Quick Navigation

- Report Overview

- Key Takeaways

- Product Type Analysis

- End User Analysis

- Measurement Type Analysis

- Distribution Channel Analysis

- Fabric Type Analysis

- Price Range Analysis

- Key Market Segments

- Regional Analysis

- Key Regions and Countries

- Market Dynamics

- Drivers

- Restraints

- Challenges

- Opportunities

- Key Company Insights

- Recent Developments

- Report Scope

Report Overview

Global Custom Made Clothes Market size is expected to be worth around USD 156.4 Billion by 2035 from USD 57.1 Billion in 2025, growing at a CAGR of 10.6% during the forecast period 2026 to 2035. This trajectory places bespoke apparel among the fastest-expanding segments within the broader global fashion industry.

The custom-made clothes market encompasses garments produced to individual measurements, covering suits, shirts, trousers, dresses, jackets, and outerwear. Businesses in this market operate across in-store tailoring boutiques, digital platforms, and hybrid measurement models. The market serves men and women across mid-range, premium, and luxury price tiers, distributing through both offline and online channels.

Key Takeaways

- Market size in 2025 stands at USD 57.1 Billion, reaching USD 156.4 Billion by 2035.

- The market grows at a CAGR of 10.6% from 2026 to 2035.

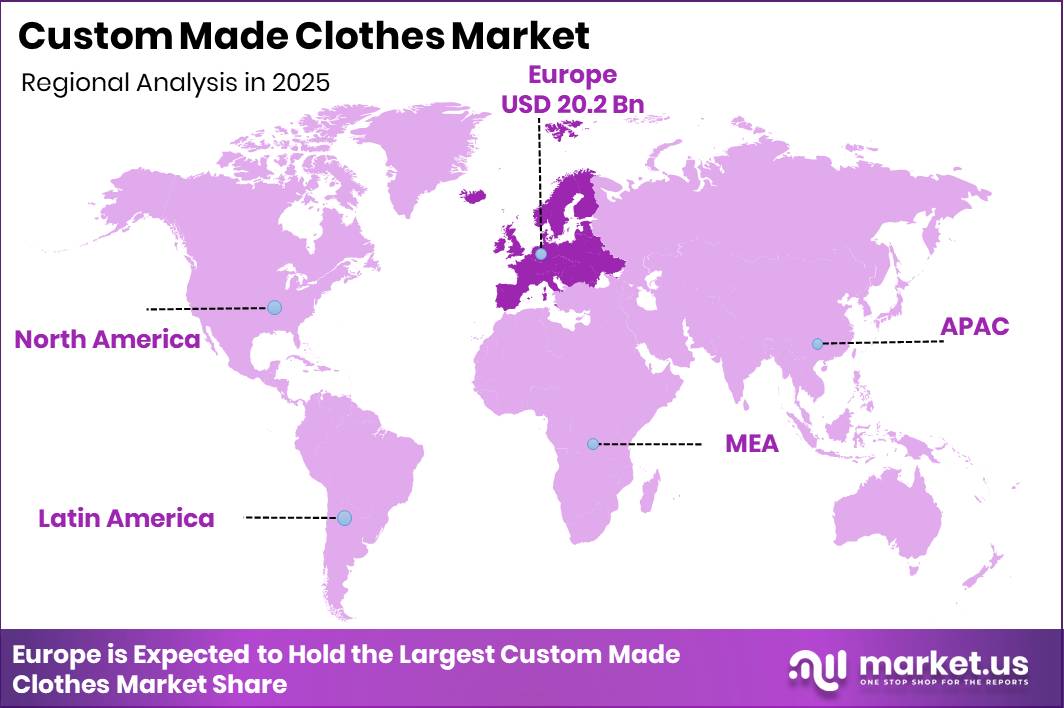

- Europe dominates with a 35.40% regional share, valued at USD 20.2 Billion in 2025.

- Suits and Blazers lead the Product Type segment with a 36.80% share.

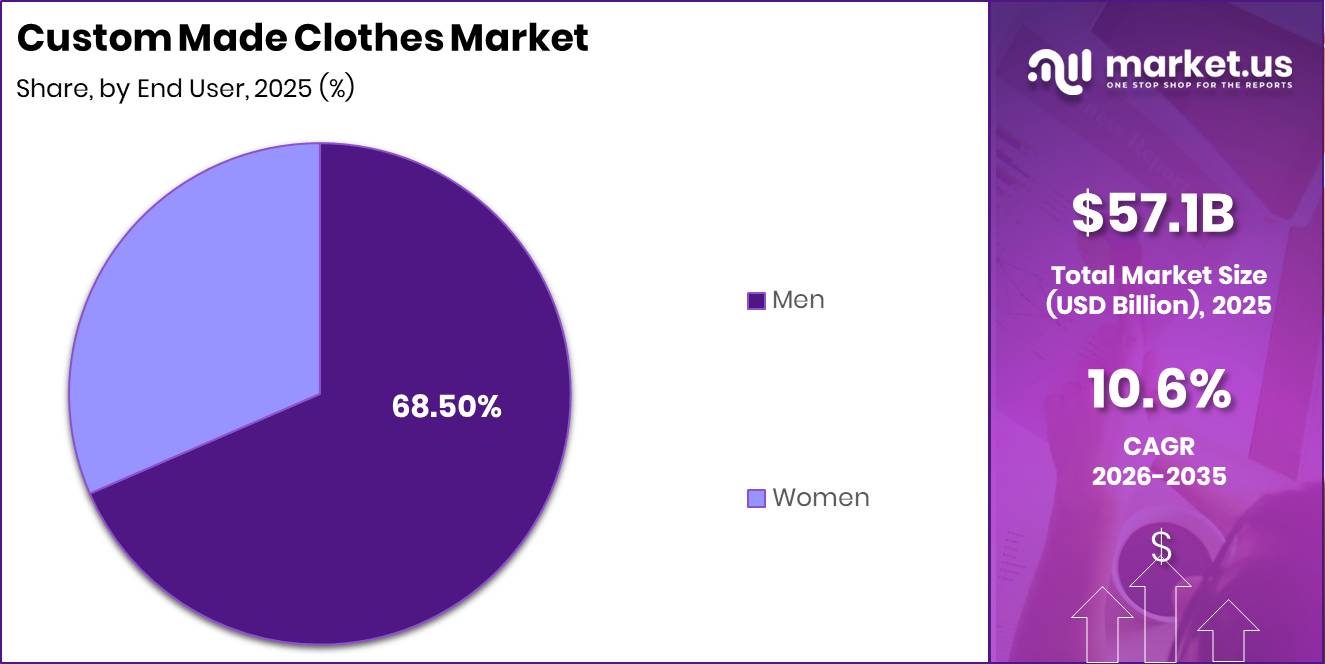

- Men dominate the End User segment with a 68.50% share.

- In-Store Measurement leads the Measurement Type segment with a 57.40% share.

- Offline Stores and Tailoring Boutiques lead Distribution Channel with a 62.30% share.

- Cotton leads the Fabric Type segment with a 34.20% share.

- Mid-Range leads the Price Range segment with a 46.90% share.

- Asia-Pacific is the fastest-growing region across the forecast period.

As per our research, 36% of consumers cite inconsistent sizing as a reason for avoiding apparel brand purchases. This behavioral gap creates a structural opening for custom-made clothing operators who deliver garment-level fit certainty. Brands that position precision fit as a core product promise stand to convert sizing-frustrated mainstream shoppers into loyal bespoke customers.

Sustainability compliance is reshaping supply chain economics across the custom apparel sector. Coats reported a 30% reduction in Scope 1 and Scope 2 emissions in its 2025 Sustainability Report, with certified renewable electricity and solar covering more than 60% of global electricity consumption. Custom garment producers whose suppliers meet these benchmarks will face lower compliance friction as environmental standards tighten globally.

As per our research, over 10,000 U.S. consumers were body-scanned in the Size USA apparel sizing study, producing one of the largest made-to-measure fit databases in apparel history. This data infrastructure reduces pattern development guesswork for custom producers. Businesses that license or build on verified anthropometric databases will deliver more consistent fit outcomes and reduce costly alteration cycles.

Product Type Analysis

Suits & Blazers dominates with 36.80% due to high male professional dress demand.

In 2025, Suits and Blazers held a dominant market position in the By Product Type segment of the Custom Made Clothes Market, with a 36.80% share. This leadership reflects deep consumer preference for structured formalwear that delivers consistent fit and professional presentation. Brands that prioritize suiting customization capture the highest average order values within the product range.

Shirts represent the next tier in custom clothing demand, driven by everyday professional wear requirements and strong online self-measurement adoption. Their repeat-purchase nature creates high customer lifetime value for brands offering stored measurement profiles. Operators who pair shirt customization with digital body profiles can reduce ordering friction and build recurring revenue streams.

Trousers occupy a complementary role to suiting in the custom apparel mix, frequently ordered alongside jackets as part of coordinated formal outfits. This bundling behavior supports higher average transaction values per customer visit. Retailers who offer suit-and-trouser coordination tools within their digital ordering platforms can increase attachment rates and reduce cart abandonment.

Dresses and Skirts are the fastest-growing sub-segment within Product Type, reflecting rising female engagement with bespoke occasion wear. Jackets and Outerwear and Others collectively hold the remaining share, covering casual and functional custom categories. These segments signal expanding category boundaries for custom apparel beyond traditional tailoring.

End User Analysis

Men dominates with 68.50% due to established formal tailoring tradition.

In 2025, Men held a dominant market position in the By End User segment of the Custom Made Clothes Market, with a 68.50% share. This dominance reflects decades of established bespoke suiting culture, particularly in professional and corporate dress environments. Operators serving male clients benefit from well-defined product categories and stronger repeat-purchase cycles tied to professional wardrobe renewal.

Women represent the fastest-growing end user segment, driven by rising demand for custom occasionwear and a broader shift toward individualized fashion. As per our research, 67% of consumers are more likely to purchase from brands featuring diverse body types in marketing. Custom apparel businesses that showcase inclusive sizing across female product lines will convert broader audiences and accelerate share gains in this segment.

Measurement Type Analysis

In-Store Measurement dominates with 57.40% due to customer preference for tactile fit verification.

In 2025, In-Store Measurement held a dominant market position in the By Measurement Type segment of the Custom Made Clothes Market, with a 57.40% share. Customers continue to prefer direct interaction with tailors for high-value garments, where fit accuracy carries significant financial and social weight. Tailoring businesses that maintain skilled in-store measurement staff protect premium margin positioning while reinforcing service quality perceptions.

Online Self-Measurement is growing as digital fit tools mature, but accuracy constraints remain a structural barrier. A 2025 body-digitization study found that smartphone-based measurement systems can exhibit deviations of approximately 20 to 30 millimeters versus benchmark anthropometric data. As per our research, size and fit issues drive clothing returns across 14 countries, confirming that measurement accuracy directly determines commercial outcomes for online custom apparel operators.

3D Body Scanning is the fastest-growing measurement method, offering the highest technical precision of all three approaches. Retail locations and specialist scanning studios that deploy 3D systems position themselves at the highest accuracy tier in the measurement market. Early investment in scanning infrastructure creates a defensible service advantage as consumer awareness of the technology increases.

Distribution Channel Analysis

Offline Stores & Tailoring Boutiques dominates with 62.30% due to trust-driven high-value transaction preference.

In 2025, Offline Stores and Tailoring Boutiques held a dominant market position in the By Distribution Channel segment of the Custom Made Clothes Market, with a 62.30% share. In-person environments enable clients to evaluate fabrics, discuss construction details, and verify fit in ways digital channels cannot yet replicate. Operators with established boutique networks hold a structural trust advantage that supports premium pricing and long-term client retention.

Online Platforms are the fastest-growing distribution channel, supported by wider consumer comfort with digital commerce and improved measurement tools. Data from the Adyen Retail Report shows that more than one-third of consumers across 28 countries reported using AI while shopping in 2025, representing a 47% year-over-year increase from 2024. The Adyen Retail Report also found that 57% of Gen Z consumers used AI for shopping, including personalized apparel recommendations, signaling a generational shift that custom online platforms must address to capture future growth.

Fabric Type Analysis

Cotton dominates with 34.20% due to versatility, breathability, and broad price accessibility.

In 2025, Cotton held a dominant market position in the By Fabric Type segment of the Custom Made Clothes Market, with a 34.20% share. Cotton’s adaptability across product categories from formal shirts to casual outerwear makes it the default choice for both entry-level and mid-range custom garments. Brands offering certified organic cotton options gain competitive differentiation as sustainability requirements tighten across key markets.

Wool occupies a critical position in the premium and luxury suiting categories, commanding the highest price per meter among commonly used tailoring fabrics. As per our research, 80% of consumers believe fashion brands should hold sustainability certifications when producing apparel. Wool suppliers with traceable provenance and sustainability credentials will see stronger demand from custom tailors competing in the premium segment.

Polyester Blends serve the mid-range and performance-oriented custom garment tier, balancing cost efficiency with durability and wrinkle resistance. Linen is the fastest-growing fabric type, reflecting seasonal and lifestyle casualwear trends in warmer markets. Silk and Others together account for the remaining share, concentrated in luxury occasionwear and specialist custom applications.

Price Range Analysis

Mid-Range dominates with 46.90% due to broad consumer accessibility and professional wardrobe demand.

In 2025, Mid-Range held a dominant market position in the By Price Range segment of the Custom Made Clothes Market, with a 46.90% share. This tier attracts professional consumers who require fit precision and fabric quality without reaching luxury price points. Operators in the mid-range benefit from higher order volumes and more frequent repeat purchases than their luxury counterparts.

Premium represents the second-largest price tier, serving clients who prioritize superior fabric sourcing, construction detail, and brand heritage. As per our research, 72% of consumers consider ethical certifications important when purchasing clothing. Premium custom brands that communicate material sourcing standards and ethical production practices will strengthen purchase intent among this value-conscious but quality-driven consumer group.

Luxury is the fastest-growing price segment, driven by wealth concentration in established tailoring markets and expanding affluent consumer bases in Asia-Pacific. This segment commands the highest margins but requires the deepest craft expertise and material investment. New entrants targeting luxury must demonstrate both design authority and supply chain credibility to compete with heritage houses.

Key Market Segments

By Product Type

- Suits and Blazers

- Shirts

- Trousers

- Dresses and Skirts

- Jackets and Outerwear

- Others

By End User

- Men

- Women

By Measurement Type

- In-Store Measurement

- Online Self-Measurement

- 3D Body Scanning

By Distribution Channel

- Offline Stores and Tailoring Boutiques

- Online Platforms

By Fabric Type

- Cotton

- Wool

- Polyester Blends

- Linen

- Silk

- Others

By Price Range

- Mid-Range

- Premium

- Luxury

Regional Analysis

Europe Dominates the Custom Made Clothes Market with a Market Share of 35.40%, Valued at USD 20.2 Billion

Europe holds the largest share of the global custom-made clothes market, anchored by centuries-old tailoring traditions in the UK, Italy, and France. High disposable incomes, strong corporate dress culture, and deep consumer appreciation for craft-quality garments sustain premium demand. Regulatory frameworks around textile traceability are also accelerating adoption of digitally traceable bespoke production across EU member states.

North America represents the second-largest regional market, driven by strong corporate professional wear demand and growing consumer interest in personalized fashion alternatives to mass-market retail. The U.S. hosts the largest concentration of digital-first custom apparel platforms globally. Brands that combine digital fit-capture technology with fast domestic fulfillment are best positioned to capture share from dissatisfied mass-market shoppers in this region.

Asia-Pacific is the fastest-growing region in the custom-made clothes market, supported by expanding middle-class wealth, rising fashion consciousness, and a deep regional base of skilled garment manufacturing. In December 2025, KNOT raised USD 5 million in funding to scale its fashion-commerce platform and expand its 60-minute fashion delivery network across India. This investment reflects rising investor confidence in rapid-turnaround custom apparel models across the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Market Dynamics

Market Opportunity Analysis - Underexploited end-user, regional, and price segments offer targeted entry points for focused custom apparel operators

The Women end-user segment remains underexploited relative to its growth trajectory, holding a minority share despite being the fastest-growing end-user group. Custom brands have historically structured product lines and measurement systems around male suiting norms, creating a structural service gap for female customers. Operators who develop female-specific fit methodologies and product ranges can capture disproportionate share as this segment accelerates.

Asia-Pacific is the fastest-growing region yet remains structurally underserved by established bespoke brands, most of which are headquartered in Europe or North America. Regional manufacturing depth in countries like India and China gives local operators a cost-and-proximity advantage in serving domestic custom demand. New entrants who build locally relevant digital ordering platforms backed by regional production networks can establish first-mover positions before global brands scale their presence.

The Luxury price segment is the fastest-growing price tier but commands the smallest absolute share within the Price Range breakdown. This gap reflects high entry barriers rather than limited consumer appetite. Investors who fund craft-credentialed bespoke brands with verified sourcing transparency stand to capture compounding margin growth as affluent consumers in Asia-Pacific and the Middle East increase bespoke spending.

3D Body Scanning is the fastest-growing measurement method but holds the smallest current share within the Measurement Type segment, indicating early-stage adoption with significant penetration headroom. Retail operators who deploy scanning infrastructure ahead of market normalization will build proprietary customer measurement databases that increase switching costs and drive repeat purchase frequency. This creates a winner-takes-more dynamic in digital measurement capability within the custom clothing market.

Technology and Innovation Landscape - Digital measurement, AI personalization, and sustainable supply chain technology define the next competitive frontier in custom apparel

Smartphone-based body-measurement systems are expanding access to remote custom ordering but carry documented technical limitations. A 2025 body-digitization study found that these systems can produce measurement deviations of 20 to 30 millimeters versus benchmark data. Operators who layer AI correction algorithms over raw smartphone inputs can reduce these errors and improve remote garment fit outcomes at scale.

3D body scanning represents the highest-precision measurement technology available to custom apparel operators today. Scanning stations capture complete body geometry in seconds, eliminating manual measurement variability and supporting automated pattern generation. Brands that integrate 3D scan data with digital pattern libraries reduce the skilled-labor dependency that currently constrains production scaling across the industry.

Generative AI is entering custom apparel workflows at the executive and operational levels simultaneously. As per our research, 35% of fashion executives reported using generative AI for customer service, product discovery, and personalization workflows in 2025. Brands that deploy AI-driven styling recommendation engines alongside their custom ordering platforms convert browsing behavior into higher-confidence purchase decisions, reducing drop-off at the product configuration stage.

Sustainable supply chain technology is reshaping input sourcing for custom apparel producers. Coats reported that certified renewable electricity and solar generation covered more than 60% of global electricity consumption in its 2025 operations. Suppliers who achieve and certify these benchmarks become preferred partners for custom brands competing in EU and UK markets where environmental compliance is increasingly a commercial prerequisite.

Drivers

Digital fit-capture adoption reduces reliance on in-person measurements and enables scalable remote ordering for custom apparel businesses. Stored digital body profiles link precise dimensions directly to pattern creation, improving fit consistency across repeat purchases. This operational shift shortens order cycles, reduces alteration requirements, and allows custom clothing brands to reach customers beyond their immediate geographic markets.

The result is higher customer retention and broader market scalability. Brands that deploy fit-capture tools lower their per-order service costs and build proprietary customer data assets that competitors without measurement infrastructure cannot easily replicate. This technology advantage compounds over time as stored profiles drive faster, more convenient repeat purchase behavior.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Textile traceability compliance push | +1.7% | EU; UK; export-oriented Asia | Medium term (2-4 years) |

| Standardized body-measurement systems | +1.5% | North America; EU; East Asia | Medium term (2-4 years) |

| Digital fit-capture adoption | +2.0% | North America core; East Asia; online apparel corridors | Short term (≤ 2 years) |

| Low-inventory production economics | +1.8% | U.S.; EU; Turkey; Mexico; Portugal | Short term (≤ 2 years) |

| Premium occasionwear demand | +1.4% | India; Middle East; UK; diaspora fashion hubs | Short term (≤ 2 years) |

| Circularity-compatible garment design | +1.3% | EU; Japan; North America premium retail | Long term (≥ 4 years) |

Restraints

Import-cost and sourcing pressure directly restrict custom apparel operators because premium tailoring businesses depend heavily on imported textiles and garment components. According to the U.S. Bureau of Labor Statistics, the U.S. import price index for apparel manufacturing inputs remained active through May 2026, confirming continued exposure to global cost fluctuations. Custom producers purchase fabrics in small batches, limiting their ability to negotiate pricing or absorb cost increases.

Unlike mass-market brands, bespoke operators cannot rapidly switch suppliers because fabric consistency is critical to garment quality and customer expectations. This inflexibility narrows affordability, delays new collections, and pushes operators toward higher-margin orders rather than broadening their customer base. Businesses that build flexible dual-sourcing agreements will manage this constraint more effectively than those relying on single-origin supply chains.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU traceability compliance burden | -1.3% | EU; UK; export-focused Asia | Medium term (2-4 years) |

| Premium price-access ceiling | -1.2% | North America; EU; middle-income urban markets | Short term (≤ 2 years) |

| Limited scalable skilled capacity | -1.0% | India; China; Italy; UK; U.S. | Long term (≥ 4 years) |

| Weak digital interoperability | -0.9% | Global online custom apparel corridors | Medium term (2-4 years) |

| Import-cost and sourcing pressure | -0.8% | U.S.; EU; nearshore supply routes | Short term (≤ 2 years) |

| Small-batch production overhead | -1.1% | Global custom ateliers and microfactories | Medium term (2-4 years) |

Challenges

Digital fit-capture adoption is accelerating growth in the custom-made clothing market by reducing dependence on traditional manual measurements. Stored digital body profiles allow customers to order remotely while maintaining consistent measurement accuracy across all future purchases. For apparel makers, fewer in-person consultations and lower alteration volumes improve operational efficiency and reduce per-order service costs.

Verified customer measurement records strengthen retention by making repeat purchases faster and more convenient. Brands that connect individual body dimensions directly to pattern development gain scalability advantages that traditional tailoring businesses cannot match. This creates a two-tier market where digitally enabled operators can serve larger customer bases without proportionally expanding physical tailoring capacity.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Complex textile DPP data demands | -1.2% | EU; UK; export-focused producers | Medium term (2-4 years) |

| Measurement and sizing variability | -1.1% | North America; EU; Asia apparel hubs | Long term (≥ 4 years) |

| Skilled tailoring labour constraints | -1.0% | India; China; EU; North America | Long term (≥ 4 years) |

| Factory-level productivity dispersion | -0.9% | Global cut-and-sew and custom units | Medium term (2-4 years) |

| Fragmented digital fit infrastructure | -1.0% | Online apparel corridors; emerging brands | Medium term (2-4 years) |

| Capital-light microfactory scaling gaps | -0.8% | U.S.; EU; nearshore textile regions | Long term (≥ 4 years) |

Opportunities

DPP-ready bespoke traceability is becoming a major opportunity as the European Union advances Digital Product Passport requirements under the Ecodesign for Sustainable Products Regulation. Textile-specific rules are expected around 2027, creating strong incentives for bespoke brands to establish product-level traceability systems ahead of implementation. QR-based garment records can store fiber composition, manufacturing location, repair history, and care instructions across the garment’s lifetime.

Bespoke apparel businesses are particularly well positioned for early DPP adoption because lower production volumes and higher garment prices make digital tracking economically feasible. Early adopters can transform regulatory readiness into a premium customer service advantage, supporting product authentication, resale transactions, and circularity initiatives. This converts a compliance obligation into a commercial differentiator that strengthens long-term client relationships and brand transparency.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| DPP-ready bespoke traceability | +2.1% | EU; UK; premium export hubs in Asia | Medium term (2-4 years) |

| Scan-to-pattern fit platforms | +2.4% | North America core; EU; East Asia digital retail | Short term (≤ 2 years) |

| Resale-linked custom wardrobes | +1.6% | EU; U.S.; Japan; premium circular-fashion markets | Long term (≥ 4 years) |

| Custom uniform subscriptions | +1.9% | North America; GCC; hospitality and healthcare hubs | Medium term (2-4 years) |

| Digital occasionwear studios | +1.8% | India; Middle East; UK; North America diaspora markets | Short term (≤ 2 years) |

| Microfactory nearshoring networks | +2.2% | U.S.; EU; Turkey; Portugal; Mexico | Long term (≥ 4 years) |

Key Company Insights

Indochino holds a structural advantage in the mid-market custom suiting segment through its network of showrooms combined with a digital measurement platform. This omnichannel model bridges in-person fit consultation with online order management. As per our research, 35% of fashion executives already deploy generative AI for personalization workflows, and Indochino’s data infrastructure positions it to adopt these tools faster than smaller boutique competitors.

Hockerty operates as a digital-native custom clothing brand serving European and North American consumers through an online-only model. As per our research, 82% of consumers consider free returns an important factor in online apparel purchasing, which creates ongoing conversion pressure for digital-only custom operators. In June 2025, Alta raised USD 11 million in seed funding for AI-powered virtual try-on and personalized styling, signaling the competitive direction that platforms like Hockerty must match to retain market share.

Key Players

- Indochino

- Hockerty

- Black Lapel

- Proper Cloth

- Lanieri

- Sumissura

- Tailor Store

- Apposta

- Scabal

- Ermenegildo Zegna

- Huntsman Savile Row

- Raja Fashions

- A Suit That Fits

- MyTailor

- Cad and The Dandy

Recent Developments

- June 2025 – Tailor raised USD 22 million in a Series A funding round to expand its composable ERP platform for retail, e-commerce, and apparel businesses, with backing from NEA, Y Combinator, ANRI, and JIC Venture Growth Investments.

- November 2025 – Tailor completed the final close of its Series A financing, bringing total funding to USD 37 million, with capital earmarked for product development, U.S. expansion, and enhanced retail and fashion-industry implementations.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 57.1 Billion |

| Forecast Revenue (2035) | USD 156.4 Billion |

| CAGR (2026-2035) | 10.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Suits and Blazers, Shirts, Trousers, Dresses and Skirts, Jackets and Outerwear, Others); By End User (Men, Women); By Measurement Type (In-Store Measurement, Online Self-Measurement, 3D Body Scanning); By Distribution Channel (Offline Stores and Tailoring Boutiques, Online Platforms); By Fabric Type (Cotton, Wool, Polyester Blends, Linen, Silk, Others); By Price Range (Mid-Range, Premium, Luxury) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Indochino, Hockerty, Black Lapel, Proper Cloth, Lanieri, Sumissura, Tailor Store, Apposta, Scabal, Ermenegildo Zegna, Huntsman Savile Row, Raja Fashions, A Suit That Fits, MyTailor, Cad and The Dandy |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |