Global Electronic Stethoscope Market By Product Type (Digital and Amplified), By Technology (Integrated Chest-Piece, Wireless Transmission and Others), By Connectivity (Wired, Wi-Fi and Bluetooth), By End-User (Hospitals & Clinics, Ambulatory Surgery Centers and Other), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179131

- Number of Pages: 324

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

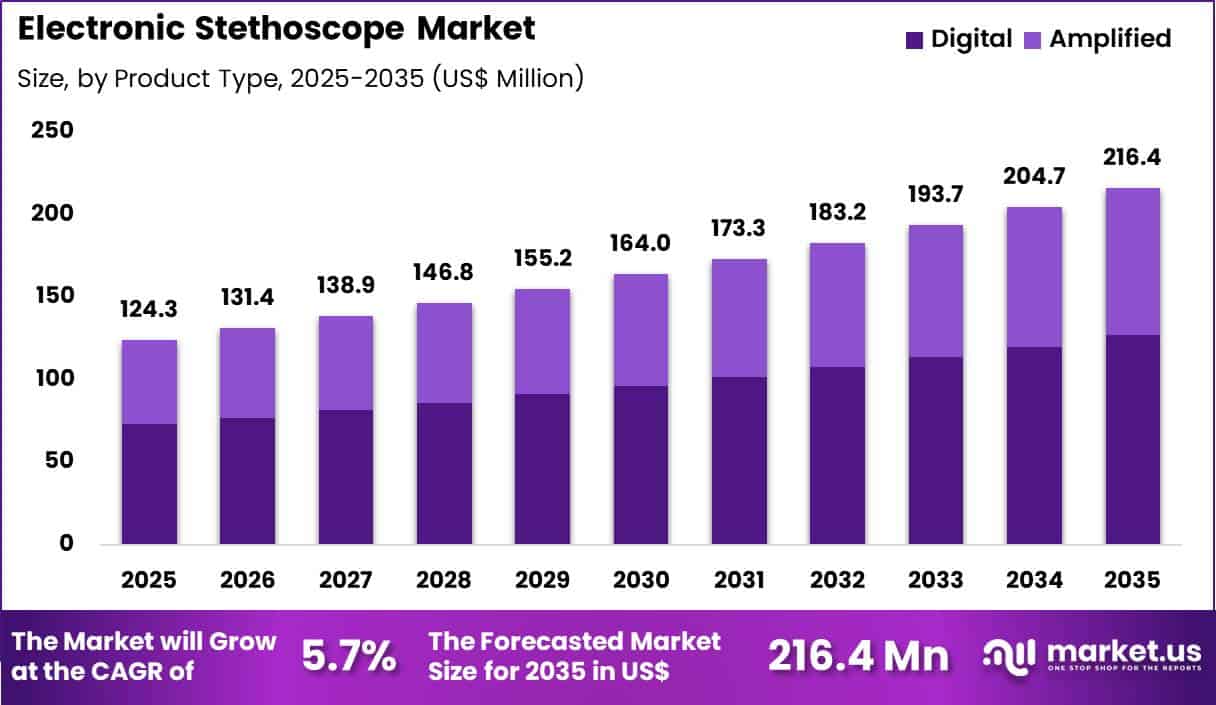

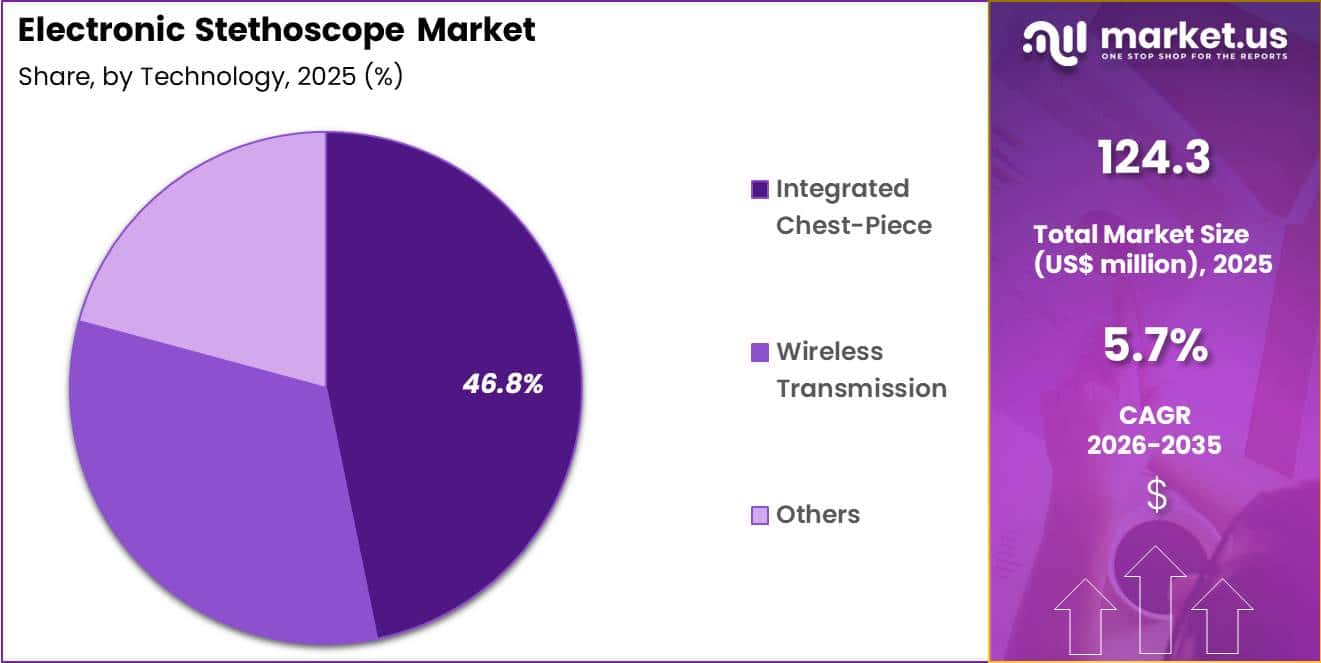

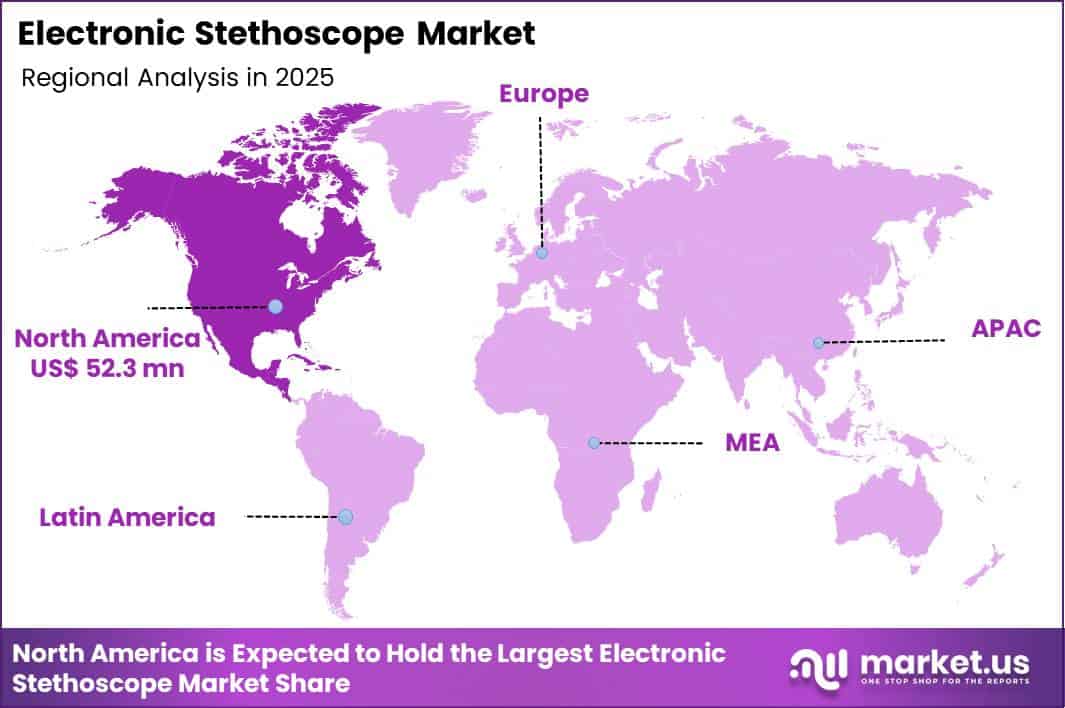

The Global Electronic Stethoscope Market size is expected to be worth around US$ 216.4 Million by 2035 from US$ 124.3 Million in 2025, growing at a CAGR of 5.7% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 42.1% share with a revenue of US$ 52.3 Million.

Increasing adoption of digital health technologies propels the electronic stethoscope market as clinicians seek enhanced auscultation capabilities that overcome limitations of traditional acoustic devices. Cardiologists increasingly employ electronic stethoscopes with amplification and noise reduction features to detect subtle murmurs and gallops in obese patients or noisy environments, improving diagnostic confidence during cardiac evaluations.

These devices support pulmonology applications by filtering ambient sounds to isolate crackles, wheezes, and diminished breath sounds in patients with chronic obstructive pulmonary disease or pneumonia. Primary care physicians utilize electronic stethoscopes with recording functionality to document abnormal heart or lung sounds, enabling secure sharing with specialists for second opinions or longitudinal monitoring.

Telemedicine practitioners apply Bluetooth-enabled models to transmit high-fidelity audio during virtual consultations, facilitating remote assessment of valvular disease or respiratory infections. Pediatricians benefit from electronic stethoscopes with adjustable frequency modes that enhance detection of congenital heart defects and pediatric lung pathologies in young children.

Manufacturers pursue opportunities to integrate artificial intelligence algorithms that provide automated interpretation of heart and lung sounds, expanding applications in high-volume screening programs and primary care settings.

Developers advance wireless connectivity and cloud storage features that allow seamless integration with electronic health records, broadening utility in multidisciplinary care teams managing complex chronic conditions. These innovations facilitate real-time collaboration during tele-auscultation, supporting remote training and expert consultation in underserved clinical environments.

Opportunities emerge in wearable electronic stethoscope patches for continuous monitoring of cardiac and respiratory parameters in post-operative recovery. Companies invest in ergonomic designs with extended battery life and antimicrobial surfaces to enhance usability and infection control.

Recent trends emphasize AI-assisted anomaly detection and multi-parameter integration with pulse oximetry, positioning electronic stethoscopes as essential tools in modern diagnostic workflows focused on accuracy, efficiency, and patient-centered care.

Key Takeaways

- In 2025, the market generated a revenue of US$ 124.3 million, with a CAGR of 5.7%, and is expected to reach US$ 216.4 million by the year 2035.

- The product type segment is divided into digital and amplified, with digital taking the lead with a market share of 58.7%.

- Considering technology, the market is divided into integrated chest-piece, wireless transmission and others. Among these, integrated chest-piece held a significant share of 46.8%.

- Furthermore, concerning the connectivity segment, the market is segregated into wired, wi-fi and bluetooth. The wired sector stands out as the dominant player, holding the largest revenue share of 44.6% in the market.

- The end-user segment is segregated into hospitals & clinics, ambulatory surgery centers and other, with the hospitals & clinics segment leading the market, holding a revenue share of 52.9%.

- North America led the market by securing a market share of 42.1%.

Product Type Analysis

Digital electronic stethoscopes accounted for 58.7% of growth within product type and led the electronic stethoscope market due to enhanced sound amplification and recording capabilities. Clinicians prefer digital devices because they offer noise reduction, frequency filtering, and sound visualization features. These tools improve detection of subtle cardiac and pulmonary abnormalities. Integration with electronic health records supports documentation and long-term patient monitoring.

Growth strengthens as telemedicine and remote consultations expand. Digital models enable physicians to record and share auscultation data for second opinions and training. Continuous improvement in signal processing technology enhances diagnostic accuracy.

Rising focus on early detection of cardiovascular and respiratory disorders further supports adoption. The segment is expected to remain dominant as healthcare providers prioritize data-driven and connected diagnostic tools.

Technology Analysis

Integrated chest-piece technology generated 46.8% of growth within technology and emerged as the leading segment due to compact design and improved acoustic sensitivity. Manufacturers design integrated systems to optimize diaphragm and sensor alignment, which enhances sound clarity. Clinicians value ergonomic construction that supports prolonged clinical use. The unified design reduces mechanical noise and improves consistency across patient assessments.

Growth accelerates as hospitals adopt advanced devices that combine acoustic precision with digital conversion. Improved durability and battery efficiency increase device reliability. Integration of high-quality sensors strengthens performance in noisy clinical environments. Ongoing innovation in material engineering enhances acoustic fidelity. The segment is projected to maintain leadership as demand for precise and user-friendly diagnostic instruments increases.

Connectivity Analysis

Wired connectivity contributed 44.6% of growth within connectivity and led the electronic stethoscope market due to stable signal transmission and data security. Healthcare institutions prioritize wired systems to ensure uninterrupted audio quality during examinations. Wired connections reduce latency and interference in busy hospital settings. Institutions also favor controlled data transfer pathways to comply with privacy standards.

Growth continues as many hospitals maintain structured IT environments that support secure wired integration. Wired devices require minimal configuration and reduce dependency on wireless infrastructure. Clinical workflows benefit from reliable plug-and-use functionality. Budget considerations further encourage adoption in cost-sensitive facilities. The segment is anticipated to sustain dominance as reliability and data integrity remain central to clinical diagnostics.

End-User Analysis

Hospitals and clinics accounted for 52.9% of growth within end-user and dominated the electronic stethoscope market due to high patient volumes and diagnostic demand. Physicians use electronic stethoscopes across cardiology, pulmonology, and general medicine departments. Hospitals invest in advanced diagnostic tools to improve early detection and treatment outcomes. Central procurement strategies support standardized equipment deployment.

Growth strengthens as healthcare systems emphasize preventive screening and digital health integration. Teaching hospitals incorporate electronic auscultation into medical training programs. Increasing incidence of respiratory and cardiovascular disorders further raises device utilization.

Clinical research initiatives also expand equipment adoption. The segment is expected to remain the primary growth driver as hospitals continue to prioritize advanced and connected diagnostic technologies.

Key Market Segments

By Product Type

- Digital

- Amplified

By Technology

- Integrated Chest-Piece

- Wireless Transmission

- Others

By Connectivity

- Wired

- Wi-Fi

- Bluetooth

By End-User

- Hospitals & Clinics

- Ambulatory Surgery Centers

- Other

Drivers

Increasing prevalence of cardiovascular and respiratory diseases is driving the market.

The rising incidence of cardiovascular and respiratory conditions globally has significantly increased the demand for electronic stethoscopes, which provide amplified sound and digital recording capabilities for improved diagnostic accuracy. Enhanced clinical awareness and routine screening programs have led to more frequent auscultation needs in primary and specialty care.

Healthcare providers are adopting electronic stethoscopes to detect subtle murmurs and adventitious sounds that may be missed with acoustic instruments. The correlation between aging populations and higher disease burden further amplifies the requirement for reliable cardiac and pulmonary assessment tools.

Government health agencies consistently report cardiovascular diseases as the leading cause of death, underscoring the need for advanced diagnostic aids. Electronic stethoscopes enable noise reduction and sound visualization, supporting better documentation and consultation. National health priorities emphasize preventive cardiology and pulmonology, promoting the integration of digital auscultation devices.

Key manufacturers are developing models with Bluetooth connectivity to align with this clinical demand. This driver sustains investment in electronic stethoscope technology across hospitals and outpatient settings. According to the World Health Organization, an estimated 19.8 million people died from cardiovascular diseases in 2022, representing approximately 32% of all global deaths.

Restraints

High cost of electronic stethoscopes compared to traditional models is restraining the market.

The significantly higher purchase price of electronic stethoscopes compared to conventional acoustic stethoscopes restricts their adoption in cost-sensitive healthcare facilities. Advanced components such as amplifiers, digital processors, and rechargeable batteries contribute to elevated manufacturing expenses. Many primary care clinics and public hospitals continue using traditional stethoscopes due to budget limitations.

Regulatory requirements for electrical safety and performance testing add to the total acquisition cost. In low-resource settings, these expenses often lead to reliance on basic acoustic instruments despite reduced functionality. Providers frequently defer upgrades to avoid capital expenditure on premium devices. This restraint is particularly evident in developing regions with constrained healthcare funding.

Industry efforts to introduce entry-level electronic models have progressed slowly. Despite superior sound quality and recording features, the cost differential slows replacement cycles. The high cost of electronic stethoscopes relative to traditional models remains a primary market restraint.

Opportunities

Rapid growth of telehealth and remote patient monitoring is creating growth opportunities.

The accelerating adoption of telehealth platforms and remote cardiac monitoring programs creates substantial potential for electronic stethoscopes with digital transmission capabilities. Governmental policies supporting virtual care reimbursement have expanded the use of connected diagnostic tools in home and ambulatory settings.

Patients with chronic heart and lung conditions increasingly require remote auscultation during virtual consultations. Partnerships between telehealth providers and stethoscope manufacturers facilitate seamless audio streaming integration. The large population of patients with known cardiac arrhythmias magnifies demand for remote-compatible electronic stethoscopes.

Educational initiatives for primary care physicians promote the use of digital auscultation in telemedicine workflows. This opportunity allows manufacturers to develop Bluetooth-enabled models optimized for virtual examinations. Leading companies are establishing collaborations with telehealth networks to capture market share.

Overall, telehealth expansion aligns with efforts to improve access to specialist care without in-person visits. The number of Medicare telehealth visits for cardiac conditions grew significantly between 2022 and 2024, reflecting this shift toward remote monitoring.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions influence the electronic stethoscope market through healthcare spending trends, clinic level procurement decisions, and investment in digital health tools. Inflation increases costs for sensors, microphones, circuit boards, and connectivity modules, which raises production and retail prices. Higher interest rates reduce discretionary capital spending by smaller practices, which slows replacement of conventional devices with digital alternatives.

Geopolitical tensions disrupt semiconductor supply chains and electronic component sourcing, creating lead time uncertainty and pricing variability. Current US tariffs on imported electronic assemblies and finished medical devices increase landed costs and pressure vendor margins. These financial constraints can delay adoption in price sensitive markets and limit expansion by emerging brands.

At the same time, healthcare providers prioritize telemedicine integration and remote auscultation capabilities to improve patient access. Strong demand for connected diagnostic tools and enhanced acoustic performance continues to support long term growth prospects.

Latest Trends

Integration of artificial intelligence for automated sound analysis is a recent trend in the market.

In 2024, the incorporation of artificial intelligence algorithms in electronic stethoscopes has advanced automated interpretation of heart and lung sounds for preliminary diagnostic support. These systems utilize machine learning models trained on large datasets of annotated auscultatory recordings to identify murmurs, wheezes, and other abnormalities.

Manufacturers have prioritized regulatory clearance for AI modules to ensure clinical reliability. Clinical evaluations in 2024 demonstrated improved detection rates for subtle cardiac pathologies. Eko Health received FDA clearance in 2024 for its AI-powered low ejection fraction detection feature integrated into its CORE series electronic stethoscopes. This development supports early identification of heart failure in primary care settings.

The trend emphasizes seamless integration with electronic health records for immediate clinical decision support. Regulatory pathways have evolved to accommodate validated AI features in diagnostic devices. Industry collaborations continue to refine algorithms for diverse patient populations. These innovations aim to enhance diagnostic consistency while addressing physician workload challenges in busy clinical environments.

Regional Analysis

North America is leading the Electronic Stethoscope Market

North America held a 42.1% share of the Electronic Stethoscope market in 2024, driven by the rapid shift toward digitally enabled clinical assessment tools. Healthcare systems prioritized devices that amplify subtle heart and lung sounds, improving diagnostic confidence in busy emergency and primary care environments. The rise of hybrid care models encouraged physicians to adopt connected auscultation tools that transmit real time audio during virtual visits.

Increasing burden of cardiovascular and pulmonary disorders reinforced the need for accurate bedside evaluation technologies. Hospitals also focused on documentation capabilities, using recording features for training, quality review, and second opinions. Integration with secure cloud platforms enhanced collaboration between specialists and frontline providers.

A credible supporting indicator comes from the American Heart Association, which reported in 2023 that nearly 48% of US adults have some form of cardiovascular disease, highlighting the sustained clinical demand for advanced auscultation solutions.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

The Electronic Stethoscope market in Asia Pacific is expected to expand consistently during the forecast period as healthcare systems modernize diagnostic infrastructure. Governments strengthen primary healthcare networks and promote digital tools that improve early disease detection. Clinicians increasingly rely on connected listening devices to support teleconsultations across remote and underserved communities.

Rapid expansion of mobile broadband networks enables seamless audio transmission and data sharing. Medical colleges upgrade simulation labs with advanced auscultation technology to improve student training. Private healthcare chains adopt smart diagnostic equipment to enhance patient experience and clinical precision.

A verifiable signal of regional need appears in 2023 data from the International Telecommunication Union, which reported continued growth in mobile broadband subscriptions across Asia Pacific, reinforcing the digital backbone that supports expansion of connected medical devices.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key competitors in the electronic stethoscope market grow by improving acoustic amplification, noise-cancellation technology, and digital signal processing that help clinicians detect subtle cardiac and pulmonary sounds with greater precision.

They also strengthen value propositions by integrating Bluetooth connectivity and mobile app compatibility that support telemedicine, remote diagnostics, and longitudinal patient tracking. Firms pursue strategic partnerships with medical schools, healthcare systems, and telehealth platforms to embed their solutions into training programs and routine clinical workflows, expanding adoption across point-of-care settings.

Geographic expansion into North America, Europe, and high-growth Asia Pacific diversifies revenue and captures demand driven by rising chronic disease prevalence and remote care initiatives. 3M Littmann, a leading global stethoscope brand under 3M Company, pairs decades-long acoustic expertise with digital enhancements and extensive clinician support resources that align product performance with professional needs.

The company advances its competitive agenda through disciplined investment in research and design, strategic collaborations that extend interoperability, and a customer-centric commercialization strategy that connects innovation with evolving clinical priorities.

Top Key Players

- 3M

- Eko Health

- Thinklabs Medical

- Cardionics

- Welch Allyn

- ADC

- American Diagnostic Corporation

- Prestige Medical

- HD Medical

- Rudolf Riester

Recent Developments

- In April 2025, Eko Health began direct online sales of its CORE 500 Digital Stethoscope in the United Kingdom. The move reflects growing acceptance of AI-enabled auscultation tools among UK regulators and healthcare procurement bodies, supporting broader adoption of advanced digital diagnostic devices.

- In June 2023, the US Food and Drug Administration granted clearance for Eko’s CORE 500 stethoscope, which integrates a three-lead ECG system. The approval highlights the integration of traditional acoustic examination with electrical cardiac monitoring within a single handheld diagnostic platform.

Report Scope

Report Features Description Market Value (2025) US$ 124.3 Million Forecast Revenue (2035) US$ 216.4 Million CAGR (2026-2035) 5.7% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape 3M, Eko Health, Thinklabs Medical, Cardionics, Welch Allyn, ADC, American Diagnostic Corporation, Prestige Medical, HD Medical, Rudolf Riester Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Electronic Stethoscope MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Electronic Stethoscope MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- 3M

- Eko Health

- Thinklabs Medical

- Cardionics

- Welch Allyn

- ADC

- American Diagnostic Corporation

- Prestige Medical

- HD Medical

- Rudolf Riester

Our Clients

- 179131

- Feb 2026