Quick Navigation

Report Overview

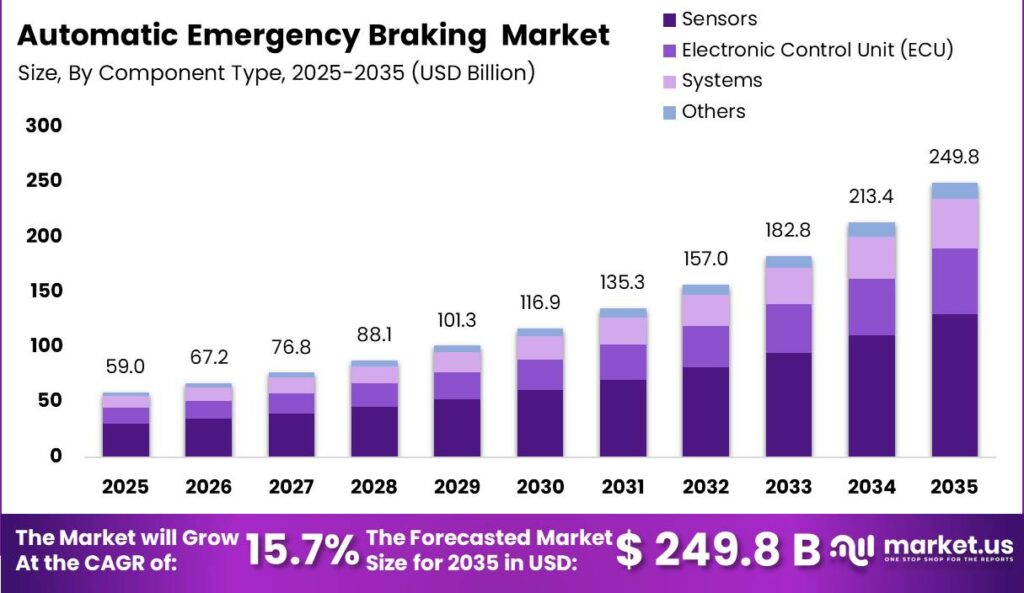

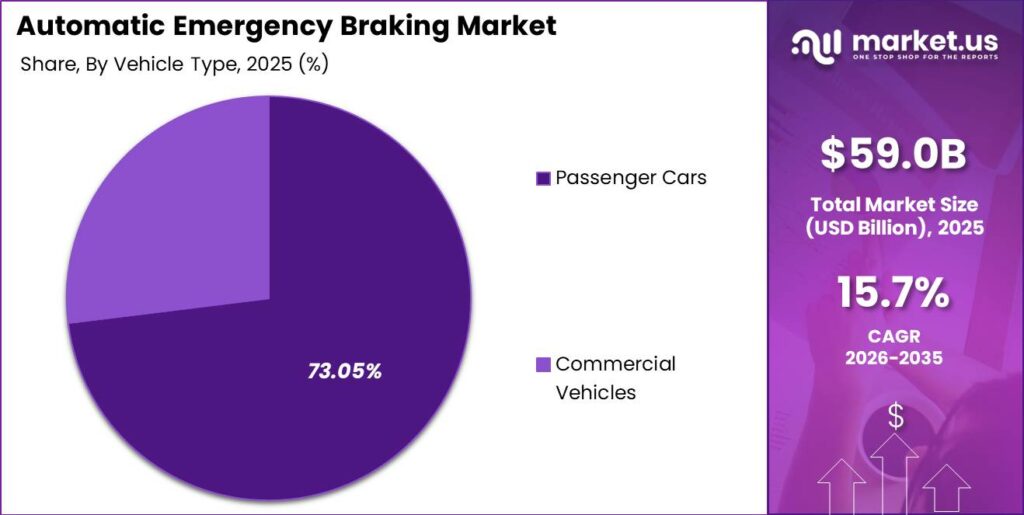

Global Automatic Emergency Braking Market size is expected to be worth around USD 249.8 Billion by 2035 from USD 59.0 Billion in 2025, growing at a CAGR of 15.7% during the forecast period 2026 to 2035.

Automatic emergency braking combines forward sensing, perception software, electronic control units, warning logic, and braking intervention to reduce or avoid imminent collisions. The market spans sensors, ECUs, integrated safety systems, passenger and commercial vehicles, and OEM or retrofit sales channels. Therefore, supplier competitiveness depends on achieving regulatory-grade performance at automotive scale while controlling sensor and validation costs.

Key Takeaways

- Market value reaches USD 59.0 Billion in 2025 and is forecast to reach USD 249.8 Billion by 2035

- The market records a CAGR of 15.7% from 2026 to 2035

- Sensors lead the component segment with a 52.00% share

- Passenger cars lead the vehicle-type segment with a 73.05% share

- OEM and factory-fitted systems account for a 75.00% sales-channel share

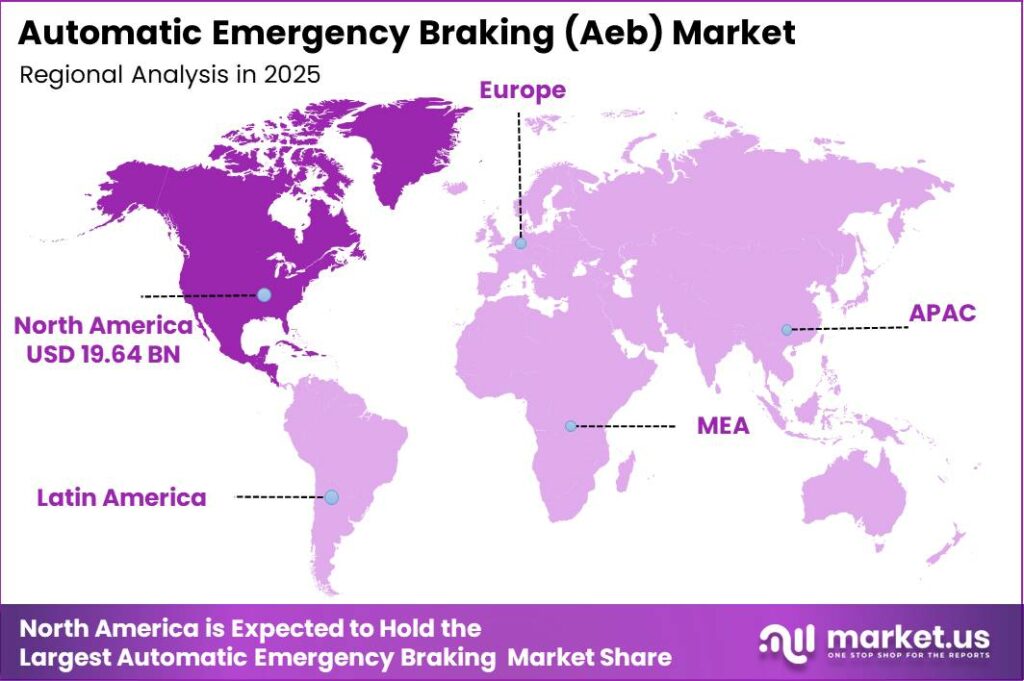

- North America leads the regional market with a 33.30% share, valued at USD 19.64 Billion

Regulation is converting AEB from an optional ADAS function into a baseline vehicle requirement. NHTSA’s FMVSS No. 127 requires AEB, pedestrian AEB, and forward-collision warning on nearly all new U.S. light vehicles by September 2029, including lead-vehicle avoidance testing up to 62 mph and pedestrian detection in daylight and darkness. This creates long-cycle sourcing visibility for sensor, software, ECU, and brake-system suppliers.

System effectiveness supports broader adoption across safety-led vehicle platforms. The PARTS study found newer AEB-equipped vehicles, from model years 2021 to 2023, reduced front-to-rear crashes by 52%, compared with 46% for model years 2015 to 2017. This signals that perception upgrades and sensor fusion can support premium pricing where measurable safety performance improves.

Component Analysis

Sensors dominate with 52.00% due to mandatory perception performance requirements.

In 2025, Sensors held a dominant market position in the Component segment of the Automatic Emergency Braking Market, with a 52.00% share. Radar, LiDAR, and camera systems provide the vehicle’s forward-scene awareness before braking decisions occur. NHTSA requires lead-vehicle collision avoidance up to 62 mph and automatic braking when a crash is imminent up to 90 mph. This makes sensing performance a central design and sourcing priority.

Electronic Control Units held a 24.00% share, making them the key decision layer between perception data and brake intervention. ECU demand rises as AEB systems process multi-sensor inputs, classify objects, and execute time-critical braking commands. The PARTS analysis evaluated 98 million vehicles and 21.2 million police-reported crashes, demonstrating the scale of real-world data needed for algorithm validation. Suppliers with validated compute platforms can win broader ADAS integration programs.

Integrated systems represented 18.00% of the component market, covering functions such as Forward Collision Warning, Crash Imminent Braking, and Dynamic Brake Support. These packaged systems simplify OEM integration by combining warnings, actuation logic, and diagnostic functions. NHTSA’s standard requires AEB, pedestrian AEB, and forward-collision warning together for nearly all U.S. light vehicles. This favors suppliers able to deliver validated, vehicle-ready modules rather than isolated components.

Other components accounted for the remaining 6.00% share, including supporting wiring, interfaces, housings, and ancillary electronics. These elements remain commercially relevant because AEB adoption converts numerous safety-related subcomponents into recurring factory-fit content. Euro NCAP reported that 98% of models assessed in 2025 achieved four stars or higher. Higher safety-rating expectations reinforce the need for dependable supporting hardware across mass-market programs.

Vehicle Type Analysis

Passenger Cars dominate with 73.05% due to extensive light-vehicle fitment requirements.

In 2025, Passenger Cars held a dominant market position in the Vehicle Type segment of the Automatic Emergency Braking Market, with a 73.05% share. Hatchbacks, sedans, SUVs, crossovers, and MPVs form the primary volume base for standardized AEB installations. FMVSS No. 127 applies to nearly all U.S. light vehicles with a gross vehicle weight rating of 10,000 pounds or less. This broad legal coverage anchors high-volume OEM demand.

Commercial Vehicles accounted for 26.95% of the market across light commercial vehicles and heavy commercial vehicles. Fleet buyers value AEB because reduced front-to-rear collisions can protect vehicle availability, operating continuity, and liability outcomes. PARTS reported that AEB reduced front-to-rear crashes by 49% across the studied model years. This performance evidence strengthens the business case for fleet safety packages and retrofit-oriented solutions.

Sales Channel / Fitment Type Analysis

OEM / Factory-Fitted dominates with 75.00% due to vehicle-platform compliance integration.

In 2025, Original Equipment Manufacturer and Factory-Fitted systems held a dominant market position in the Sales Channel / Fitment Type segment of the Automatic Emergency Braking Market, with a 75.00% share. OEM integration enables sensor placement, ECU calibration, brake compatibility, and validation during vehicle development. NHTSA requires covered manufacturers to meet the standard for vehicles manufactured on or after September 1, 2029. Factory fitment therefore remains the principal compliance route.

Aftermarket retrofit systems held the remaining 25.00% share and address installed fleets that lack factory-integrated AEB. This channel depends on practical installation, dependable calibration, and alignment with fleet operating environments. The PARTS study found pedestrian AEB reduced single-vehicle frontal crashes involving non-motorists by 9%. Retrofit providers can use measurable risk reduction to position systems with commercial fleets and insurers.

Key Market Segments

By Component

- Sensors

- Radar Sensors

- LiDAR Sensors

- Camera / Vision Sensors

- Others

- Electronic Control Unit (ECU)

- Systems

- Forward Collision Warning (FCW)

- Crash Imminent Braking (CIB)

- Dynamic Brake Support (DBS)

- Others

By Vehicle Type

- Passenger Cars

- Hatchbacks

- Sedans

- SUVs / Crossovers

- MPVs

- Commercial Vehicles

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

By Sales Channel / Fitment Type

- Original Equipment Manufacturer (OEM) / Factory-Fitted

- Aftermarket Retrofit Systems

Regional Analysis

North America Dominates the Automatic Emergency Braking Market with a Market Share of 33.30%, Valued at USD 19.64 Billion

North America leads due to its established ADAS supplier ecosystem, high safety-feature penetration, and the forthcoming U.S. compliance requirement. FMVSS No. 127 will require AEB and pedestrian AEB across nearly all new passenger cars and light trucks by September 2029. This makes North America a priority region for suppliers building compliant radar, camera, compute, braking, and validation capabilities.

Europe remains a strategically important region because vehicle safety assessment influences OEM feature roadmaps and consumer expectations. Euro NCAP conducted 108 vehicle-safety assessments involving more than 50 automotive brands in 2025, while 98% of tested models achieved four stars or more. This raises the commercial value of AEB systems that provide dependable pedestrian, cyclist, and higher-speed collision mitigation performance.

Asia-Pacific offers volume expansion through passenger vehicles, local EV platforms, and mass-market ADAS adoption. Latin America and the Middle East and Africa create selective opportunities where rating programs, fleet safety needs, and gradual vehicle-feature upgrades support adoption. Bharat NCAP evaluates safety-assist technologies for M1 vehicles up to 3,500 kg and operates as a voluntary rating framework above regulatory requirements. This creates an indirect route for safety-feature differentiation in India.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Market Dynamics

Market Opportunity Analysis - Commercial fleets, retrofit systems, and emerging-market safety platforms widen the addressable base

Commercial vehicles offer an underexploited route beyond the passenger-car base, despite representing 26.95% of vehicle-type demand. Fleet operators prioritize reduced accident exposure, vehicle uptime, and measurable safety outcomes. AEB reduced front-to-rear crashes by 49% across studied model years. Suppliers that adapt long-range detection, heavy-vehicle braking interfaces, and fleet-data services can pursue a higher-value product mix.

Aftermarket retrofit AEB systems offer another route to address older vehicles that will not receive factory-installed functions. This channel represents 25.00% of fitment demand and can serve commercial operators with extended replacement cycles. Providers need installation efficiency, calibration discipline, and clear evidence of safety value. The 9% reduction in non-motorist crashes associated with pedestrian AEB supports outcome-based positioning for fleet and insurance customers.

India offers an emerging safety-led opening because Bharat NCAP is structured as a voluntary assessment framework that evaluates safety-assist technologies. The program covers M1 vehicles up to 3,500 kg and evaluates adult occupant protection, child occupant protection, and safety assists. Suppliers that develop cost-sensitive camera-radar architectures can help domestic OEMs use safety features as a model-differentiation tool before uniform mandatory fitment expands.

Technology and Innovation Landscape - Sensor fusion, software-defined updates, and AI perception elevate AEB capability

Radar-camera fusion is becoming central to next-generation AEB because it combines camera classification with radar range and velocity data. NHTSA’s requirement for pedestrian detection in daylight and darkness places particular pressure on architectures that rely only on visible-light cameras. Suppliers that optimize fusion algorithms can improve detection confidence while reducing false braking, strengthening their value in both regulatory and premium-safety programs.

AI-based object classification and trajectory prediction can improve braking decisions in complex traffic scenes involving pedestrians, cyclists, intersections, and cross-traffic. The PARTS result of a 52% reduction in front-to-rear crashes for newer AEB systems demonstrates that system-generation advances produce real-world performance gains. Investment in data pipelines, simulation, and vehicle-edge compute can therefore create defensible software differentiation.

Software-defined vehicle architectures create a pathway for over-the-air AEB refinements after vehicle delivery. This allows OEMs to address perception improvements, scenario tuning, and safety-function upgrades without replacing core electronic hardware. However, suppliers must design updates around strict validation, cybersecurity, and functional-safety controls. The growing dependence on integrated systems, which hold 18.00% of component demand, supports demand for maintainable software architectures.

Drivers

Mandatory AEB rules provide the strongest structural catalyst because they transform a discretionary ADAS feature into a vehicle-program requirement. NHTSA projects FMVSS No. 127 will save at least 360 lives and prevent at least 24,000 injuries annually once implemented. OEMs must consequently secure compliant sensors, software, ECUs, and brake integration well before the September 2029 deadline, increasing multi-year sourcing opportunities for qualified suppliers.

Safety ratings and proven system effectiveness reinforce this regulatory pull. Newer AEB systems reduced front-to-rear crashes by up to 52%, according to the PARTS study, compared with 46% for earlier model-year systems. This creates a commercial rationale for radar-camera fusion and advanced perception software, particularly where OEMs seek higher safety scores and measurable fleet-risk reduction.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory AEB Regulations — EU General Safety Regulation & NHTSA FMVSS 127 | +5.2% | EU (all Contracting Parties to UN R152), United States, Japan, South Korea, Australia | Short term (≤ 2 years) |

| Rapid OEM ADAS Fitment Rate Increase Across Mass-Market Vehicle Segments | +3.8% | Global, led by China, Europe, North America | Short term (≤ 2 years) |

| NCAP Safety Rating Pressure Driving Voluntary AEB Adoption in Emerging Markets | +2.4% | India (Bharat NCAP), China (C-NCAP), Latin America (Latin NCAP), ASEAN NCAP | Short term (≤ 2 years) |

| Automotive Radar Sensor Cost Deflation Enabling Mid-Range Vehicle Integration | +2.0% | Global, most impactful in Asia-Pacific & Latin America price-sensitive segments | Short term (≤ 2 years) |

| Rising EV Platform Adoption Accelerating ADAS Suite Standardization | +1.5% | China (primary), Europe, United States, South Korea | Medium term (2–4 years) |

| Insurance Premium Incentives & Fleet Telematics Integration Boosting Retrofit Demand | +0.8% | United States, UK, Germany, Australia | Medium term (2–4 years) |

Restraints

System integration and homologation costs restrict adoption in lower-priced vehicles and slow broader penetration in price-sensitive markets. OEMs must validate AEB against road, weather, vehicle, pedestrian, cyclist, and braking scenarios before production release. NHTSA’s rule requires pedestrian detection in daylight and darkness, with automatic braking up to 45 mph in pedestrian scenarios. These requirements raise development costs and increase the appeal of scalable shared platforms.

Regulatory uncertainty can defer capital commitments despite the current September 2029 compliance deadline. Suppliers must balance long sensor-development cycles against potential changes in timing or performance interpretation. The Federal Register states that compliance applies to most covered vehicles manufactured on or after September 1, 2029. OEMs that delay architecture decisions may face compressed supplier qualification and production-validation schedules.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NHTSA FMVSS 127 Regulatory Uncertainty & Potential Compliance Deadline Extension | -3.2% | United States; cascading to Tier-1 supplier CapEx and OEM program schedules globally | Short term (≤ 2 years) |

| High System Integration Cost Limiting Adoption in Sub-$15,000 Vehicle Price Tier | -2.1% | India, Southeast Asia, Latin America, Sub-Saharan Africa | Medium term (2–4 years) |

| Automotive OEM Production Slowdown & EV Demand Cooling in Key Markets | -1.4% | United States, Europe, China | Short term (≤ 2 years) |

| Semiconductor Supply Constraints for Automotive-Grade Radar & Vision SoCs | -1.0% | Global, most acute for non-Tier-1 ADAS suppliers lacking secured wafer agreements | Short term (≤ 2 years) |

| Consumer & Liability Resistance from Phantom Braking Incidents | -0.8% | United States, Europe, Australia | Short term (≤ 2 years) |

Challenges

Nighttime pedestrian performance remains a core technical challenge because camera-only systems can lose perception accuracy under weak illumination and difficult contrast conditions. FMVSS No. 127 requires pedestrian detection in both daylight and darkness and automatic braking up to 45 mph when a pedestrian is detected. This creates revenue potential for radar-camera fusion, thermal sensing, low-light perception models, simulation services, and specialized validation datasets.

Multi-sensor fusion also increases software and cybersecurity demands across the AEB value chain. Suppliers must combine sensor inputs, distinguish genuine hazards, predict trajectories, and ensure safe braking decisions without excessive false activations. The 52% front-to-rear crash reduction observed in newer AEB systems indicates that technology refinement delivers measurable value. Suppliers that improve validation speed and software reliability can command stronger positions in integrated ADAS programs.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Pedestrian AEB Night Performance Gap | -2.3% | Global, acute in markets with high pedestrian & mixed-traffic road environments | Medium term (2–4 years) |

| Multi-Sensor Fusion Algorithm Complexity & Validation | -1.8% | Global, across all OEMs and Tier-1 ADAS suppliers | Long term (≥ 4 years) |

| Edge-Case & Adverse Weather Reliability Limits | -1.4% | Northern Europe, Canada, Russia, mountainous regions globally | Long term (≥ 4 years) |

| Cybersecurity & OTA Update Vulnerability in ADAS ECUs | -1.0% | Global, driven by EU UNECE WP.29 R155 regulation & U.S. auto cybersecurity frameworks | Medium term (2–4 years) |

| Skilled ADAS Software & Validation Talent Deficit | -0.7% | United States, Germany, Japan, India (Bangalore, Pune engineering clusters) | Long term (≥ 4 years) |

Opportunities

Heavy-duty commercial vehicles represent an attractive expansion path because they require longer sensing ranges, more demanding brake integration, and fleet-focused safety performance. Commercial vehicles currently account for 26.95% of the AEB market, establishing a substantial installed base for advanced and retrofit solutions. AEB’s demonstrated reduction in front-to-rear crashes provides suppliers with a measurable value proposition for fleet operators.

Aftermarket retrofit systems create an additional route to monetize the existing vehicle fleet, especially where operators seek safety upgrades before natural fleet replacement. The aftermarket represents 25.00% of the sales-channel segment. The PARTS study also found that pedestrian AEB reduced crashes with non-motorists by 9%. Providers that combine installation, telematics, driver coaching, and insurer-facing data can differentiate beyond hardware supply.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Heavy-Duty Truck AEB Mandate (NHTSA-FMCSA Joint Rulemaking) | +3.1% | United States, EU, Australia, Canada | Medium term (2–4 years) |

| Two-Wheeler & Three-Wheeler AEB Adoption in Emerging Markets | +2.4% | India, China, Indonesia, Vietnam, Thailand | Long term (≥ 4 years) |

| Aftermarket & Fleet Retrofit AEB Systems for In-Service Vehicles | +1.8% | United States, EU, Australia, India (commercial fleet) | Medium term (2–4 years) |

| AEB-as-a-Data-Service & Usage-Based Insurance Integration Platform | +1.3% | United States, UK, Germany, Australia, Japan | Medium term (2–4 years) |

| Off-Highway & Agricultural Vehicle AEB Expansion | +0.9% | North America, Europe, Australia, Brazil | Long term (≥ 4 years) |

Key Company Insights

Robert Bosch GmbH is positioned across the AEB stack through automotive sensing, electronics, software, and braking-system capabilities. This breadth allows Bosch to compete for integrated OEM ADAS programs rather than single-component contracts. Its July 2025 SX600 and SX601 radar system-on-chip launch supports Level 2+ functions including AEB, adaptive cruise control, and blind-spot detection. This approach strengthens Bosch’s relevance as sensor fusion becomes more central to compliant AEB performance.

Continental AG benefits from its broad automotive systems presence, which supports embedded AEB integration across vehicle platforms and safety architectures. The company’s strategic opportunity rests on linking sensing, compute, and actuation requirements into validated solutions for OEMs. Regulatory standards require coordinated vehicle-level performance rather than component-level compliance alone. Continental’s ability to support system integration can reduce OEM development complexity, although platform price pressure remains a material margin risk.

Key Players

- Robert Bosch GmbH

- Continental AG

- ZF Friedrichshafen AG (ZF-TRW)

- Mobileye (Intel Corporation)

- Autoliv Inc.

- DENSO Corporation

- Valeo S.A.

- Hyundai Mobis Co., Ltd.

- Aisin Corporation

- Knorr-Bremse AG

- Magna International Inc.

- Mando Corporation

- Aptiv PLC

- NXP Semiconductors N.V.

- Infineon Technologies AG

Recent Developments

- March 2025: Volkswagen Group announced a collaboration with Mobileye and Valeo for future MQB vehicle ADAS platforms that include Automatic Emergency Braking functions.

- July 2025: Bosch launched SX600 and SX601 radar system on chip products for Level 2+ ADAS functions including AEB, adaptive cruise control, and blind spot detection.

- September 2025: Valeo entered a long term partnership with Momenta to develop intelligent assisted and autonomous driving solutions using radar camera sensor fusion.

- 2025: ZF Friedrichshafen agreed to sell its passenger car ADAS business to Harman International for approximately EUR 1.5 Billion while retaining commercial vehicle ADAS development.

Report Scope

| Report Features | Description |

|---|---|

| Market Value 2025 | USD 59.0 Billion |

| Forecast Revenue 2035 | USD 249.8 Billion |

| CAGR 2026-2035 | 15.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | Component, Vehicle Type, Sales Channel / Fitment Type, Region |

| Regional Analysis | North America, Europe, Asia Pacific, Latin America, Middle East and Africa |

| Competitive Landscape | Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG, Mobileye, Autoliv Inc., DENSO Corporation, Valeo S.A., Hyundai Mobis, Aisin Corporation, Knorr-Bremse AG, Magna International Inc., Mando Corporation, Aptiv PLC, NXP Semiconductors N.V., Infineon Technologies AG |

| Customization Scope | Customization for segments and region country-level analysis will be provided. Additional customization can be completed based on requirements. |

| Purchase Options | Single User License, Multi-User License up to 5 users, Corporate Use License with unlimited users and printable PDF |

Market")