightening environmental standards on construction materials.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global self-healing concrete market is dominated by a small group of large multinational construction material companies such as Holcim, Sika AG, BASF SE, and CEMEX that hold the majority of market share through strong research capabilities, global distribution networks, and long-established relationships with engineering firms and government procurement bodies.

These companies have the financial strength to manage lengthy product development cycles, navigate complex regulatory approvals, and invest in large-scale demonstration projects, giving them a commercialisation edge that smaller players find very difficult to match in a market where proven field performance and material certification are absolute requirements.

To capture this growth, tier-one manufacturers are shifting from simple material supply toward specialized engineering, particularly in capsule-based delivery technologies and embedded vascular networks. Larger players are increasingly choosing to acquire or partner with these specialists rather than build all capabilities in-house, a trend that is reshaping the competitive landscape and speeding up the commercialisation of next-generation self-healing technologies.

Key Players

- Sika AG

- BASF SE

- Basilisk

- CEMEX S.A.B. de C.V.

- Xypex Chemical Corporation

- Kryton International Inc.

- PENETRON

- Hycrete, Inc.

- GCP Applied Technologies

- Holcim

- Heidelberg Materials

- Wacker Chemie AG

- Acciona

- Devan Chemicals

- RPM International Inc.

- Others

Key Developments

- In January 2025, PolyU officially announced the development of its low-carbon marine self-healing concrete technology aimed at achieving carbon neutrality in coastal infrastructure, integrating biomineralisation and recycled waste aggregates for enhanced crack healing and sustainability.

- In November 2025, Xypex Chemical Corporation merged with a specialty polymer company focused on advanced encapsulation technologies, strengthening its capsule-based self-healing concrete capabilities with improved healing kinetics.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 143.6 Bn |

| Forecast Revenue (2035) | USD 2019.0 Bn |

| CAGR (2026–2035) | 30.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020–2024 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Intrinsic, Capsule-Based, and Vascular), By Installation (Infrastructure, Industrial, Commercial, and Residential), By Component (Bridges & Tunnels, Buildings, Roads & Highways, and Marine Structures), By Technology (Bacterial-Based, Microcapsule-Based, Polymer-Based, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC – China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America – Brazil, Mexico & Rest of Latin America; Middle East & Africa – GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Sika AG, BASF SE, Basilisk, CEMEX S.A.B. de C.V., Xypex Chemical Corporation, Kryton International Inc., PENETRON, Hycrete Inc., GCP Applied Technologies, Holcim, Heidelberg Materials, Wacker Chemie AG, Acciona, Devan Chemicals, RPM International Inc. |

| Customization Scope | Customization for segments and region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |