Quick Navigation

Market Overview

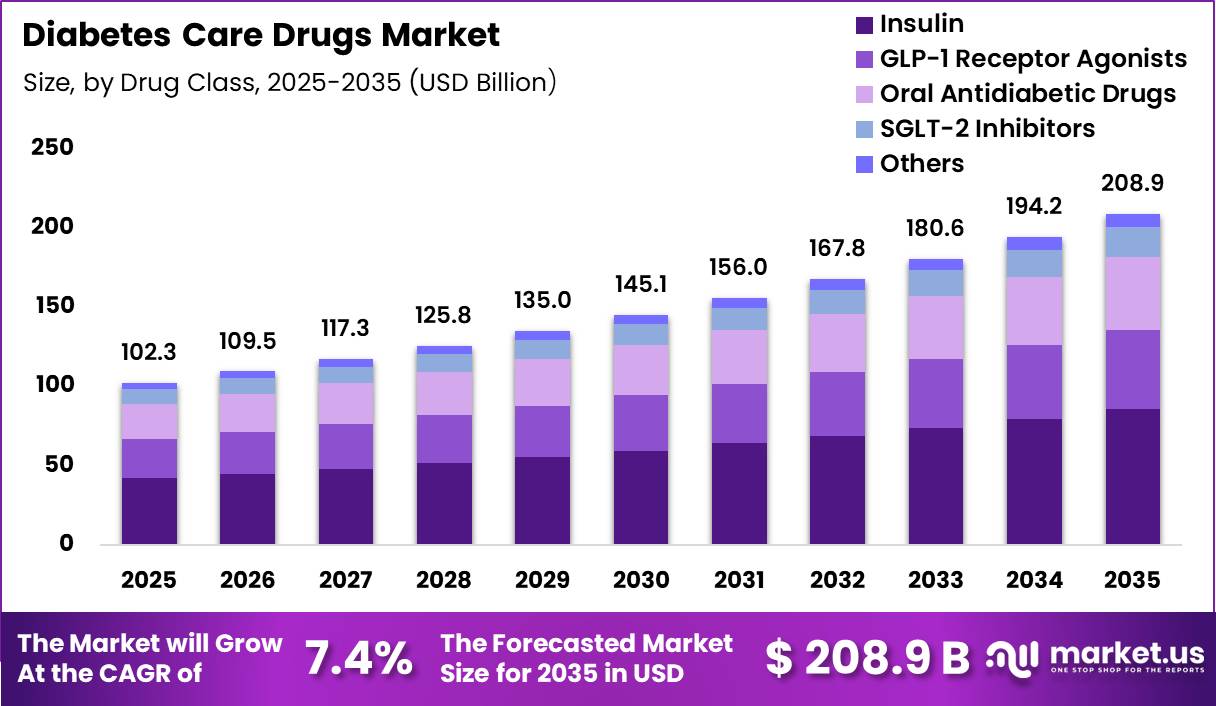

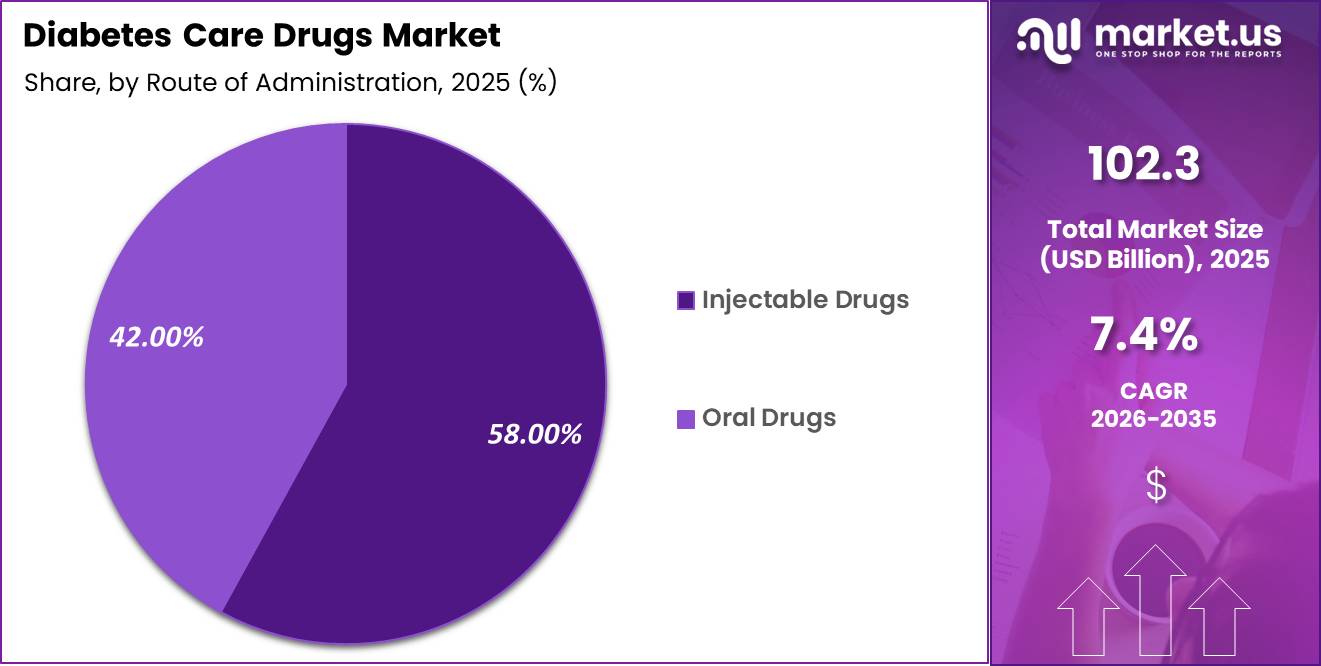

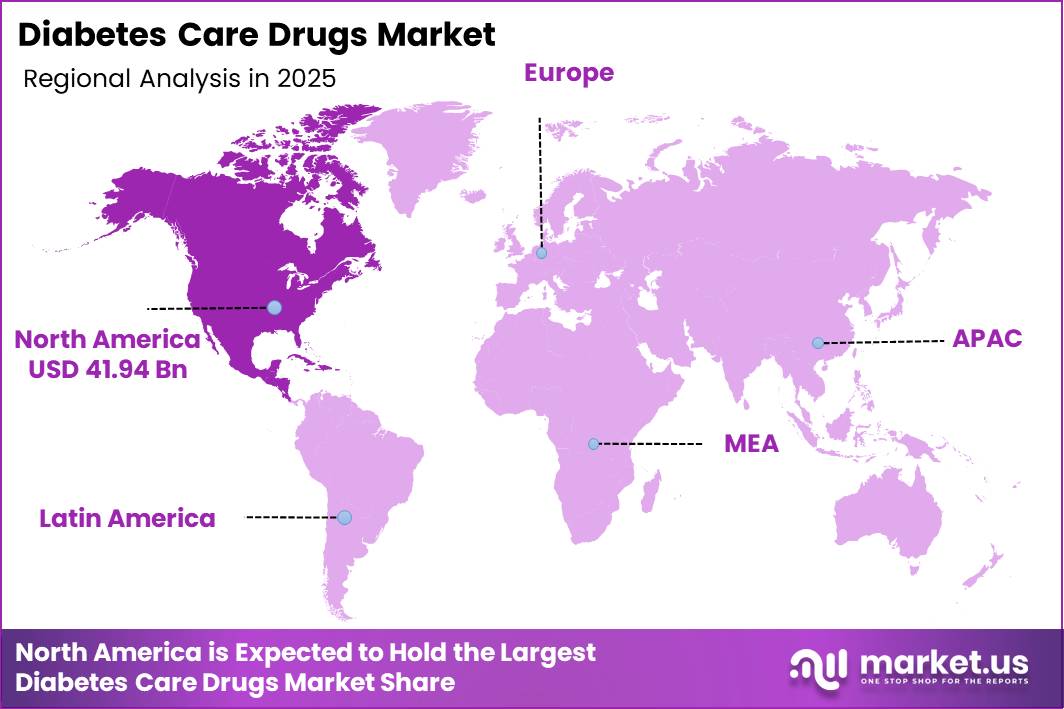

The Global Diabetes Care Drugs Market size is expected to be worth around US$ 208.94 Billion by 2035 from US$ 102.3 Billion in 2025, growing at a CAGR of 7.4% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 41.00% share with a revenue of US$ 41.94 billion.

Diabetes remains one of the most significant global health challenges of the 21st century, driving demand for diabetes care drugs, including insulins, oral hypoglycaemic agents, and newer therapies.

According to the International Diabetes Federation and World Health Organisation, approximately 589 million adults aged 20–79 years are living with diabetes worldwide in 2024, roughly 1 in 9 adults, and this number is projected to rise to 853 million by 2050.

The WHO reports that global diabetes prevalence among adults (18+) has grown from around 7% in 1990 to 14% by 2022, with more than half of adults with diabetes not receiving medication, especially in low and middle-income countries. Insulin and glucose-lowering drugs are essential treatments, and their inclusion on the WHO Model List of Essential Medicines underscores their critical role in care worldwide.

Diabetes is also a substantial economic burden. Global health expenditure attributable to diabetes surpassed USD 1 trillion in 2024, representing about 12% of total global health spending. This includes prescriptions, monitoring, and complications management. In the United States alone, diabetes care accounted for over USD 335 billion in direct medical costs and another USD 305 billion in reduced productivity.

Rising prevalence, increased treatment uptake, and expanded use of advanced therapies (including GLP-1 agonists and biosimilars) are key drivers for the global diabetes care drugs market as nations prioritise broader access to affordable, quality medicines.

Key Takeaways

- Market Size: The Global Diabetes Care Drugs Market size was US$ 102.3 billion in 2025. The market is estimated to grow to US$ 208.9 billion by 2035.

- Market Share: The Compound Annual Growth Rate (CAGR) of the market from 2026 to 2035 will be 7.4%.

- Drug Class: Insulin has the largest market share, accounting for 41% of total drug class revenue.

- Route of Administration: Injectable Drugs leads the segment, accounting for 58% of total route of administration revenue.

- Disease Type: Type 2 Diabetes dominates the segment, accounting for 84% of total disease type revenue.

- Distribution Channel: Retail Pharmacies lead the segment, accounting for 43% of total distribution channel revenue.

- End User: Homecare Settings leads the segment, accounting for 66% of total end-user revenue.

- Drug Type: Branded Drugs dominate the segment, accounting for 71% of total drug type revenue.

- Regional: North America is the dominant regional market, accounting for 41% of global revenue.

Drug Class Analysis

The diabetes care drugs market is segmented by drug class into Insulin, GLP-1 Receptor Agonists, Oral Antidiabetic Drugs (OADs), SGLT-2 Inhibitors, and Others, including DPP-4 inhibitors and amylin analogues.

In 2025, insulin dominates the market with a 41.00% share, reflecting its indispensable role in the management of both Type 1 diabetes and advanced Type 2 diabetes. Long-acting, rapid-acting, and biosimilar insulins continue to support widespread adoption across developed and emerging healthcare systems.

GLP-1 receptor agonists account for 24.00% of the market, driven by their dual benefits in glycemic control and weight management, alongside favourable cardiovascular outcomes. Oral antidiabetic drugs (OADs), including metformin and sulfonylureas, represent 22.00%, supported by affordability, long clinical use, and strong uptake in early-stage Type 2 diabetes.

SGLT-2 inhibitors hold 9.00%, benefiting from increasing use in patients with cardiovascular and renal comorbidities. The remaining 4.00% is attributed to other drug classes, which serve niche patient populations or combination therapy needs. Overall, innovation and therapy diversification continue to reshape drug-class dynamics.

Route of Administration Analysis

Based on the route of administration, the diabetes care drugs market is divided into Injectable Drugs and Oral Drugs. In 2025, injectable drugs dominate with a 58.00% market share, largely due to the extensive use of insulin and injectable GLP-1 receptor agonists.

These therapies remain critical for patients with Type 1 diabetes and those with advanced or poorly controlled Type 2 diabetes, where injectable delivery ensures rapid and predictable therapeutic effects.

Advancements in pen injectors, prefilled devices, and once-weekly injectable formulations have significantly improved patient convenience and adherence, reinforcing the dominance of injectables. Additionally, the growing clinical emphasis on early insulin initiation and combination injectable therapies contributes to sustained demand.

Oral drugs account for 42.00% of the market, driven by their ease of administration, cost-effectiveness, and suitability for early-stage diabetes management. Oral antidiabetic agents such as metformin, DPP-4 inhibitors, and SGLT-2 inhibitors remain first-line or add-on therapies for millions of patients worldwide.

While oral formulations continue to expand, especially in emerging markets, injectable therapies maintain a leading position due to their clinical necessity and broader therapeutic scope.

Disease Type Analysis

By disease type, the diabetes care drugs market is segmented into Type 2 Diabetes, Type 1 Diabetes, and Gestational Diabetes. In 2025, Type 2 diabetes dominates the market with an 84.00% share, reflecting its overwhelming global prevalence and long-term treatment requirements.

Patients with Type 2 diabetes often require lifelong pharmacological management, including oral drugs, injectables, and combination therapies, driving sustained drug consumption.

Lifestyle changes, urbanisation, ageing populations, and rising obesity rates continue to fuel the expansion of Type 2 diabetes, particularly in low- and middle-income regions. The availability of multiple drug classes tailored to disease progression further strengthens this segment’s dominance.

Type 1 diabetes represents a smaller but essential share, as patients are fully dependent on insulin therapy from diagnosis onward. Although the patient population is comparatively limited, high per-patient drug utilisation supports steady demand.

Gestational diabetes accounts for the remaining share, characterised by temporary but critical drug use during pregnancy. Increased screening and awareness are improving diagnosis rates, modestly contributing to market growth. Overall, disease-type segmentation remains heavily skewed toward Type 2 diabetes.

Distribution Channel Analysis

The diabetes care drugs market is segmented by distribution channel into Retail Pharmacies, Hospital Pharmacies, Online Pharmacies, and Speciality Pharmacies.

In 2025, retail pharmacies lead with a 43.00% market share, supported by their widespread presence, easy accessibility, and strong role in dispensing chronic medications. Retail outlets are often the primary source for insulin refills and oral antidiabetic drugs, particularly for long-term outpatient management.

Hospital pharmacies maintain a significant share due to their role in initiating therapy, managing acute cases, and supplying injectable drugs during inpatient care. Online pharmacies are gaining momentum, driven by digital health adoption, home delivery services, and competitive pricing, especially among urban and tech-savvy populations.

Meanwhile, speciality pharmacies focus on high-value injectable drugs and patient support programs, particularly for advanced therapies such as GLP-1 receptor agonists.

Together, these channels form a diversified distribution ecosystem. While retail pharmacies remain dominant, online and speciality channels are expected to expand steadily as healthcare systems emphasise convenience, adherence, and personalised diabetes care delivery.

End User Analysis

Based on end users, the diabetes care drugs market is segmented into Homecare Settings, Hospitals, Clinics & Diabetes Centres. In 2025, home care settings dominate with a 66.00% market share, reflecting the chronic nature of diabetes and the growing emphasis on self-management. Most patients administer insulin or oral medications at home, supported by education programs and user-friendly drug delivery devices.

The expansion of home-based care is further supported by advancements in self-injection pens, continuous glucose monitoring integration, and telemedicine follow-ups.

These factors reduce hospital dependency and promote long-term adherence, particularly among stable patients. Hospitals account for a smaller share, primarily serving newly diagnosed patients, those with complications, or individuals requiring intensive glycemic control.

Clinics and diabetes centres play a critical role in ongoing disease management, therapy optimisation, and patient education. Although institutional care remains essential for complex cases, the dominance of home care settings underscores the shift toward decentralised, patient-centric diabetes treatment models.

Drug Type Analysis

By drug type, the diabetes care drugs market is divided into Branded Drugs and Generic Drugs. In 2025, branded drugs dominate with a 71.00% market share, driven by strong physician preference, extensive clinical evidence, and continuous innovation.

Branded insulin analogues and novel injectable therapies, particularly GLP-1 receptor agonists, command premium pricing due to their enhanced efficacy and safety profiles.

Ongoing research, patent protection, and aggressive product differentiation strategies support the continued dominance of branded drugs. These products are often favoured in developed markets and among patients with comprehensive insurance coverage.

Generic drugs account for 29.00% of the market, playing a vital role in improving affordability and access, especially in cost-sensitive regions. Generic metformin, sulfonylureas, and biosimilar insulins are widely adopted through public healthcare programs. While the generic segment is expanding gradually, branded drugs retain a strong lead due to innovation-driven demand and established brand trust within diabetes care.

Key Market Segments

By Drug Class

- Insulin

- GLP-1 Receptor Agonists

- Oral Antidiabetic Drugs (OADs)

- SGLT-2 Inhibitors

- Others (DPP-4, Amylin Analogues, etc.)

By Route of Administration

- Injectable Drugs

- Oral Drugs

By Disease Type

- Type 2 Diabetes

- Type 1 Diabetes

- Gestational Diabetes

By Distribution Channel

- Retail Pharmacies

- Hospital Pharmacies

- Online Pharmacies

- Specialty Pharmacies

By End User

- Homecare Settings

- Hospitals

- Clinics & Diabetes Centres

By Drug Type

- Branded Drugs

- Generic Drugs

Drivers

The rising diagnosed type 2 diabetes burden, combined with persistent treatment gaps, remains a key market driver because a large share of people living with diabetes still do not receive adequate pharmacological therapy. Growing disease prevalence, increasing diagnosis rates, and expanding screening programs continue to enlarge the pool of patients eligible for treatment.

Significant unmet need remains across emerging and underserved regions, where access to medicines and routine diabetes management is often limited. As healthcare systems improve detection and treatment initiation, millions of additional patients are expected to enter therapy pathways. This trend supports demand for affordable, scalable, and easy-to-administer treatment options that can be delivered through primary-care settings.

It also encourages broader distribution networks, public-health partnerships, and high-volume manufacturing models. Overall, the opportunity is driven by expanding treatment access and conversion of untreated patients into long-term therapy users rather than by prevalence growth alone.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising diagnosed type 2 burden and low treatment coverage | +2.1% | APAC, MENA, LatAm, Africa | Medium term |

| Cardio-renal label expansion for GLP-1 therapies | +1.8% | US, EU5, Japan, China urban | Short term |

| Obesity-diabetes treatment convergence | +1.6% | North America core, EU, GCC, urban APAC | Medium term |

| Earlier diagnosis and screening intensification | +1.2% | China, India, the US, ASEAN, Gulf | Short term |

| Public health targets improving drug access | +1.4% | LMIC corridors, Africa, South Asia, MENA | Long term |

| Shift toward oral and adherence-friendly regimens | +1.0% | India, China, LatAm, EU, US | Medium term |

Challenges

Adherence and persistence erosion remains a significant market challenge because initiating therapy does not always translate into sustained long-term treatment use. Diabetes management often requires continuous medication adherence, lifestyle changes, and regular monitoring, making long-term persistence difficult, particularly in earlier-stage disease where symptoms may be less apparent.

Treatment discontinuation can be driven by factors such as medication side effects, complex dosing schedules, treatment fatigue, affordability concerns, and inconsistent follow-up care.

Poor adherence increases the risk of disease progression and costly complications, reducing both clinical outcomes and the overall effectiveness of healthcare interventions.

As a result, manufacturers and healthcare providers must invest in patient-support programs, simplified treatment regimens, digital engagement tools, and refill-management systems to improve persistence.

Without stronger adherence strategies, growth in patient initiations may not fully convert into sustained treatment utilisation, limiting the market’s ability to realise the full value of its existing patient base.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| GLP-1 capacity balancing | -1.4% | US, EU, Japan, China urban | Medium term |

| Insulin market concentration | -1.2% | LMICs, MENA, Africa, South Asia | Long term |

| Cold-chain continuity gaps | -0.9% | Africa, ASEAN, LatAm, rural India | Medium term |

| Adherence and persistence erosion | -1.0% | US, EU, APAC urban | Short term |

| Primary-care capability mismatch | -0.8% | LMIC corridors, Tier-2 APAC, Africa | Long term |

| Multi-indication pricing strain | -0.7% | US, EU regulatory hubs, OECD Asia | Medium term |

Restraints

Compounding rollback is a near-term market restraint because the end of temporary compounded supply channels reduces treatment access for some patients who previously relied on lower-cost or more accessible alternatives.

As regulatory enforcement returned to normal following the resolution of product shortages, patients were required to transition back to approved commercial therapies through standard prescription and reimbursement pathways.

This shift introduced greater affordability, coverage, and administrative barriers for certain patient groups. Some individuals may discontinue treatment, delay therapy reinitiation, or struggle to move into approved channels, creating short-term demand disruption.

The impact is most pronounced among price-sensitive patients and those facing access challenges. Although the transition improves regulatory oversight, product quality assurance, and supply-chain stability, it can temporarily reduce treatment continuity and slow market growth until patient conversion to approved therapies is completed.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Medicare price resets | -1.3% | US Medicare core, OECD spill-over | Medium term |

| Insulin affordability gap | -1.5% | LMICs, South Asia, Africa, MENA | Long term |

| Formulary gatekeeping | -1.0% | US, EU, Japan, Canada | Short term |

| Compounding rollback | -0.8% | North America core | Short term |

| Analogue price mismatch | -0.7% | Africa, South Asia, LMIC tenders | Medium term |

| Monitoring-device shortfall | -0.6% | LMICs, rural APAC, LatAm | Long term |

Opportunity

Prediabetes Rx conversion is a future growth opportunity because most diabetes-drug revenue is still generated after a formal type 2 diabetes diagnosis, while the much larger prediabetes population remains largely untreated with medication. In the U.S., 97.6 million adults had prediabetes versus 38.1 million with diabetes, creating a substantially larger addressable risk pool.

Even a modest 3–5% conversion of high-risk prediabetic individuals could add roughly 2.9–4.9 million potential treatment candidates. Growth potential lies in payer-supported, risk-stratified prevention programs targeting individuals with obesity, elevated A1c, and cardiometabolic risks.

Such approaches could reduce patient acquisition costs by 20–30% compared with broad direct-to-consumer expansion while supporting value-based pricing through avoided disease progression.

With more than 589 million adults living with diabetes globally and over 40% remaining undiagnosed, companies that establish screening-to-prescription pathways can unlock a significant new revenue layer independent of growth in the diagnosed diabetes population.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Prediabetes Rx conversion | +1.6% | North America core, GCC, urban APAC | Medium term |

| Cardio-renal-metabolic bundles | +1.3% | US, EU5, Japan, China urban | Short term |

| Oral incretin mass-market tiering | +1.9% | India, China, SEA, LatAm | Medium term |

| Women’s metabolic lifecycle plays | +1.1% | US, EU, India, Brazil | Medium term |

| Public-sector tender localisation | +1.4% | India, MENA, Africa, ASEAN | Long term |

| Digital outcomes pricing | +0.9% | US, EU, advanced APAC | Short term |

Regional Analysis

In 2025, North America led the diabetes care drugs market, holding more than 41% of the share with revenues reaching US$ 41.94 billion.

This dominance is attributed to a high prevalence of diabetes, a robust healthcare infrastructure, and widespread access to advanced drug therapies, such as insulin analogues and injectable incretin-based drugs. Favourable reimbursement policies, high diagnosis rates, and strong adoption of innovative branded medications further solidify the region’s leadership.

Europe ranks as the second-largest regional market, driven by an ageing population, a rising incidence of Type 2 diabetes, and strong public healthcare systems. Countries in Western Europe show consistent demand for both oral antidiabetic drugs and injectable therapies, supported by national treatment guidelines and government-backed reimbursement programs. The increasing use of biosimilars is also enhancing affordability and accessibility.

The Asia-Pacific market is experiencing the fastest growth, propelled by rapid urbanisation, lifestyle changes, and a growing diabetic population in countries like China and India. Expanding healthcare coverage and improving diagnosis rates are accelerating the adoption of medications, particularly oral therapies.

Meanwhile, Latin America and the Middle East & Africa contribute smaller but steadily expanding shares to the market. Growth in these regions is driven by improving healthcare access, rising awareness of diabetes, and government-led initiatives for diabetes management, positioning them as emerging opportunities within the global market.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Player Analysis

Suppliers in the global diabetes care drugs market seek a competitive advantage through novel drug class innovation, particularly GLP-1 receptor agonist and SGLT-2 inhibitor platform development, alongside biosimilar insulin portfolio expansion targeting generic market share capture as branded insulin patents expire.

Key strategic focus areas include once-weekly injectable formulation development, reducing patient administration burden, combination therapy product development addressing multiple diabetes management targets simultaneously, and emerging market distribution network expansion reaching underdiagnosed and undertreated diabetic populations across Asia Pacific, Latin America, and the Middle East.

Companies continue investing in patient adherence programs, digital health platform integration enabling connected glucose monitoring and medication management, and real-world evidence generation supporting payer formulary inclusion and reimbursement authorisation across global healthcare systems.

The progressive expansion of GLP-1 receptor agonist indications beyond diabetes into obesity and cardiovascular disease management is creating structurally new premium revenue streams for leading innovator manufacturers while simultaneously expanding the addressable patient population beyond conventional diabetes treatment market boundaries through the forecast period to 2035.

Top Key Players

- Novo Nordisk A/S

- Eli Lilly and Company

- Sanofi S.A.

- Merck & Co., Inc.

- AstraZeneca PLC

- Boehringer Ingelheim GmbH

- Novartis AG

- Pfizer Inc.

- Abbott Laboratories

- Johnson & Johnson

- Sun Pharmaceutical Industries Ltd.

- Dr. Reddy’s Laboratories Ltd.

- Lupin Limited

- Biocon Limited

- Mankind Pharma Ltd.

- Other Key Players

Recent Developments

- In January 2026, Novo Nordisk expanded its once-weekly semaglutide injectable formulation across Asian and Middle Eastern markets, targeting growing Type 2 diabetes patient populations through hospital pharmacy and retail institutional distribution networks.

- In February 2026, Eli Lilly and Company secured expanded reimbursement authorisation for its tirzepatide GLP-1 receptor agonist across five additional European national health service formularies, covering Type 2 diabetes and obesity management indications.

- In March 2026, Biocon Limited launched its biosimilar insulin glargine across North American retail and speciality pharmacy channels, targeting cost-sensitive diabetic patient populations seeking affordable branded insulin alternatives through institutional procurement programs.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 102.30 Billion |

| Forecast Revenue (2035) | US$ 208.94 Billion |

| CAGR (2026-2035) | 7.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Drug Class (Insulin, GLP-1 Receptor Agonists, Oral Antidiabetic Drugs, SGLT-2 Inhibitors, Others), By Route of Administration (Injectable Drugs, Oral Drugs), By Disease Type (Type 2 Diabetes, Type 1 Diabetes, Gestational Diabetes), By Distribution Channel (Retail Pharmacies, Hospital Pharmacies, Online Pharmacies, Specialty Pharmacies), By End User (Homecare Settings, Hospitals, Clinics & Diabetes Centers), By Drug Type (Branded Drugs, Generic Drugs) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Novo Nordisk A/S, Eli Lilly and Company, Sanofi S.A., Merck & Co., Inc., AstraZeneca PLC, Boehringer Ingelheim GmbH, Novartis AG, Pfizer Inc., Abbott Laboratories, Johnson & Johnson, Sun Pharmaceutical Industries Ltd., Dr. Reddy’s Laboratories Ltd., Lupin Limited, Biocon Limited, Mankind Pharma Ltd., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |