Quick Navigation

Report Overview

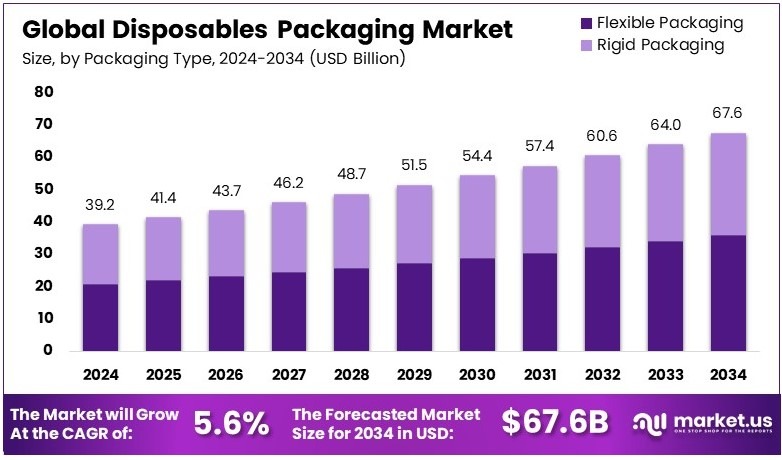

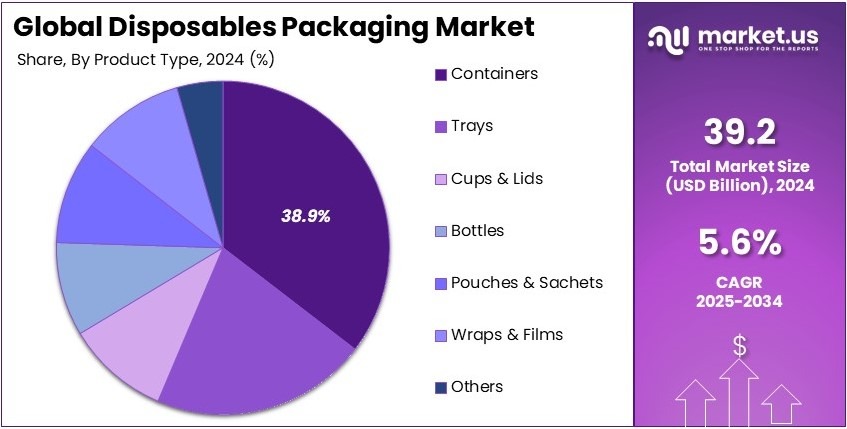

The Global Disposables Packaging Market size is expected to be worth around USD 67.6 Billion by 2034, from USD 39.2 Billion in 2024, growing at a CAGR of 5.6% during the forecast period from 2025 to 2034.

Disposables packaging refers to single-use packaging used to wrap or contain products. It is commonly used in food, healthcare, and retail sectors. Materials include plastic, paper, and aluminum. This packaging type is designed for convenience, hygiene, and easy disposal after one use, reducing the need for cleaning or reuse.

The disposables packaging market includes manufacturers and sellers of single-use packaging. It serves industries like food delivery, medical supplies, and personal care. Market demand is driven by urban lifestyles, hygiene concerns, and growth in e-commerce. Innovation focuses on eco-friendly materials and compliance with sustainability regulations.

The disposables packaging sector is growing as e-commerce expands. In 2023, global retail e-commerce sales hit $5.9 trillion. This number is expected to exceed $8 trillion by 2027. With more online orders, the need for safe and efficient and protective packaging rises, especially for fragile items like glass and electronics.

The disposables packaging market is becoming more competitive. Companies now focus on packaging that is strong, lightweight, and easy to recycle. As per Supply Chain Beyond, 20%-30% of return shipments during holidays are due to product damage. This increases demand for better protective packaging and smarter material use.

In addition, businesses are adding layers of protection to reduce waste and prevent returns. For example, experts recommend using 3 inches of internal packaging when shipping glass items. This best practice lowers damage risk and improves customer experience. As a result, good packaging now supports both brand image and logistics.

On the flip side, market saturation is rising. Many players offer similar packaging solutions, pushing prices down. To stand out, firms are adopting eco-friendly materials or offering custom designs. Those that combine strength, sustainability, and cost-efficiency have better chances to grow in this crowded space.

Meanwhile, environmental regulations are also changing the game. In the U.S., Extended Producer Responsibility (EPR) laws are gaining traction. Minnesota has passed rules that require producers to manage packaging waste by 2031. This shift forces companies to rethink packaging design and material use across all stages.

On a broader scale, sustainable packaging reduces landfill waste and lowers carbon footprints. Locally, businesses that adopt recyclable or compostable packaging attract more eco-conscious consumers. This is especially visible in cities like Seattle and San Francisco, where green standards and consumer preferences shape business strategies.

Key Takeaways

- The Disposables Packaging Market was valued at USD 39.2 billion in 2024 and is expected to reach USD 67.6 billion by 2034, with a CAGR of 5.6%.

- In 2024, Plastic dominated the material segment with 41.8%, due to its cost-effectiveness and widespread use in disposable packaging.

- In 2024, Flexible Packaging led the packaging type segment with 52.7%, owing to its lightweight nature and durability.

- In 2024, Containers accounted for 38.9% of the product type segment, driven by their versatility in food and beverage packaging.

- In 2024, Food & Beverage dominated the end-use industry segment with 60.1%, due to increasing demand for packaged and ready-to-eat meals.

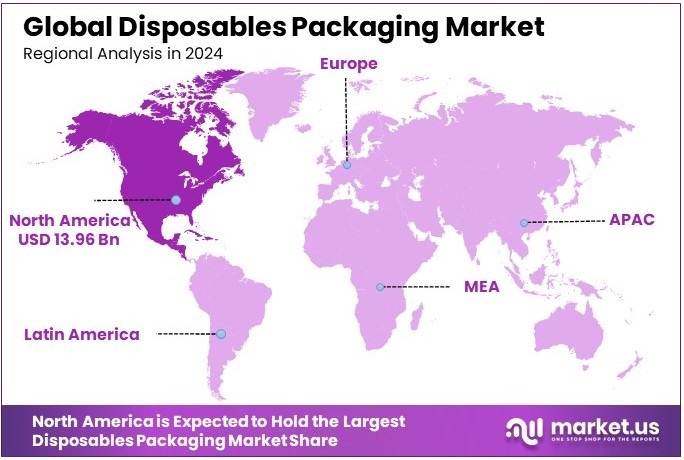

- In 2024, North America led the market with 35.6% and USD 13.96 billion, driven by strong demand from the foodservice and healthcare industries.

Material Type Analysis

Plastic dominates with 41.8% due to its low cost, light weight, and high flexibility across industries.

Plastic remains the most used material in the disposables packaging market. It is widely used because it is affordable, easy to shape, and lightweight. These qualities make it ideal for food packaging, medical items, and consumer products. Plastic containers, trays, and wraps are popular because they preserve freshness and protect against leaks or damage.

In fast-food chains, plastic is commonly used for cups, lids, and utensils. It is also used for takeout packaging and meal kits. The growth of online food delivery and convenience stores supports the high demand for plastic packaging. However, rising concerns about plastic waste have pushed some brands to explore recyclable or biodegradable versions. Still, plastic’s role remains dominant due to its cost efficiency and practicality.

Paper and paperboard are gaining popularity for being eco-friendly. These materials are favored for their recyclability and are used in sustainable packaging campaigns. Aluminum is used mainly in beverage cans and foil trays where long shelf life is required. Glass is chosen for premium and reusable packaging. The remaining category includes biodegradable materials and new innovations that support green packaging goals.

Packaging Type Analysis

Flexible Packaging dominates with 52.7% due to its lightweight nature, lower cost, and space-saving storage.

Flexible packaging is now the leading packaging type. It uses fewer materials than rigid packaging and helps reduce shipping costs. Items like wraps, pouches, sachets, and films fall under this category. Flexible packaging also adjusts easily to the shape of the product.

It is commonly used for snacks, condiments, wet wipes, and frozen foods. This format also protects products from moisture and air, which helps improve shelf life. Many companies prefer flexible packaging for single-use items due to ease of use and disposal. With rising demand for portable and resealable products, this segment continues to grow fast.

Rigid packaging includes containers, bottles, and hard trays. These are used when products need extra protection or structure. While not as space-saving as flexible types, rigid packaging offers better stacking and is often chosen for items that are fragile or heavy.

Product Type Analysis

Containers dominate with 38.9% due to their high usage in food service, safety features, and multi-size availability.

Containers are the most used product type in disposables packaging. They are popular across restaurants, takeout services, and meal delivery platforms. Containers help maintain temperature, protect from contamination, and are available in different sizes for portion control.

Many food outlets use containers for both hot and cold items. With rising demand for home-delivered meals, the need for secure and leak-proof containers has grown rapidly. These containers are often made of plastic, paper, or aluminum and can be stackable, microwavable, or compostable depending on the brand. This level of flexibility adds to their high usage and market share.

Trays are used for ready-to-eat meals and bakery items. Cups and lids are essential in cafes and beverage outlets. Bottles are mainly used for drinks, sauces, or personal care products.

Pouches and sachets are growing due to their use in condiments, wet wipes, and sample packaging. Wraps and films are often used in supermarkets for fresh produce and meat. The remaining category includes clamshells, boxes, and hybrid packaging styles.

End-Use Industry Analysis

Food & Beverage dominates with 60.1% due to daily consumption, strong retail presence, and rising food delivery trends.

The food and beverage industry leads the use of disposable packaging. People need packaged food every day, whether at restaurants, supermarkets, or delivery apps. Disposable packaging helps keep food clean, fresh, and easy to carry.

Items like sandwich wraps, takeout boxes, coffee cups, and meal trays are used across cafes, fast-food chains, and vending machines. This segment also benefits from growing urban populations and changing eating habits. As consumers prefer quick, ready-to-eat meals, food packaging demand keeps rising. Online food delivery apps like Uber Eats and DoorDash have made disposables essential.

Healthcare uses disposable packaging for medicines, instruments, and hygiene products. Personal care & cosmetics mainly use it for packaging creams, wipes, and travel kits. The industrial segment uses disposables for product parts, protective layers, and chemical containment. The remaining category includes education, hospitality, and events where disposable packaging supports convenience and safety.

Key Market Segments

By Material Type

- Plastic

- Paper & Paperboard

- Aluminum

- Glass

- Others

By Packaging Type

- Rigid Packaging

- Flexible Packaging

By Product Type

- Trays

- Containers

- Cups & Lids

- Bottles

- Pouches & Sachets

- Wraps & Films

- Others

By End-Use Industry

- Food & Beverage

- Healthcare

- Personal Care & Cosmetics

- Industrial

- Others

Driving Factors

Food Delivery and Safety Innovations Drive Market Growth

The disposables packaging market is expanding due to rising demand from the food and beverage industry. Single-use packaging offers convenience for fast food, takeout, and ready-to-eat meals. With busy lifestyles and urban living, more consumers now rely on delivery apps like DoorDash and Uber Eats. This trend continues to increase the use of trays, cups, wraps, and containers.

In addition, online food delivery and e-commerce platforms require strong and secure packaging for transportation. As deliveries increase, brands focus on packaging that is leak-proof, stackable, and heat-resistant. These features ensure customer satisfaction and product integrity.

Tamper-evident and child-resistant packaging is also gaining traction. These solutions are now common in pharmaceuticals, household items, and food products. They ensure safety and compliance with health regulations, especially in packaged beverages, baby food, and cleaning items.

Healthcare and pharmaceutical sectors are adopting hygienic disposable packaging too. Items like syringe wrappers, medicine trays, and surgical packaging require sterile, single-use options. Hospitals and clinics use these solutions daily, especially after COVID-19, which highlighted hygiene needs.

Restraining Factors

Environmental Pressure and Cost Volatility Restrain Market Growth

While demand for disposables is strong, environmental and cost-related issues are slowing broader growth. Many governments are now enforcing strict rules on single-use plastics. These regulations limit the use of non-biodegradable packaging materials. As a result, companies must invest more in research and development to find eco-friendly alternatives.

Along with this, the price of raw materials like plastic resin and paper pulp fluctuates often. These price swings affect production costs and lower profit margins for manufacturers. Sudden changes in supply chains or oil prices can make packaging more expensive to produce and less competitive.

In addition, more consumers now prefer reusable or refillable packaging. Eco-conscious customers are turning away from disposables in favor of sustainable choices. This behavior shift puts pressure on brands to rethink packaging formats.

Recycling and waste management systems also pose challenges. Many regions lack the infrastructure to handle the large volume of disposable waste. This causes higher landfill use and public concern over pollution.

Altogether, regulatory pressure, material costs, consumer shifts, and recycling gaps are key challenges for market players. Companies need to act quickly to offer greener, cost-stable solutions to stay relevant in a tightening market environment.

Growth Opportunities

Eco Packaging and Smart Solutions Provide Opportunities

The disposables packaging market has promising opportunities in green materials and smart design. One major area is the shift to biodegradable and compostable packaging. Brands are now replacing plastic with cornstarch-based plastics, sugarcane fibers, and bamboo. These materials break down naturally and appeal to eco-conscious consumers and businesses.

Companies are also investing in advanced barrier coatings that improve shelf life and strength. These coatings make biodegradable packaging more effective, especially for food items that need grease or moisture resistance. This helps reduce food waste and improve packaging performance.

Another growing opportunity is in smart and interactive packaging. By adding QR codes or temperature sensors, companies can give customers product details or freshness updates. These features build trust and enhance user experience, especially in premium segments.

Paper-based and molded fiber packaging is also gaining popularity. These alternatives to plastic are not only biodegradable but are also strong enough for many commercial uses. Fast-food chains, healthcare firms, and retailers are switching to these formats.

Emerging Trends

Simplified, Engaging, and Eco Designs Are Latest Trending Factor

Current trends in the disposables packaging market focus on sustainability, engagement, and minimalism. One exciting trend is the rise of plant-based and edible packaging. These innovations reduce plastic waste and serve dual purposes. For example, edible spoons or seaweed wraps add value and reduce disposal needs.

Brands are also using QR codes and NFC tags to connect with consumers. These tech additions allow customers to scan packages and access product origins, safety data, or promotions. This builds transparency and brand trust while creating an interactive shopping experience.

Another trend is minimalist and lightweight packaging design. By using fewer materials and simple structures, companies reduce costs and environmental impact. Brands like Apple and Unilever have adopted minimalist packaging for both aesthetics and sustainability.

Lastly, there’s growing interest in monomaterial packaging. These packages are made from a single material, like 100% paper or plastic, which makes recycling much easier. This trend supports circular economy goals and simplifies waste sorting for consumers.

Regional Analysis

North America Dominates with 35.6% Market Share

North America leads the Disposables Packaging Market with a 35.6% share, totaling USD 13.96 billion. This strong market position is supported by high demand from the food service industry, fast-paced lifestyles, and the rise in e-commerce packaging. The U.S. and Canada together show consistent use of disposable materials across multiple sectors including food, healthcare, and retail.

Key growth drivers include widespread use of takeout services, especially through food delivery platforms like Uber Eats and DoorDash. Quick-service restaurants and cafes continue to rely heavily on disposable trays, cups, and containers. Supermarkets also promote pre-packaged foods for convenience. In addition, the healthcare industry in the region contributes significantly through the use of disposable medical packaging for hygiene and safety.

Market dynamics are shaped by consumer preference for convenience, hygiene, and single-use packaging. Despite growing awareness about environmental impact, disposable packaging remains in high demand. However, more companies are now using recyclable and biodegradable options to meet regulations and customer expectations. The region’s strong manufacturing and distribution infrastructure ensures easy access to disposable packaging solutions.

Regional Mentions:

- Europe: Europe continues to push sustainable practices in disposable packaging. Countries like Germany and France promote recyclable materials and strict environmental standards. Growth is steady as brands shift to paper-based and plant-based alternatives across food and retail sectors.

- Asia Pacific: Asia Pacific is growing rapidly due to urbanization and rising demand for packaged food. Countries like China, India, and Japan lead in consumption and production of disposable packaging. Street food culture and expanding e-commerce fuel the segment’s growth.

- Middle East & Africa: The Middle East and Africa are seeing steady growth in disposable packaging. Rising tourism, hospitality, and foodservice demand contribute to market expansion. Countries like UAE and South Africa are increasing investment in hygienic packaging solutions.

- Latin America: Latin America is adopting disposable packaging across sectors like food and healthcare. Countries like Brazil and Mexico drive demand through expanding retail markets. Sustainability awareness is rising, pushing local brands to explore biodegradable options.

Key Regions and Countries Covered in the Report

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Landscape

The disposables packaging market is growing due to rising demand in food service, healthcare, and e-commerce. The top four companies—Amcor plc, Berry Global Inc., Sealed Air Corporation, and Mondi Group—lead the market with scale, innovation, and a global footprint.

These companies offer a wide range of disposable packaging solutions, including flexible, rigid, and protective packaging. Their products serve various industries such as food, medical, personal care, and industrial sectors. Their large portfolios allow them to meet different customer needs.

Innovation is a key strength. These companies invest in sustainable packaging materials and advanced technology. Their focus is on reducing plastic waste and offering recyclable or compostable solutions. These efforts support global sustainability goals and appeal to eco-conscious customers.

Strong manufacturing and supply chain capabilities help these players maintain consistent quality and delivery. They operate production sites across multiple countries, ensuring supply efficiency and cost control. This global presence supports their partnerships with multinational clients.

Customer relationships and tailored solutions give them a competitive edge. These companies work closely with clients to design packaging that fits specific brand and product needs. This approach strengthens loyalty and long-term contracts.

Digital tools and automation are also part of their strategy. They use smart packaging, data tracking, and automation to improve performance and customer experience.

In conclusion, the leading companies in the disposables packaging market stand out due to their product range, focus on sustainability, global supply networks, and customer-centered solutions. Their ongoing investment in eco-friendly packaging and advanced technologies keeps them competitive in a fast-changing market.

Major Companies in the Market

- Amcor plc

- Berry Global Inc.

- Sealed Air Corporation

- Mondi Group

- Sonoco Products Company

- Huhtamaki Oyj

- Reynolds Group Holdings Limited

- Constantia Flexibles Group GmbH

- Novolex Holdings, Inc.

- Tetra Pak International S.A.

- WestRock Company

- Bemis Company, Inc. (now part of Amcor)

- Printpack, Inc.

Recent Developments

- International Paper: On March 2025, International Paper set ambitious targets for 2027, aiming for net sales between $26 billion and $28 billion and free cash flow of $2.0 billion to $2.5 billion. To optimize production, the company planned to close seven plants without impacting customer service, following its merger with DS Smith.

- Amcor and Berry Global Group: On November 2024, Amcor announced the acquisition of Berry Global Group through a stock merger valued at approximately $8.4 billion. The merger aims to enhance Amcor’s U.S. presence and capabilities in consumer and health packaging, positioning the combined entity as a leader in the plastic packaging industry.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 39.2 Billion |

| Forecast Revenue (2034) | USD 67.6 Billion |

| CAGR (2025-2034) | 5.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material Type (Plastic, Paper & Paperboard, Aluminum, Glass, Others), By Packaging Type (Rigid Packaging, Flexible Packaging), By Product Type (Trays, Containers, Cups & Lids, Bottles, Pouches & Sachets, Wraps & Films, Others), By End-Use Industry (Food & Beverage, Healthcare, Personal Care & Cosmetics, Industrial, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Amcor plc, Berry Global Inc., Sealed Air Corporation, Mondi Group, Sonoco Products Company, Huhtamaki Oyj, Reynolds Group Holdings Limited, Constantia Flexibles Group GmbH, Novolex Holdings, Inc., Tetra Pak International S.A., WestRock Company, Bemis Company, Inc. (now part of Amcor), Printpack, Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |