Quick Navigation

Market Overview

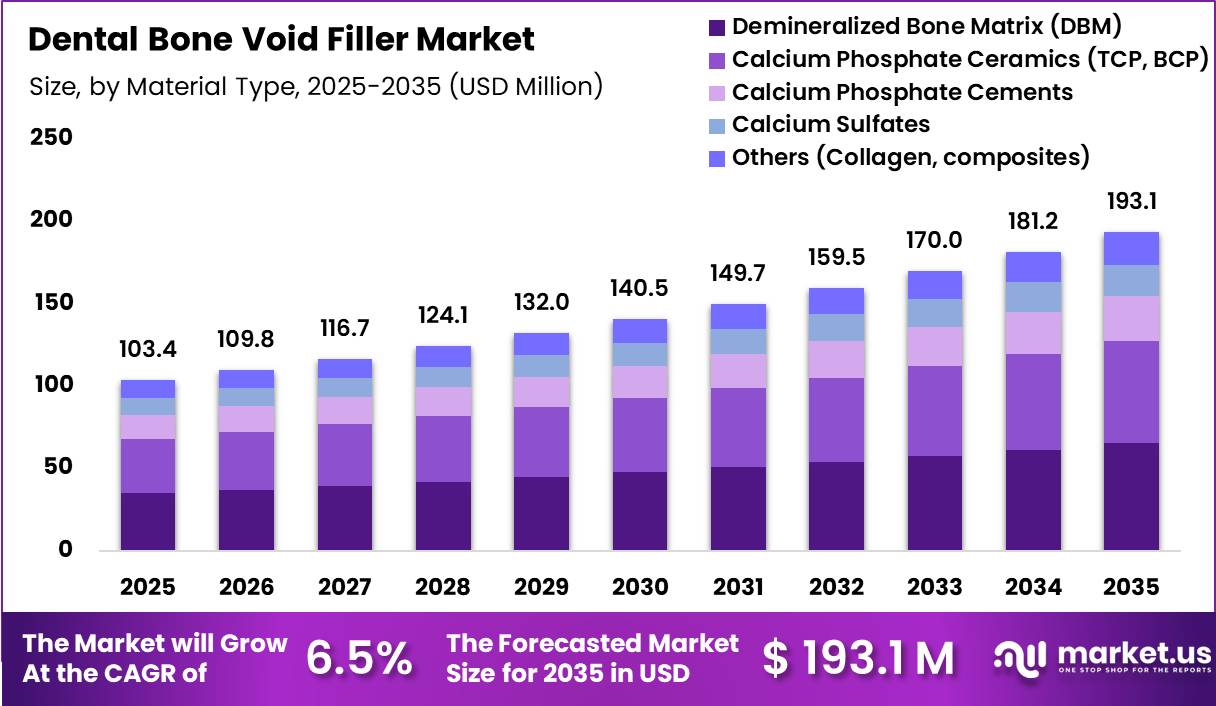

Global Dental Bone Void Filler Market size is expected to be worth around US$ 193.1 Million by 2035 from US$ 103.4 Million in 2025, growing at a CAGR of 6.5% during the forecast period from 2026 to 2035. In 2025, Europe led the market, achieving over 39.00% share with a revenue of US$ 40.33 Million.

The dental bone void filler market is an important segment of the dental biomaterials industry, supporting procedures that restore or regenerate bone in the oral and maxillofacial region. Dental bone void fillers are used to fill, augment, or reconstruct bone defects caused by tooth loss, periodontal disease, trauma, congenital conditions, or surgical procedures.

According to the U.S. Food and Drug Administration (FDA), dental bone grafting materials may include hydroxyapatite, tricalcium phosphate, collagen, and biodegradable polymer-based materials designed to support bone regeneration in oral defects.

Demand for dental bone void fillers is closely linked to the growing volume of dental implant procedures and the increasing prevalence of tooth loss among aging populations. Bone grafting is frequently performed before or during implant placement to ensure adequate jawbone volume and density. The American Association of Oral and Maxillofacial Surgeons (AAOMS) notes that bone grafting is widely used in tooth extraction sites, implant procedures, facial trauma reconstruction, and corrective jaw surgeries to restore bone quantity and function.

Technological advancements have expanded the range of available materials, including autografts, allografts, xenografts, and synthetic substitutes. Clinical research indicates that these materials are commonly used in procedures such as ridge augmentation, sinus lift surgery, socket preservation, and periodontal regeneration. Synthetic bone substitutes are gaining attention because they offer consistent quality, eliminate donor-site complications, and are readily available for clinical use.

The market continues to benefit from increasing awareness of oral health, rising adoption of dental implants, and ongoing innovation in regenerative dentistry. As healthcare providers seek predictable and minimally invasive solutions for bone reconstruction, dental bone void fillers are expected to remain a critical component of modern dental treatment protocols.

Key Takeaways

- Market Size: Global Dental Bone Void Filler Market size is expected to be worth around US$ 193.1 Million by 2035 from US$ 103.4 Million in 2025.

- Market Share: The market is growing at a CAGR of 6.5% during the forecast period from 2026 to 2035.

- Material Type: Demineralized Bone Matrix (DBM) dominated the dental bone void filler market with a 33.90% share in 2025.

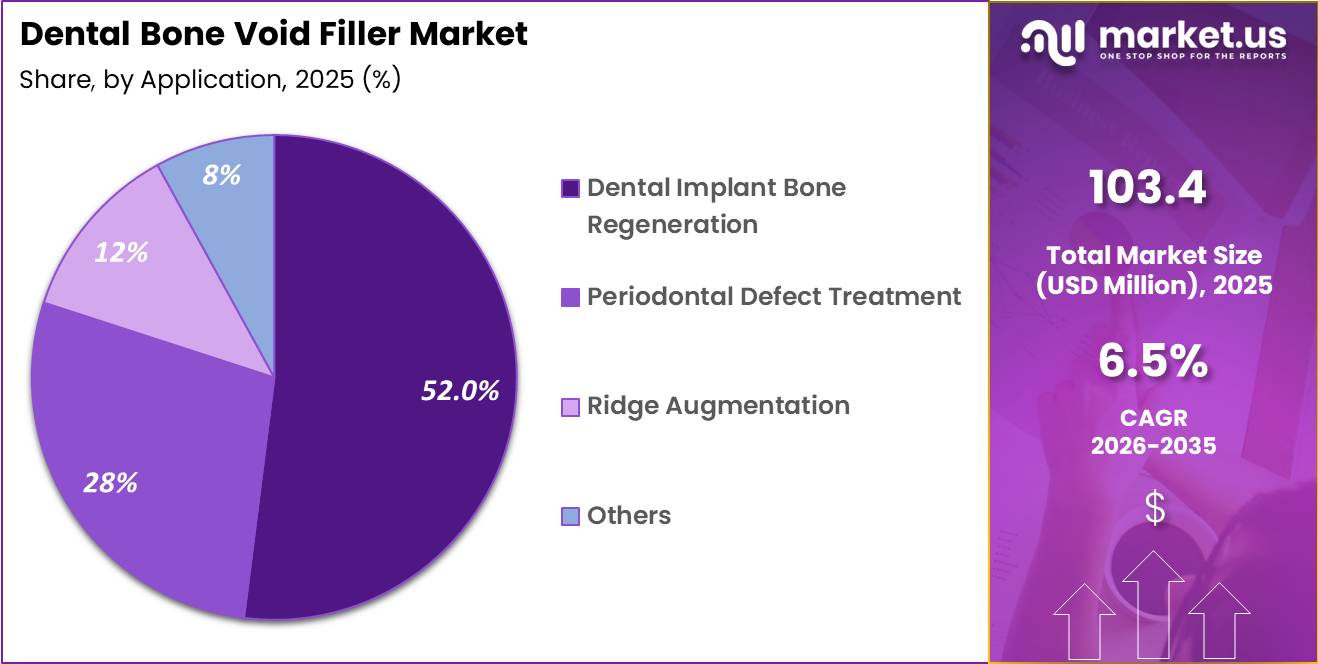

- Application: Dental Implant Bone Regeneration accounted for the largest share of the dental bone void filler market, representing 52.00% of total revenue in 2025.

- End User: Dental Clinics dominated the dental bone void filler market with a 61.00% share in 2025.

- Form: Putty/Gel dominated the dental bone void filler market with a 44.00% share in 2025.

- Distribution Channel: Direct Institutional Sales held the largest share of the dental bone void filler market, accounting for 78.00% of revenue in 2025.

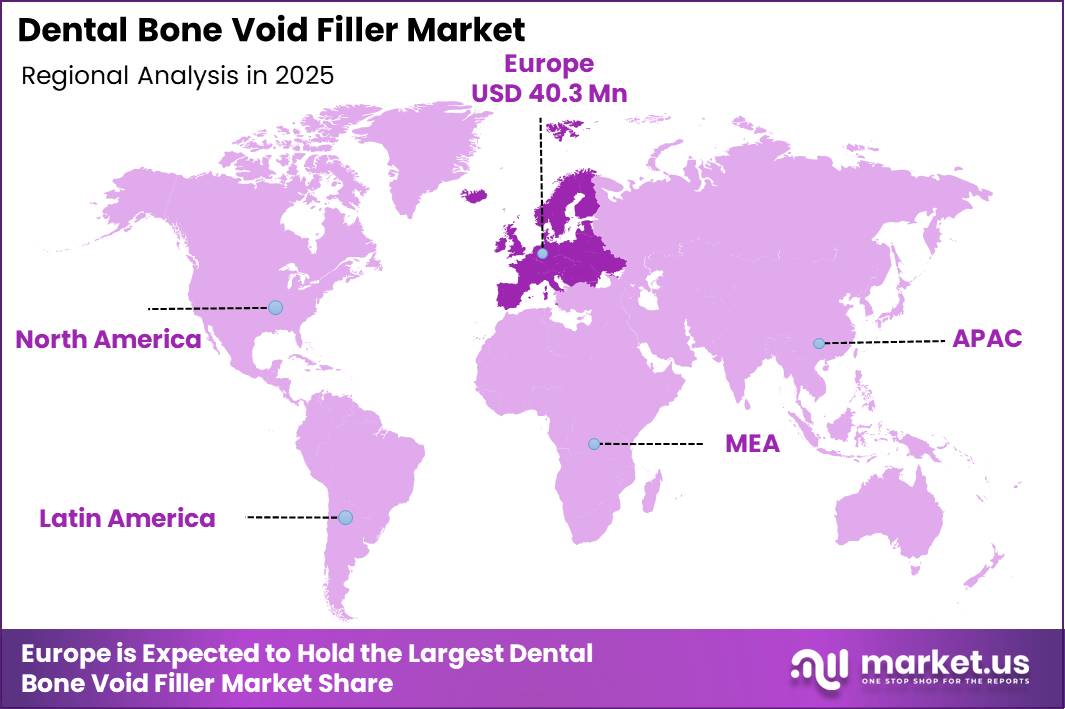

- Regional Analysis: In 2025, Europe led the market, achieving over 39.00% share with a revenue of US$ 40.33 Million.

Material Type Analysis

Demineralized Bone Matrix (DBM) dominated the dental bone void filler market with a 33.90% share in 2025. Its leadership is largely driven by its natural bone-regenerating properties and strong compatibility with surrounding tissues, making it a preferred choice in dental implant and periodontal procedures. DBM contains naturally occurring growth factors that support new bone formation, helping clinicians achieve predictable healing outcomes.

The increasing preference for biologically active grafting materials and the rising volume of dental reconstruction procedures continue to strengthen the segment’s position. Companies such as Geistlich Pharma AG have contributed to the growing adoption of advanced regenerative solutions that improve clinical performance and patient recovery.

Calcium phosphate ceramics are emerging as a strong growth area due to their excellent structural support and osteoconductive characteristics. These materials are increasingly used in cases requiring long-term bone stability and volume preservation. Calcium phosphate cements are also gaining attention because of their moldability and ease of application during surgical procedures.

Meanwhile, calcium sulfate and composite-based materials continue to find niche applications where faster resorption or customized regenerative properties are required. Ongoing innovation in biomaterials is expected to expand the range of treatment options available to dental professionals.

Application Analysis

Dental Implant Bone Regeneration accounted for the largest share of the dental bone void filler market, representing 52.00% of total revenue in 2025. The segment dominates because successful implant placement often depends on adequate bone volume and density, making bone regeneration procedures an essential step in many treatments.

Rising rates of tooth loss, increasing demand for dental implants, and growing patient awareness regarding long-term restorative solutions continue to support market expansion. Dental practitioners are increasingly incorporating bone fillers to improve implant stability and treatment outcomes. Companies such as Straumann Group have played an important role in advancing implant-focused regenerative solutions that support bone growth and integration.

Periodontal defect treatment is emerging as a significant growth area as awareness of gum disease management increases worldwide. More patients are seeking treatments that preserve natural teeth and restore supporting bone structures, creating new opportunities for regenerative products.

Ridge augmentation is also gaining traction due to the growing need for bone enhancement before implant placement. Other specialized applications, including sinus lift and socket preservation procedures, continue to contribute to market growth as clinicians adopt more comprehensive regenerative treatment approaches.

End User Analysis

Dental Clinics dominated the dental bone void filler market with a 61.00% share in 2025. Their leadership is primarily attributed to the large volume of implant placements, periodontal therapies, and routine bone grafting procedures performed in specialized dental settings. Clinics offer convenient access to treatment, personalized patient care, and advanced dental technologies, making them the preferred choice for both practitioners and patients.

The expansion of private dental practices and growing investments in digital dentistry further support the segment’s dominance. Companies such as Dentsply Sirona continue to support clinics with innovative solutions designed to improve treatment efficiency and clinical outcomes.

Hospitals remain an important contributor to market demand, particularly for complex oral and maxillofacial surgeries that require extensive bone reconstruction. Academic and research institutes are also experiencing steady growth as they focus on biomaterial research, clinical training, and the development of next-generation regenerative products.

Collaboration between educational institutions and industry participants is helping accelerate innovation and improve the overall adoption of advanced dental bone fillers across global healthcare systems.

Form Analysis

Putty/Gel dominated the dental bone void filler market with a 44.00% share in 2025. This segment leads because of its superior handling properties, ease of placement, and ability to adapt to irregular bone defects. Dental surgeons prefer putty and gel formulations as they remain stable at the treatment site and simplify the grafting process, reducing procedure time while improving surgical precision.

These benefits make them particularly valuable in implant-related bone regeneration and periodontal applications. The growing preference for minimally invasive dental procedures has further strengthened demand for these user-friendly formulations. Companies such as Osteogenics Biomedical have expanded product offerings focused on convenient and effective regenerative solutions.

Granules are witnessing increasing adoption due to their versatility and ability to provide structural support during bone healing. Paste formulations are also gaining popularity because they can be easily delivered into difficult-to-reach treatment areas, improving clinical flexibility.

Other specialized forms continue to serve specific surgical requirements where customized graft configurations are needed. As manufacturers develop advanced delivery systems and improved biomaterials, the market is expected to see greater adoption of innovative filler formats that enhance both clinician experience and patient outcomes.

Distribution Channel Analysis

Direct Institutional Sales held the largest share of the dental bone void filler market, accounting for 78.00% of revenue in 2025. The segment dominates because hospitals, dental clinics, and specialized surgical centers prefer sourcing products directly from manufacturers to ensure quality assurance, product availability, and technical support. Direct purchasing arrangements also help healthcare providers secure competitive pricing and access to professional training programs.

As regenerative dental procedures become increasingly sophisticated, clinicians value closer relationships with manufacturers that can provide product expertise and clinical guidance. Companies such as BioHorizons have strengthened market presence through direct engagement with dental professionals and treatment centers.

Distributor networks continue to expand their role by improving product accessibility across regional and local markets. They remain particularly important in emerging economies where direct manufacturer reach may be limited.

Online procurement is another rapidly growing channel, supported by digital transformation within healthcare purchasing systems. Dental practices are increasingly using online platforms for streamlined ordering and inventory management, creating new opportunities for suppliers to enhance customer engagement and improve purchasing efficiency.

Key Market Segments

Material Type

- Demineralized Bone Matrix (DBM)

- Calcium Phosphate Ceramics (TCP, BCP)

- Calcium Phosphate Cements

- Calcium Sulfates

- Others (Collagen, composites)

Application

- Dental Implant Bone Regeneration

- Periodontal Defect Treatment

- Ridge Augmentation

- Others

End User

- Dental Clinics

- Hospitals

- Academic & Research Institutes

Form

- Putty / Gel

- Granules

- Paste

- Others

Distribution Channel

- Direct Institutional Sales

- Distributors

- Online Procurement

Opportunitys

Ridge preservation bundles

Alveolar ridge preservation is already clinically recognized, but its broader commercialization as a standardized post-extraction bundle remains underpenetrated, which is why it is an opportunity rather than a current driver: the baseline market benefits from routine graft use in implants, whereas upside comes from packaging socket filler, membrane, digital planning, and deferred implant conversion into a protocolized revenue stack sold at the time of extraction.

The white space is large because ridge preservation in the posterior maxilla has been shown to reduce the odds of later sinus floor augmentation to 0.18 versus spontaneous healing, while preserving ridge height and reducing sinus pneumatization, which means suppliers can position fillers as a cost-avoidance tool rather than a commodity input.

With graft substitute costs cited around $46.2 to $140 and membranes at $12 to $189, the monetization lever is not only material ASP but attach-rate expansion, where a supplier that lifts post-extraction biologic bundle penetration by 15% to 20% across implant-oriented clinics could plausibly add 200 to 300 basis points to site-level regenerative revenue growth while improving downstream implant case conversion and reducing surgical complexity.

This is especially attractive in North America, Europe, Japan, and South Korea, where older populations are rising and clinicians increasingly seek predictable workflows; Organisation for Economic Co-operation and Development notes the old-age dependency ratio rose from 21 per 100 working-age people in 1994 to 33 in 2024 and is expected to reach 55 over the next 30 years, expanding the pool needing extraction-to-restoration planning rather than single-visit intervention.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Ridge preservation bundles | +2.1% | North America, EU, Japan, South Korea | Short term |

| DSO protocol rollouts | +1.8% | North America core, UK, Australia | Short term |

| Synthetic premium shift | +1.6% | EU, North America, China urban | Medium term |

| Medically complex implant pathways | +1.4% | OECD markets, GCC, Tier-1 APAC | Medium term |

| Value-tier emerging access | +2.4% | India, ASEAN, LATAM, MENA | Medium term |

| Biomaterial M&A roll-ups | +1.2% | Global, especially EU and U.S. | Long term |

Drivers

Implant case expansion from tooth loss and periodontitis burden

The most durable growth engine is the rising pool of patients entering implant pathways after periodontal destruction, extraction, and edentulism, because bone void fillers are frequently used in socket preservation, ridge augmentation, and sinus floor elevation before or during implant placement.

World Health Organization states oral diseases affect nearly 3.7 billion people globally, while severe periodontitis remains one of the most prevalent chronic oral conditions; a recent burden study estimated severe periodontitis incident cases rose from about 50.8 million in 1990 to 89.6 million in 2021, a 76.3% increase, enlarging the addressable reconstruction base even before elective esthetic demand is counted.

In the United States, long-run implant utilization has already shown structural momentum, with prevalence rising from 0.7% in 1999–2000 to 5.7% in 2015–2016 and an average covariate-adjusted annual increase of 14%, indicating that a larger share of restorative cases is migrating toward implant-supported rehabilitation rather than conventional bridges or removable prosthetics.

For bone void filler vendors, that shifts the revenue model toward higher-value procedure bundles: filler plus membrane, biologic handling aids, and indication-specific kits for extraction sockets, horizontal ridge defects, and peri-implant defects, which typically increases average revenue per case and improves distributor pull-through in specialist oral surgery and implantology channels.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Implant case expansion from tooth loss and periodontitis burden | +1.9% | North America core, EU, Japan, South Korea, urban China, Gulf | Medium term (2-4 years) |

| Aging demographics raising graftable ridge preservation and sinus lift volumes | +1.4% | EU, Japan, South Korea, North America, China tier-1/2 spill-over | Long term (≥ 4 years) |

| Premium shift toward synthetic and xenograft biomaterials with faster chairside workflow | +1.2% | North America core, EU, APAC private-clinic corridors | Short term (≤ 2 years) |

| Regulatory tightening improving product quality and favoring scaled suppliers | +0.8% | U.S., EU, UK aligned markets, export-oriented APAC manufacturing hubs | Medium term (2-4 years) |

| High implant economics supporting adjunct graft attachment rates | +1.0% | U.S., Canada, Western Europe, Australia, affluent APAC metros | Short term (≤ 2 years) |

| Digital implant planning and guided surgery increasing graft conversion efficiency | +0.9% | North America, Germany/Italy/Spain, South Korea, China premium clinics | Medium term (2-4 years) |

Challenges

Regulatory pathway complexity

Dental bone void filler manufacturers face a persistent operating challenge because approval, clinical evidence, and post-market obligations remain fragmented across the US, EU, and other major jurisdictions rather than converging into a single usable evidence package.

In the US, U.S. Food and Drug Administration guidance for dental bone grafting material devices specifies structured animal-study expectations including at least three timepoints and at least three animals per treatment and control group per timepoint in suitable models, which increases preclinical design complexity, extends validation cycles, and raises dossier-preparation costs before commercialization even begins.

In Europe, EU Medical Device Regulation obligations require proactive post-market surveillance, trend reporting, and broader clinical evaluation maintenance, meaning manufacturers must continuously fund regulatory upkeep rather than treat compliance as a one-time launch event.

For a niche dental biomaterials category, this creates launch sequencing delays that can reasonably stretch 12–24 months across jurisdictions, increase regulatory overhead by mid-single-digit percentage points of revenue for smaller portfolios, and force companies to prioritize only the highest-return geographies first, creating a modeled friction drag of roughly 1.1% points on full growth potential.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Regulatory pathway complexity | -1.1% | EU compliance hubs, US approval corridor, Japan and India review markets | Long term (≥ 4 years) |

| Calcium phosphate input volatility | -0.8% | China-linked supply nodes, EU processors, North America import channels | Medium term (2–4 years) |

| Allograft logistics fragility | -0.9% | India, Southeast Asia, Latin America, parts of Eastern Europe | Long term (≥ 4 years) |

| Surgical talent bottleneck | -1.0% | US shortage counties, UK backlog zones, APAC secondary cities | Long term (≥ 4 years) |

| Evidence consistency gap | -0.7% | US and EU clinical centers, adoption-sensitive emerging markets | Medium term (2–4 years) |

| Scale-up of advanced grafts | -0.6% | North America and EU innovation clusters, selective APAC manufacturing bases | Long term (≥ 4 years) |

Restraints

Stricter clinical evidence burden

The first major restraint is the tightening of evidence expectations for dental bone grafting materials, because U.S. Food and Drug Administration’s 2024 draft guidance moved the center of gravity away from light predicate-based equivalence toward more explicit in vivo performance packages, including clinically relevant canine or porcine models, at least three evaluation time points, and at least three animals per treatment per time point, with radiography, histology, histomorphometry, and increasingly microCT-style characterization.

In practice, that raises premarket study complexity, extends validation calendars by roughly 6 to 12 months for smaller manufacturers, and lifts regulatory burn through added CRO, animal-model, imaging, and documentation costs before first revenue, which is especially damaging in a market where many products compete on handling, osteoconductivity claims, and indication breadth rather than radical therapeutic differentiation.

The strategic effect is slower SKU refresh, delayed geographic line extensions, and more conservative distributor onboarding, so even where demand for ridge preservation and implant-site development remains intact, commercialization velocity drops and forecast CAGR is clipped by an estimated 1.4 percentage points, with the harshest impact on venture-backed, subscale, and private-label entrants that cannot easily absorb higher pre-launch evidence spend.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter clinical evidence burden | -1.4% | North America core, EU | Short term (≤ 2 years) |

| EU MDR certification drag | -1.2% | EU, UK-linked Europe, export hubs | Medium term (2-4 years) |

| Out-of-pocket procedure deferral | -1.6% | APAC, LATAM, parts of Europe, uninsured NA | Short term (≤ 2 years) |

| Input and sterilization cost inflation | -0.9% | North America, EU, APAC corridors | Short term (≤ 2 years) |

| Freight and trade-policy volatility | -0.8% | US import channels, EU-Asia lanes, APAC corridors | Short term (≤ 2 years) |

| Premium pricing versus implant economics | -1.1% | Emerging markets, mid-tier clinics globally | Medium term (2-4 years) |

Regional Analysis

Europe dominated the Dental Bone Void Filler Market

Europe dominated the Dental Bone Void Filler Market in 2025, accounting for over 39.0% of global revenue and generating approximately US$ 40.33 million. The region’s leadership is primarily supported by its well-established dental care infrastructure, widespread adoption of advanced regenerative dentistry techniques, and a high volume of dental implant procedures.

Countries such as Germany, France, Italy, and Spain continue to witness strong demand for bone augmentation procedures due to the growing prevalence of periodontal diseases, tooth loss, and age-related oral health conditions.

Europe also benefits from the presence of leading dental biomaterial manufacturers, extensive clinical research activities, and favorable reimbursement frameworks in several countries, which encourage the use of advanced bone void fillers in routine dental practice. Additionally, the region maintains stringent quality and safety standards for dental biomaterials, increasing clinician confidence and supporting the adoption of premium grafting solutions.

The region’s market growth is further reinforced by increasing awareness of aesthetic dentistry, rising demand for dental implants among the aging population, and continuous technological advancements in synthetic and bioengineered bone graft materials. Europe has one of the world’s largest elderly populations, a demographic highly susceptible to tooth loss and bone resorption, creating sustained demand for bone regeneration products.

Furthermore, growing investments in dental research and innovation are enabling the development of highly biocompatible and osteoconductive bone void fillers that improve treatment outcomes. The expanding popularity of minimally invasive dental procedures and the increasing number of specialized dental clinics across Europe are also contributing to market expansion.

With strong healthcare systems, a mature dental industry, and ongoing advancements in regenerative dentistry, Europe is expected to maintain its leading position in the Dental Bone Void Filler Market throughout the forecast period.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Player Analysis

The Dental Bone Void Filler Market is moderately consolidated, with a mix of global medical device leaders and specialized dental biomaterial companies competing through innovation, clinical validation, and comprehensive treatment solutions.

Leading participants such as Medtronic, Stryker Corporation, Zimmer Biomet, Johnson & Johnson (DePuy Synthes), and Geistlich Pharma AG hold strong market positions due to their extensive product portfolios, established distribution networks, and long-standing relationships with healthcare providers.

Competition is increasingly centered on the development of advanced bone graft substitutes that offer enhanced biocompatibility, faster bone regeneration, and improved handling characteristics for dental and maxillofacial procedures. Companies are also investing in clinician education and evidence-based product development to strengthen market presence and support adoption across dental practices and surgical centers.

Competitive strategies within the market focus heavily on research and development, strategic partnerships, and continuous product innovation. Medtronic and Stryker Corporation leverage their broad orthopedic and regenerative medicine expertise to expand biomaterial capabilities, while Zimmer Biomet and Johnson & Johnson (DePuy Synthes) emphasize integrated surgical solutions that improve procedural efficiency and clinical outcomes.

Geistlich Pharma AG remains a key innovator in dental regeneration, focusing on scientifically validated biomaterials tailored for implantology and periodontal applications. Market participants are increasingly pursuing workflow integration by combining bone void fillers with digital treatment planning, implant systems, and regenerative product ecosystems.

This ecosystem-based approach enables companies to deliver comprehensive solutions rather than standalone products, strengthening customer loyalty and creating competitive differentiation in the evolving dental regenerative care landscape.

Top Key Players

- Medtronic

- Stryker Corporation

- Zimmer Biomet

- Johnson & Johnson (DePuy Synthes)

- Geistlich Pharma AG

- Dentsply Sirona

- Straumann Group

- BioHorizons

- Osteogenics Biomedical

- Collagen Matrix Inc.

- Curasan AG

- Graftys

- BONESUPPORT AB

- RTI Surgical

- Dentium Co., Ltd.

Recent Developments

- In April 2026, Theradaptive announced completion of patient enrollment in the RESTORE clinical study evaluating OsteoAdapt® DE, a regenerative bone graft technology designed for alveolar ridge augmentation and dental bone reconstruction procedures.

- In February 2026, Nobel Biocare acquired Versah®, adding the Densah® Bur and Osseodensification technology platform used in ridge expansion, sinus lift procedures, and implant-site bone preservation to its regenerative dentistry portfolio.

- In October 2025, Geistlich Pharma launched Geistlich Bio-Gide® Forte in North America, a next-generation collagen membrane developed for guided bone regeneration and dental implant site development with enhanced tensile strength and handling characteristics.

- In March 2026, OsteoGen introduced its Bioactive Crystal Technology (BCT)-based dental bone graft platform, utilizing non-sintered calcium phosphate crystals designed to improve bone regeneration compared with traditional ceramic graft materials.

Report Scope

| Report Features | Description |

| Market Value (2025) | US$ 103.4 Million |

| Forecast Revenue (2035) | US$ 193.1 Million |

| CAGR (2026-2035) | 6.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material Type (Demineralized Bone Matrix (DBM), Calcium Phosphate Ceramics (TCP, BCP), Calcium Phosphate Cements, Calcium Sulfates, Others (Collagen, composites)), By Application (Dental Implant Bone Regeneration, Periodontal Defect Treatment, Ridge Augmentation, Others), By End User (Dental Clinics, Hospitals, Academic & Research Institutes), By Form (Putty / Gel, Granules, Paste, Others), By Distribution Channel (Direct Institutional Sales, Distributors, Online Procurement) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Medtronic, Stryker Corporation, Zimmer Biomet, Johnson & Johnson (DePuy Synthes), Geistlich Pharma AG, Dentsply Sirona, Straumann Group, BioHorizons, Osteogenics Biomedical, Collagen Matrix Inc., Curasan AG, Graftys, BONESUPPORT AB, RTI Surgical, Dentium Co., Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |