Quick Navigation

Report Overview

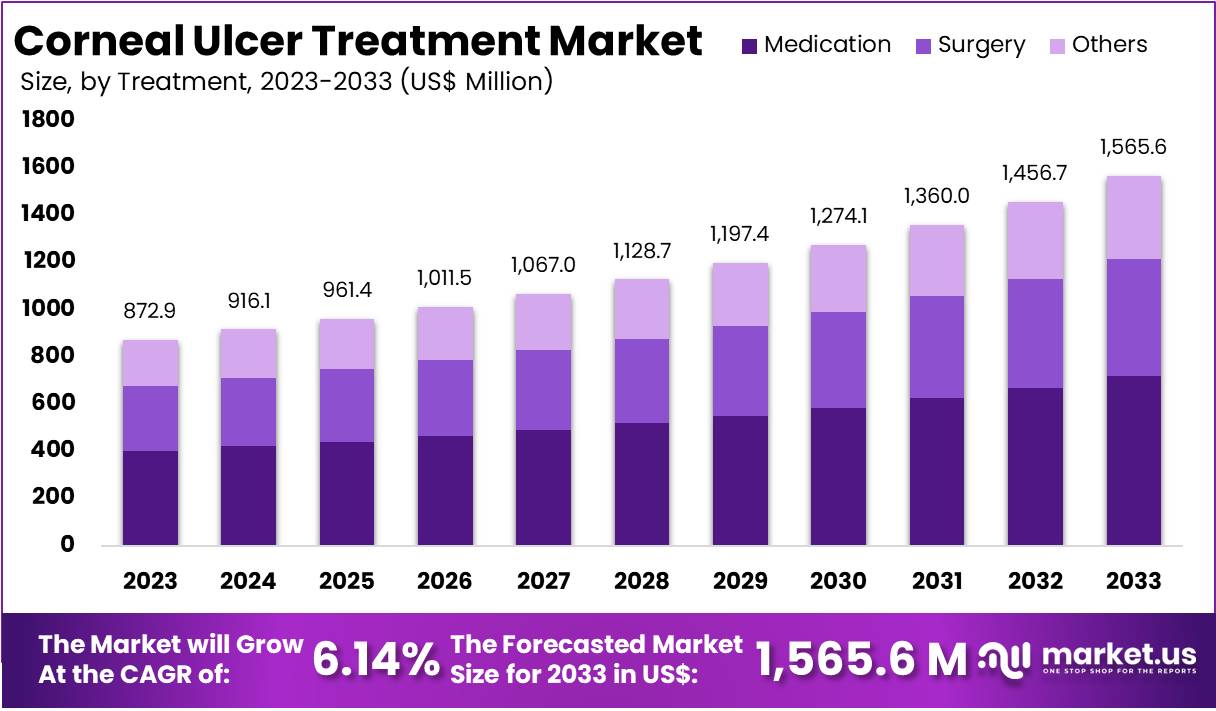

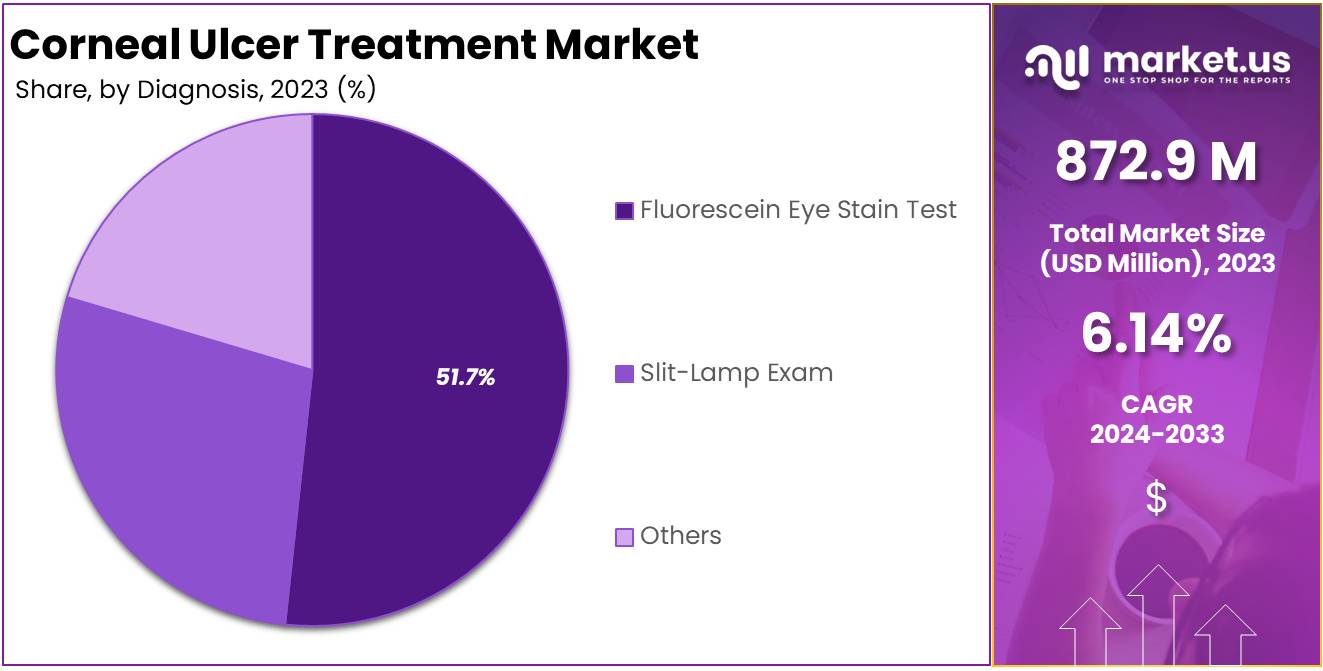

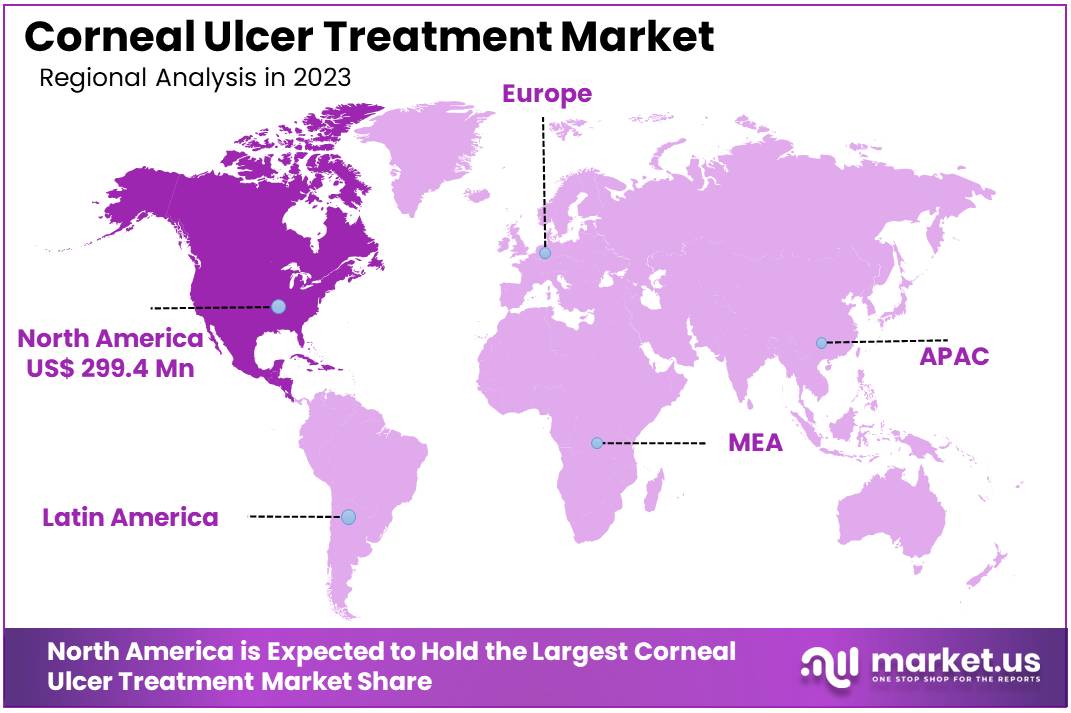

The Global Corneal Ulcer Treatment Market size is expected to be worth around US$ 1565.6 Million by 2034, from US$ 872.9 Million in 2024, growing at a CAGR of 6.14% during the forecast period from 2025 to 2034. North America held a dominant market position, capturing more than a 34.30% share and holds US$ 299.4 Million market value for the year.

Corneal ulcer treatment involves the medical management of an open sore or erosion on the cornea, which is the transparent front surface of the eye. Corneal ulcers often develop due to infections, injuries, or underlying eye conditions. Treatment strategies aim to reduce infection, encourage healing, and prevent vision impairment. Effective management often includes antibiotics, anti-inflammatory medications, and advanced therapies designed to accelerate recovery and improve clinical outcomes.

The corneal ulcer treatment sector has witnessed substantial growth, driven by advancements in regenerative medicine. For instance, plasma rich in growth factors (PRGF) eye drops have emerged as an innovative therapy. These eye drops are derived from a patient’s blood and contain growth factors and cytokines that promote tissue regeneration and reduce inflammation. PRGF has shown promise in treating persistent corneal epithelial defects and neurotrophic keratitis, conditions that are challenging to manage with conventional therapies.

Another notable development is the approval of cenegermin eye drops, a recombinant human nerve growth factor. According to clinical studies, cenegermin effectively treats moderate to severe neurotrophic keratitis by stimulating nerve healing and restoring corneal integrity. This targeted therapy highlights the sector’s focus on biologically driven treatments, offering improved outcomes for patients with chronic corneal damage. Additionally, the integration of blood-derived products, such as autologous serum eye drops, has gained traction. These solutions provide essential nutrients and growth factors that support corneal epithelial healing, reflecting a shift towards personalized eye care.

The prevalence of corneal ulcers has further fueled demand for improved treatment options. According to the National Institutes of Health, the United States records between 30,000 to 75,000 cases of corneal ulcers annually. Notably, 12.2% of all corneal transplants are performed to manage infectious keratitis, emphasizing the significance of effective treatment strategies. However, treatment adherence remains inconsistent. A study published in PubMed Central revealed that less than 20% of corneal ulcer cases are managed following standard guidelines, while 48.7% of patients received antibiotic therapy without prior cultures, highlighting gaps in clinical practices.

The economic burden of corneal ulcer treatment is considerable. For example, in India, healthcare costs vary significantly depending on the timing and setting of treatment. Early intervention at vision centers averages INR 70 per patient, whereas delayed treatment at tertiary centers can increase costs to INR 21,100 per patient. This disparity underscores the importance of early diagnosis and prompt treatment to minimize financial strain on patients and healthcare systems.

Clinical outcomes for corneal ulcers vary based on treatment approaches. For instance, a study reported that 56.1% of patients achieved complete epithelialization within two weeks post-treatment. Furthermore, 60% experienced healing within one month, while 78% achieved full recovery within three months. These findings highlight the need for improved adherence to treatment protocols to enhance recovery rates and reduce complications.

Key Takeaways

- Market Growth: The global corneal ulcer treatment market is projected to reach US$ 1,565.6 million by 2034, growing at a CAGR of 6.14%.

- Treatment Segment: In 2023, medications dominated the treatment segment, accounting for over 45.9% of the market share.

- Diagnosis Segment: The fluorescein eye stain test led the diagnosis segment in 2023, securing more than a 51.7% market share.

- Symptoms Segment: Severe pain emerged as the dominant symptom in 2023, holding a substantial 31.8% market share.

- Dosage Segment: Tablets dominated the dosage segment in 2023, capturing over 41.2% of the market share.

- Route of Administration: Oral administration led this category in 2023, contributing to over 56.2% of the market share.

- End Users Segment: Hospitals held a commanding position in 2023, accounting for more than 56.2% of the total market share.

- Distribution Channel: Hospital pharmacies dominated the distribution channel segment in 2023, securing over 55.1% of the market share.

- Regional Analysis: North America led the global market in 2023, with a 34.3% share and a market value of US$ 299.4 million.

Treatment Analysis

In 2023, Medication held a dominant market position in the Treatment Segment of Corneal Ulcer Treatment, capturing more than a 45.9% share. This was largely due to the extensive use of antibiotic, antifungal, and antiviral eye drops. These medications are often the primary treatment choice because they effectively control infections and promote faster healing. Their ease of use and availability further contributed to their widespread adoption. As a result, medication remains the preferred solution for managing corneal ulcers.

Surgical treatments are another key option in corneal ulcer management. Procedures like corneal transplantation are often recommended for severe cases that do not respond to medications. Although surgery is crucial for advanced conditions, it is less common due to its higher costs and extended recovery periods. However, technological advancements have improved surgical outcomes, supporting gradual growth in this segment. As surgical methods become more refined, their role in treating complex cases is expanding.

The Others category includes alternative therapies such as amniotic membrane transplantation and therapeutic contact lenses. These methods are gaining attention for their ability to aid recovery in stubborn or slow-healing cases. Although this segment holds a smaller market share, ongoing innovations are improving their effectiveness. As research advances, these alternative approaches are expected to play a larger role in corneal ulcer treatment.

Diagnosis Analysis

In 2023, Fluorescein Eye Stain Test held a dominant market position in the Diagnosis Segment of Corneal Ulcer Treatment, capturing more than a 51.7% share. This diagnostic method is widely preferred for its efficiency and ease of use. The test involves placing a special dye in the eye, which highlights corneal damage under blue light. Its fast results make it ideal for emergency cases where immediate diagnosis is crucial. This has contributed significantly to its market dominance.

The slit-lamp exam is another important method used for diagnosing corneal ulcers. This technique allows detailed examination of the eye’s structures, enabling specialists to assess the size, depth, and severity of ulcers. Due to its accuracy, ophthalmologists frequently rely on this method for in-depth evaluation. The slit-lamp exam is commonly performed in specialized clinics and hospitals. Its ability to provide precise insights makes it a valuable tool in complex corneal ulcer cases.

Other diagnostic methods, such as microbial cultures and confocal microscopy, are also gaining importance. These advanced techniques help identify the specific cause of the ulcer, including bacterial, viral, or fungal infections. While not as widely used as the Fluorescein Eye Stain Test or slit-lamp exam, they are essential in cases where standard tests yield unclear results. These methods are often recommended for persistent or severe corneal ulcers that require detailed investigation.

Symptoms Analysis

In 2023, Severe Pain held a dominant market position in the Symptoms Segment of Corneal Ulcer Treatment, capturing more than a 31.8% share. Severe pain is often the most alarming symptom, prompting patients to seek urgent medical care. This symptom is linked to serious corneal damage, which can significantly affect vision if left untreated. Due to its severity, healthcare providers frequently prescribe intensive treatments such as antibiotic drops, antifungal medications, and corticosteroids to manage pain and control infection.

Redness and discharge from the eye are also key symptoms driving the demand for corneal ulcer treatments. These symptoms commonly appear in the early stages, encouraging patients to seek medical evaluation. Early intervention helps prevent complications, reducing the risk of vision impairment. Treatment for these symptoms often involves antimicrobial drops and lubricants to ease discomfort. As awareness about eye health increases, timely diagnosis and treatment have become more accessible in various healthcare settings.

Additional symptoms such as blurry vision, swollen eyelids, and vision changes further contribute to treatment demand. These symptoms can disrupt daily activities, motivating patients to pursue medical care. Blurry vision, in particular, is a serious concern as it may indicate progressing infection or corneal scarring. Advances in diagnostic tools and improved treatment methods are enhancing patient outcomes, supporting the overall growth of the corneal ulcer treatment market.

Dosage Analysis

In 2023, Tablet held a dominant market position in the Dosage Segment of Corneal Ulcer Treatment, capturing more than a 41.2% share. Tablets are widely used for treating severe corneal ulcers due to their systemic action. They effectively target deeper infections that topical treatments may not reach. Healthcare providers often combine tablets with eye drops or ointments to improve treatment outcomes. This combination therapy helps manage complex infections and supports faster recovery.

Eye drops also play a crucial role in corneal ulcer treatment. They are commonly recommended for mild to moderate cases. Eye drops provide direct application to the infected area, ensuring fast relief with fewer side effects. They are often prescribed for early-stage infections or as a preventive solution following minor eye injuries. Due to their ease of use and minimal discomfort, eye drops are widely accepted in outpatient care settings.

Other dosage forms, such as ointments and injectables, account for the remaining market share. These options are generally used in more complex cases that require enhanced drug retention. Ointments are valued for their prolonged contact with the eye’s surface, while injectables provide targeted treatment for severe conditions. These alternatives are essential for managing persistent infections or patients with compromised immune systems.

Rout Of Administration Analysis

In 2023, Oral held a dominant market position in the Route of Administration Segment of Corneal Ulcer Treatment, capturing more than a 56.2% share. This dominance is linked to the convenience and effectiveness of oral medications. Oral treatments are widely prescribed for severe or deep corneal ulcers where localized therapies may not be sufficient. Their ability to provide consistent therapeutic effects throughout the body makes them a preferred choice for healthcare providers.

Topical treatments also play a significant role in managing corneal ulcers. These include antibiotic and antiviral eye drops, which deliver medication directly to the affected area. Topical treatments are often recommended for mild to moderate cases due to their targeted action. They are known for minimizing systemic side effects, making them a safe option for many patients. Additionally, their availability and fast-acting relief contribute to their popularity in clinical use.

Other administration methods, such as injectable treatments, are reserved for severe cases requiring intensive care. These approaches are often used when oral or topical therapies fail to deliver desired results. While less common, injectable treatments are crucial in treating aggressive infections or complications. Healthcare providers may also combine multiple treatment methods to improve outcomes, particularly in complex corneal ulcer cases.

End Users Analysis

In 2023, Hospital held a dominant market position in the End Users Segment of Corneal Ulcer Treatment, capturing more than a 56.2% share. This strong presence is due to hospitals’ access to advanced diagnostic tools and specialized ophthalmic care. Hospitals employ experienced healthcare professionals who manage severe corneal ulcer cases efficiently. Their ability to provide immediate treatment and handle complex cases has reinforced their leadership in the market.

Clinics also held a significant share in the Corneal Ulcer Treatment market. These facilities are often preferred by patients seeking quick consultations and less intensive care. Clinics are known for their convenience, shorter waiting times, and effective outpatient services. As a result, they are increasingly becoming a popular choice for early-stage corneal ulcer treatments or follow-up care, contributing notably to the market’s growth.

Other end-user segments, such as specialized eye care centers and ambulatory surgical units, have also contributed to the market. These facilities offer focused treatment for complex eye conditions and provide essential post-surgical care. With advancements in treatment techniques and improved awareness, their role is expected to expand further in the coming years. This segment continues to support the growing demand for effective corneal ulcer treatments.

Distribution Channel Analysis

In 2023, Hospital Pharmacy held a dominant market position in the Distribution Channel Segment of Corneal Ulcer Treatment, capturing more than a 55.1% share. This strong presence is due to the availability of specialized medications and professional healthcare support in hospital settings. Hospital pharmacies play a crucial role in ensuring patients have access to effective treatments, especially for urgent or severe corneal ulcer cases. Their ability to provide immediate care makes them a preferred option for many patients.

The rising prevalence of corneal ulcers has further increased the demand for hospital pharmacies. These facilities often offer comprehensive care, including expert consultations and specialized prescriptions. Patients seeking urgent treatment or complex therapies are more likely to rely on hospital pharmacies. This trend has contributed to their significant share in the distribution channel landscape. Moreover, hospital pharmacies are known for maintaining better stock levels of essential eye care medications.

While hospital pharmacies lead the segment, retail and online pharmacies are also growing. Retail pharmacies offer convenience for patients with stable conditions, providing easy access to common medications. Meanwhile, online pharmacies are gaining popularity due to home delivery services and cost-effective pricing. However, hospital pharmacies continue to hold a dominant position as they cater to critical cases requiring immediate treatment and professional supervision.

Key Market Segments

By Treatment

- Medication

- Surgery

- Others

By Diagnosis

- Fluorescein Eye Stain Test

- Slit-Lamp Exam

- Others

By Symptoms

- Redness

- Tears

- Discharge from Eye

- Blurry Vision

- Swollen Eyelids

- Vision Changes

- Severe Pain

- Others

By Dosage

- Eye Drops

- Tablet

- Others

By Rout Of Administration

- Oral

- Topical

- Others

By End Users

- Clinic

- Hospital

- Others

By Distribution Channel

- Hospital Pharmacy

- Retail Pharmacy

- Online Pharmacy

Drivers

Rising Prevalence of Eye Infections

The rising prevalence of eye infections is a significant factor driving the demand for corneal ulcer treatments. Bacterial, fungal, and viral infections are increasingly common, contributing to a higher incidence of corneal ulcers. Poor hygiene practices, such as improper handwashing or unsanitary conditions, have heightened infection risks. Additionally, individuals who frequently touch their eyes without proper care may face a higher likelihood of developing infections, further driving the need for effective treatment options.

Contact lens misuse is another critical factor contributing to the surge in eye infections. Extended wear, inadequate cleaning, or improper storage of contact lenses can lead to bacterial contamination. Moreover, individuals with diabetes are more susceptible to infections due to compromised immune systems. As diabetes rates continue to rise globally, the risk of developing eye infections also increases, further supporting the demand for corneal ulcer treatments in healthcare settings.

Restraints

High Treatment Costs

High treatment costs remain a significant restraint in the corneal ulcer treatment market. Advanced procedures, including corneal transplants and specialized antimicrobial therapies, are often expensive. These treatments require skilled healthcare professionals, advanced medical facilities, and costly medications. As a result, access to such therapies is often restricted in low- and middle-income regions. This financial barrier limits the adoption of advanced treatments, impacting overall market growth in these areas.

In many developing regions, healthcare systems face budget constraints, making it challenging to allocate resources for costly treatments. Patients in these regions may struggle to afford expensive medications or surgical procedures, further limiting access. Additionally, limited insurance coverage in some countries increases the financial burden on patients. This disparity in treatment accessibility highlights a significant challenge for the corneal ulcer treatment market, particularly in underserved regions where affordable care options are crucial.

Opportunities

Advancements in Drug Delivery Systems

Advancements in drug delivery systems are creating new opportunities in the healthcare market. Innovations such as sustained-release ocular implants are improving treatment outcomes. These implants deliver medication gradually, ensuring consistent drug levels in the eye. This method reduces the need for frequent dosing, improving patient convenience and adherence. Such advancements are particularly beneficial for chronic eye conditions that require long-term treatment, enhancing overall patient outcomes and supporting market growth.

In addition, nano-formulations are gaining attention for their targeted drug delivery capabilities. These formulations enhance drug absorption and ensure precise medication delivery to affected areas. By improving bioavailability and reducing side effects, nano-formulations offer effective treatment solutions for various ocular conditions. This innovation is expected to drive demand in the market, especially for conditions that require controlled and sustained medication release. As a result, the integration of these advanced delivery systems is contributing significantly to the expansion of the healthcare sector.

Trends

Increased Focus on Combination Therapies

Healthcare providers are increasingly adopting combination therapies to improve treatment outcomes. This approach involves integrating antibiotics, antifungals, and anti-inflammatory drugs to target multiple infection pathways. By combining these medications, healthcare professionals can enhance the efficacy of treatments. This method is particularly effective in managing complex infections, where a single therapy may prove insufficient. Additionally, combination therapies help reduce the risk of developing drug resistance, which is a growing concern in clinical practice.

The rising adoption of combination therapies is driven by their ability to address multiple treatment challenges simultaneously. For instance, antibiotics combat bacterial infections, while antifungals control fungal growth. Anti-inflammatory drugs further aid in reducing tissue inflammation and promoting recovery. This integrated treatment method is becoming essential in managing severe or persistent infections. As healthcare providers seek improved patient outcomes, combination therapies are expected to gain more prominence in clinical settings.

Regional Analysis

In 2023, North America held a dominant market position, capturing more than a 34.30% share and holds US$ 299.4 million market value for the year. This strong presence is largely due to the region’s advanced healthcare infrastructure. Medical facilities in North America are well-equipped with modern technologies, ensuring improved diagnosis and treatment for corneal ulcers. Additionally, awareness campaigns about eye health play a crucial role in encouraging early treatment, further strengthening the market.

The rising number of corneal ulcer cases in North America has contributed significantly to market growth. Factors such as excessive screen time, frequent use of contact lenses, and environmental pollutants are key contributors to eye-related infections. These rising health concerns have created a greater demand for advanced treatment options. As a result, pharmaceutical companies are actively developing innovative therapies to meet this growing need.

Government initiatives have further supported the growth of the corneal ulcer treatment market in North America. Regulatory bodies such as the U.S. Food and Drug Administration (FDA) play an essential role in approving effective treatments. Their support encourages pharmaceutical firms to invest in new therapies. This regulatory framework ensures that patients have access to safe and efficient treatments, driving market expansion.

The presence of prominent pharmaceutical companies and research institutions in North America has also contributed to its market dominance. These organizations are consistently investing in research and development to improve treatment methods. By launching advanced therapies, they cater to the increasing demand for effective corneal ulcer treatments. This combination of innovation, investment, and healthcare support continues to position North America as a leading region in the global corneal ulcer treatment market.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The Corneal Ulcer Treatment Market is supported by several major pharmaceutical companies contributing to product development and treatment advancements. Pfizer Inc. is a significant player with a wide range of anti-infective medications and ophthalmic solutions. The company’s focus on innovation strengthens its presence in the market. Similarly, GlaxoSmithKline plc (GSK) offers effective antimicrobial and antiviral therapies. GSK’s expertise in treating bacterial and viral infections positions it as a key contributor to corneal ulcer management.

Sanofi actively participates in the market with its range of anti-inflammatory and immune-modulating drugs. The company’s continuous efforts to expand its ophthalmology portfolio have improved treatment options for corneal ulcers. Meanwhile, Novartis AG is recognized for its strong ophthalmology division, focusing on innovative eye care solutions. The company’s research in ocular diseases supports advancements in corneal ulcer therapies. Both Sanofi and Novartis are key players driving improved patient outcomes.

Allergan plays a crucial role in ophthalmic care, offering a comprehensive range of eye care products. The company’s investment in research helps develop effective corneal ulcer treatments. Additionally, Other Key Players are actively expanding their presence through strategic partnerships and acquisitions. These companies are enhancing treatment accessibility and ensuring competitive growth within the corneal ulcer treatment sector.

Market Key Players

- Pfizer Inc.

- GlaxoSmithKline plc

- Sanofi

- Novartis AG

- Allergan

- Merck & Co. Inc.

- Mylan N.V.

- Teva Pharmaceutical Industries Ltd.

- Bayer AG

- Sun Pharmaceutical Industries Ltd.

- Aurobindo Pharma

- Lupin

- AbbVie Inc.

- Cumberland Pharmaceuticals Inc.

- Melinta Therapeutics LLC

- Eli Lilly and Company

- Cipla Inc.

- Dr. Reddy’s Laboratories Ltd.

- AstraZeneca

- Johnson & Johnson Private Limited

Recent Developments

- October 2024: Sanofi reported a notable increase in its business EPS guidance for 2024, attributed to strong sales performance, which included a 15.7% sales growth in Q3 2024. Although this development is not directly linked to corneal ulcer treatment, the company’s improved financial position may enhance its capacity to invest in ophthalmic research and development initiatives.

- June 2023: Novartis disclosed an agreement to divest its ‘front of eye’ ophthalmology assets to Bausch + Lomb. The transaction, valued at up to USD 2.5 billion, included USD 1.75 billion in upfront cash along with additional milestone payments. The deal encompassed the sale of Xiidra, a treatment for dry eye disease, along with other assets related to ocular surface conditions. While not directly focused on corneal ulcers, this strategic move highlights Novartis’ efforts to prioritize key therapeutic areas.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 872.9 Million |

| Forecast Revenue (2033) | US$ 1565.6 Million |

| CAGR (2024-2033) | 6.14% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Treatment (Medication, Surgery, Others), By Diagnosis (Fluorescein Eye Stain Test, Slit-Lamp Exam, Others), By Symptoms (Redness, Tears, Discharge from Eye, Blurry Vision, Swollen Eyelids, Vision Changes, Severe Pain, Others), By Dosage (Eye Drops, Tablet, Others), By Rout Of Administration (Oral, Topical, Others), By End Users (Clinic, Hospital, Others), By Distribution Channel (Hospital Pharmacy, Retail Pharmacy, Online Pharmacy) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Pfizer Inc., GlaxoSmithKline plc, Sanofi, Novartis AG, Allergan, Merck & Co. Inc., Mylan N.V., Teva Pharmaceutical Industries Ltd., Bayer AG, Sun Pharmaceutical Industries Ltd., Aurobindo Pharma, Lupin, AbbVie Inc., Cumberland Pharmaceuticals Inc., Melinta Therapeutics LLC, Eli Lilly and Company, Cipla Inc., Dr. Reddy’s Laboratories Ltd., AstraZeneca, Johnson & Johnson Private Limited |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |