Quick Navigation

Market Overview

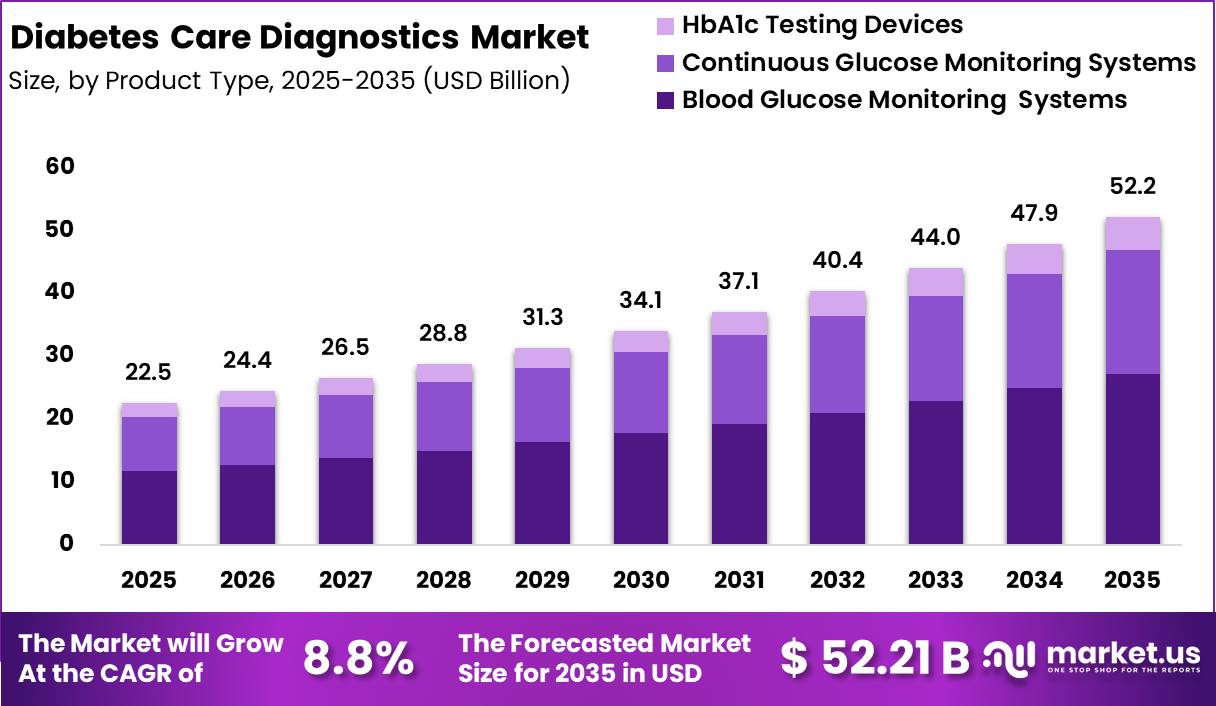

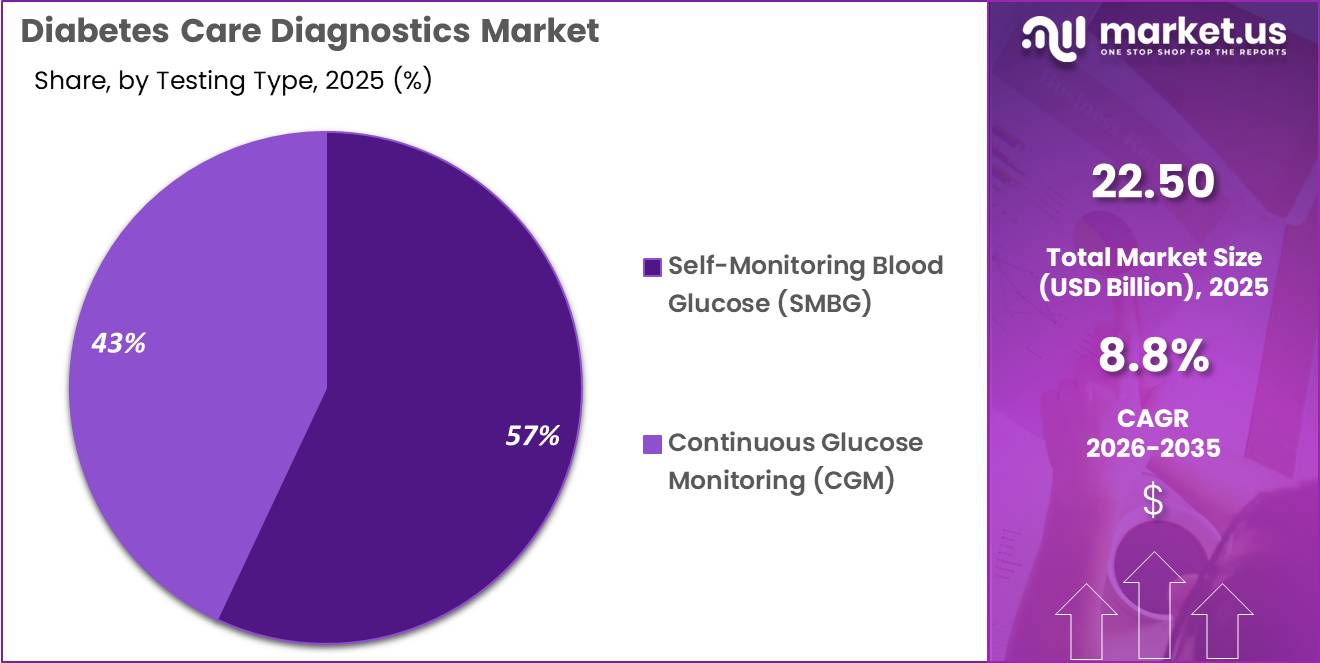

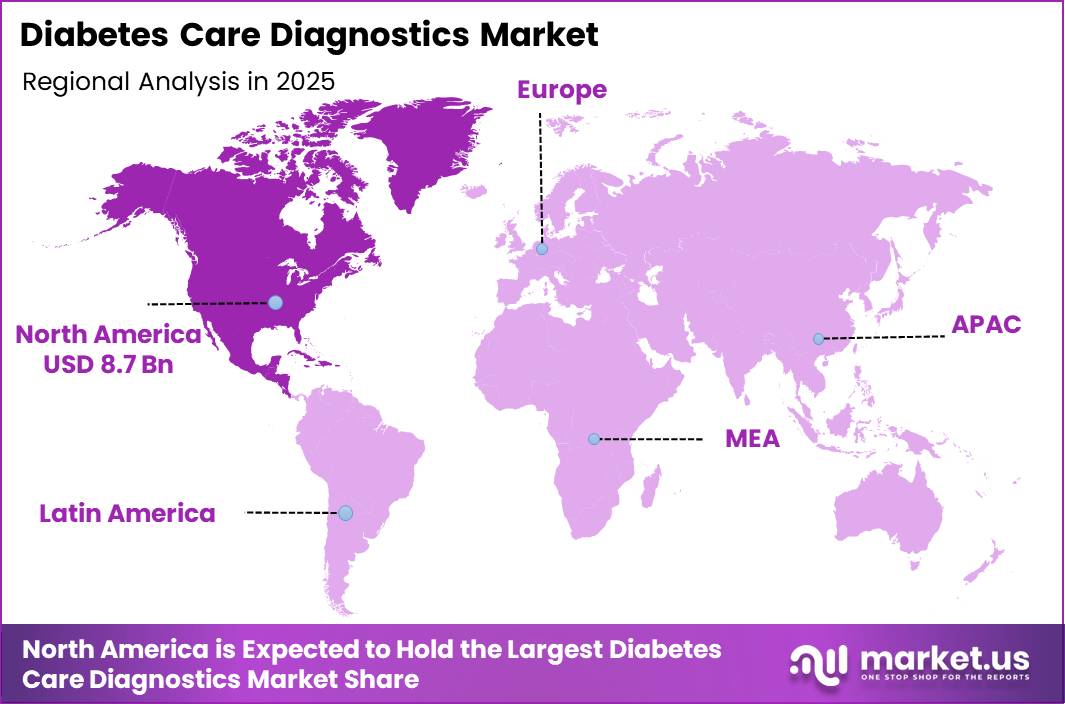

Global Diabetes Care Diagnostics Market size is expected to be worth around US$52.21 Billion by 2035 from US$22.50 Billion in 2025, growing at a CAGR of 8.80% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 39.00% share with a revenue of US$ 8.77 Billion.

Diabetes is a chronic metabolic disease marked by elevated blood glucose levels and is a leading global public health challenge. According to the World Health Organisation, approximately 830 million people worldwide live with diabetes, with many undiagnosed due to lack of screening and care access, particularly in low- and middle-income countries.

Early detection through diagnostics, including blood glucose and glycated haemoglobin (HbA1c) testing, is critical to preventing complications such as cardiovascular disease, kidney failure, and vision loss.

In India, current estimates indicate around 77 million adults are living with diabetes, and another 25 million are in a prediabetic state, with more than half unaware of their condition. Timely diagnosis is essential to reduce the risk of severe complications. National surveys indicate that efforts to improve diagnosis and control are expanding, but gaps in awareness and treatment coverage remain across regions.

In the United States, government data show an estimated 40.1 million people have diagnosed or undiagnosed diabetes, representing about 12% of the population. Among these, about 27.6% of adults with diabetes are unaware of their condition without regular testing.

Diagnostics form the foundation of comprehensive diabetes care. Regular screening for elevated blood glucose and HbA1c levels supports timely management, improves patient outcomes, and helps national health systems monitor disease trends and target interventions effectively.

Key Takeaways

- Market Size: The Global Diabetes Care Diagnostics Market size was US$ 22.5 billion in 2025. The market is estimated to grow to US$ 52.21 billion by 2035.

- Market Share: The Compound Annual Growth Rate (CAGR) of the market from 2026 to 2035 will be 8.8%.

- Product Type: Blood Glucose Monitoring (BGM) Systems has the largest market share, accounting for 52% of total sales.

- Testing Type: Self-Monitoring Blood Glucose (SMBG) dominates the segment, accounting for 57% of total revenue.

- Component: Test Strips lead the segment, accounting for 42% of total revenue.

- Application: Type 2 Diabetes dominates the segment, accounting for 68% of total revenue.

- End User: Home Care Settings leads the segment, accounting for 61% of total revenue.

- Distribution Channel: Retail Pharmacies dominate the segment, accounting for 41% of total revenue.

- Regional: North America is the dominant regional market, accounting for 39% of global sales.

Product Type Analysis

The Glucose Monitoring Devices Market is segmented by product type into Blood Glucose Monitoring (BGM) Systems, Continuous Glucose Monitoring (CGM) Systems, and HbA1c Testing Devices.

In 2025, Blood Glucose Monitoring (BGM) Systems dominate the market with a 52.00% share, driven by their long-standing clinical acceptance, affordability, and widespread availability across both developed and emerging economies. BGM systems are extensively used for routine self-testing and remain the first-line solution for daily glucose checks, particularly among patients with stable diabetes conditions.

Continuous Glucose Monitoring (CGM) Systems account for 38.00% of the market, reflecting rapid adoption due to technological advancements such as real-time glucose tracking, trend analysis, and integration with mobile applications. CGM systems are increasingly preferred by patients requiring intensive glycemic control, especially those with fluctuating glucose levels.

HbA1c Testing Devices represent 10.00% of the market and play a critical role in long-term diabetes management by providing insights into average blood glucose levels over several months. Although their usage frequency is lower compared to daily monitoring tools, they are essential in clinical settings for treatment evaluation and disease progression assessment.

Testing Type Analysis

Based on testing type, the market is divided into Self-Monitoring Blood Glucose (SMBG) and Continuous Glucose Monitoring (CGM). In 2025, Self-Monitoring Blood Glucose (SMBG) dominates with a 57.00% market share, supported by its cost-effectiveness, simplicity, and extensive use in home care settings.

SMBG devices, including glucometers and test strips, enable patients to perform on-demand testing and remain widely prescribed for routine diabetes management.

The dominance of SMBG is particularly evident in regions with high diabetes prevalence and limited access to advanced monitoring technologies. Patients with Type 2 diabetes and those managing their condition through oral medications often rely on SMBG due to lower monitoring frequency requirements.

Continuous Glucose Monitoring (CGM) accounts for 43.00% of the market and continues to grow as awareness of real-time glucose tracking benefits increases. CGM systems reduce the need for frequent finger pricks and provide continuous data, improving treatment adherence and clinical outcomes. Despite higher costs, CGM adoption is expanding among insulin-dependent patients and technologically aware consumers.

Component Analysis

The market is segmented by components into Test Strips, Glucose Meters, Sensors, and Lancets & Lancing Devices. In 2025, Test Strips dominate the component segment with a 42.00% market share, primarily due to their recurring usage and consumable nature. Each blood glucose test requires a new strip, resulting in consistent demand across both SMBG and certain clinical testing environments.

Glucose Meters hold a significant share as essential hardware devices used alongside test strips. While meter replacement cycles are longer, technological improvements such as Bluetooth connectivity and data storage capabilities support steady demand.

Sensors represent a rapidly growing component segment, driven by the increasing adoption of CGM systems. These sensors enable continuous glucose measurement and are replaced periodically, contributing to recurring revenue streams.

Lancets & Lancing Devices play a supporting yet essential role in glucose testing, particularly for SMBG users. Although relatively low-cost, their widespread use across millions of daily tests ensures a stable market presence and sustained demand.

Application Analysis

By application, the market is segmented into Type 2 Diabetes, Type 1 Diabetes, and Gestational Diabetes. In 2025, Type 2 Diabetes dominates with a 68.00% market share, reflecting the global rise in lifestyle-related metabolic disorders. The large patient base, combined with long-term disease management requirements, drives consistent demand for glucose monitoring devices in this segment.

Patients with Type 2 diabetes often rely on SMBG systems for routine monitoring, particularly those managing the condition through diet, oral medications, or non-intensive insulin therapy. The chronic nature of the disease further supports recurring device and consumable usage.

Type 1 Diabetes represents a substantial segment due to the necessity for frequent glucose monitoring and insulin management. CGM systems are increasingly adopted in this group to prevent hypoglycemic events and improve glycemic control.

Gestational Diabetes accounts for a smaller yet important share of the market. Temporary but critical monitoring needs during pregnancy drive device usage in this segment, particularly in clinical and home care settings, to ensure maternal and fetal health.

End User Analysis

Based on end users, the market is segmented into Home Care Settings, Hospitals, and Diagnostic Laboratories. In 2025, Home Care Settings dominate with a 61.00% market share, driven by the growing emphasis on self-management of diabetes and the convenience of at-home testing. Portable devices, easy-to-use interfaces, and remote data tracking capabilities have significantly increased home-based glucose monitoring adoption.

Hospitals account for a notable share due to their role in acute diabetes management, inpatient monitoring, and treatment initiation. Glucose monitoring devices are essential in emergency care, intensive care units, and post-surgical settings.

Diagnostic Laboratories contribute to market demand through periodic HbA1c testing and confirmatory diagnostics. Although testing frequency is lower compared to home use, laboratories play a crucial role in disease diagnosis, therapy assessment, and long-term monitoring, supporting steady utilisation of advanced glucose testing equipment.

Distribution Channel Analysis

The market is segmented by distribution channel into Retail Pharmacies, Hospital Pharmacies, Online Pharmacies, and Diagnostic Centres. In 2025, Retail Pharmacies lead the market with a 41.00% share, supported by their widespread presence, easy accessibility, and strong consumer trust. Retail pharmacies serve as the primary point of purchase for glucometers, test strips, and lancets, especially for home care users.

Hospital Pharmacies represent a significant channel, particularly for newly diagnosed patients and those requiring insulin-dependent therapies. These pharmacies ensure device availability during inpatient care and post-discharge treatment initiation.

Online Pharmacies are experiencing rapid growth due to convenience, competitive pricing, and home delivery services. Increased digital adoption and chronic disease management platforms are accelerating this channel’s expansion.

Diagnostic Centres contribute through bundled testing services and device-linked diagnostics, particularly for HbA1c testing, supporting diversified distribution and market penetration.

Key Market Segments

By Product Type

- Blood Glucose Monitoring (BGM) Systems

- Continuous Glucose Monitoring (CGM) Systems

- HbA1c Testing Devices

By Testing Type

- Self-Monitoring Blood Glucose (SMBG)

- Continuous Glucose Monitoring (CGM)

By Component

- Test Strips

- Glucose Meters

- Sensors

- Lancets & Lancing Devices

By Application

- Type 2 Diabetes

- Type 1 Diabetes

- Gestational Diabetes

By End User

- Home Care Settings

- Hospitals

- Diagnostic Laboratories

By Distribution Channel

- Retail Pharmacies

- Hospital Pharmacies

- Online Pharmacies

- Diagnostic Centers

Driver

Earlier CGM use under the 2026 care standards

The 2026 American Diabetes Association Standards materially strengthen the role of CGM by recommending use from diabetes onset and thereafter for broader insulin-treated and risk-managed populations, which expands the clinically eligible pool beyond intensive insulin users into earlier and more routine care pathways.

This lifts diagnostics demand because CGM adoption increases glucose-data frequency, follow-up review intensity, therapy-adjustment decisions, and linkage to HbA1c and confirmatory testing, rather than functioning as a stand-alone device category.

Commercially, the driver supports a shift from episodic strip-based monitoring toward recurring sensor consumption, app-linked analytics, and provider dashboard integration, improving revenue visibility and accelerating adoption in specialist and high-volume primary-care settings.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Earlier CGM use under the 2026 care standards | +2.4% | North America core, EU developed markets, APAC urban care hubs | Short term (≤ 2 years) |

| Reimbursement-led expansion of monitored patients | +1.9% | U.S. core, Western Europe, Japan | Short term (≤ 2 years) |

| OTC glucose biosensors widening Type 2 access | +1.6% | U.S. core, selected EU digital channels, APAC private-pay cities | Medium term (2-4 years) |

| Rising diabetes prevalence enlarging test volumes | +2.7% | South Asia, China, MENA, North America, Latin America | Long term (≥ 4 years) |

| HbA1c standardisation strengthening lab demand | +1.3% | U.S., EU, Japan, China, India private hospital networks | Medium term (2-4 years) |

| Primary-care screening scale-up in public systems | +1.1% | ASEAN, Africa, Latin America, India | Long term (≥ 4 years) |

Challenge

Regulatory evidence overload

A major challenge in the Diabetes Care Diagnostics Market is the rising compliance burden attached to in vitro diagnostics, because manufacturers and laboratories now face a denser evidence, documentation, and surveillance workload before new assays, connected glucose tools, and workflow upgrades can scale efficiently across regions.

In the US, the FDA’s 2024 final rule set out a staged phaseout approach for laboratory-developed tests across 2025–2028, increasing pressure on laboratories to strengthen complaint handling, registration, listing, labelling, and performance documentation even when the test menu is already clinically embedded.

In Europe, IVDR has moved a much larger share of IVDs into formal third-party conformity assessment, which extends review queues, increases technical file complexity, and forces companies to commit more regulatory staff hours per SKU than under the prior regime.

For diabetes diagnostics suppliers, this does not stop sales today, but it does create a recurring launch-lag effect in which 9–18 months can be lost in dossier upgrades, clinical performance packages, post-market surveillance planning, and notified body coordination, reducing the speed at which new assay menus and digital features convert into revenue.

The modelled drag of about 1.1% points reflects slower portfolio refresh cycles, delayed country rollouts, and heavier fixed compliance costs that are particularly difficult for mid-sized firms to absorb, making regulatory operations, evidence generation, and lifecycle documentation a long-duration strategic capability rather than a back-office function.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Regulatory evidence overload | -1.1% | EU regulatory hubs, US reference labs | Long term (≥ 4 years) |

| Reagent sourcing instability | -0.8% | APAC supply bases, EU, North America | Medium term (2-4 years) |

| Fragmented care data infrastructure | -0.9% | North America, EU, Gulf, Urban Asia | Long term (≥ 4 years) |

| Skilled diagnostics labour gaps | -0.7% | Global hospitals, LatAm, Asia, Africa | Medium term (2-4 years) |

| Affordability-pressure screening gaps | -1.0% | South Asia, Africa, LatAm public systems | Long term (≥ 4 years) |

| Connected-device cyber exposure | -0.5% | Digitised diabetes care markets | Medium term (2-4 years) |

Restraints

Reimbursement tightening

Reimbursement pressure remains one of the most material restraints in the diabetes care diagnostics market because public and private payers are increasingly demanding tighter evidence of clinical utility, lower total cost per monitored patient, and stricter eligibility criteria before expanding coverage for advanced monitoring formats such as CGM and connected diagnostic tools.

In practical terms, this reduces realised pricing through tender-based procurement, rebate-heavy payer contracts, prescription controls, and utilisation caps, especially in developed markets where diagnostic intensity is already high, and payers are trying to contain chronic-care spending.

The quantitative bottleneck is not only a lower net selling price but also slower patient onboarding, delayed renewals, and reduced test frequency in cost-sensitive segments, which together can remove roughly 0.9% points from baseline market CAGR by constraining revenue expansion despite rising diabetes prevalence.

Strategically, this creates margin compression for manufacturers, discourages aggressive commercial expansion into lower-yield accounts, and pushes suppliers to concentrate investment on high-acuity or premium populations rather than broad-based volume growth.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement tightening | -0.9% | North America core, EU | Medium term |

| Regulatory approval burden | -0.8% | EU, UK, selective APAC | Medium term |

| Sensor input cost pressure | -0.7% | NA, EU, APAC corridors | Short term |

| Channel affordability gaps | -0.6% | India, ASEAN, LATAM, Africa | Medium term |

| Supply chain instability | -0.5% | APAC export hubs, LATAM, MEA | Short term |

| Data integration friction | -0.4% | EU, North America, advanced APAC | Long term |

Opportunity

Pharmacy-led PoC expansion

This is an opportunity rather than a current market driver because baseline diabetes diagnostics growth already reflects routine glucose and HbA1c testing within hospitals and physician-linked laboratories.

Whereas the still-underbuilt white space lies in shifting testing access into pharmacy chains, community clinics, and retail point-of-care networks that can capture underdiagnosed and undertested populations, especially across low- and middle-income countries where 81% of adults with diabetes live and roughly 252 million adults remain undiagnosed globally.

A scalable pharmacy-led point-of-care model could target HbA1c, fasting glucose, urine albumin, and lipid checks at a 3–8 dollar price point per encounter, and if it reaches only 8–10% of the undiagnosed or insufficiently monitored pool across India, Southeast Asia, Latin America, and parts of Africa.

It could create a realistic incremental annual testing layer of 1.5–2.0 billion dollars by the early 2030s, with store-level gross margins in the 30–40% range due to low labor intensity and reagent standardization.

The upside exists because this network expansion monetises access gaps that current institutional testing models do not fully serve, and it could lift market growth by roughly 1.1% points above baseline if operators build dense last-mile footprints before reimbursement systems and local diagnostic chains mature.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Pharmacy-led PoC expansion | +1.1% | India, SEA, LATAM, MEA | Short term |

| Home HbA1c subscription kits | +0.9% | North America, the EU, Japan, and Korea | Short term |

| Prediabetes conversion screening | +0.8% | North America, China, India, GCC | Medium term |

| Cardiometabolic test bundling | +0.7% | North America, EU, GCC | Medium term |

| Pregnancy & GDM diagnostics | +0.8% | India, SEA, MENA, Sub-Saharan Africa | Medium term |

| Diabetes data monetisation layers | +0.6% | North America, EU | Long term |

Regional Analysis

In 2025, North America led the Diabetes Care Diagnostics Market, achieving over 39.00% share with revenue of US$8.77 billion, underscoring the region’s strong leadership in diabetes diagnosis and monitoring.

This dominance is supported by a high prevalence of diabetes, a well-developed healthcare infrastructure, and widespread adoption of advanced diagnostic technologies, including self-monitoring blood glucose systems, continuous glucose monitoring, and routine HbA1c testing.

In addition, strong insurance coverage, favourable reimbursement frameworks, and proactive screening programs contribute to sustained demand and early diagnosis across the region. Europe holds a substantial market share, driven by an increasing focus on preventive healthcare and standardised diabetes management protocols.

Government-supported public health initiatives, routine diagnostic testing, and growing awareness of early disease detection support stable demand across both Western and Eastern Europe. The region also benefits from strong clinical guidelines emphasising regular HbA1c monitoring and long-term disease management.

The Asia-Pacific region is emerging as the fastest-growing market, fueled by a rapidly expanding diabetic population, urbanisation, and lifestyle changes. Improving healthcare access, rising healthcare expenditure, and government-led awareness programs are accelerating the adoption of glucose monitoring and diagnostic solutions, particularly in densely populated countries.

Latin America, the Middle East & Africa represent smaller but steadily growing markets. Ongoing improvements in diagnostic infrastructure, increasing healthcare investments, and rising awareness of diabetes management are gradually strengthening market penetration in these regions.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Player Analysis

Competitive advantage in the global diabetes care diagnostics market is achieved through continuous glucose monitoring technology innovation, integrated digital health platform development connecting glucose data with mobile applications and clinical decision support systems, and established distribution relationships spanning retail pharmacies, hospital pharmacies, and direct-to-consumer e-commerce channels.

Top Key Players

- Abbott Laboratories

- Dexcom

- Roche Diagnostics

- Medtronic

- Ascensia Diabetes Care

- LifeScan

- B. Braun

- ARKRAY

- Terumo Corporation

- Nova Biomedical

- Siemens Healthineers

- AgaMatrix

- Trividia Health

- Ypsomed

- Senseonics Holdings

- Other Key Players

Recent Developments

- In February 2026, Dexcom introduced a new integrated digital health platform connecting its CGM systems with mobile application-based predictive analytics, targeting Type 1 and Type 2 diabetes patients seeking proactive glucose trend management.

- In March 2026, Roche Diagnostics expanded its blood glucose monitoring system portfolio with new connected glucose meter technology, targeting retail pharmacy and home care distribution channels across European and North American markets.

- In April 2026, Medtronic secured a multi-year distribution agreement with a leading Asian retail pharmacy network covering its CGM and BGM product portfolio, expanding its institutional presence across home care and hospital-based diabetes management settings in the region.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 22.50 Billion |

| Forecast Revenue (2035) | US$ 52.21 Billion |

| CAGR (2026-2035) | 8.80% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Blood Glucose Monitoring (BGM) Systems, Continuous Glucose Monitoring (CGM) Systems, HbA1c Testing Devices), By Testing Type (Self-Monitoring Blood Glucose (SMBG), Continuous Glucose Monitoring (CGM)), By Component (Test Strips, Glucose Meters, Sensors, Lancets & Lancing Devices), By Application (Type 2 Diabetes, Type 1 Diabetes, Gestational Diabetes), By End User (Home Care Settings, Hospitals, Diagnostic Laboratories), By Distribution Channel (Retail Pharmacies, Hospital Pharmacies, Online Pharmacies, Diagnostic Centers) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Abbott Laboratories, Dexcom, Roche Diagnostics, Medtronic, Ascensia Diabetes Care, LifeScan, B. Braun, ARKRAY, Terumo Corporation, Nova Biomedical, Siemens Healthineers, AgaMatrix, Trividia Health, Ypsomed, Senseonics Holdings, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |