Quick Navigation

Report Overview

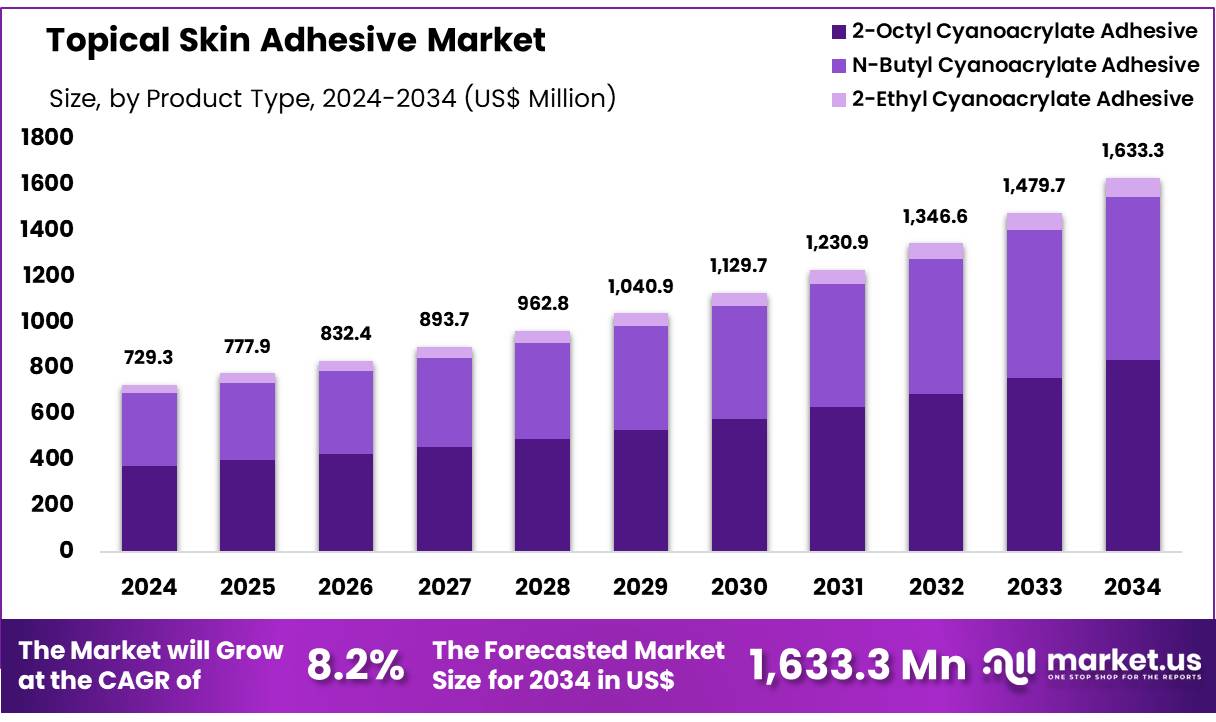

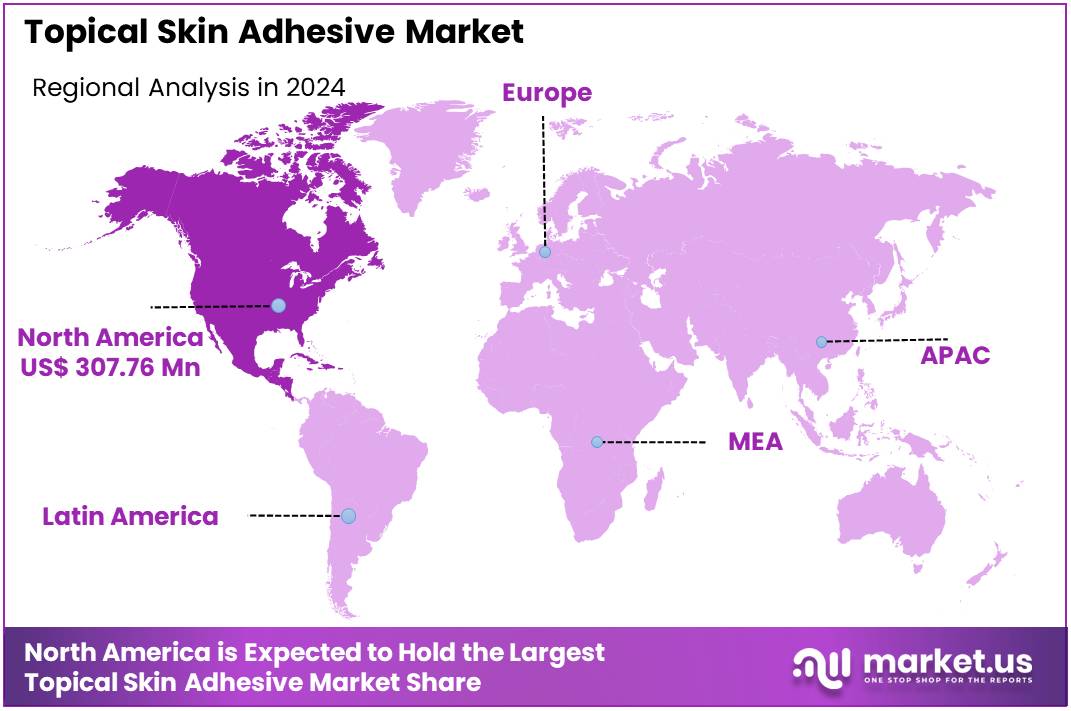

Global Topical Skin Adhesive Market size is expected to be worth around US$ 1633.3 Million by 2034 from US$ 729.30 Million in 2024, growing at a CAGR of 8.2% during the forecast period from 2024 to 2034. In 2024, North America led the market, achieving over 42.20% share with a revenue of US$ 307.76 Million.

The global topical skin adhesives market is experiencing significant growth, driven by the increasing demand for minimally invasive surgical procedures and advanced wound care solutions. These adhesives are particularly effective for managing minor injuries, such as those resulting from minimally invasive procedures, skin grafts, and uncomplicated trauma-induced lacerations.

They are especially suited for non-bleeding wounds in stable areas of skin, which are not subjected to stretching. Compared to traditional sutures and staples, topical skin adhesives offer several advantages, including reduced infection risk, faster healing times, and less pain for patients. The rise in chronic wound cases, such as diabetic ulcers and pressure sores, further propels the market, as these conditions demand efficient and effective wound management solutions.

Technological advancements in adhesive formulations, including bioresorbable and antimicrobial options, are enhancing the efficacy and safety of these products, contributing to market expansion. Additionally, the global shift towards patient-centric care and the growing trend of outpatient surgeries are fueling the demand for user-friendly and versatile adhesive products.

These adhesives align with modern healthcare needs by simplifying the closure of wounds without the need for sutures, reducing recovery times, and providing quick, reliable solutions. However, the high cost of advanced adhesive technologies may pose challenges in cost-sensitive regions, potentially limiting their widespread adoption.

Key Takeaways

- The Topical Skin Adhesive market generated a revenue of US$ 729.30 Million and is predicted to reach US$ 1633.25 Million, with a CAGR of 8.2%.

- Based on the Product Type, the 2-Octyl Cyanoacrylate Adhesive segment generated the most revenue for the market with a market share of 51.3%.

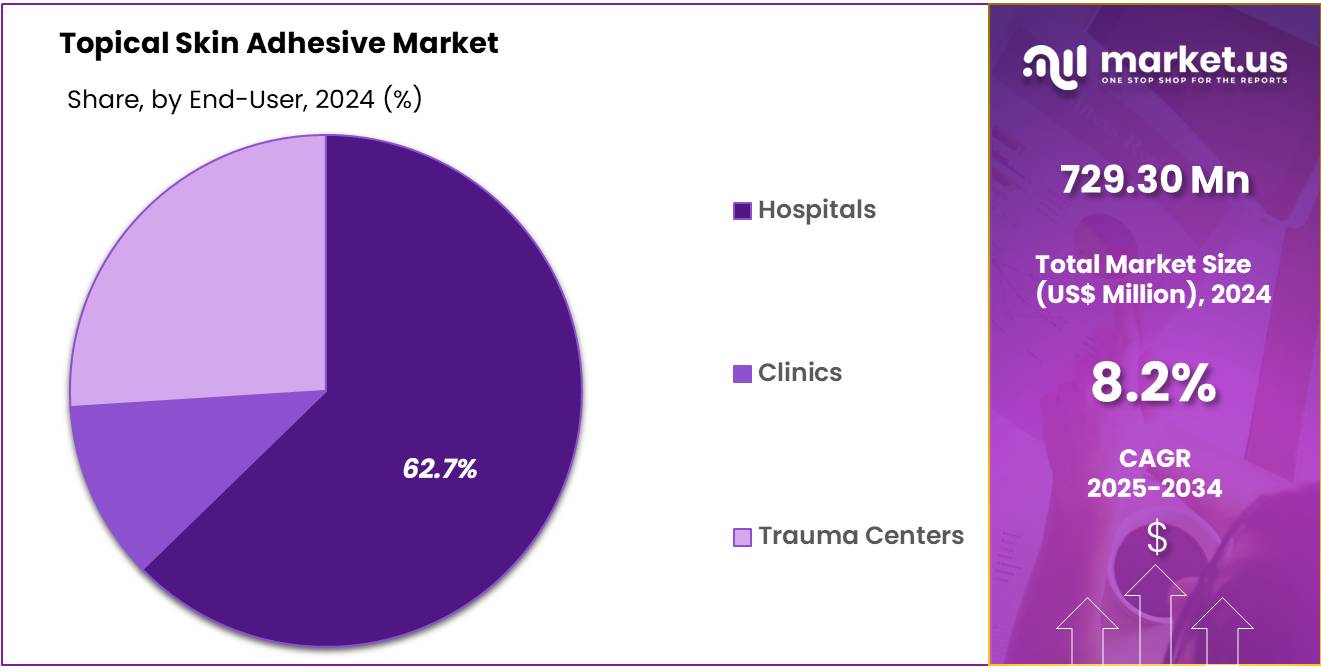

- Based on the End-User, the Hospitals segment generated the most revenue for the market with a market share of 62.7%.

- Based on the Application, the Surgical Incisions segment generated the most revenue for the market with a market share of 37.3%.

- Based on the Distribution Channel, the Offline segment generated the most revenue for the market with a market share of 79.8%.

- Region-wise, North America remained the lead contributor to the market, by claiming the highest market share, amounting to 42.20%.

Product Type Analysis

In 2023, N-2-Butyl-Cyanoacrylate Adhesive held a dominant position in the By Type segment of the Topical Skin Adhesive Market, accounting for over 51.3% of the market share. This strong market presence is driven by its superior adhesive properties, making it highly effective for wound closure, surgical incisions, and trauma care. Its versatility in various medical applications, including emergency medicine, dermatology, and surgical procedures, further contributes to its widespread adoption.

Compared to traditional sutures and staples, N-2-Butyl-Cyanoacrylate offers advantages such as faster healing times, reduced infection risks, and improved cosmetic outcomes, making it a preferred choice among healthcare professionals.

Additionally, its strong bonding capability and flexibility allow for better wound protection while minimizing patient discomfort. The adhesive’s widespread availability and cost-effectiveness have further strengthened its market dominance. As healthcare providers continue to seek efficient, non-invasive wound closure solutions, the demand for N-2-Butyl-Cyanoacrylate Adhesive is expected to remain high.

End-User Analysis

In the global Topical Skin Adhesive Market, hospitals dominated the end-user segment, driven by the high volume of surgical procedures, trauma cases, and emergency treatments requiring advanced wound closure solutions. Hospitals serve as primary healthcare centers for both minor and major surgeries, where topical skin adhesives are increasingly preferred over traditional sutures and staples due to their ease of application, reduced infection risk, and faster healing times.

The growing adoption of minimally invasive procedures and outpatient surgeries has further boosted the use of skin adhesives in hospital settings. Additionally, the rising number of accident-related injuries and emergency admissions contributes to increased demand for efficient wound closure methods. With the expansion of healthcare infrastructure, particularly in emerging markets, hospitals continue to play a crucial role in driving the adoption of topical skin adhesives. This trend is expected to sustain market growth as hospitals seek cost-effective and patient-friendly wound management solutions.

Application Analysis

In 2023, the surgical segment held a dominant position in the By Application category of the Topical Skin Adhesive Market, capturing over 37.3% of the market share. This strong market presence is driven by the extensive use of topical skin adhesives in various surgical procedures across hospitals, ambulatory surgical centers, and specialty clinics worldwide. Surgical applications cover a wide range of procedures, including wound closure, incision management, and surgical site protection, where skin adhesives are increasingly favored over traditional sutures and staples.

Their rapid bonding capabilities, ease of application, and ability to provide secure and flexible wound closure contribute to their growing adoption in operating rooms. Additionally, topical adhesives minimize scarring, reduce infection risks, and enhance patient comfort, making them an ideal choice for both minimally invasive and complex surgical interventions. As healthcare facilities continue to prioritize efficient, non-invasive wound closure techniques, the demand for topical skin adhesives in surgical applications is expected to remain strong.

Distribution Channel Analysis

The offline distribution channel dominated the Topical Skin Adhesive Market, driven by the strong presence of hospital pharmacies, retail pharmacies, and medical supply stores that provide direct access to healthcare professionals and end-users. Hospitals and surgical centers primarily procure topical skin adhesives through bulk purchasing agreements with distributors, ensuring a steady and reliable supply.

Additionally, offline channels offer personalized customer support, product demonstrations, and immediate availability, which are critical for healthcare providers when selecting medical adhesives. Retail pharmacies and specialty medical stores also play a significant role, catering to outpatient needs and minor wound care applications.

Despite the rise of e-commerce and digital sales platforms, offline distribution remains the preferred channel due to established supplier relationships, regulatory compliance, and product authenticity assurance. As hospitals and clinics continue to rely on traditional procurement methods, the offline segment is expected to maintain its dominance in the market.

Key Market Segments

Product Type

- 2-Octyl Cyanoacrylate Adhesive

- N-Butyl Cyanoacrylate Adhesive

- 2-Ethyl Cyanoacrylate Adhesive

End-User

- Hospitals

- Clinics

- Trauma Centers

Application

- Surgical Incisions

- Trauma-Induced Lacerations

- Burn and Skin Grafting

- Wound Closure

- Others

Distribution Channel

- Online

- Offline

Drivers

Growing Trauma and Accident Cases

The rising number of trauma and accident cases worldwide is a significant factor driving the growth of the Topical Skin Adhesive Market. Injuries from road accidents, workplace mishaps, sports activities, and household incidents often require immediate wound closure to prevent infections and promote faster healing. Topical skin adhesives are increasingly preferred over traditional sutures and staples due to their quick application, reduced scarring, and lower risk of infections.

According to the World Health Organization (WHO), road traffic accidents cause approximately 1.3 million deaths annually, while 20 to 50 million people suffer non-fatal injuries, many of which require medical intervention, including wound closure. Additionally, the American Association for the Surgery of Trauma (AAST) reports that trauma is the leading cause of death for individuals under the age of 45, emphasizing the urgent need for advanced wound management solutions.

Beyond road accidents, sports-related injuries also contribute to the increasing demand for topical skin adhesives. The Centers for Disease Control and Prevention (CDC) states that over 3.5 million sports injuries occur in the U.S. each year, requiring rapid and effective wound closure methods. Similarly, workplace injuries are another key concern. The International Labour Organization (ILO) estimates that nearly 374 million non-fatal work-related injuries occur globally each year, further driving the demand for efficient wound care products like skin adhesives.

In emergency settings, topical skin adhesives provide rapid wound closure, reducing patient discomfort and allowing for early discharge from healthcare facilities. As trauma and accident cases continue to rise globally, the adoption of topical skin adhesives is expected to grow, particularly in emergency care, trauma centers, and ambulatory surgical units, positioning the market for steady expansion in the coming years.

Restrains

High Cost of Advanced Adhesives

The high cost of advanced topical skin adhesives is a major restraint in the market, particularly affecting low- and middle-income regions where affordability is a concern. Unlike traditional sutures and staples, premium medical adhesives involve complex manufacturing processes, including the use of high-quality cyanoacrylates, advanced biocompatible materials, and strict regulatory compliance, which drive up costs.

For example, surgical-grade cyanoacrylate adhesives can cost $25–$50 per application, whereas traditional sutures cost significantly less, making them the preferred choice in cost-sensitive healthcare settings. Additionally, in many developing countries, healthcare budgets are constrained, and out-of-pocket expenses for wound closure products remain high. According to the World Bank, more than 800 million people worldwide spend at least 10% of their household budget on healthcare, limiting their access to premium-priced adhesives.

Moreover, insurance coverage for advanced wound closure products varies significantly, with many public healthcare systems not fully reimbursing the cost of medical adhesives. This further restricts their widespread adoption, especially in government hospitals and rural healthcare centers. Unless manufacturers develop cost-effective solutions or expand reimbursement policies, the high cost of advanced skin adhesives will continue to limit their penetration in price-sensitive markets, slowing overall market growth.

Opportunities

Increasing Adoption of Minimally Invasive Surgeries

Minimally invasive surgeries (MIS) are gaining popularity due to their advantages, including reduced scarring, faster recovery times, and lower risks of complications. This trend presents a significant opportunity for skin adhesives to replace traditional sutures and staples in wound closure. According to the World Health Organization (WHO), over 313 million surgical procedures are performed annually worldwide, with a growing percentage being minimally invasive.

Skin adhesives, such as cyanoacrylate-based formulations, offer several benefits, including faster application, reduced infection risks, and improved cosmetic outcomes. Studies indicate that skin adhesives can reduce wound closure time by up to 50% compared to sutures. The cosmetic surgery sector is also contributing to this shift.

The American Society of Plastic Surgeons (ASPS) reported that in 2022, over 26.2 million cosmetic procedures were performed, with a significant portion being minimally invasive. With patient demand for scar-free healing rising, skin adhesives are expected to play a crucial role in modern wound closure techniques, replacing traditional sutures in various surgical applications.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly impact global markets, influencing supply chains, investments, and healthcare accessibility. Economic downturns, inflation, and currency fluctuations can increase production costs, limit consumer spending, and reduce healthcare budgets. For example, the International Monetary Fund (IMF) reported that global inflation reached 8.8% in 2022, affecting healthcare expenditures.

Geopolitical tensions, such as trade restrictions and conflicts, disrupt medical supply chains. The Russia-Ukraine war, for instance, caused shortages of critical raw materials used in medical devices, impacting manufacturing. Similarly, U.S.-China trade tensions have led to increased tariffs on medical imports, raising costs.

Government policies, such as the Inflation Reduction Act in the U.S., influence pharmaceutical pricing and market dynamics. Additionally, fluctuating oil prices affect logistics and distribution costs. Businesses must navigate these uncertainties by diversifying supply chains and leveraging regional partnerships to mitigate risks and maintain operational stability.

Latest Trends

The global topical skin adhesive market is experiencing notable growth, driven by several key trends. Advancements in adhesive materials, such as biodegradable and eco-friendly options, are gaining prominence, offering improved sustainability and patient comfort. Additionally, the integration of skin adhesives with wearable medical technology is expanding, as these adhesives are crucial for securely attaching sensors and monitoring devices.

Customization is also on the rise, with manufacturers developing adhesives tailored to specific medical applications, such as wound care, cosmetic surgeries, and pediatric use. Another emerging trend is the shift towards using topical skin adhesives as non-invasive alternatives to sutures and staples for wound closure, as they reduce scarring and infection risks.

These trends highlight the growing demand for more efficient, personalized, and environmentally conscious solutions in the medical adhesive sector, contributing to the market’s steady expansion and the increasing adoption of skin adhesives across various healthcare applications.

Regional Analysis

North America Dominates the Global Topical Skin Adhesive Market

North America dominates the global topical skin adhesive market due to its advanced healthcare infrastructure, high adoption of innovative medical technologies, and the presence of key industry players. The region accounts for a significant market share of 42.20%, with the U.S. leading in demand for wound closure solutions. Major companies such as Johnson & Johnson (Ethicon) and Medtronic have a strong presence, driving innovation and expanding product offerings.

A key factor contributing to North America’s dominance is the increasing preference for minimally invasive procedures, where topical skin adhesives are widely used as an alternative to sutures and staples. Additionally, the region has a high volume of surgical procedures, including cosmetic and trauma surgeries, which boosts the demand for skin adhesives.

Regulatory support from agencies like the FDA ensures the availability of high-quality and safe products, further fostering market growth. The rising prevalence of chronic wounds, particularly among the aging population and diabetic patients, also fuels market expansion. Moreover, growing awareness among healthcare professionals and patients about the benefits of topical skin adhesives, such as reduced infection risk and faster healing, strengthens market penetration.

With continuous technological advancements and increasing healthcare expenditures, North America is expected to maintain its leadership in the global topical skin adhesive market.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The global topical skin adhesive market is characterized by a competitive landscape dominated by several key players. Johnson & Johnson (Ethicon) holds a significant market share of approximately 45%, leading the industry. Other major companies include Medtronic, Advanced Medical Solutions, Medline, B. Braun (Aesculap), Chemence Medical, and Adhezion Biomedical. Collectively, these top seven players account for about 80% of the market share.

The competitive dynamics are influenced by factors such as product innovation, strategic partnerships, and regional market expansion. Companies are focusing on developing advanced adhesives with improved properties to meet the evolving needs of healthcare providers and patients. The presence of established players and the high market concentration contribute to a competitive environment, with ongoing efforts to enhance product offerings and expand market reach.

Top Key Players

- Adhezion Biomedical, LLC

- Glustich Inc.

- Healthium Medtech Pvt. Ltd.

- Meril Life Sciences Pvt. Ltd.

- Surgitech Innovation

- Epiglue Pharma Pvt. Ltd.

- Braun

- Johnson & Johnson

- Medline

- Advanced Medical Solutions Group Plc

- Chemence Medical, Inc.

Recent Developments

- In November 2023, DuPont partnered with STMicroelectronics to create the Liveo™ Smart Biosensing Patch, a wearable device designed for remote biosignal monitoring, which enhances patient comfort and performance. Unveiled at the MEDICA Trade Fair, the patch features multifunctional sensors aimed at improving cardiac monitoring.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 729.30 Million |

| Forecast Revenue (2034) | US$ 1633.25 Million |

| CAGR (2025-2034) | 8.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2019-2024 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | Product Type- 2-Octyl Cyanoacrylate Adhesive, N-Butyl Cyanoacrylate Adhesive and 2-Ethyl Cyanoacrylate Adhesive, End-User-Hospitals, Clinics, Trauma Centers, Application- Surgical Incisions, Trauma-Induced Lacerations, Burn and Skin Grafting, Wound Closure and Others and Distribution Channel- Online and Offline |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Adhezion Biomedical, LLC, Glustich Inc., Healthium Medtech Pvt. Ltd., Meril Life Sciences Pvt. Ltd., Surgitech Innovation, Epiglue Pharma Pvt. Ltd., B. Braun, Johnson & Johnson, Medline, Advanced Medical Solutions Group Plc and Chemence Medical, Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |