Quick Navigation

Market Overview

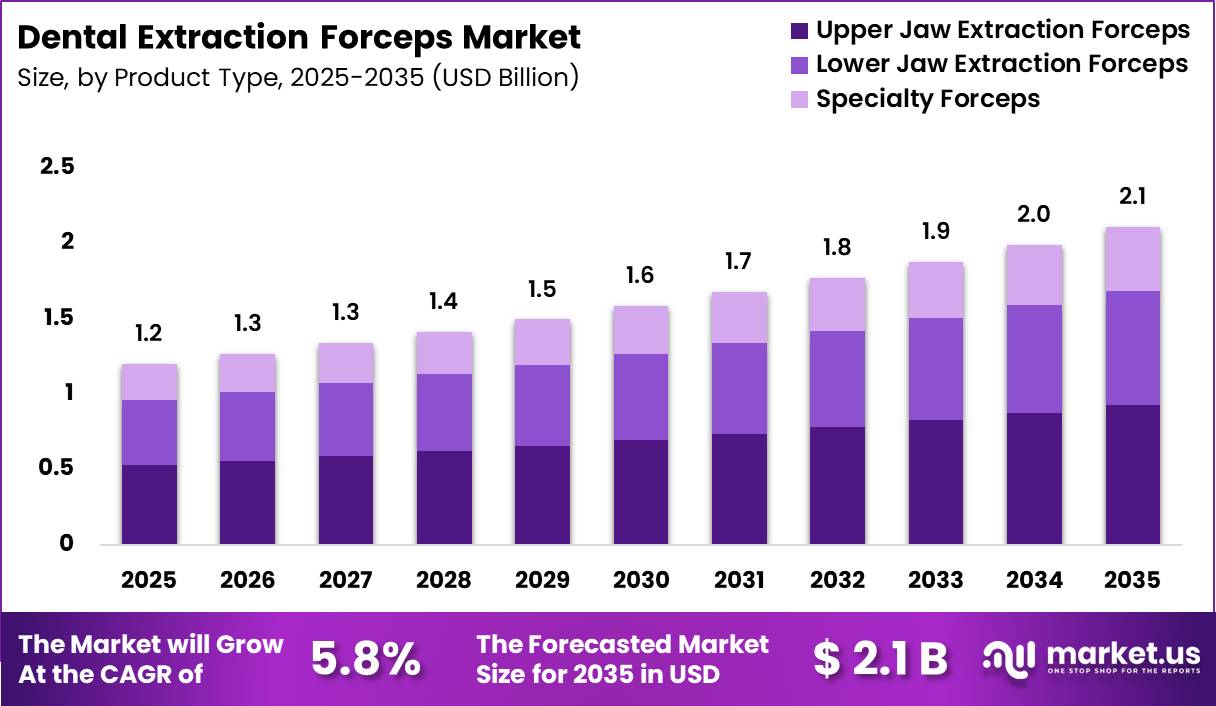

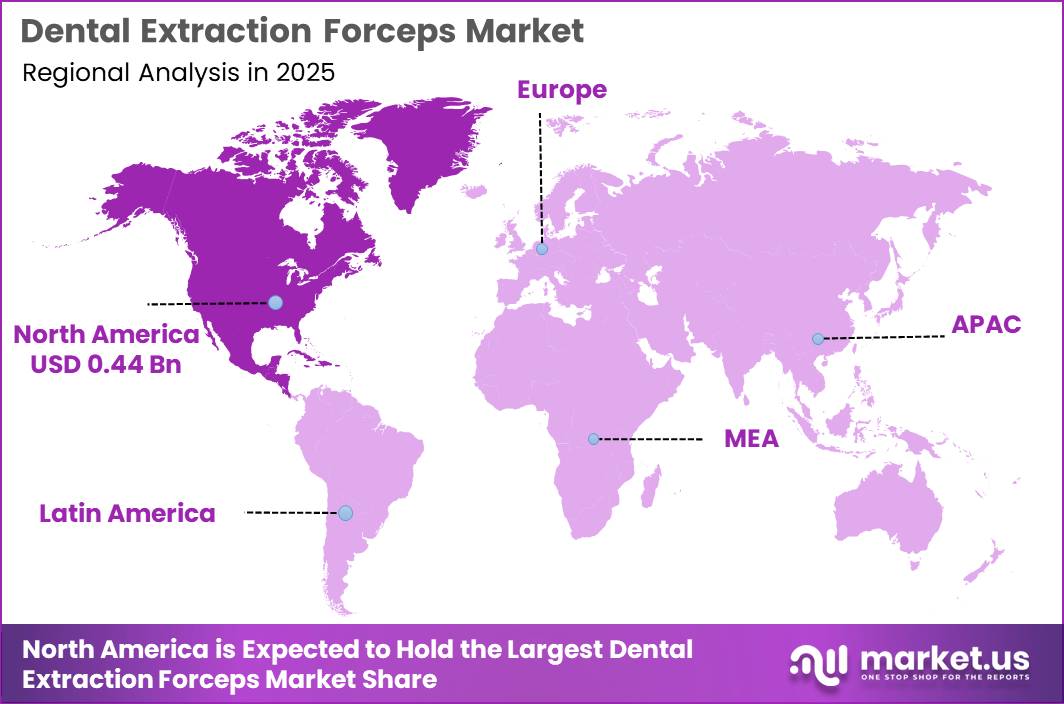

Global Dental Extraction Forceps Market size is expected to be worth around US$ 2.1 Billion by 2035 from US$ 1.2 Billion in 2025, growing at a CAGR of 5.8% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 37.00% share with a revenue of US$ 0.44 Billion.

Dental extraction forceps are specialised surgical instruments used by dentists and oral surgeons to remove teeth during simple and surgical extractions. They consist of a handle, hinge, and beaks designed to grip tooth surfaces, with different shapes for maxillary and mandibular applications to optimise force and safety in clinical practice.

According to the World Health Organisation (WHO), oral diseases affect nearly 3.7 billion people globally, with untreated dental caries being the most common condition worldwide and often necessitating dental extraction procedures when restorative treatment is no longer viable. Government data from England’s National Health Service show that in the financial year ending 2024, there were 49,112 tooth extraction episodes recorded in hospitals for children and young people aged 0 to 19 years, with 62 % linked to decay.

Dental extraction forceps are recognised on key medical device standards lists, such as the U.S. Food and Drug Administration-recognised consensus standards (ISO 9173 2 and ISO 9173 3), which classify these as Class I dental instruments used in routine clinical care. Their use remains central in standard dental practice.

Simple forceps-based extractions account for over half of routine extraction procedures in primary care settings. As global oral disease prevalence continues to rise, demand for reliable, ergonomically designed extraction forceps in clinics and hospitals is expected to remain steady.

Key Takeaways

- Market Size: The Global Dental Extraction Forceps Market size was US$ 1.2 billion in 2025. The market is estimated to grow to US$ 2.1 billion by 2035

- Market Share: The Compound Annual Growth Rate (CAGR) of the market from 2026 to 2035 will be 5.8%.

- Product Type: Upper Jaw Extraction Forceps has the largest market share, accounting for 44% of total sales.

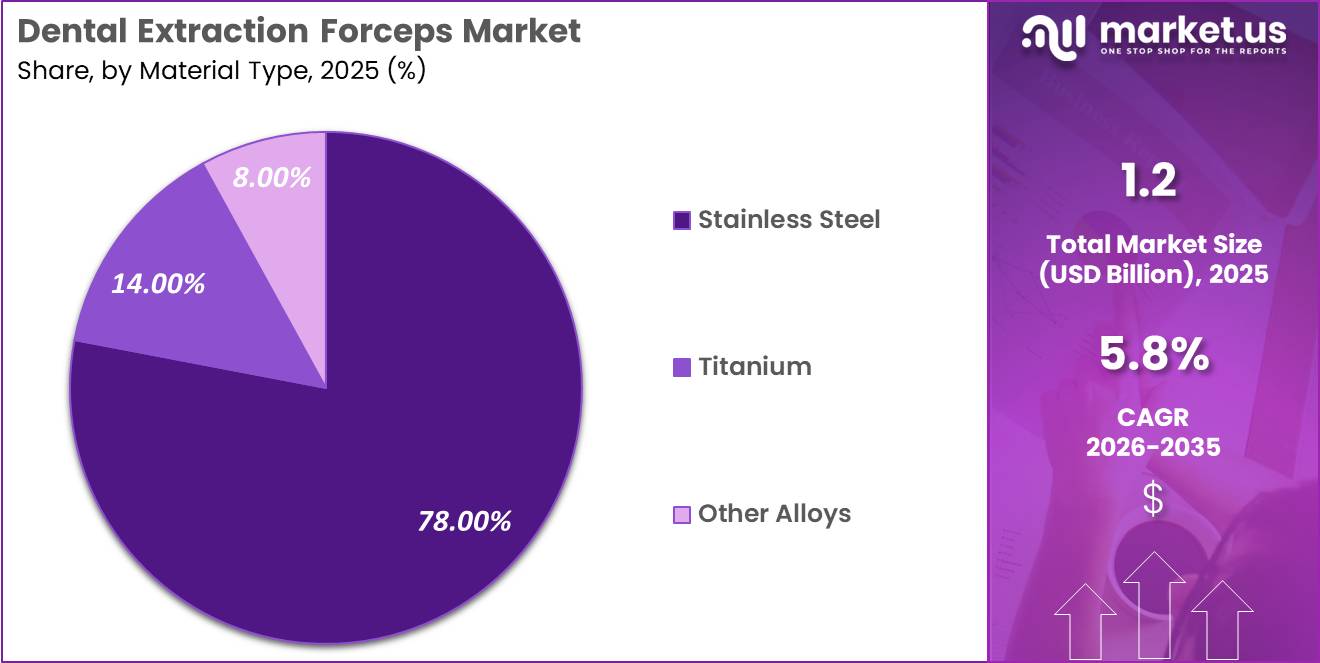

- Material Type: Stainless Steel dominates the segment, accounting for 78% of total revenue.

- Application: Tooth Extraction (General) leads the segment, accounting for 52% of total revenue.

- Product Design: Standard Forceps dominate the segment, accounting for 57% of total revenue.

- End User: Dental Clinics lead the segment, accounting for 63% of total revenue.

- Distribution Channel: Direct Institutional Sales dominate the segment, accounting for 76% of total revenue.

- Regional: North America is the dominant regional market, accounting for 37% of global sales.

Product Type Analysis

The Dental Extraction Forceps Market by product type is structured around anatomical specificity and procedural efficiency. Upper Jaw Extraction Forceps dominate the segment, accounting for 44.00% market share in 2025, driven by their high utilisation in routine maxillary extractions. Maxillary teeth often require forceps with specialised beak curvature and angulation to accommodate thinner cortical bone and varied root morphology, supporting consistent demand across general dental practices.

Lower Jaw Extraction Forceps represent 36.00% of the market, reflecting their essential role in mandibular procedures where higher bone density necessitates stronger grip and controlled leverage. The segment benefits from growing procedural volumes in molar and premolar extractions, particularly in adult and geriatric populations. The Speciality Forceps segment, including wisdom tooth and pediatric forceps, contributes 20.00% market share.

Demand is supported by increasing third-molar removal procedures and pediatric dental interventions requiring size-specific, atraumatic designs. Overall, product type segmentation highlights the importance of anatomical precision, with manufacturers focusing on expanded forceps portfolios to address diverse clinical extraction needs.

Material Type Analysis

Material selection plays a critical role in durability, sterilisation compatibility, and clinical performance within the Dental Extraction Forceps Market. Stainless Steel forceps dominate with a 78.00% market share in 2025, owing to their high tensile strength, corrosion resistance, and cost-effectiveness. Stainless steel instruments are widely preferred across dental clinics and hospitals due to their long service life and compatibility with repeated autoclave sterilisation cycles.

Titanium forceps account for 14.00% of the market, supported by growing interest in lightweight instruments that reduce operator fatigue during prolonged procedures. Titanium’s biocompatibility and resistance to corrosion make it attractive for premium and specialised applications, particularly in surgical and implant-focused practices.

The Other Alloys segment, holding 8.00% market share, includes composite metals and coated alloys designed to enhance grip, reduce glare, or improve wear resistance. While adoption remains limited due to higher costs and narrower clinical use, innovation in advanced alloys continues to create niche opportunities. Overall, stainless steel remains the industry standard, while alternative materials gain traction in high-end and speciality segments.

Application Analysis

Application-based segmentation reflects procedural frequency and clinical necessity across dental care settings. Tooth Extraction (General) leads the market with a 52.00% share in 2025, driven by the high prevalence of dental caries, periodontal disease, and routine extractions performed in primary dental care.

These procedures rely heavily on standard extraction forceps, ensuring consistent demand. Wisdom Tooth Removal accounts for 24.00% of the market, supported by rising third-molar impaction cases and increased awareness of preventive extractions among adolescents and young adults. This segment often requires specialised forceps designed for limited access and complex root anatomy.

Orthodontic Extraction contributes 14.00% market share, reflecting steady demand for premolar extractions as part of orthodontic treatment planning. Growth is supported by increasing orthodontic case volumes globally. The Surgical Extraction (Impacted Teeth) segment holds 10.00%, driven by complex cases requiring enhanced grip and precision. Collectively, application segmentation underscores strong demand across both routine and specialised extraction procedures.

End User Analysis

End-user segmentation highlights purchasing patterns and procedural concentration across healthcare settings. Dental Clinics dominate the market with a 63.00% share in 2025, as they serve as the primary point of care for routine and elective tooth extractions. High patient footfall, frequent instrument replacement, and preference for customised forceps drive sustained demand from private and group dental practices.

Hospitals account for 28.00% of the market, reflecting their role in managing complex extractions, surgical cases, and medically compromised patients. Hospital-based oral and maxillofacial departments require a broad range of forceps, including surgical and speciality designs, contributing to steady procurement volumes.

Academic & Research Institutes hold 9.00% market share, supported by dental education programs and clinical training requirements. These institutions procure forceps in bulk for student training, simulation labs, and research activities. While smaller in share, this segment plays a critical role in standardising instrument use and influencing long-term adoption trends. Overall, dental clinics remain the key demand centre, with hospitals and academic institutions providing stable secondary demand.

Product Design Analysis

Product design segmentation reflects evolving clinical preferences for efficiency, comfort, and tissue preservation. Standard Forceps lead with a 57.00% market share in 2025, driven by their widespread use in routine extractions and familiarity among practitioners. These designs offer reliable grip and durability, making them the default choice in most dental settings.

Ergonomic / Lightweight Forceps account for 31.00% of the market, supported by increasing focus on clinician comfort and reduction of hand fatigue during high procedure volumes. Improved handle geometry, balanced weight distribution, and enhanced grip textures are key adoption drivers, particularly in busy dental clinics and surgical practices.

Atraumatic Forceps hold 12.00% market share, reflecting growing emphasis on minimally invasive techniques and alveolar bone preservation. These forceps are increasingly used in pre-implant and cosmetic dentistry workflows where socket integrity is critical. Although adoption is slower due to higher costs and technique sensitivity, demand is rising steadily. Overall, while standard designs remain dominant, innovation in ergonomic and atraumatic forceps is reshaping future product preferences.

Distribution Channel Analysis

Distribution channel dynamics in the Dental Extraction Forceps Market are shaped by procurement scale, pricing control, and supplier relationships. Direct Institutional Sales dominate with a 76.00% market share in 2025, driven by bulk purchasing by dental chains, hospitals, and academic institutions. Direct sales enable manufacturers to offer customised product bundles, consistent quality assurance, and competitive pricing, strengthening long-term contracts.

Distributors account for 18.00% of the market, serving independent dental clinics and smaller practices that prefer localised supply, faster delivery, and after-sales support. This channel remains important in regions with fragmented healthcare infrastructure where direct manufacturer reach is limited.

Online Sales represent 6.00% market share, reflecting gradual digital adoption among dental professionals. E-commerce platforms offer price transparency and convenience, particularly for replacement purchases and standard forceps. However, concerns around authenticity, quality verification, and limited customisation constrain faster growth. Overall, direct institutional sales remain the dominant channel, while distributors and online platforms provide complementary access routes, especially for smaller-scale buyers.

Key Market Segments

By Product Type

- Upper Jaw Extraction Forceps

- Lower Jaw Extraction Forceps

- Speciality Forceps (Wisdom Tooth, Pediatric)

By Material Type

- Stainless Steel

- Titanium

- Other Alloys

By Application

- Tooth Extraction (General)

- Wisdom Tooth Removal

- Orthodontic Extraction

- Surgical Extraction (Impacted Teeth)

By Product Design

- Standard Forceps

- Ergonomic / Lightweight Forceps

- Atraumatic Forceps

By End User

- Dental Clinics

- Hospitals

- Academic & Research Institutes

By Distribution Channel

- Direct Institutional Sales

- Distributors

- Online Sales

Driver

High oral disease burden sustaining extraction volumes

The first demand engine remains the sheer procedural base created by untreated decay, advanced periodontal disease, and late-stage tooth retention failure. WHO reported in 2025 that oral diseases affect nearly 3.7 billion people globally and that untreated caries in permanent teeth remains the most common health condition in the Global Burden of Disease 2021 dataset, while severe periodontitis affected more than 1 billion people in 2021 at an age-standardised prevalence of 12.5%.

Because extraction is frequently the terminal intervention after failed restorative care, especially where prevention and endodontics are under-penetrated, this burden supports recurring purchases of maxillary, mandibular, pediatric, and root-tip forceps across public hospitals, dental schools, and high-volume clinics.

Commercially, that translates into dependable baseline utilisation rather than episodic capital demand: clinics can defer premium imaging or CAD/CAM purchases, but they cannot operate oral surgery chairs without sterilizable extraction sets, which is why this driver contributes the largest incremental lift to 2026–2030 growth expectations

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High oral disease burden sustaining extraction volumes | +1.4% | APAC core, Latin America, Africa, South Asia | Short term |

| Population ageing and tooth-loss case mix expansion | +1.1% | North America, EU, Japan, China, South Korea | Medium term |

| Access expansion in community, ambulatory, and rural dental care | +0.9% | India, ASEAN, Brazil, Mexico, Middle East spill-over | Short term |

| Reprocessing and compliance tightening for reusable instruments | +0.8% | North America core, EU, UK, advanced APAC | Medium term |

| Shift toward surgical efficiency and speciality forceps replacement cycles | +0.7% | North America, EU, private APAC urban hubs | Short term |

| Implant-pathway and pre-prosthetic extraction demand | +0.6% | North America, EU, China coastal, GCC corridors | Medium term |

Challenge

Reusable forceps and similar surgical instruments face increasing compliance complexity because, despite being mechanically simple, they are regulated under stringent reusable medical device frameworks that require extensive validation of cleaning, disinfection, sterilisation, maintenance, and reuse processes.

In Europe, Class Ir requirements involve detailed documentation and notified-body oversight for reprocessing validation, while in the U.S., manufacturers must still comply with device listing, establishment registration, labelling, and post-market surveillance obligations.

This creates a persistent documentation and validation burden rather than a strict market barrier, with portfolio updates often requiring 6–12 months of additional time and increasing compliance-related payroll and external testing costs by 8–15% for smaller manufacturers.

Additional requirements such as simulated-use testing, IFU validation, residual contamination studies, and lifecycle reuse justification further slow product refresh cycles and discourage niche SKU proliferation. As a result, manufacturers increasingly consolidate product families and standardise validation frameworks across regions to manage regulatory workload, but the overall effect remains a slower time-to-market and reduced agility in launching new instrument variants.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Stainless steel cost volatility | -1.1% | North America core, EU manufacturing hubs, APAC export corridors | Medium term (2-4 years) |

| Reusable instrument compliance load | -0.9% | EU regulatory hubs, U.S. import channels, UK compliance market | Medium term (2-4 years) |

| Sterilisation validation burden | -0.8% | North America clinics, EU hospital dentistry, urban APAC chains | Medium term (2-4 years) |

| Dental staffing and throughput gaps | -1.2% | U.S. core, Western Europe, developed APAC metros | Long term (≥ 4 years) |

| Fragmented procurement price pressure | -0.7% | India, Southeast Asia, Latin America, private-clinic channels globally | Short term (≤ 2 years) |

| UDI and traceability digitisation | -0.6% | EU device market, U.S. listings, China transition markets | Medium term (2-4 years) |

Restraint

MDR/FDA compliance load

The biggest structural drag remains the mismatch between rising regulatory burden and the modest ASP of extraction forceps, because reusable surgical instruments in Europe still require notified-body involvement under MDR Article 52(7), and eligible legacy pathways run only to 31 December 2028, forcing manufacturers to absorb recertification, technical file remediation, sterilization validation, post-market surveillance, and labeling upgrades on product families that often generate limited annual revenue per SKU.

In parallel, U.S. suppliers of dental forceps generally remain subject to annual establishment registration, device listing, labelling controls, and UDI-related traceability expectations, even where a 510(k) exemption applies, which raises fixed QA/RA spend and pushes smaller OEMs toward SKU rationalisation rather than portfolio expansion.

For a mid-tier catalogue supplier, this can realistically translate into 250 to 450 basis points of EBIT dilution on low-volume forceps lines, 6 to 12 months of delayed EU market continuity work for borderline legacy assortments, and a 3% to 6% reduction in active regional SKU breadth as companies prioritise high-turn patterns over niche extraction variants, thereby clipping forecast volume conversion despite stable clinical need.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| MDR/FDA compliance load | -1.2% | EU core, North America core | Medium term |

| Steel and passivation inflation | -0.9% | EU, North America, APAC export corridors | Short term |

| Tariffs and landed-cost volatility | -0.8% | U.S. imports, China-linked corridors, EU-U.S. trade lanes | Short term |

| Clinic budget pressure | -1.0% | EU, Latin America, South Asia, low-income U.S. pockets | Medium term |

| Workforce and procedure bottlenecks | -0.7% | U.S. shortage states, rural EU, emerging APAC | Medium term |

| Freight and inventory disruption | -0.6% | APAC-Europe, APAC-North America, distributor hubs | Short term |

Opportunity

DSO platform partnerships

This is an opportunity rather than a current market driver because most extraction forceps are still sold as fragmented SKU-level instruments into independent clinics, whereas dental support organisations are increasingly centralising procurement, training, technology adoption, and multi-site standardisation, creating a future route for vendors to convert one-off instrument sales into enterprise contracts with formulary status, recurring replenishment, and data-linked account expansion.

DSOs have expanded their reach by consolidating single clinics into scaled networks and using centralized purchasing to improve efficiency, so a supplier that secures preferred-vendor status across even 300 to 1,000 chairs can cut customer-acquisition cost by an estimated 25% to 40%, raise account lifetime value by 2.0x to 3.0x versus independent-practice selling.

Layer 300 to 600 basis points of EBITDA improvement through lower field-sales intensity, tighter SKU rationalization, and cross-selling of elevators, root-tip picks, surgical sets, and sterilization accessories; in a market where baseline growth is procedure-led, that procurement-platform capture can realistically add about 1.6 percentage points to CAGR by shifting share faster than underlying extraction volume grows.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| DSO platform partnerships | +1.6% | North America core, Western Europe, ANZ | Short term (≤ 2 years) |

| Pediatric sedation kits | +1.3% | North America, GCC, urban APAC, Latin America private care | Short term (≤ 2 years) |

| Value-engineered LMIC portfolios | +2.1% | India, SEA, Africa, Latin America | Medium term (2-4 years) |

| Oral surgery adjacency bundles | +1.8% | North America, EU, Japan, South Korea | Medium term (2-4 years) |

| Eco-sterile service models | +1.1% | EU, UK, Nordics, Canada | Medium term (2-4 years) |

| Geriatric and full-arch extraction sets | +1.5% | Japan, EU, China urban, North America | Long term (≥ 4 years) |

Regional Analysis

In 2025, North America led the market, achieving over 37.00% share with a revenue of US$ 0.44 billion. The global Dental Extraction Forceps Market demonstrates distinct regional dynamics shaped by healthcare infrastructure, oral disease prevalence, reimbursement systems, and access to dental care services.

North America holds a significant share of the market, driven by advanced dental infrastructure, high adoption of minimally invasive oral surgery tools, and the strong presence of dental practitioners in the United States and Canada. Increasing cases of dental caries and periodontal diseases, along with routine tooth extraction procedures in outpatient settings, continue to support steady demand.

Europe follows closely, supported by well-established public healthcare systems, a rising geriatric population, and a strong emphasis on preventive dentistry. Countries such as Germany, the United Kingdom, and France contribute substantially due to high procedural volumes and continuous upgrades in dental surgical instruments.

Asia-Pacific is the fastest-growing regional market, fueled by a large patient pool, improving healthcare access, and expanding dental clinic networks in countries such as China, India, and Japan. Rising awareness of oral hygiene and increasing affordability of dental treatments are further accelerating adoption.

Latin America shows moderate growth, with Brazil and Mexico leading due to gradual improvements in dental care infrastructure. Meanwhile, the Middle East and Africa region is emerging, driven by increasing healthcare investments, urbanisation, and growing dental tourism in select Gulf countries, though limited access in rural areas still restrains overall penetration.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Player Analysis

Competitive advantage in the global dental extraction forceps market is achieved through precision instrument manufacturing expertise, surgical-grade stainless steel material quality, comprehensive product range coverage across pediatric, adult, and speciality extraction forceps designs, and established distribution relationships with dental practices, hospitals, and dental supply distributors globally. These factors collectively enable manufacturers to ensure consistent product reliability, clinical performance, and wide accessibility across both developed and emerging healthcare markets.

Major strategic priorities for leading manufacturers include continued investment in ergonomic instrument design, improving clinician grip and procedural control, expansion of sterilisation-compatible and corrosion-resistant material formulations, and development of specialised forceps designs targeting specific tooth morphology and surgical extraction techniques.

Regulatory compliance with medical device standards, including FDA 510(k) clearance and CE marking, combined with dental school and institutional procurement relationships, represents a critical competitive differentiator for manufacturers seeking sustained market access across hospital dental departments and private practice procurement channels globally.

Top Key Players

- Hu-Friedy (STERIS)

- Dentsply Sirona

- Carl Martin GmbH

- ASA Dental

- A. Titan Instruments

- GDC (Global Dental Products)

- Nordent Manufacturing

- Integra LifeSciences

- Brasseler USA

- KLS Martin Group

- LM-Dental

- J&J Instruments

- Medesy S.r.l.

- Other Key Players

Recent Developments

- In January 2026, Hu-Friedy (STERIS) launched an expanded range of pediatric dental extraction forceps featuring an enhanced ergonomic handle design, targeting pediatric dental practices and hospital dental departments seeking improved precision instruments for younger patients’ extraction procedures.

- In February 2026, Dentsply Sirona introduced a new corrosion-resistant surgical stainless steel forceps line incorporating advanced sterilisation-cycle durability testing, targeting institutional dental supply distributors and hospital procurement buyers across North American and European markets.

- In March 2026, KLS Martin Group expanded its speciality extraction forceps portfolio with new root-tip and molar-specific designs, targeting oral surgery practices and dental hospital departments requiring precision instruments for complex extraction procedures.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 1.2 Billion |

| Forecast Revenue (2035) | US$ 2.1 Billion |

| CAGR (2026-2035) | 5.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Upper Jaw Extraction Forceps, Lower Jaw Extraction Forceps, Specialty Forceps (Wisdom Tooth, Pediatric)), By Material Type (Stainless Steel, Titanium, Other Alloys), By Application (Tooth Extraction (General), Wisdom Tooth Removal, Orthodontic Extraction, Surgical Extraction (Impacted Teeth)), By Product Design (Standard Forceps, Ergonomic/Lightweight Forceps, Atraumatic Forceps), By End User (Dental Clinics, Hospitals, Academic & Research Institutes), By Distribution Channel (Direct Institutional Sales, Distributors, Online Sales) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Hu-Friedy (STERIS), Dentsply Sirona, Carl Martin GmbH, ASA Dental, Hu-Friedy Group, A. Titan Instruments, GDC (Global Dental Products), Nordent Manufacturing, Integra LifeSciences, Brasseler USA, Hu-Friedy Mfg. Co., KLS Martin Group, LM-Dental, J&J Instruments, Medesy S.r.l., |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |