Quick Navigation

Report Overview

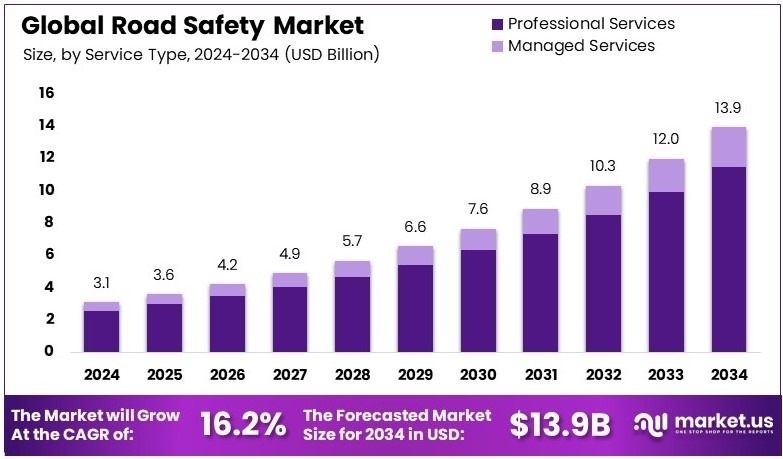

The Global Road Safety Market size is expected to be worth around USD 13.9 Billion by 2034, from USD 3.1 Billion in 2024, growing at a CAGR of 16.2% during the forecast period from 2025 to 2034.

Road safety involves measures and practices designed to reduce accidents and injuries on roads. It includes traffic laws, vehicle standards, and infrastructure improvements. Road safety focuses on protecting drivers, passengers, and pedestrians. It relies on education, enforcement, and engineering to prevent accidents and save lives.

The road safety market includes products and services aimed at improving safety on roads. This market offers safety equipment, technologies, consulting, and training. It serves governments, institutions, and companies looking to reduce accidents. The market focuses on providing solutions that enhance compliance, prevention, and overall safety measures.

Road safety is a significant concern worldwide as stakeholders continuously seek to minimize traffic-related accidents. Intelligent transportation systems (ITS) are proving to be a powerful tool in this effort.

According to the U.S. Department of Transportation, these systems can potentially reduce crashes by up to 80%. This technology focuses on enhancing the responsiveness and effectiveness of traffic management, thereby safeguarding the lives of commuters and reducing congestion on roads.

The road safety market is experiencing robust growth, driven by an increase in vehicle numbers and heightened traffic management needs. As of the second quarter of 2024, the U.S. reported approximately 291.1 million vehicles in operation, a figure that reflects a continual upward trend in vehicle ownership.

Globally, the number of motor vehicles, including cars, trucks, and buses, was already over 1 billion in 2010, with projections indicating it could reach 2 billion by 2035. The growing vehicle population necessitates advanced road safety solutions to manage increased traffic volumes and enhance public safety effectively.

The impact of road safety measures is substantial on both local and broader scales. In 2022, the U.S. National Highway Traffic Safety Administration (NHTSA) highlighted the ongoing challenge, reporting 42,795 fatalities from motor vehicle traffic crashes. This statistic equates to a fatality rate of 1.35 deaths per 100 million vehicle miles traveled, underscoring the critical need for comprehensive and effective road safety strategies.

Government investments and regulations play a pivotal role in shaping these strategies. By implementing stringent safety standards and investing in advanced transportation technologies, governments can significantly decrease the incidence of road-related fatalities and injuries, thereby enhancing the overall safety and efficiency of transportation systems.

Key Takeaways

- The Road Safety Market was valued at USD 3.1 Billion in 2024, and is expected to reach USD 13.9 Billion by 2034, with a CAGR of 16.2%.

- In 2024, Red Light & Speed Enforcement Systems dominate the solution type segment with 58.3%, demonstrating their critical role in reducing traffic violations.

- In 2024, Professional Services lead the service type segment with 82.5%, highlighting their importance in implementing safety solutions.

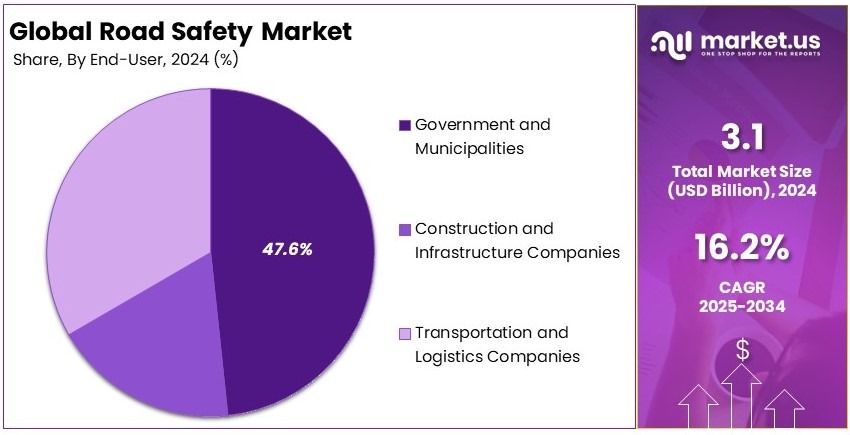

- In 2024, Government and Municipalities dominate the end-user segment with 47.6%, emphasizing their significant investment in road safety.

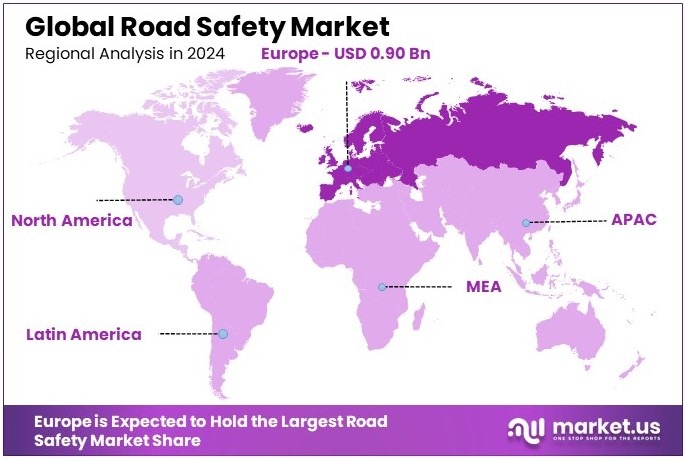

- In 2024, Europe leads the regional market with 29.1% and a value of USD 0.90 Bn, reflecting strong regional growth.

Solution Type Analysis

Red Light & Speed Enforcement Systems dominate with 58.3% due to their critical role in enforcing traffic laws and improving road safety.

The Road Safety Market is integral to enhancing vehicular safety and reducing traffic-related incidents. Within this market, Solution Types are pivotal segments, and Red Light & Speed Enforcement Systems stand out as the dominant sub-segment, commanding 58.3% of the market share.

Their prominence is attributed to the essential function they serve in monitoring and enforcing traffic compliance, thereby significantly decreasing the occurrence of road accidents and fatalities.

Other key solution types in this segment include Incident Detection and Monitoring Systems, Automatic License Plate Recognition (ALPR) Systems, Traffic Management Systems, and Surveillance Systems. Incident Detection and Monitoring Systems are crucial for immediate response to accidents, ensuring rapid deployment of emergency services.

ALPR Systems enhance security and traffic enforcement by automating vehicle identification and tracking. Traffic Management Systems are vital for optimizing traffic flow and reducing congestion, especially in urban areas. Surveillance Systems provide continuous monitoring, contributing to overall road safety and security.

Service Type Analysis

Professional Services dominate with 82.5% due to their essential role in implementing and optimizing road safety solutions.

In the realm of Road Safety, Service Types play a crucial role, with Professional Services being the most significant, holding 82.5% of the segment’s market share. This predominance is due to the comprehensive support these services offer, encompassing consulting, advisory, and implementation services, which are essential for deploying effective road safety systems.

The segment also includes Managed Services, which although smaller, are vital for the ongoing management and maintenance of road safety systems. These services ensure that the systems are not only well-integrated into current traffic infrastructure but are also continually updated to adapt to evolving road conditions and traffic patterns.

End-User Analysis

Government and Municipalities dominate with 47.6% due to their primary responsibility for public safety and infrastructure management.

The End-User segment of the Road Safety Market is crucial, with Government and Municipalities leading the way, accounting for 47.6% of the market.

This group’s leading position stems from its foundational role in public safety and infrastructure management, which includes implementing road safety measures to protect citizens and reduce traffic-related issues.

Other significant end-users include Construction and Infrastructure Companies and Transportation and Logistics Companies. Construction and Infrastructure Companies rely on robust road safety systems during building projects to ensure the safety of workers and the public.

Transportation and Logistics Companies use these systems to maintain the safety of their operations and ensure efficient and secure transport of goods and services.

Key Market Segments

By Solution Type

- Red Light Enforcement Systems

- Speed Enforcement Systems

- Incident Detection and Monitoring Systems

- Automatic License Plate Recognition (ALPR) Systems

- Traffic Management Systems

- Surveillance Systems

By Service Type

- Professional Services

- Consulting and Advisory Services

- Implementation Services

- Managed Services

By End-User

- Government and Municipalities

- Construction and Infrastructure Companies

- Transportation and Logistics Companies

Driving Factors

Multiple Factors Drive Market Growth

The Road Safety Market is influenced by various driving factors that work together. An increasing number of vehicles on the road globally raises the demand for safety solutions. More vehicles mean higher risk, which pushes investments in safety products.

Growing adoption of advanced traffic management systems also supports market growth. As cities implement smarter traffic controls, safety improves, and market demand rises. Advancements in Vehicle-to-Infrastructure (V2I) communication make systems more responsive. This technology connects vehicles with road infrastructure, reducing accidents.

Additionally, there is an increasing focus on pedestrian and cyclist safety. Urban planners and governments prioritize safer streets for all users. This multifaceted growth is seen when a city installs intelligent traffic lights and surveillance systems, leading to smoother traffic flow and fewer accidents.

Restraining Factors

Economic and Regulatory Challenges Restrain Market Growth

The Road Safety Market faces several challenges that may slow its progress. Implementing traffic regulations uniformly across regions is difficult. Not all areas have the same resources or policies. This inconsistency can hinder the adoption of safety measures.

Limited adoption of technology in low-income regions slows market growth further. These areas often cannot afford advanced safety systems. Maintenance and upkeep of safety equipment also present a challenge. Regular servicing is costly and time-consuming, deterring some investments.

Resistance to new technologies from traditional stakeholders can create additional barriers. Some prefer old methods and are reluctant to change. These challenges affect market dynamics in different ways. For instance, uniform regulation issues may delay projects. Technological hesitance reduces market penetration. Maintenance hurdles can lead to equipment downtime and inefficiency.

The reluctance of stakeholders may stall new product introductions. As a result, companies face obstacles in expanding their reach and maintaining consistent quality. Addressing these challenges requires clear policies, affordable solutions, and effective change management.

Growth Opportunities

Innovation Provides Opportunities

The Road Safety Market sees ample opportunities through new technological advances. AI-powered crash detection and prevention systems promise quicker response and better outcomes. These systems analyze driving patterns and alert drivers before accidents occur.

Expansion of connected vehicle technology for safety applications increases collaboration between cars and road infrastructure. This can reduce collisions and improve traffic flow. There is also increasing demand for smart signage and digital traffic lights. Such technology makes roads safer by communicating real-time information effectively.

Rising adoption of cloud-based traffic management solutions opens another door. These solutions offer scalable, efficient methods to handle traffic data and emergencies. For example, a city using smart traffic lights can adjust signals based on current road conditions, reducing accidents.

AI detection systems predict high-risk scenarios on busy highways, prompting timely interventions. The move to cloud-based solutions means faster updates and better coordination during emergencies.

Emerging Trends

Smart Trends Are Latest Trending Factor

Emerging trends continue to shape the Road Safety Market. Adoption of vision-based traffic monitoring solutions is on the rise. Cameras and sensors watch traffic patterns and identify hazards in real-time. This technology improves response times and reduces accidents.

Growth in real-time traffic data sharing platforms also stands out. Sharing information between agencies and vehicles helps prevent collisions and manage congestion. Focus on zero-accident road safety initiatives drives new programs and policies. Governments and companies work together to eliminate traffic fatalities.

Development of eco-friendly road marking and signage is another trend. These sustainable solutions reduce environmental impact and often improve visibility for drivers. These trends impact market dynamics significantly. Vision-based monitoring offers precise, actionable data. Real-time data sharing enhances coordination among drivers and authorities.

Zero-accident initiatives push for safer infrastructure and practices. Eco-friendly signage aligns with green policies, appealing to environmentally conscious consumers. For example, a city implementing smart cameras and green road markings can see fewer accidents and cleaner streets. Trends like these guide purchasing decisions and influence policy.

Regional Analysis

Europe Dominates with 29.1% Market Share

Europe leads the Road Safety Market with a 29.1% share, valued at USD 0.90 billion. This dominance is attributed to rigorous regulatory standards, high levels of public safety awareness, and significant investments in road infrastructure improvements.

The region benefits from a well-established framework for traffic management and road safety, supported by strong legislative and technological advancements. Furthermore, Europe’s commitment to reducing road fatalities through the implementation of advanced road safety systems like speed cameras and traffic management systems plays a crucial role.

The future impact of Europe on the global Road Safety Market looks promising, as the region continues to innovate and implement new technologies to enhance road safety. The ongoing initiatives to integrate more advanced telematics and traffic data analysis tools are expected to further solidify Europe’s leadership position.

Regional Mentions:

- North America: North America holds a significant share in the Road Safety Market, driven by technological integration and stringent enforcement of traffic laws. The region’s focus on reducing road incidents through state-of-the-art surveillance and communication systems supports its market strength.

- Asia Pacific: Asia Pacific is rapidly advancing in the Road Safety Market, with emerging economies like India and China prioritizing road safety initiatives. The region’s fast-paced urbanization and increasing vehicle ownership necessitate enhanced road safety measures, fueling market growth.

- Middle East & Africa: The Middle East and Africa are experiencing growth in the Road Safety Market due to increased government initiatives aimed at improving road safety standards. Investments in modern traffic management and enforcement technologies are gradually reshaping the region’s road safety landscape.

- Latin America: Latin America is making steady progress in the Road Safety Market. The region is increasingly adopting traffic management solutions to cope with the high rate of road accidents, spurred by urban growth and increased motorization.

Key Regions and Countries Covered in the Report

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Landscape

In the Road Safety Market, the forefront is led by Jenoptik AG, Kapsch TrafficCom AG, Sensys Gatso Group AB, and Redflex Holdings. These companies are at the helm due to their significant contributions to traffic management solutions and their pivotal roles in enhancing road safety globally.

Jenoptik AG is a leader in speed and red-light enforcement solutions, providing sophisticated sensor technologies and photo enforcement equipment. The company’s focus on innovative traffic monitoring solutions helps in effectively reducing road accidents and enhancing traffic behavior.

Kapsch TrafficCom AG offers a comprehensive suite of solutions for tolling and urban access management, along with advanced traffic management systems. Its commitment to connected mobility solutions helps cities manage traffic flows more efficiently, thus reducing congestion and improving road safety.

Sensys Gatso Group AB specializes in providing systems for speed enforcement and red-light enforcement. The company’s products are integral in supporting law enforcement agencies to deter traffic violations and improve road user safety across various regions.

Redflex Holdings develops traffic management products that deliver significant reductions in traffic violations and accidents. Their systems, including fixed and mobile speed cameras, play a crucial role in managing urban traffic and enhancing the safety measures in place.

These leading companies are crucial in driving innovation and regulatory compliance in the Road Safety Market. Through their continued efforts to develop and deploy advanced road safety technologies, they help in shaping safer transportation environments and influence global market trends.

Major Companies in the Market

- Jenoptik AG

- Kapsch TrafficCom AG

- Sensys Gatso Group AB

- Redflex Holdings

- Verra Mobility Corporation

- SWARCO AG

- FLIR Systems, Inc.

- Cubic Corporation

- Siemens Mobility

- Motorola Solutions, Inc.

- Thales Group

- Conduent, Inc.

- IDEMIA

Recent Developments

- Iteris Inc. and Almaviva: On November 2024, Iteris Inc. was acquired by Almaviva, an Italian digital solutions provider. This strategic move is expected to expand Iteris’ global reach and enhance its capabilities in delivering advanced traffic management and road safety solutions.

- Motorola Solutions and Silent Sentinel: On February 2024, Motorola Solutions acquired Silent Sentinel, a UK-based provider of specialized, long-range cameras. Silent Sentinel’s security systems, designed for the Homeland Security market, are capable of identifying anomalies from up to 20 miles away.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 3.1 Billion |

| Forecast Revenue (2034) | USD 13.9 Billion |

| CAGR (2025-2034) | 16.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Solution Type (Red Light Enforcement Systems, Speed Enforcement Systems, Incident Detection and Monitoring Systems, Automatic License Plate Recognition Systems, Traffic Management Systems, Surveillance Systems), By Service Type (Professional Services: Consulting and Advisory Services, Implementation Services, Managed Services), By End-User (Government and Municipalities, Construction and Infrastructure Companies, Transportation and Logistics Companies) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Jenoptik AG, Kapsch TrafficCom AG, Sensys Gatso Group AB, Redflex Holdings, Verra Mobility Corporation, SWARCO AG, FLIR Systems, Inc., Cubic Corporation, Siemens Mobility, Motorola Solutions, Inc., Thales Group, Conduent, Inc., IDEMIA |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |