Quick Navigation

Report Overview

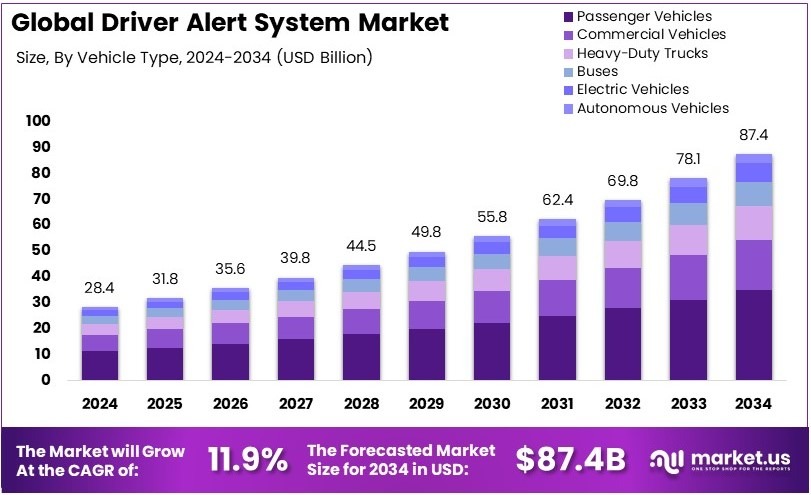

The Global Driver Alert System Market size is expected to be worth around USD 87.4 Billion by 2034, from USD 28.4 Billion in 2024, growing at a CAGR of 11.9% during the forecast period from 2025 to 2034.

A Driver Alert System is a safety feature in vehicles that monitors the driver’s behavior and alertness. It uses sensors or cameras to detect signs of driver fatigue, distraction, or drowsiness and provides warnings to encourage the driver to take a break or refocus. This system helps improve road safety.

The Driver Alert System Market refers to the demand for systems that monitor and alert drivers about their condition and focus. This market includes different technologies, such as lane-departure warning, fatigue detection, and distraction monitoring, and caters to the automotive industry aiming to enhance driver safety.

Driver alert systems are designed to enhance driver safety by providing real-time warnings for potential risks. These systems include features like lane departure warnings and fatigue alerts. As road safety becomes a top priority, demand for these systems is rising. This trend is expected to grow as automation in vehicles increases.

The driver alert system market is seeing steady growth due to increased safety concerns and regulations. As of 2023, vehicle safety features, including driver alert systems, are becoming mandatory in many regions. In fact, the adoption of these systems is expected to increase, driven by both consumer demand and regulatory requirements, boosting market growth.

Key growth factors for driver alert systems include the rising focus on road safety and the need to reduce accidents caused by driver error. As awareness of these systems’ benefits grows, so does demand. Governments are also playing a role by mandating these systems in new vehicles, providing additional market opportunities.

The market remains competitive, with numerous companies introducing innovative driver assistance technologies. Despite this, the market is not yet fully saturated, with significant room for growth in emerging markets. Regions like Asia and Africa, where vehicle safety regulations are improving, offer considerable expansion potential for driver alert systems.

Government investment is driving the growth of driver alert systems. In addition to safety mandates, many countries are offering incentives for automakers to integrate these systems. These policies are encouraging manufacturers to adopt advanced safety features, resulting in increased availability and adoption of driver alert systems in vehicles.

Key Takeaways

- The Driver Alert System Market was valued at USD 28.4 billion in 2024 and is expected to reach USD 87.4 billion by 2034, with a CAGR of 11.9%.

- In 2024, Passenger Vehicles dominate the vehicle type segment, reflecting their higher adoption rates of advanced safety technologies.

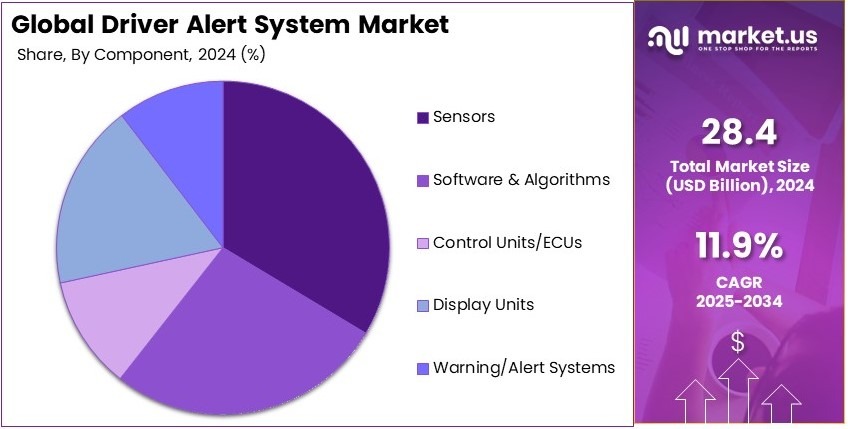

- In 2024, Sensors lead the component segment, driven by their critical role in detecting and responding to potential driving hazards.

- In 2024, Lane Departure Warning (LDW) dominates the technology type segment, reflecting its effectiveness in preventing accidents caused by driver distraction or fatigue.

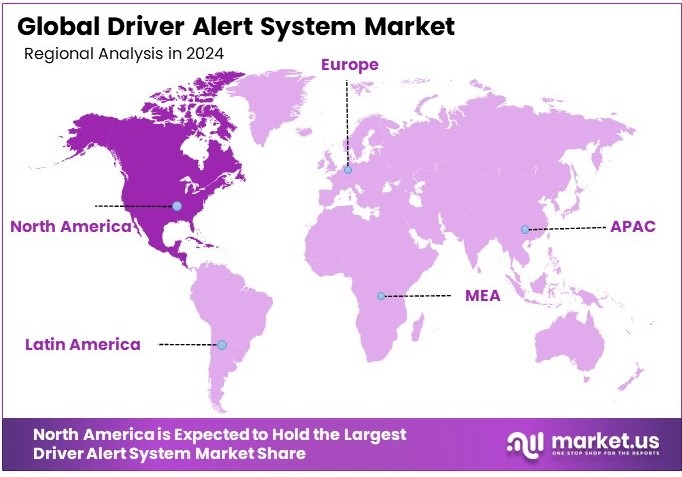

- In 2024, North America leads the regional market, benefiting from strong regulatory support for advanced driver assistance systems (ADAS) and high consumer demand.

Vehicle Type Analysis

Passenger Vehicles dominate with a substantial share due to the increasing adoption of driver alert systems for safety and convenience.

In the Driver Alert System market, passenger vehicles hold the largest share, driven by the increasing demand for safety features and the rise in consumer awareness regarding road safety. As more drivers seek advanced safety technologies, automakers have integrated driver alert systems into passenger vehicles to reduce accidents and enhance driving experience.

These systems, which include features like lane departure warning, forward collision warning, and adaptive cruise control, are seen as essential to improving vehicle safety. Consumers now expect these technologies in new cars, and this has led to a rapid increase in their adoption.

Commercial vehicles and heavy-duty trucks, though significant, make up a smaller portion of the market. They are increasingly equipped with driver alert systems to prevent accidents in challenging driving conditions, such as on highways or construction zones.

Electric vehicles (EVs) and autonomous vehicles also contribute to the market but are still emerging in the context of driver alert systems. EVs benefit from such systems as part of their overall appeal as eco-friendly, high-tech alternatives.

Autonomous vehicles, on the other hand, have driver alert systems as part of their broader suite of advanced driver-assistance systems (ADAS), though they are still under development and testing for full commercial use.

Component Analysis

Sensors dominate with a significant share due to their essential role in enabling the functionality of various driver alert systems.

Sensors are the dominant component in the driver alert system market. These devices are responsible for detecting obstacles, monitoring vehicle surroundings, and feeding data to the system to trigger alerts. Without sensors, many of the key functionalities of driver alert systems, such as lane departure warnings, blind spot detection, and collision warnings, would not be possible.

Advanced sensor technologies, such as radar, LIDAR, and cameras, are continuously evolving, making these systems more effective in preventing accidents. Sensors provide the real-time data necessary for making critical safety decisions, which has made them indispensable in modern vehicles.

Software and algorithms follow closely behind as a critical component, responsible for interpreting data collected by sensors and making decisions based on it. Without these, the sensor data would be useless.

Control units and electronic control units (ECUs) are responsible for managing the data and ensuring the proper operation of driver alert systems. Display units, on the other hand, serve as the interface between the system and the driver, alerting them to potential hazards. Warning and alert systems are integral to providing feedback to the driver once an issue is detected.

Technology Type Analysis

Lane Departure Warning (LDW) dominates with a significant share due to its widespread implementation and importance in preventing accidents.

Lane Departure Warning (LDW) technology is one of the leading technologies in the driver alert system market. This system warns drivers when they unintentionally drift out of their lane, helping to reduce accidents caused by distracted driving or fatigue.

As one of the earliest and most widely implemented features, LDW has been included in many new vehicles, especially as part of the push for enhanced safety in both passenger and commercial vehicles. This technology has proven effective in preventing accidents, particularly on highways, and is now often seen as a standard feature in new vehicles.

Forward Collision Warning (FCW) and Automatic Emergency Braking (AEB) are closely following in importance. These technologies are essential for preventing rear-end collisions and mitigating the severity of accidents. By providing timely warnings and, in the case of AEB, automatically applying brakes when a collision is imminent, they reduce accidents and injuries significantly.

Blind Spot Detection (BSD) is another key technology, especially in larger vehicles like trucks and buses. This system alerts drivers to vehicles that may be in their blind spots, reducing the risk of lane-change accidents.

Other technologies, such as Driver Attention Monitoring, Pedestrian Detection, and Drowsiness/Fatigue Detection, are also contributing to the market but are less widespread in implementation compared to LDW. These technologies are gaining popularity as automakers focus on enhancing driver safety further. However, they are still seen more in premium models or as optional add-ons rather than standard features.

Key Market Segments

By Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

- Heavy-Duty Trucks

- Buses

- Electric Vehicles (EVs)

- Autonomous Vehicles

By Component

- Sensors

- Software & Algorithms

- Control Units/ECUs

- Display Units

- Warning/Alert Systems

By Technology Type

- Lane Departure Warning (LDW)

- Lane Keeping Assist (LKA)

- Forward Collision Warning (FCW)

- Automatic Emergency Braking (AEB)

- Blind Spot Detection (BSD)

- Driver Attention Monitoring

- Pedestrian Detection

- Traffic Sign Recognition

- Adaptive Cruise Control (ACC)

- Drowsiness/Fatigue Detection

- Collision Avoidance System

Driving Factors

Rising Road Safety Concerns and Traffic Accidents Drive Market Growth

The Driver Alert System Market is experiencing significant growth due to rising road safety concerns and the increasing frequency of traffic accidents. With road traffic accidents leading to significant loss of life and economic costs, both governments and consumers are prioritizing solutions to improve road safety.

Driver alert systems, such as lane departure warning, forward collision warning, and drowsiness detection, are designed to mitigate these risks by alerting drivers about potential dangers.

As the number of road accidents continues to rise globally, there is growing pressure on automakers to incorporate these technologies into their vehicles. This surge in demand for safety features is further fueled by public awareness campaigns highlighting the importance of preventing accidents and minimizing injuries.

As consumers become more safety-conscious, the adoption of driver alert systems is expanding rapidly, contributing to the growth of the market. Additionally, governments around the world are setting stricter road safety standards, mandating that more vehicles be equipped with these safety technologies, which in turn drives the demand for driver alert systems in both new and existing vehicles.

Restraining Factors

Limited Consumer Awareness and Adoption in Emerging Markets Restrain Market Growth

Despite the promising growth of the Driver Alert System Market, certain factors present barriers, particularly limited consumer awareness and adoption in emerging markets. In many developing countries, vehicle safety features are not prioritized, and consumers are often unaware of the benefits that driver alert systems offer in terms of accident prevention and overall safety.

Due to the lack of education on the advantages of these technologies, consumers in emerging markets may be less inclined to pay for or demand such systems in their vehicles.

Additionally, the cost of adding advanced safety features to vehicles can be a significant deterrent in price-sensitive regions. Without a strong understanding of the value these systems provide, consumers may choose to forgo them, slowing adoption rates.

Furthermore, in some countries, a lack of government mandates or incentives for safety technologies limits the widespread implementation of driver alert systems, which hinders the growth of the market in these regions. As awareness and affordability improve, the adoption of driver alert systems in emerging markets is expected to increase, but until then, this remains a restraint for market growth.

Growth Opportunities

Integration of Real-time Data and Cloud Computing in Driver Alert Systems Provides Opportunities

he integration of real-time data and cloud computing presents significant opportunities for the growth of the Driver Alert System Market. By using cloud-based technologies, driver alert systems can receive and analyze data from a variety of sources, such as traffic conditions, weather, and road hazards, in real-time. This allows for more accurate and timely alerts, improving the overall effectiveness of the system.

For instance, integrating data from connected vehicles, smart infrastructure, and traffic management systems could enable a driver alert system to provide warnings about upcoming hazards like traffic jams, accidents, or sudden weather changes. The ability to continuously update and refine safety algorithms through cloud computing also improves the adaptability and responsiveness of these systems.

As connected cars and smart cities become more widespread, the demand for driver alert systems that leverage real-time data and cloud-based solutions will increase. This integration can also enhance vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communication, making driver alert systems more comprehensive and capable of preventing accidents in complex environments.

Emerging Trends

Development of Haptic Feedback for Driver Alerts Is Latest Trending Factor

One of the latest trends in the Driver Alert System Market is the development of haptic feedback for driver alerts. Haptic feedback involves the use of vibrations or tactile sensations to alert the driver to potential hazards. This trend is gaining traction as it offers a more discreet and intuitive way of delivering safety warnings without relying on visual or auditory signals.

In situations where a driver may be distracted or experiencing sensory overload, haptic feedback provides a direct and non-intrusive form of alert that ensures the driver’s attention is quickly drawn to the potential danger. For instance, a steering wheel or seat can vibrate to warn a driver if they are drifting out of their lane or approaching an obstacle too quickly.

Haptic feedback also has the advantage of being less likely to contribute to driver distraction compared to loud, frequent auditory alerts. As automakers continue to innovate and look for ways to enhance the safety and comfort of their vehicles, the incorporation of haptic feedback is becoming an increasingly important feature in driver alert systems.

Regional Analysis

North America Dominates with Major Market Share

North America leads the Driver Alert System market, holding a significant share. This strong market presence is driven by the region’s advanced automotive industry, high consumer demand for vehicle safety features, and ongoing innovation in automotive technologies. The adoption of driver alert systems is bolstered by stricter safety regulations and increasing consumer awareness about road safety.

Key factors contributing to North America’s dominance include the presence of major automakers like General Motors, Ford, and Tesla, which are investing heavily in active safety systems. These automakers are incorporating driver alert technologies like lane departure warning and forward collision warning into their vehicles to meet safety standards.

Additionally, consumers in North America are increasingly seeking vehicles with advanced safety features, driving the demand for these systems. Government regulations such as the National Highway Traffic Safety Administration’s (NHTSA) push for better vehicle safety standards also contribute to market growth.

Regional Mentions:

- Europe: Europe has a strong market presence in driver alert systems, driven by strict safety regulations and a high focus on environmental sustainability. Countries like Germany and France are at the forefront, integrating advanced safety features in vehicles.

- Asia Pacific: Asia Pacific is growing rapidly in the driver alert system market, particularly in China and Japan. Major automakers in this region are accelerating their efforts to include safety technologies as part of their consumer offerings.

- Middle East & Africa: The Middle East and Africa are witnessing a gradual increase in the adoption of driver alert systems, driven by rising road safety awareness and growing demand for advanced vehicles in countries like the UAE and South Africa.

- Latin America: Latin America is beginning to adopt driver alert systems, particularly in Brazil and Mexico. The region’s rising middle class and demand for safer vehicles are contributing to the growth of these systems in the automotive market.

Key Regions and Countries Covered in the Report

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Landscape

The Driver Alert System Market is highly competitive, with leading companies like Bosch Group, Denso Corporation, Autoliv Inc., and Continental AG driving innovation and market growth. These companies play a vital role in developing and deploying driver assistance technologies that enhance vehicle safety and improve overall driving experiences.

Bosch Group is a global leader in automotive technologies, including driver alert systems. Bosch’s advanced sensor technology and its expertise in radar, camera, and ultrasonic sensors make it a key player in this market. The company provides systems like lane-keeping assistance, forward collision warning, and emergency braking, which are crucial for reducing accidents. Bosch’s strong R&D capabilities ensure continuous improvement in safety features and integration of new technologies.

Denso Corporation is another major player in the driver alert system sector. Known for its electronic components and automotive systems, Denso supplies a variety of advanced safety features, including collision prevention and driver monitoring systems. Denso’s products are integrated into vehicles of leading automakers worldwide. The company focuses on enhancing vehicle safety through innovations in artificial intelligence (AI) and sensor fusion technologies.

Autoliv Inc. specializes in safety systems and is widely recognized for its airbag and seatbelt solutions. In the driver alert system market, Autoliv offers features like lane departure warning and adaptive cruise control. With a strong global presence, the company collaborates closely with automakers to design systems that improve driver awareness and reduce the risk of accidents. Autoliv’s extensive expertise in safety and strong partnerships help maintain its competitive edge.

Continental AG is a key player in the development of driver assistance technologies. The company provides a wide range of safety systems, including forward collision warning, lane-keeping assistance, and driver drowsiness detection. Continental’s focus on innovation and its broad portfolio of sensors, cameras, and radar systems make it a leader in the driver alert system market, contributing significantly to vehicle safety.

These four companies are at the forefront of driver alert systems, shaping the future of automotive safety with cutting-edge technologies.

Major Companies in the Market

- Bosch Group

- Denso Corporation

- Autoliv Inc.

- Continental AG

- Aptiv PLC

- Valeo SA

- Magna International Inc.

- Delphi Technologies

- Mobileye (Intel Corporation)

- ZF Friedrichshafen AG

- Harman International (Samsung Electronics)

- Texas Instruments

- Omron Corporation

Recent Developments

- Smart Eye: On October 2024, Smart Eye’s AIS CV Alert driver monitoring system was officially homologated by Solaris, a leading manufacturer of city and intercity buses in Europe. The certification confirms that Solaris’s vehicles meet the EU’s General Safety Regulation (GSR) requirements, which mandate the integration of advanced drowsiness detection systems in new commercial vehicles, including buses and trucks.

- Bosch: On January 2025, Bosch announced at CES that it is expanding its cloud-based wrong-way driver alert system through a partnership with SiriusXM. Originally introduced in 2019, the system uses anonymized data to track vehicles as they approach highway entrance or exit points. If a vehicle is traveling in the wrong direction, the system issues an alert through the vehicle’s radio speakers or connected smartphone.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 28.4 Billion |

| Forecast Revenue (2034) | USD 87.4 Billion |

| CAGR (2025-2034) | 11.9% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Vehicle Type (Passenger Vehicles, Commercial Vehicles, Heavy-Duty Trucks, Buses, Electric Vehicles, Autonomous Vehicles), By Component (Sensors, Software & Algorithms, Control Units/ECUs, Display Units, Warning/Alert Systems), By Technology Type (Lane Departure Warning, Lane Keeping Assist, Forward Collision Warning, Automatic Emergency Braking, Blind Spot Detection, Driver Attention Monitoring, Pedestrian Detection, Traffic Sign Recognition, Adaptive Cruise Control, Drowsiness/Fatigue Detection, Collision Avoidance System) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Bosch Group, Denso Corporation, Autoliv Inc., Continental AG, Aptiv PLC, Valeo SA, Magna International Inc., Delphi Technologies, Mobileye (Intel Corporation), ZF Friedrichshafen AG, Harman International (Samsung Electronics), Texas Instruments, Omron Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |