Quick Navigation

Report Overview

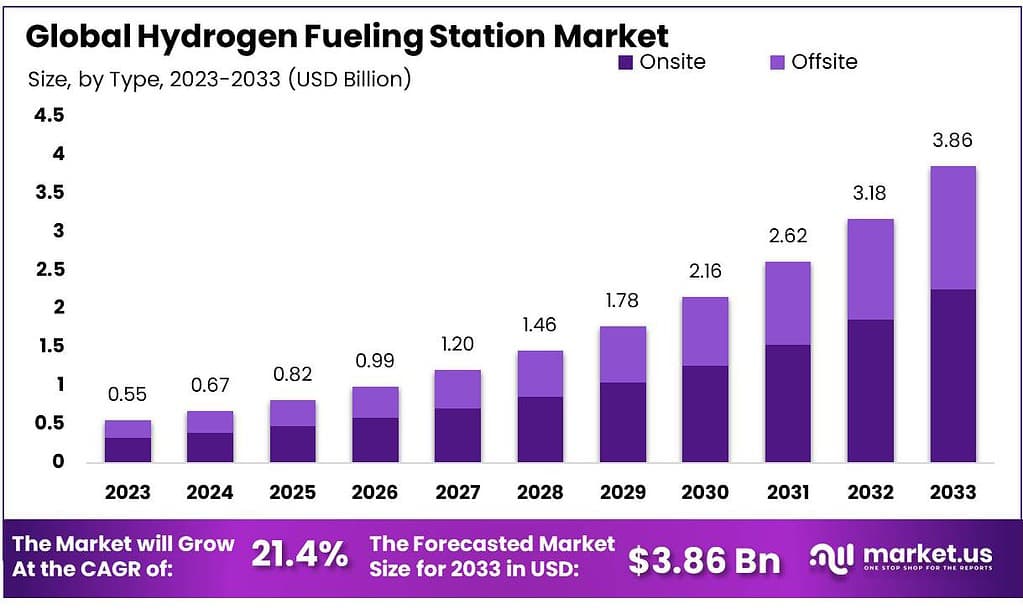

The global Hydrogen Fueling Station Market size is expected to be worth around USD 3.86 billion by 2033, from USD 0.55 billion in 2023, growing at a CAGR of 21.4% during the forecast period from 2023 to 2033.

The hydrogen fueling station market is witnessing significant growth driven by the global shift towards sustainable energy solutions and the increasing adoption of hydrogen-powered vehicles. As of recent data, there are approximately 700 hydrogen fueling stations worldwide, with projections indicating this number could increase substantially as countries intensify efforts to meet carbon neutrality goals. The market’s expansion is further bolstered by substantial investments from both public and private sectors aimed at enhancing hydrogen infrastructure.

For instance, the European Union has committed to expanding its hydrogen refueling infrastructure as part of its broader strategy to reduce greenhouse gas emissions by 55% by 2030. In the United States, federal funding initiatives like the Infrastructure Investment and Jobs Act allocate funds specifically for the development of clean hydrogen hubs, including fueling stations. Moreover, advancements in electrolysis technology are reducing the costs associated with hydrogen production, thereby making hydrogen fueling stations more economically viable.

However, challenges such as high operational costs and safety concerns related to hydrogen storage and handling continue to pose hurdles to rapid market expansion. Despite these obstacles, the hydrogen fueling station market is expected to grow at a compounded annual growth rate of over 20% in the next decade, driven by continuous technological advancements and increasing governmental support.

Key Takeaways

- Market Growth: Projected to expand from USD 0.55 billion in 2023 to USD 3.86 billion by 2033, growing at a CAGR of 21.4%.

- Type: Onsite stations dominate with over 58.6% share, valued for their convenience and efficiency.

- Pressure: High-pressure stations lead the market, capturing more than a 76.3% share

- Mobility: Fixed stations are predominant, capturing more than a 65.2% share

- Commercial vehicles are the largest segment, capturing more than a 44.6% share

- Asia Pacific leads with 63.6% market share in 2023,

By Type

In 2023, the hydrogen fueling station market was categorized into several types, including onsite, reforming, electrolysis, and offsite. Each segment has its specific dynamics and market share.

Onsite Hydrogen Fueling Stations primarily generate hydrogen directly at the point of dispensing. capturing more than a 58.6% share. This segment is characterized by its convenience and efficiency, as it eliminates the need for transport and reduces hydrogen degradation risks. Onsite stations are popular in locations with space constraints and where the safety and freshness of hydrogen are paramount.

Reforming Stations utilize reforming technologies to extract hydrogen from natural gas or other hydrocarbons. This type is favored for its cost-effectiveness and scalability. However, it’s less environmentally friendly compared to other methods due to CO2 emissions during the reforming process. These stations are common in areas with existing natural gas infrastructure.

Electrolysis Stations involve splitting water into hydrogen and oxygen through electrolysis. This segment is gaining traction due to its ability to produce green hydrogen when powered by renewable energy sources. It represents a growing market as industries and governments push for zero-emission hydrogen solutions. Electrolysis stations are particularly prevalent in regions with surplus renewable energy capacities.

Offsite Hydrogen Fueling Stations involve hydrogen production at a separate facility, from where it is then transported to the fueling station. This type is advantageous for economies of scale in hydrogen production and is typically used in larger networks with centralized production facilities. Offsite stations are essential in creating extensive hydrogen infrastructure networks, especially in densely populated urban areas.

By Pressure

In 2023, the hydrogen fueling station market was segmented by pressure into low pressure and high-pressure categories, each serving different operational needs and market demands.

High-Pressure Stations dominated the market, capturing more than a 76.3% share. These stations are essential for fueling modern hydrogen fuel cell vehicles, which typically require high-pressure hydrogen for efficient storage and extended range. High-pressure stations can compress hydrogen to pressures up to 700 bar, facilitating quicker refueling times and greater vehicle mileage. This segment’s growth is propelled by the increasing adoption of hydrogen-powered buses and trucks, particularly in regions aggressively pursuing decarbonization goals.

Low Pressure Stations, on the other hand, are typically used in smaller applications or in early-stage markets where the infrastructure for high pressure can be prohibitively expensive. Low-pressure systems, compressing hydrogen to around 350 bar or less, are simpler and less costly, making them suitable for smaller fleets or less frequent usage scenarios. Despite holding a smaller market share, this segment benefits from lower installation and maintenance costs, and it continues to serve an essential role in diverse market niches.

By Mobility

In 2023, the hydrogen fueling station market was segmented by mobility into fixed and mobile stations, each addressing distinct needs within the hydrogen infrastructure.

Fixed Hydrogen Stations held a dominant market position, capturing more than a 65.2% share. These stations are permanently installed and are a critical part of the hydrogen supply chain, serving as the backbone for hydrogen-powered transportation. Fixed stations are typically located in strategic locations such as urban centers, transportation hubs, and along major highways. Their stable presence allows for the reliable and consistent refueling necessary for daily commuters and commercial transport operations.

Mobile Hydrogen Stations, although smaller in market share, offer flexibility and are pivotal during the early stages of market development or in areas with low vehicle density. These stations can be relocated as needed, making them ideal for temporary applications, pilot projects, or to provide supplementary coverage in areas lacking fixed infrastructure. Mobile stations are also used at events or as backup systems to ensure continuity of service during maintenance or upgrades of fixed stations.

By End-Use

In 2023, the hydrogen fueling station market was segmented by end-use into marine, railways, commercial vehicles, and aviation, with each segment targeting specific transportation modes.

Commercial Vehicles held a dominant market position, capturing more than a 44.6% share. This segment includes buses, trucks, and utility vehicles that are increasingly adopting hydrogen fuel cell technology to meet emission regulations and reduce reliance on diesel. The widespread deployment of hydrogen fueling stations for commercial vehicles is driven by the need for long-haul transport solutions that can refuel quickly and cover long distances without emissions.

Marine end-use involves hydrogen fueling stations serving ships and ferries, particularly in coastal and inland waterways where reducing maritime emissions is a priority. Although smaller in market share, this segment is growing as ports and shipping companies invest in hydrogen technologies to comply with stricter environmental standards.

Railways are also transitioning to hydrogen as a clean alternative to diesel locomotives, especially in non-electrified routes. Hydrogen-powered trains offer a sustainable solution with minimal infrastructure change required, where hydrogen stations are set up along railway lines to support fuel cell trains.

Aviation uses hydrogen in experimental and small aircraft to achieve zero-emission flight, though this segment is in the early stages of development. The presence of hydrogen fueling stations at airports is key to supporting research and development of hydrogen-powered planes and potentially larger commercial deployments in the future.

Market Key Segments

By Type

- Onsite

- Reforming

- Electrolysis

- Offsite

By Pressure

- Low Pressure

- High Pressure

By Mobility

- Fixed Hydrogen Station

- Mobile Hydrogen Station

By End-Use

- Marine

- Railways

- Commercial Vehicles

- Aviation

Drivers

Government Incentives and Regulatory Support

One of the primary drivers of the hydrogen fueling station market is the robust support from government incentives and regulatory frameworks. Governments worldwide are implementing a variety of subsidies, tax rebates, and funding initiatives aimed at accelerating the deployment of hydrogen infrastructure to meet ambitious environmental targets and reduce greenhouse gas emissions. These policy measures are crucial as they lower the financial barriers to entry for new players and reduce the capital and operational expenditures for businesses involved in the development of hydrogen fueling stations.

For example, the European Union has incorporated hydrogen technology as a cornerstone of its strategy to achieve a climate-neutral economy by 2050. Significant funding has been directed towards innovation in hydrogen technologies and the development of widespread hydrogen refueling infrastructure through the Clean Hydrogen Partnership and other EU-funded programs. Similarly, in the United States, the federal government has introduced policies such as the Hydrogen and Fuel Cell Technologies Office’s funding programs which support hydrogen infrastructure as part of broader efforts to promote clean energy technologies.

These governmental initiatives not only provide direct financial assistance but also often include commitments to purchase hydrogen-powered vehicles for public transportation fleets, further stimulating market demand. For instance, California’s Zero-Emission Vehicle (ZEV) program mandates a certain percentage of new vehicle sales to be zero-emission by 2035, encouraging automotive manufacturers and consumers to adopt hydrogen technology.

Moreover, governments are actively working on setting up regulatory frameworks that ensure the safety and efficiency of hydrogen stations. Regulations regarding the storage, handling, and transportation of hydrogen are being standardized to boost public confidence and streamline the implementation across different regions. These regulations also help in addressing safety concerns associated with hydrogen, which is highly flammable, by establishing strict guidelines for station design and operation.

Additionally, international collaborations, such as the Hydrogen Energy Ministerial Meeting where multiple countries agree on cooperative initiatives to expand the global hydrogen market, are reinforcing the market driver. These agreements often result in synchronized policies that facilitate cross-border hydrogen infrastructure projects, enhancing the geographical reach of fueling stations and ensuring a steady expansion of the hydrogen economy.

The impact of these governmental efforts is evident in the growing number of hydrogen fueling stations and the increasing investment from the private sector. Companies are more willing to invest in hydrogen technologies when they perceive strong governmental commitment to supporting the industry. This results in a positive feedback loop, where public support encourages private investment, which in turn leads to more robust market growth, technological innovations, and eventually, a decrease in hydrogen fuel costs due to economies of scale and technological advancements.

Restraints

High Initial Costs and Infrastructure Challenges

A significant restraint impacting the growth of the hydrogen fueling station market is the high initial investment required for infrastructure development and the associated challenges. Establishing a hydrogen fueling station involves substantial capital outlay for various components such as land acquisition, construction, and the installation of specialized equipment for hydrogen production, storage, and dispensing. The technology for handling hydrogen, particularly at high pressures necessary for fueling modern hydrogen fuel cell vehicles, is complex and costly. These stations must also adhere to stringent safety and environmental regulations, further elevating the initial setup costs.

The infrastructure challenges extend beyond the stations themselves to include the supply chain for hydrogen. For hydrogen to be viable as a widespread fuel source, there needs to be a robust infrastructure not only for fuel but also for production and distribution. Hydrogen can be produced using various methods, including natural gas reforming and water electrolysis, each with its own set of infrastructure requirements and cost implications. The distribution of hydrogen, whether via pipelines, trucks, or other means, requires investment in new logistics solutions or the conversion of existing systems, which is an expensive and technically challenging process.

Moreover, the return on investment (ROI) for hydrogen fueling stations is currently less predictable and generally slower than that for more established fueling options like gasoline or electric charging stations. This uncertainty in ROI discourages many potential investors and delays the development of new stations. The limited number of hydrogen-powered vehicles currently on the roads compounds this problem, as the demand for hydrogen fueling services is still developing, leading to lower utilization rates of existing hydrogen stations and further stretching the timeline for profitability.

Additionally, the lack of standardized technologies across different regions and manufacturers adds another layer of complexity and cost. Different countries and companies may adopt diverse technologies for hydrogen production, storage, and dispensing, leading to a fragmented market that hinders large-scale deployment and interoperability of hydrogen fueling infrastructure. This lack of standardization can lead to inefficiencies and increased costs for maintenance and operation, as specialized skills and equipment are needed to handle the different technologies.

The competitive landscape also presents challenges. Hydrogen fueling infrastructure must compete with well-established fossil fuel stations and rapidly expanding electric vehicle charging networks. Governments and businesses may find it more cost-effective to invest in these existing technologies rather than in hydrogen, particularly in regions where the regulatory and consumer push towards hydrogen is weaker.

Despite these challenges, the hydrogen fueling station market has potential pathways for growth. Technological advancements and economies of scale can reduce costs over time, and stronger regulatory and financial incentives from governments can improve the business case for hydrogen. Furthermore, as the environmental impact of other fuels becomes increasingly untenable, hydrogen may receive more attention as a cleaner alternative, which could shift market dynamics favorably.

Opportunity

Expansion into Emerging Markets and Integration with Renewable Energy

A major opportunity for the hydrogen fueling station market lies in its potential expansion into emerging markets, coupled with the integration of hydrogen production with renewable energy sources. As countries around the world increasingly focus on reducing carbon emissions and promoting cleaner energy alternatives, hydrogen is being recognized as a pivotal element in the energy transition. This recognition is particularly evident in emerging economies, where rapid industrialization and urbanization are driving demand for sustainable energy solutions.

Emerging markets present a unique opportunity for the deployment of hydrogen fueling stations due to their growing economic development and increased investment in infrastructure. These regions often have less entrenched fossil fuel infrastructure, which reduces barriers to adopting new technologies such as hydrogen. Moreover, governments in these areas are looking to improve air quality and reduce reliance on imported oil, positioning hydrogen as an attractive alternative. Incentives such as tax benefits, subsidies, and favorable regulations can accelerate the establishment of hydrogen infrastructure in these markets.

Integrating hydrogen production with renewable energy sources offers another significant opportunity. By using electricity generated from wind, solar, or hydroelectric power to produce hydrogen through water electrolysis, the process becomes entirely clean, producing no carbon emissions. This “green” hydrogen is increasingly seen as a key component of a sustainable energy future. As the costs of renewable energy continue to decrease and technologies improve, the economic feasibility of producing green hydrogen improves, making it more accessible and appealing.

The synergistic relationship between hydrogen fueling stations and renewable energy can also stimulate local economies. For example, regions with high potential for solar or wind energy can leverage these resources to produce hydrogen locally, reducing energy import costs and creating jobs in both renewable energy and hydrogen infrastructure sectors. This approach also helps stabilize the grid and manage the intermittency issues associated with renewable energy sources.

Furthermore, the use of hydrogen extends beyond transportation. It can serve as a storage medium for excess renewable energy, help decarbonize industrial processes, and be used for heating in residential and commercial buildings. These applications broaden the potential market for hydrogen and, by extension, for hydrogen fueling stations.

To capitalize on these opportunities, stakeholders in the hydrogen fueling station market need to engage in strategic partnerships with renewable energy providers, technology firms, and local governments. Such collaborations can facilitate the sharing of technology, resources, and expertise, thereby accelerating the deployment of hydrogen stations and the integration with renewable energy systems.

Trends

Technological Advancements in Hydrogen Fueling Technologies

A significant trend in the hydrogen fueling station market is the rapid technological advancements in fueling technologies that enhance efficiency, reduce costs, and improve safety. These innovations are vital for accelerating the adoption of hydrogen as a mainstream fuel option and are shaping the future of the hydrogen economy.

One of the key advancements is the development of high-capacity, high-throughput hydrogen dispensers that can refuel vehicles as quickly as conventional gasoline pumps. This is crucial for commercial viability, as one of the traditional drawbacks of hydrogen fueling has been the longer refueling times compared to diesel or gasoline. Modern systems have significantly reduced these times, offering refueling speeds that are competitive with traditional fuels, thereby improving consumer convenience and operational efficiency.

Another important technological trend is the improvement in hydrogen storage systems at fueling stations. Advanced materials and compression techniques are now being employed to store larger amounts of hydrogen at higher pressures. This increases the fueling capacity of each station and extends the range of hydrogen vehicles, making them more practical for everyday use and long-haul transport. For instance, innovations in solid-state hydrogen storage technology offer safer and more energy-dense alternatives to traditional high-pressure gas storage.

Furthermore, the integration of digital technologies into hydrogen stations is enhancing operational efficiencies and user experiences. Technologies such as Internet of Things (IoT) sensors and smart management systems are being implemented to monitor and optimize fuel dispensing, maintenance, and safety processes. These systems provide real-time data analytics, helping station operators to maintain the integrity of the fuel, predict maintenance needs, and manage inventories efficiently.

Another trend is the development of modular and scalable hydrogen fueling stations. These modular stations can be easily expanded or adapted based on demand and are particularly useful in emerging markets or for temporary installations. The scalability of such stations allows for a more flexible and economically feasible deployment, facilitating broader market penetration and adaptation to varying regional needs.

In addition, the push for greener hydrogen production methods at the point of refueling is gaining traction. On-site hydrogen production through water electrolysis, powered by renewable energy sources, is becoming more common. This not only reduces the carbon footprint associated with hydrogen production but also cuts down on logistics costs and complexities related to hydrogen transport.

As these technological advancements continue, the cost of hydrogen fuel production, storage, and dispensation is expected to decrease, making hydrogen fuel stations more attractive to investors and consumers alike. Moreover, these innovations contribute to making hydrogen a safer and more reliable energy source, which is essential for gaining public trust and regulatory approval.

Regional Analysis

In 2023, the Asia Pacific region secured its position as the leading market for hydrogen fueling stations, achieving a significant market share of 63.6%. This dominance is largely driven by the region’s swift industrialization, particularly noticeable in countries like China, India, and Japan. The rapid industrial growth has boosted the demand for hydrogen fueling stations across multiple sectors, including transportation, industrial manufacturing, and urban infrastructure.

The region’s development trajectory is further propelled by large-scale infrastructure projects, where hydrogen fueling stations are crucial for supporting clean energy transportation initiatives and reducing urban pollution. Moreover, there is an increasing focus on sustainability and environmental preservation, which has spurred the adoption of hydrogen technologies throughout the region. This shift is in line with global movements towards reducing reliance on fossil fuels and minimizing environmental degradation.

Additionally, supportive government policies and significant investments in infrastructure development are key factors driving the growth of the hydrogen fueling station market in the Asia Pacific. These efforts not only enhance the efficiency of energy use in industrial applications but also promote the broader adoption and sustainability of hydrogen infrastructure in the region.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In the burgeoning Hydrogen Fueling Station market, key players play pivotal roles in shaping industry dynamics, driving innovation, and fostering market growth. These players, equipped with diverse capabilities and strategic initiatives, are instrumental in advancing the adoption of hydrogen as a clean energy source for transportation.

Market Key Players

- Air Liquide

- Air Products and Chemicals Inc.

- Linde plc

- Nel ASA

- FuelCell Energy Inc.

- ITM Power plc

- McPhy Energy

- sera GmbH

- China Petrochemical Corporation

- Ballard Power Systems

- TotalEnergies

Recent Developments

In 2023, Air Liquide significantly advanced its position in the hydrogen fueling station market through strategic collaborations and the development of new infrastructure across Europe.

September 2023 FuelCell Energy Inc., uniquely produces renewable electricity, hydrogen, and water from directed biogas. This facility is notable for its capacity to generate up to 1,200 kg/day of hydrogen, which not only supports Toyota’s logistic needs at the port but also supplies an adjacent heavy-duty hydrogen refueling station.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 0.55 Bn |

| Forecast Revenue (2033) | US$ 3.86 BN |

| CAGR (2024-2033) | 21.4% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type(Onsite, Reforming, Electrolysis, Offsite), By Pressure(Low Pressure, High Pressure), By Mobility(Fixed Hydrogen Station, Mobile Hydrogen Station), By End-Use(Marine, Railways, Commercial Vehicles, Aviation) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Air Liquide, Air Products and Chemicals Inc., Linde plc, Nel ASA, FuelCell Energy Inc., ITM Power plc, McPhy Energy, sera GmbH, China Petrochemical Corporation, Ballard Power Systems, TotalEnergies |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

Hydrogen Fueling Station Market size is expected to be worth around USD 3.86 Bn by 2033

The Hydrogen Fueling Station Market is expected to grow at 21.4% CAGR (2023-2033).

Air Liquide, Air Products and Chemicals Inc., Linde plc, Nel ASA, FuelCell Energy Inc., ITM Power plc, McPhy Energy, sera GmbH, China Petrochemical Corporation, Ballard Power Systems, TotalEnergies