Quick Navigation

- Market Overview

- Key Takeaways

- Product Type Analysis

- Material Type Analysis

- Application Analysis

- End User Analysis

- Fabrication Method Analysis

- Distribution Channel Analysis

- Key Market Segments

- Driving Factors

- Challenges

- Restraining Factors

- Opportunity

- Regional Analysis

- Key Player Analysis

- Recent Developments

- Report Scope

Market Overview

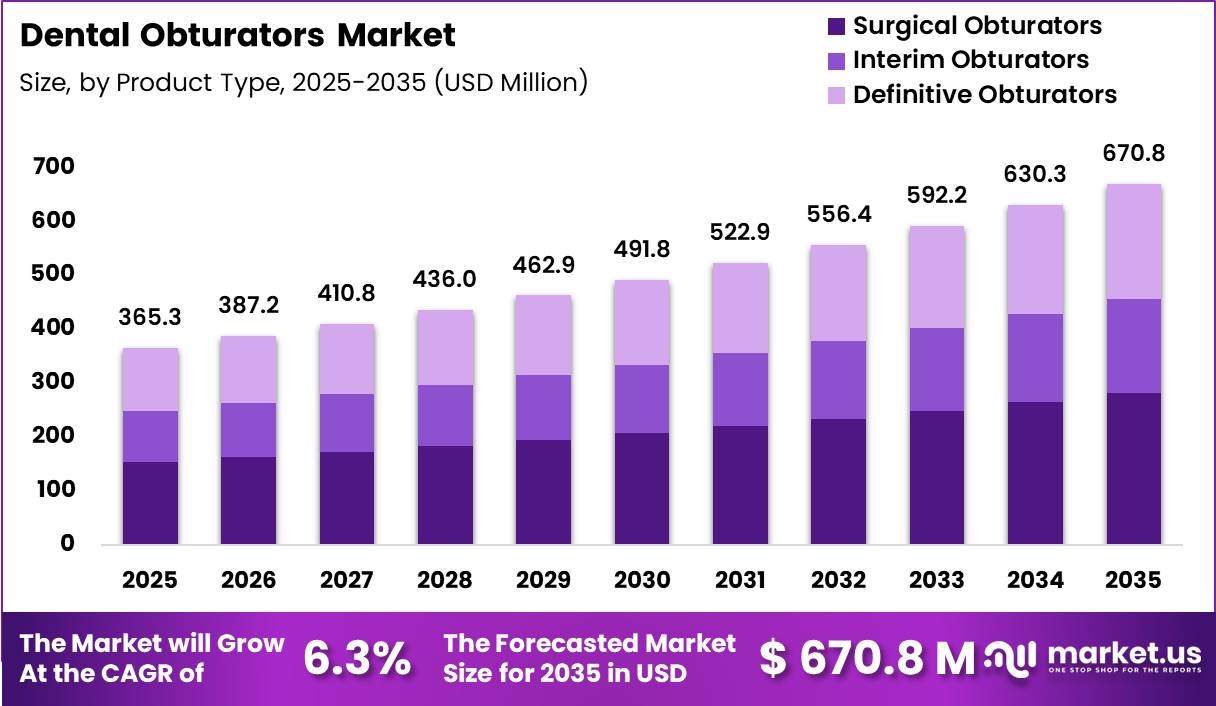

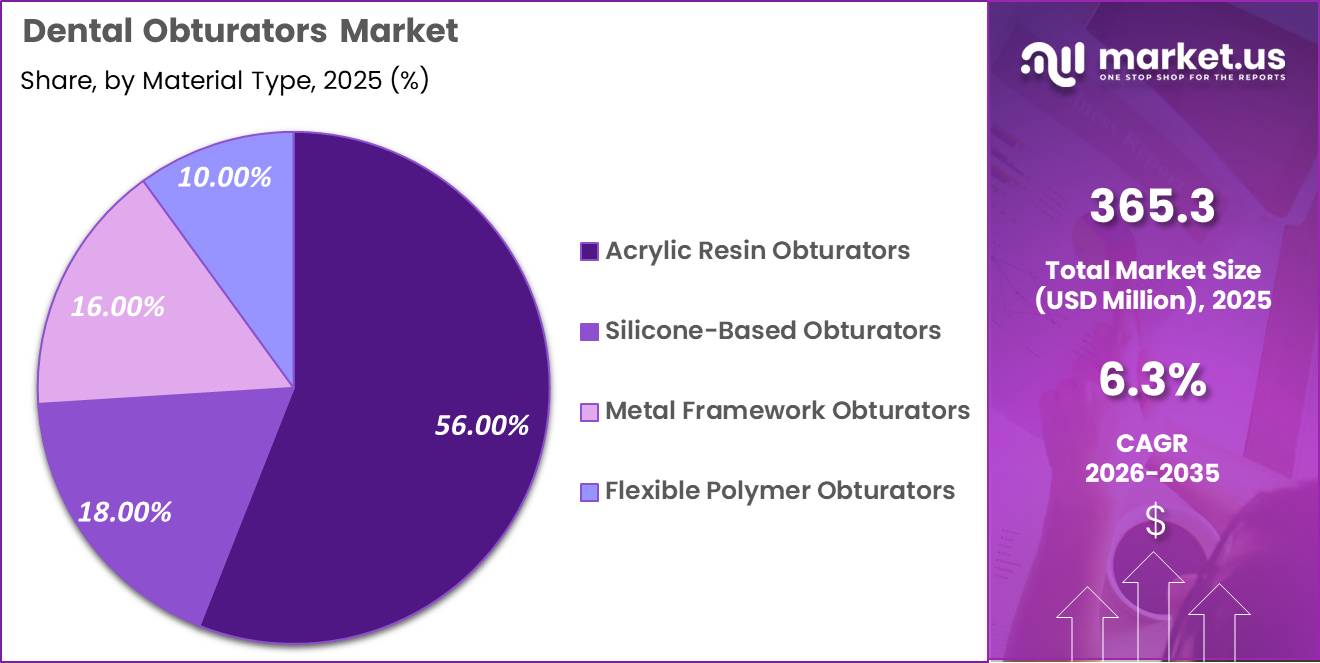

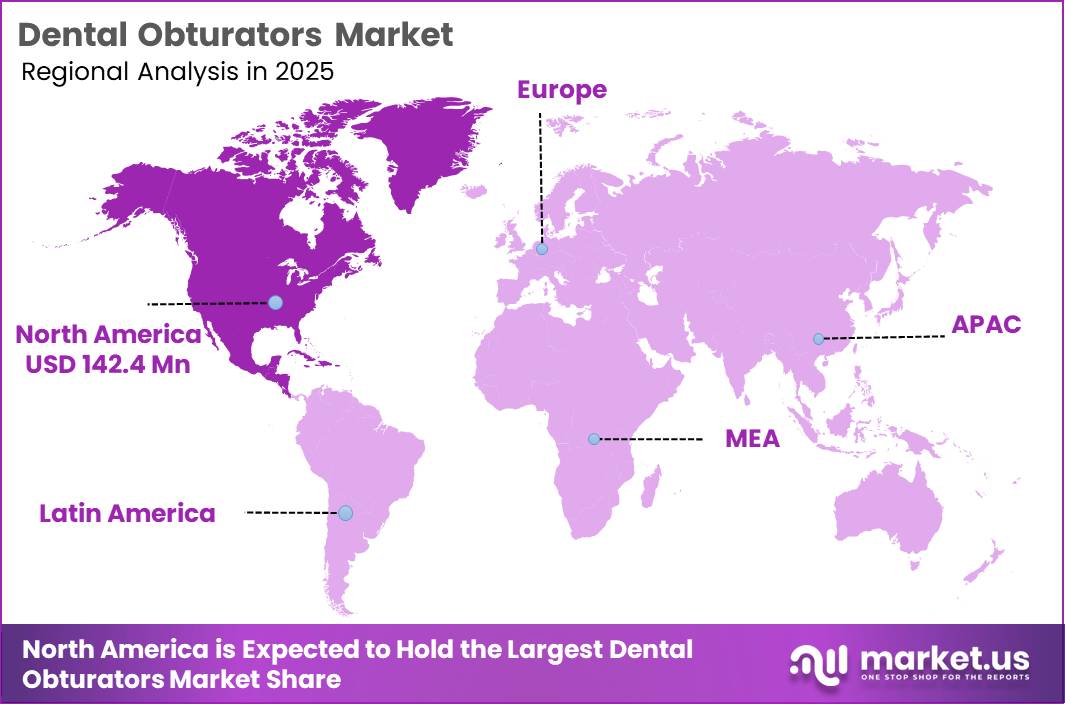

Global Dental Obturators Market size is expected to be worth around US$ 670.8 Million by 2035 from US$ 365.3 Million in 2025, growing at a CAGR of 6.3% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 39.00% share with a revenue of US$ 142.47 Million.

The Global Dental Obturators Market supports essential oral rehabilitation procedures, helping restore oral function, speech, and mastication for patients with defects arising from congenital conditions, trauma, or surgical resections. Dental obturators are specialised maxillofacial prostheses designed to close palatal or orofacial openings, enabling improved quality of life for affected individuals.

Oral diseases represent a significant global health challenge. According to the World Health Organisation Global Oral Health Status Report 2022, oral conditions affect an estimated 3.5 billion people and are among the most common noncommunicable diseases worldwide. Oral health disorders include dental caries, periodontal disease, tooth loss, and structural defects requiring prosthetic intervention like obturators to restore function and structure in affected patients.

The need for dental obturators correlates with the prevalence of oral disease and the number of surgical procedures that result in maxillary or palatal defects. Intraoral prostheses such as interim and definitive obturators are recognised in clinical coverage guidelines for functional rehabilitation following oral cancer resection or congenital defects.

Recent industry analyses estimate the global dental obturators market at approximately USD 388 million in 2023, with projections to grow over the coming decade, reflecting continued demand driven by the prevalence of oral disease and advances in prosthetic fabrication.

Key Takeaways

- Market Size: The Global Dental Obturators Market size was US$ 365.3 Million in 2025. The market is estimated to grow to US$ 670.8 million by 2035.

- Market Share: The Compound Annual Growth Rate (CAGR) of the market from 2026 to 2035 will be 6.3%.

- Product Type: Surgical Obturators has the largest market share, accounting for 42% of total sales.

- Material Type: Acrylic Resin Obturators dominate the segment, accounting for 56% of total revenue.

- Application: Maxillectomy Rehabilitation leads the segment, accounting for 48% of total revenue.

- End User: Hospitals lead the segment, accounting for 45% of total revenue.

- Fabrication Method: Conventional Fabrication dominates the segment, accounting for 68% of total revenue.

- Distribution Channel: Direct Hospital Procurement dominates the segment, accounting for 52% of total revenue.

- Regional: North America is the dominant regional market, accounting for 39% of global sales.

Product Type Analysis

The dental obturators market is segmented by product type into surgical obturators, interim obturators, and definitive obturators, each serving a distinct phase of oral rehabilitation. In 2025, surgical obturators dominated with a 42.00% market share, reflecting their critical role immediately following maxillofacial surgeries, particularly maxillectomy procedures.

These devices are essential for separating the oral and nasal cavities post-surgery, enabling early speech, swallowing, and wound protection. Rising incidences of oral cancers and tumour resections have significantly increased demand for surgical obturators in hospital settings.

Interim obturators accounted for 26.00% of the market, acting as transitional solutions during the healing phase. Their adaptability to changing oral anatomy makes them valuable in short-term rehabilitation, especially in oncology recovery pathways. Definitive obturators held a substantial 32.00% share, driven by their long-term functional and aesthetic benefits.

Custom-designed prostheses support permanent restoration of speech and mastication, particularly for patients with stable post-surgical anatomy. Collectively, product type segmentation highlights the importance of a phased treatment approach, with each obturator type addressing evolving clinical needs throughout the patient rehabilitation journey.

Material Type Analysis

Material selection plays a pivotal role in the performance, comfort, and durability of dental obturators. In 2025, acrylic resin obturators led the market with a dominant 56.00% share, owing to their affordability, ease of fabrication, and widespread acceptance in conventional prosthodontics. Acrylic resins provide sufficient rigidity, customisation flexibility, and repairability, making them the preferred choice for both interim and definitive obturators in many clinical settings.

Silicone-based obturators captured 18.00% of the market, supported by their superior softness, flexibility, and patient comfort. These materials are particularly beneficial for patients with sensitive tissues or irregular defect margins, although higher costs and durability concerns limit broader adoption. Metal framework obturators accounted for 16.00%, driven by demand for enhanced structural strength and longevity in complex or extensive defects. They are commonly used in definitive prostheses requiring long-term stability.

Finally, flexible polymer obturators represented 10.00% of the market, reflecting growing interest in lightweight, aesthetic, and patient-friendly alternatives. Overall, material segmentation demonstrates a balance between cost-effectiveness, comfort, and mechanical performance.

Application Analysis

By application, the dental obturators market is primarily driven by maxillofacial rehabilitation needs. In 2025, maxillectomy rehabilitation dominated with a 48.00% market share, underscoring the critical role of obturators in managing defects resulting from oral cancer surgeries. These devices restore essential oral functions such as speech, swallowing, and mastication, significantly improving post-surgical quality of life. The rising global burden of head and neck cancers continues to fuel demand in this segment.

Rehabilitation of congenital defects, including cleft palate conditions, represents a key secondary segment. These cases require early and often long-term prosthetic intervention, supporting consistent demand across pediatric and adult populations. Traumatic oral defects, resulting from accidents or injuries, also contribute meaningfully to market growth, particularly in regions with high trauma incidence.

Additionally, other oral and maxillofacial defects, such as infections or osteonecrosis-related resections, form a smaller yet clinically important segment. Overall, application-based segmentation highlights the market’s strong dependence on complex surgical and reconstructive dentistry, with obturators serving as indispensable rehabilitative tools.

End User Analysis

End-user segmentation reveals where dental obturators are most frequently prescribed, fabricated, and fitted. In 2025, hospitals dominated the market with a 45.00% share, reflecting their central role in managing maxillofacial surgeries, oncology treatments, and complex reconstructive procedures. Hospitals benefit from integrated surgical and prosthodontic teams, enabling immediate obturator placement following tumour resections or trauma surgeries.

Dental clinics represent a significant secondary segment, driven by increasing referrals for follow-up care, adjustments, and long-term prosthetic management. As awareness of oral rehabilitation improves, clinics are increasingly involved in providing definitive obturators and post-surgical monitoring.

Prosthodontic speciality centres account for a growing share due to their advanced expertise in complex oral prostheses. These centres often handle challenging anatomical cases and offer customised solutions using advanced materials and digital workflows. Their role is particularly important for definitive obturator fabrication requiring precision and aesthetic optimisation.

Overall, end-user segmentation underscores the collaborative nature of obturator care, with hospitals leading initial intervention and specialised dental providers supporting long-term rehabilitation outcomes.

Fabrication Method Analysis

Fabrication method segmentation reflects technological adoption patterns in the dental obturators market. In 2025, conventional fabrication dominated with a 68.00% market share, highlighting the continued reliance on traditional impression-based techniques. Conventional methods remain widely used due to lower costs, established clinical familiarity, and accessibility in developing and mid-income regions. Acrylic processing and manual customisation continue to meet the needs of a large patient base.

However, CAD/CAM digital fabrication is gaining momentum, supported by advances in intraoral scanning, 3D modelling, and milling technologies. Although representing a smaller share, digital fabrication offers superior precision, reproducibility, and reduced turnaround times. These advantages are particularly valuable for complex maxillofacial defects where accuracy is critical.

Adoption of digital methods is accelerating in speciality centres and advanced hospitals, driven by investments in digital dentistry infrastructure. As costs decline and training expands, CAD/CAM-based obturator fabrication is expected to grow steadily. Overall, fabrication segmentation illustrates a transitional market, where conventional methods dominate volume, while digital technologies shape future innovation and efficiency.

Distribution Channel Analysis

Distribution channels play a crucial role in determining accessibility and procurement efficiency for dental obturators. In 2025, direct hospital procurement led the market with a 52.00% share, reflecting the high volume of obturators required in surgical and oncology departments. Hospitals often source obturators directly to ensure timely availability for post-operative care and better coordination with surgical teams.

Dental laboratories form a key secondary distribution channel, supplying custom-fabricated obturators to hospitals, dental clinics, and speciality centres. Their expertise in prosthetic design and material processing supports both interim and definitive obturator demand. The growing trend toward outsourced fabrication strengthens the role of laboratories in the supply chain.

Speciality dental distributors account for a smaller yet important segment, particularly in regions with fragmented healthcare infrastructure. These distributors facilitate access to materials, prefabricated components, and specialised obturator systems for clinics and prosthodontic practices.

Overall, distribution channel segmentation highlights the dominance of institutional procurement while emphasising the supportive role of laboratories and distributors in expanding market reach and ensuring continuity of care.

Key Market Segments

By Product Type

- Surgical Obturators

- Interim Obturators

- Definitive Obturators

By Material Type

- Acrylic Resin Obturators

- Silicone-Based Obturators

- Metal Framework Obturators

- Flexible Polymer Obturators

By Application

- Maxillectomy Rehabilitation

- Congenital Defects (Cleft Palate)

- Traumatic Oral Defects

- Other Oral & Maxillofacial Defects

By End User

- Hospitals

- Dental Clinics

- Prosthodontic Specialty Centers

By Fabrication Method

- Conventional Fabrication

- CAD/CAM Digital Fabrication

By Distribution Channel

- Direct Hospital Procurement

- Dental Laboratories

- Speciality Dental Distributors

Driving Factors

Rising endodontic case pool from untreated caries burden

WHO reported in 2025 that oral diseases affect nearly 3.7 billion people globally and that untreated dental caries in permanent teeth remain the most common health condition worldwide, creating a structurally large funnel for restorative and endodontic intervention rather than a temporary demand spike.

A 2025 global burden analysis estimated about 2.24 billion cases of caries in permanent teeth in 2021 and projected the count to edge up to 2.26 billion by 2050, showing that the addressable pool for root canal-related procedures remains persistent even if treatment penetration improves only gradually.

In the U.S., Centers for Disease Control and Prevention linked 2024 surveillance commentary noted untreated decay in permanent teeth at about 22% among adults aged 20 to 34, while CDC referenced summaries still indicate that over 90% of adults aged 20 to 64 have experienced at least one cavity, which supports continued downstream need for canal obturation materials, delivery systems, and retreatment instruments rather than a one off consumables cycle.

For manufacturers, this driver improves baseline volume predictability as caries moves from preventive failure to pulpal involvement; the business mix shifts toward recurring sealer, cone, and obturator sales with higher frequency than capital equipment, particularly in high-density urban care systems across APAC and Latin America, where untreated disease incidence and delayed presentation remain more common, as reported by the World Health Organisation.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising endodontic case pool from untreated caries burden | +1.9% | Global, with APAC, Latin America, Middle East & Africa volume upside; North America and EU replacement demand | Medium term (2-4 years) |

| Bioceramic sealer adoption lifting obturation value per procedure | +1.6% | North America core, EU, Japan, South Korea, urban China, Gulf clinics | Short term (≤ 2 years) |

| Workflow digitisation and motor-integrated obturation ecosystems | +1.3% | North America core, Western Europe, Australia, Japan, premium private clinics in APAC | Short term (≤ 2 years) |

| Regulatory standard upgrades are accelerating product refresh and compliance-led switching | +0.9% | U.S., EU, UK-aligned import markets, advanced APAC | Medium term (2-4 years) |

| Retreatment intensity and complexity management in bioceramic-filled canals | +0.8% | North America, EU, Brazil, India, and referral endodontic centres globally | Medium term (2-4 years) |

| Expanding oral-health access and chairside efficiency economics | +1.1% | India, Southeast Asia, Latin America, Middle East, public-private care corridors | Long term (≥ 4 years) |

Challenges

Persistent oral workforce gaps

Chronic shortages and maldistribution of oral health professionals slow the addressable patient flow for obturator procedures by constraining chair capacity, extending wait times, and delaying complex maxillofacial rehabilitation even when prosthetic products are available, creating an estimated drag of 1.2% points on potential market CAGR in 2026.

WHO estimates indicate that Africa had about 57,000 oral health professionals in 2022, or roughly 0.37 per 10,000 people versus a needs benchmark of 1.33, implying a shortfall exceeding 100,000 practitioners and demand for nearly 199,000 workers by 2030, including over 100,000 dentists.

In the United States, around 202,000 active dentists in 2024 equate to 59.5 per 100,000 people, yet 63.7 million residents still live in dental Health Professional Shortage Areas, with an estimated need for 10,700 additional dentists.

For obturator indications requiring long chair time and multidisciplinary coordination, workforce gaps create months-long backlogs, reduce clinic throughput by 10–20 %, and limit penetration of complex rehabilitation, particularly in public systems. Strategic responses include task-sharing, teleconsultation and AI-assisted planning to reduce chair time, expanded specialist training, and integration of obturator pathways into national cancer and craniofacial programs.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Persistent oral workforce gaps | -1.2% | Africa, Latin America, rural Asia, underserved US | Long term (≥ 4 years) |

| Fragmented prosthetic workflows | -0.9% | North America, Western Europe, Japan, GCC | Medium term (2-4 years) |

| Material supply volatility | -0.7% | APAC logistics corridors, EU import hubs, global OEMs | Medium term (2-4 years) |

| Reimbursement and affordability strain | -1.0% | Emerging Asia, Africa, Latin America, low-income OECD | Long-term (≥ 4 years) |

| Digital–analogue integration lag | -0.8% | Global tier-2 clinics, public hospitals, Eastern Europe | Medium term (2-4 years) |

| Regulatory and QA compliance load | -0.6% | EU regulatory hubs, North America core, Japan | Short term (≤ 2 years) |

Restraining Factors

EU MDR compliance burden

A second restraint is the elevated compliance burden under the EU Medical Device Regulation, which has increased documentary, clinical, post-market surveillance, and traceability requirements for dental device manufacturers, including stronger biocompatibility justification, technical documentation, and ongoing surveillance obligations, while EUDAMED-related transparency and registration requirements expanded further from May 28, 2026, for manufacturers, importers, and notified bodies.

Even where obturation devices are not frontier technologies, smaller manufacturers face materially higher regulatory overhead from clinical evaluation report updates, post-market surveillance and post-market clinical follow-up workflows, unique device identification administration, and certificate maintenance.

Notified body processes also remain capacity constrained and procedurally cautious, with a 2025 survey showing only 13 notified bodies responding and limited practical use of conditional certification tools, reinforcing the market’s low tolerance for incomplete evidence packages.

The business impact includes delayed CE pipeline conversion, higher compliance operating expenses, slower line extensions, and selective withdrawal of low-volume SKUs from Europe, which in turn can reduce regional launch velocity and trim roughly 0.9% points from medium-term CAGR for EU-facing obturation portfolios.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tariff-led input inflation | -1.1% | North America core, China-linked supply routes | Short term (≤ 2 years) |

| EU MDR compliance burden | -0.9% | EU, UK-linked distributors, CE-export hubs | Medium term (2-4 years) |

| Clinic cost squeeze | -0.8% | U.S., Canada, Western Europe, urban APAC | Short term (≤ 2 years) |

| Reimbursement-price mismatch | -0.7% | North America core, insured urban markets | Medium term (2-4 years) |

| Workforce bottlenecks | -0.6% | U.S., EU, Australia, Gulf urban centres | Short term (≤ 2 years) |

| Oral-care affordability gap | -1.0% | LATAM, MEA, South Asia, lower-tier APAC | Long term (≥ 4 years) |

Opportunity

DSO-led premium system conversion

A major white space is not the existence of root-canal demand itself, but the under-monetised conversion of fragmented obturation purchasing into enterprise-level, protocolized procurement within dental service organisations and multi-site speciality groups, where vendors can shift from low-value consumable selling to higher-ARPU system selling through bundled obturators, matched tips, sealers, training, and digital workflow support.

This is an opportunity rather than a current driver because the baseline market already reflects routine endodontic treatment volumes. At the same time, the upside comes from raising wallet share per procedure and reducing clinical variability across chains that control hundreds of chairs and can standardise formulary decisions in a single contract cycle.

The commercial logic is strengthened by the scale of the dental economy, with U.S. dental expenditures reaching $ 189 billion in 2024 as tracked by the American Dental Association, while reimbursement pressure is pushing practices to scrutinize write-offs and procedure economics more tightly.

Making vendors that can show 3–5 minutes lower chair time, 100–250 basis points higher assistant utilization, and 4–7% lower rework or retreatment-related consumable waste more likely to win enterprise conversion even a 10–15% penetration gain in organized group dentistry could expand vendor revenue per contracted site by roughly 20–35% versus standalone obturator-only sales, supporting an incremental market CAGR uplift of about 1.6 % points above baseline.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| DSO-led premium system conversion | +1.6% | North America core, EU, ANZ | Short term |

| Bioceramic single-cone kits for GP dentistry | +2.1% | APAC, LATAM, CEE, Middle East | Short term |

| Medical-dental integration referral capture | +1.4% | U.S., EU5, Japan | Medium term |

| Geriatric mobile endodontic pathways | +1.2% | Japan, Western Europe, South Korea, urban China | Medium term |

| Adjacent canal-disinfection platform bundling | +2.4% | North America, EU, premium APAC | Medium term |

| Value-tier localization and roll-up M&A | +1.9% | India, Southeast Asia, Africa, LATAM | Long term |

Regional Analysis

In 2025, North America led the market, achieving over 39.00% share with a revenue of US$ 142.47 Million. Reflecting the region’s strong clinical infrastructure and high adoption of advanced maxillofacial prosthetic solutions. The United States remains the dominant contributor, supported by a high prevalence of oral cancers, traumatic facial injuries, and congenital craniofacial defects, all of which drive demand for surgical and definitive dental obturators.

Widespread access to prosthodontists, favourable reimbursement for medically necessary oral prostheses, and the early adoption of digital impression and CAD/CAM technologies further reinforce regional leadership.

Europe represents the second-largest market, driven by increasing awareness of post-oncologic oral rehabilitation and strong public healthcare coverage in countries such as Germany, France, and the United Kingdom. The presence of specialised maxillofacial centres and growing emphasis on quality-of-life restoration after head and neck cancer surgeries support steady demand, despite regulatory compliance costs under the Medical Device Regulation.

The Asia-Pacific region is projected to register the fastest growth rate through the forecast period. Rising oral cancer incidence, expanding dental care access, and increasing investments in hospital infrastructure in countries like China, India, and Japan are key growth drivers.

Meanwhile, Latin America and the Middle East & Africa show moderate but improving adoption, supported by gradual improvements in surgical capacity, dental education, and awareness of prosthetic rehabilitation options.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Player Analysis

Competitive advantage in the global dental obturators market is achieved through specialised prosthodontic manufacturing expertise spanning surgical, interim, and definitive obturator product categories, established relationships with hospital maxillofacial surgery departments and prosthodontic speciality centres, and continued investment in CAD/CAM digital fabrication technology that improves obturator fit precision and reduces production turnaround times.

Major strategic priorities for leading manufacturers include expansion of flexible polymer and silicone-based material formulations that enhance patient comfort for long-term obturator wear, development of digital workflow integration supporting faster definitive obturator fabrication following maxillectomy procedures, and sustained investment in hospital procurement relationships reflecting the predominantly institutional nature of obturator demand.

Strong direct hospital procurement relationships, combined with growing partnerships with speciality dental distributors across Asia Pacific markets, represent a critical competitive differentiator for manufacturers serving both oncology-related maxillectomy rehabilitation and congenital defect treatment pathways.

Top Key Players

- Dentsply Sirona

- Straumann Group

- Zimmer Biomet Dental

- Envista Holdings

- Ivoclar Vivadent

- GC Corporation

- 3M Oral Care

- Keystone Dental

- Kulzer GmbH

- VITA Zahnfabrik

- Shofu Inc.

- Bego GmbH

- Nobel Biocare

- Osstem Implant

- Glidewell Laboratories

- Other Key Player

Recent Developments

- In January 2026, Dentsply Sirona launched an expanded definitive obturator material line featuring enhanced silicone-based formulations, targeting prosthodontic speciality centres seeking improved patient comfort for long-term maxillectomy rehabilitation cases.

- In February 2026, Straumann Group introduced a new CAD/CAM digital fabrication workflow for surgical and interim obturators, targeting hospital maxillofacial surgery departments seeking faster turnaround between resection surgery and prosthetic placement.

- In March 2026, Glidewell Laboratories expanded its definitive obturator fabrication capacity using digital scanning and 3D printing technology, targeting prosthodontic speciality centres across North American hospital networks requiring rapid custom obturator production.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 365.3 Million |

| Forecast Revenue (2035) | US$ 670.8 Million |

| CAGR (2026-2035) | 6.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Surgical Obturators, Interim Obturators, Definitive Obturators), By Material Type (Acrylic Resin Obturators, Silicone-Based Obturators, Metal Framework Obturators, Flexible Polymer Obturators), By Application (Maxillectomy Rehabilitation, Congenital Defects (Cleft Palate), Traumatic Oral Defects, Other Oral & Maxillofacial Defects), By End User (Hospitals, Dental Clinics, Prosthodontic Specialty Centers), By Fabrication Method (Conventional Fabrication, CAD/CAM Digital Fabrication), By Distribution Channel (Direct Hospital Procurement, Dental Laboratories, Specialty Dental Distributors) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Dentsply Sirona, Straumann Group, Zimmer Biomet Dental, Envista Holdings, Ivoclar Vivadent, GC Corporation, 3M Oral Care, Keystone Dental, Kulzer GmbH, VITA Zahnfabrik, Shofu Inc., Bego GmbH, Nobel Biocare, Osstem Implant, Glidewell Laboratories, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |