Quick Navigation

Report Overview

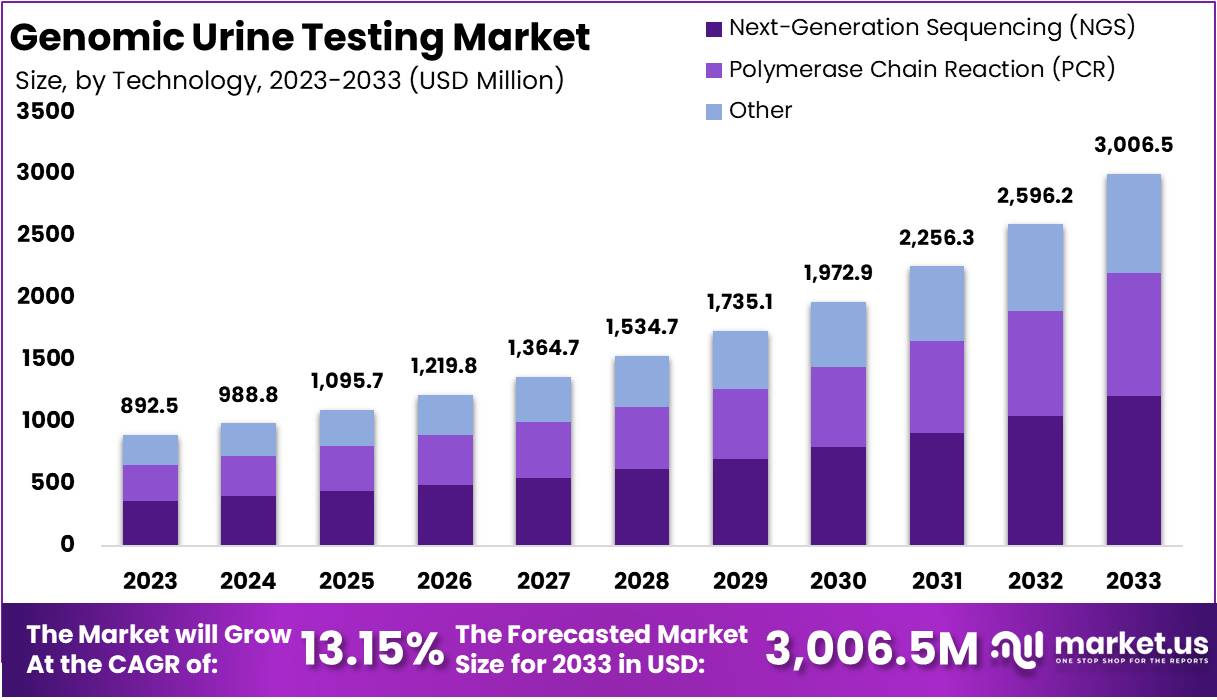

The Global Genomic Urine Testing Market size is expected to be worth around US$ 3006.5 Million by 2033, from US$ 892.5 Million in 2023, growing at a CAGR of 13.15% during the forecast period from 2024 to 2033. North America held a dominant market position, capturing more than a 33.18% share and holds US$ 296.11 Million market value for the year.

Genomic urine testing is a sophisticated diagnostic technique that analyzes genetic material such as DNA and RNA present in urine samples. This non-invasive method is gaining prominence in medical diagnostics, particularly for detecting bladder cancer. The technique identifies genetic mutations, biomarkers, and molecular indicators associated with various health conditions, providing valuable insights for early detection and monitoring.

Advancements in genomic technologies have played a significant role in improving genomic urine testing. According to a study, the development of next-generation sequencing (NGS) has enhanced the ability to identify genetic mutations linked to bladder cancer. NGS analysis of urine cytology specimens has shown reliable detection of genetic alterations correlating with clinical features and treatment responses. This advancement has improved the accuracy and reliability of genomic urine tests, benefiting both patients and healthcare providers.

The non-invasive nature of genomic urine testing offers a significant advantage over traditional diagnostic methods. Conventional procedures, such as cystoscopy, are invasive and often uncomfortable for patients. Genomic urine assays provide a more patient-friendly alternative, with studies indicating that these tests can reduce the need for cystoscopies by up to 53%. This approach enhances patient comfort while ensuring accurate detection of urothelial cancers, improving overall diagnostic efficiency.

Early detection capabilities further strengthen the value of genomic urine testing. A study conducted by the National Institutes of Health (NIH) highlighted that genomic urine assays can effectively detect urinary tract recurrences following bladder cancer treatment. This early detection capability allows for timely intervention, potentially reducing the frequency of invasive procedures and improving patient outcomes. Identifying cancer recurrence at an early stage significantly enhances treatment success rates.

The integration of biomarkers has also improved the sensitivity and specificity of genomic urine tests. For instance, the detection of fibroblast growth factor receptor 3 (FGFR3) mutations in urine samples has been associated with low-grade tumors, aiding in distinguishing between different tumor types. The inclusion of such biomarkers enhances diagnostic precision and supports more personalized treatment strategies.

Genomic urine testing holds particular relevance in the diagnosis of various cancers. According to data, bladder cancer accounts for approximately 4% of all new cancer cases in the United States, with 83,000 new cases reported annually. Globally, it is the tenth most common cancer, with around 500,000 new cases and 200,000 deaths each year. Meanwhile, prostate cancer remains the most commonly diagnosed cancer in men, with about 1.2 million cases reported annually in the United States, leading to 350,000 deaths. Testicular cancer, though less common, caused approximately 8,300 deaths globally in 2013, primarily affecting men aged 15 to 40 years.

Key Takeaways

- The global genomic urine testing market is projected to reach approximately USD 3006.5 million by 2033, rising from USD 892.5 million in 2023.

- The market is expected to expand at a compound annual growth rate (CAGR) of 13.15% from 2024 to 2033.

- In 2023, Next-Generation Sequencing (NGS) dominated the technology segment, accounting for over 40.3% of the total market share.

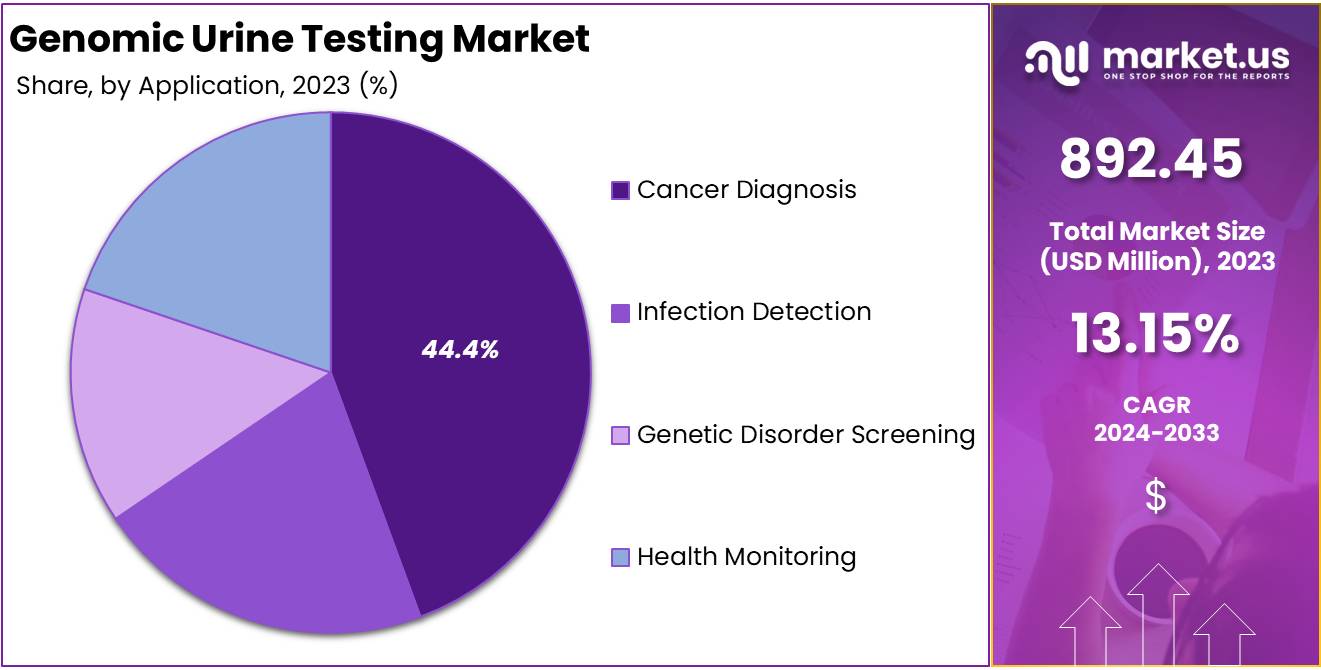

- Cancer diagnosis emerged as the leading application segment in 2023, securing more than 44.4% of the total market share.

- Hospitals and clinics held a dominant market position in 2023, representing over 51.4% of the genomic urine testing market.

- North America held a commanding market position in 2023, accounting for over 33.18% and reaching USD 296.11 million in value.

Technology Analysis

In 2023, Next-Generation Sequencing (NGS) held a dominant market position in the Technology Segment of Genomic Urine Testing, capturing more than a 40.3% share. NGS technology’s accuracy and ability to analyze multiple genetic markers have made it a preferred choice in diagnostic testing. This method is particularly effective in detecting genetic mutations linked to cancer and other diseases. Its growing use in precision medicine further strengthens its role in genomic urine testing.

Polymerase Chain Reaction (PCR) technology also secured a significant share of the genomic urine testing market. PCR is widely chosen for its affordability and fast results. Diagnostic laboratories often rely on PCR to identify infectious agents and detect genetic abnormalities. Its efficiency in delivering precise outcomes makes it a trusted option for routine genetic screening in urine samples. This technology remains essential in both clinical and research settings.

Other technologies, such as microarrays and hybridization techniques, accounted for the remaining market share. These methods are commonly applied in research and specialized diagnostic procedures. While less popular than NGS or PCR, they play a vital role in expanding genomic insights. The increasing demand for non-invasive diagnostic solutions continues to drive advancements across all genomic urine testing technologies.

Application Analysis

In 2023, Cancer Diagnosis held a dominant market position in the Application Segment of Genomic Urine Testing, capturing more than a 44.4% share. This strong presence was largely due to the increasing use of non-invasive methods for early cancer detection. Genomic urine testing has gained popularity as it effectively identifies cancer biomarkers through urine samples. The rising number of cancer cases worldwide and ongoing advancements in genetic testing technologies have further supported this segment’s growth.

Infection Detection ranked as the second-largest segment in the Genomic Urine Testing market. This growth was driven by the rising demand for fast and accurate diagnostic solutions. Genomic urine testing is increasingly being used to detect urinary tract infections (UTIs), sexually transmitted infections (STIs), and other bacterial or viral conditions. Its non-invasive nature and ability to deliver precise results have made it a preferred choice in clinical settings, improving patient outcomes.

Genetic Disorder Screening and Health Monitoring are also emerging as key growth segments. Genomic urine testing is gaining attention for identifying hereditary conditions and tracking overall health status. This method provides valuable insights into genetic risks, allowing individuals to adopt preventive healthcare measures. Growing awareness about personalized medicine and proactive health management is expected to boost demand in these segments over the coming years.

End-User Analysis

In 2023, Hospitals and Clinics held a dominant market position in the End-User Segment of Genomic Urine Testing, capturing more than a 51.4% share. This dominance can be attributed to the rising adoption of genomic urine testing for early disease diagnosis and routine health assessments. Hospitals and clinics have increasingly integrated these tests into their diagnostic protocols, improving patient outcomes through precise and timely detection.

Diagnostic Laboratories represented another key segment, contributing significantly to market growth. These facilities are essential for conducting complex genomic urine analyses, particularly in specialized testing scenarios. Their advanced equipment and expertise in genomic sequencing enable accurate results, driving their increasing role in the healthcare sector.

Research and Academic Institutions have also shown notable involvement in genomic urine testing. Their focus on developing innovative diagnostic tools and conducting clinical trials has supported advancements in this field. This segment’s growth is further fueled by collaborations with healthcare providers to improve genomic testing applications in personalized medicine.

Key Market Segments

Technology

- Next-Generation Sequencing (NGS)

- Polymerase Chain Reaction (PCR)

- Others

Application

- Cancer Diagnosis

- Infection Detection

- Genetic Disorder Screening

- Health Monitoring

End-User

- Hospitals and Clinics

- Diagnostic Laboratories

- Research and Academic Institutions

- Others

Drivers

Rising Prevalence of Urological Cancers Driving Genomic Urine Testing Market Growth

The increasing incidence of urological cancers, especially bladder and prostate cancers, is a key factor driving the genomic urine testing market. These cancers are becoming more common, leading to a higher demand for improved diagnostic solutions. Genomic urine testing offers a non-invasive method for detecting these conditions at an early stage. This advantage has encouraged healthcare providers to adopt such tests to enhance diagnostic accuracy. As a result, the market has witnessed significant growth, particularly in regions with rising cancer cases.

Early detection plays a vital role in improving cancer treatment outcomes. Genomic urine tests provide a quick and efficient way to identify genetic markers linked to urological cancers. This method minimizes the need for invasive procedures, improving patient comfort and compliance. Additionally, advancements in genomic technologies have enhanced test precision, further driving adoption. The combination of rising cancer cases and improved diagnostic solutions continues to fuel growth in the genomic urine testing market.

Recent studies have highlighted advancements in the diagnosis and treatment of urological cancers. For instance, a study published in the Journal of Clinical Oncology demonstrated that a half-hour MRI scan could expedite treatment for bladder cancer patients, reducing the time to treatment from 14 weeks to 7 weeks. Additionally, prostate cancer diagnoses have increased, with nearly 55,000 cases reported in the UK in 2023, partly due to a backlog from the COVID-19 pandemic.

Restraints

Cost Challenges and Limited Reimbursement Policies

High costs linked to genomic testing procedures act as a significant restraint in the market. Advanced technologies used in genomic urine testing require substantial investment, making the tests expensive for healthcare providers and patients. The high costs are particularly challenging for individuals without comprehensive health insurance. As a result, patients in developing regions or areas with limited healthcare infrastructure may face barriers in accessing these services, ultimately hindering market growth.

Limited reimbursement policies further restrict the adoption of genomic urine testing. In several regions, insurance providers may not fully cover the costs of advanced genomic procedures. This lack of financial support places a burden on healthcare facilities and patients, reducing overall testing rates. Consequently, these reimbursement challenges limit the broader implementation of genomic urine testing, slowing market expansion despite its clinical benefits. Addressing these issues is crucial for enhancing accessibility and promoting wider market growth.

Opportunities

Enhanced Accuracy in Genomic Urine Testing with NGS Technology

Advancements in next-generation sequencing (NGS) technology present a notable opportunity in genomic urine testing. Enhanced sequencing techniques have significantly improved the accuracy and efficiency of detecting genetic mutations. This advancement is crucial for identifying biomarkers linked to various cancers. By improving precision, NGS allows for the early detection of cancer-related mutations, aiding healthcare providers in initiating timely treatment strategies. As a result, the integration of NGS technology enhances diagnostic capabilities, offering better outcomes for patients undergoing genomic urine tests.

Furthermore, NGS technology streamlines the testing process by enabling comprehensive genetic analysis using minimal urine samples. This advancement reduces the need for invasive procedures, improving patient comfort and compliance. The improved accuracy of NGS also minimizes the risk of false positives or negatives, ensuring more reliable test results. With these benefits, NGS technology is positioned to play a pivotal role in advancing genomic urine testing, supporting early cancer detection and improving overall diagnostic precision.

Trends

AI Integration Enhances Precision in Genomic Urine Testing

The integration of artificial intelligence (AI) in genomic urine testing is gaining significant attention. AI-driven algorithms are enhancing the accuracy and speed of data interpretation. This advancement is improving the detection of urological conditions, such as bladder and kidney cancers. By analyzing complex genomic data, AI enables healthcare professionals to identify genetic markers linked to these conditions. As a result, faster diagnosis and targeted treatment plans are becoming more achievable, improving patient outcomes and reducing diagnostic errors.

Moreover, AI integration in genomic urine testing is streamlining laboratory workflows. Automated data processing reduces manual intervention, minimizing the risk of human error. AI systems can quickly analyze large datasets, providing clinicians with actionable insights in less time. This efficiency is especially beneficial for high-volume testing centers. As the demand for precision diagnostics grows, the adoption of AI technologies in genomic urine testing is expected to expand, driving innovation in urological disease management.

Regional Analysis

In 2023, North America held a dominant market position, capturing more than a 33.18% share and holds US$ 296.11 million market value for the year. This growth can be linked to the region’s strong healthcare infrastructure and the widespread adoption of genomic technologies. The presence of well-established diagnostic laboratories has further supported this market expansion. These factors have contributed significantly to North America’s leadership in the genomic urine testing sector.

The rising occurrence of chronic diseases, including cancer and kidney disorders, has increased demand for genomic urine testing across North America. Healthcare providers are increasingly adopting genomic testing for early disease detection and personalized treatment planning. The United States, in particular, has shown considerable growth in this sector due to rising investments in precision medicine initiatives. This investment trend continues to enhance testing adoption rates.

Regulatory support has played a vital role in strengthening the genomic urine testing market in North America. Government agencies such as the National Institutes of Health (NIH) have actively funded genomic research projects. These initiatives have promoted innovation in diagnostic tools and improved access to advanced genomic testing solutions. As a result, healthcare facilities across the region have integrated these technologies into routine diagnostic practices.

North America’s strong network of healthcare providers and diagnostic centers has further bolstered market growth. Leading institutions have prioritized genomic testing to improve patient outcomes and enhance early diagnosis strategies. This focus on innovation, combined with increasing awareness about genomic testing, is expected to sustain North America’s dominant position in the global genomic urine testing market.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The Genomic Urine Testing market features several prominent players driving innovation and growth. Illumina, Inc. plays a significant role by offering advanced sequencing platforms that enhance testing accuracy. Its expertise in next-generation sequencing (NGS) improves data interpretation, supporting precise diagnostic results. Similarly, Foundation Medicine, Inc. leverages comprehensive genomic profiling technologies, particularly in cancer diagnostics. This approach strengthens early detection capabilities, improving patient outcomes. These companies actively invest in research and development to expand their genomic urine testing solutions.

Hologic, Inc. is recognized for its molecular diagnostic innovations. The company offers specialized solutions that detect genetic markers in urine samples. These advancements support disease diagnosis and personalized treatment strategies. Guardant Health, Inc. is another key player known for its liquid biopsy expertise. Guardant Health’s genomic testing solutions are widely used for non-invasive cancer screening, enhancing early detection in oncology. Both companies focus on technological improvements to strengthen their presence in the genomic urine testing sector.

Quest Diagnostics Incorporated plays a crucial role with its extensive diagnostic testing network. The company offers comprehensive genomic urine testing solutions that aid clinical decision-making. In addition to major players, several other industry participants focus on cost-effective solutions and improved testing accuracy. These companies also expand genomic urine testing applications in diverse healthcare settings. Collectively, these efforts support market growth by improving diagnostic reliability and expanding access to non-invasive genomic testing.

Market Key Players

- Illumina

- Foundation Medicine

- Hologic

- Guardant Health

- Quest Diagnostics

- Roche

- BioRad Laboratories

- Labcorp

- Genomic Health

- Cancer Genetics

- Mayo Clinic Laboratories

- Exact Sciences

- ArcherDX

- Thermo Fisher Scientific

Recent Developments

- January 2025: Hologic finalized a $350 million acquisition of a company specializing in novel ultrasound imaging devices, aiming to enhance its breast imaging portfolio.

- In October 2024: Illumina introduced the MiSeq i100 series, a line of compact and cost-effective gene sequencers designed to enhance accessibility for smaller research and testing laboratories. The MiSeq i100 is priced at $49,000, while the higher-capacity i100 Plus is available for $109,000. These benchtop devices deliver results in approximately four hours, significantly faster than previous models, and support various applications, including panels for detecting respiratory and urinary pathogens.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 892.5 Million |

| Forecast Revenue (2033) | US$ 3006.5 Million |

| CAGR (2024-2033) | 13.15% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology (Next-Generation Sequencing (NGS), Polymerase Chain Reaction (PCR), Others), By Application (Cancer Diagnosis, Infection Detection, Genetic Disorder Screening, Health Monitoring), By End-User (Hospitals and Clinics, Diagnostic Laboratories, Research and Academic Institutions, Others) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Illumina, Foundation Medicine, Hologic, Guardant Health, Quest Diagnostics, Roche, BioRad Laboratories, Labcorp, Genomic Health, Cancer Genetics, Mayo Clinic Laboratories, Exact Sciences, ArcherDX, Thermo Fisher Scientific, and Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |