Quick Navigation

Report Overview

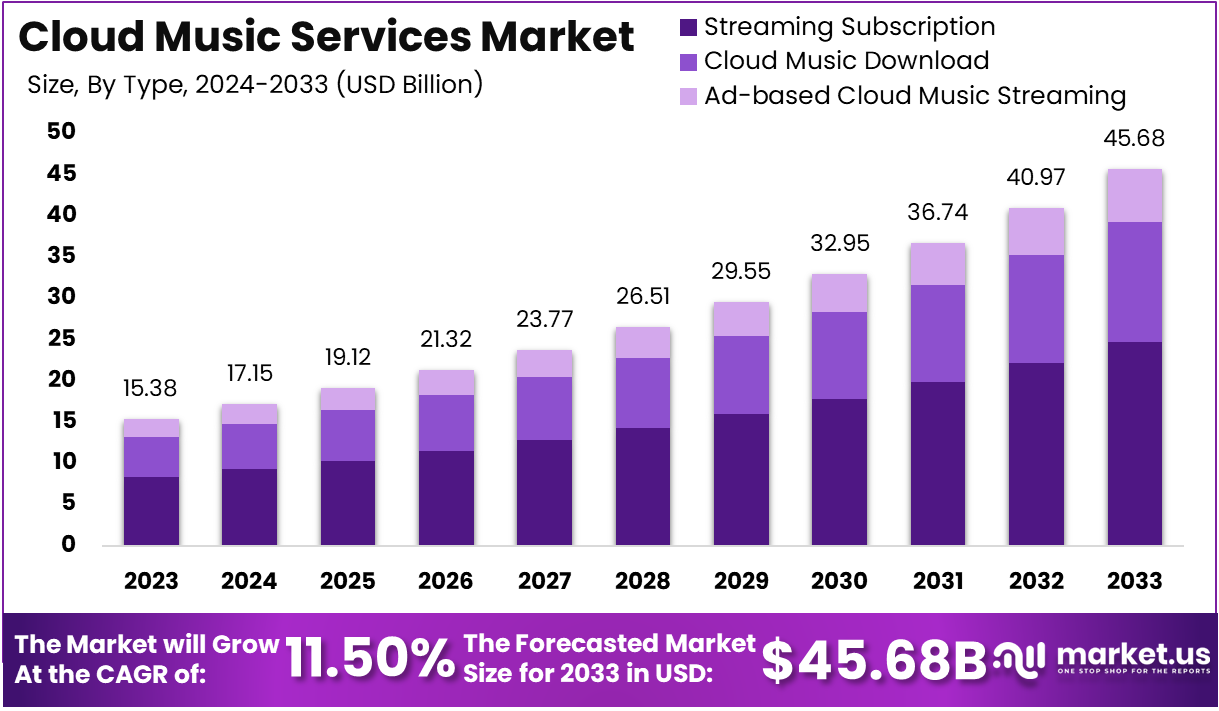

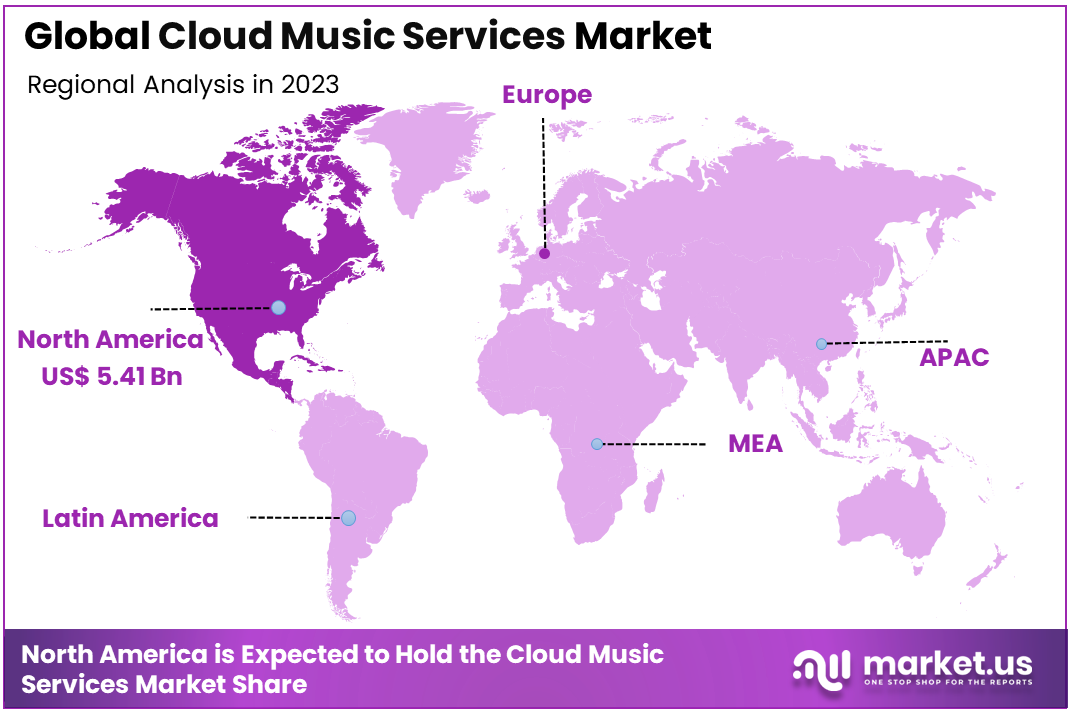

The Global Cloud Music Services Market size is expected to be worth around USD 45.68 Billion By 2033, from USD 15.38 Billion in 2023, growing at a CAGR of 11.50% during the forecast period from 2024 to 2033. In 2023, North America held a dominant market position, capturing more than a 35.3% share, holding USD 5.41 Billion in revenue.

Cloud music services refer to platforms that allow users to store, stream, and share music through the internet, leveraging cloud-based technology. Instead of downloading music onto devices, users can access vast libraries of songs via the cloud, offering them a more flexible and seamless music experience. Popular cloud music services include platforms like Spotify, Apple Music, Amazon Music, and Google Play Music.

These services enable users to stream music on-demand, create personalized playlists, and share songs across multiple devices. The Cloud technology ensures that users can access their music collection from any device, without the need for physical storage, making it highly convenient and user-friendly.

The cloud music services market has grown rapidly over the last decade, driven by advancements in internet speeds, widespread smartphone adoption, and increased consumer demand for convenient and on-the-go music consumption. This market is characterized by a shift away from traditional methods of purchasing and downloading music towards streaming services, which offer vast libraries accessible at the click of a button.

Consumers are also increasingly looking for personalized music experiences, with features like algorithm-based playlists and curated recommendations, which has further boosted the market. The global cloud music services market is expected to grow significantly in the coming years, as more people shift toward subscription-based services and away from physical media.

The demand for cloud music services is growing steadily as consumers opt for subscription models that offer ad-free listening and access to extensive music libraries. According to recent reports, the demand for premium subscription-based services is particularly high, as consumers are willing to pay for enhanced listening experiences and exclusive content.

This trend is not only seen in developed markets but also in emerging economies where disposable income is rising, and mobile internet usage is expanding. Additionally, there is an increasing demand for cloud music services among businesses and content creators who seek to integrate music into their work environments or projects, further driving market expansion.

Cloud music services are increasingly tapping into new market opportunities, particularly by diversifying their offerings beyond just music. For example, services like Spotify and Apple Music have expanded into podcasts, exclusive live concerts, and even video content. This diversification provides additional revenue streams and allows platforms to appeal to a broader audience.

Another significant opportunity lies in emerging markets where internet access is expanding, and mobile devices are becoming more affordable. As these regions continue to develop, they present an untapped potential for cloud music services to expand their subscriber base. Partnerships with other industries, such as automotive and smart home devices, also provide opportunities for further integration of music services into everyday life.

Technological advancements are playing a crucial role in the growth of cloud music services. The rise of artificial intelligence (AI) and machine learning has allowed music platforms to enhance their recommendation algorithms, offering users a more personalized music experience. These technologies analyze user behavior to suggest songs, albums, or playlists based on preferences, boosting user engagement.

Additionally, improvements in cloud infrastructure, such as better data storage and faster streaming capabilities, have enabled smoother, higher-quality music streaming. Integration with smart home devices, wearables, and in-car entertainment systems is another trend that showcases how advancements in technology are enhancing the accessibility and usability of cloud music services.

Furthermore, innovations in audio compression techniques are improving streaming efficiency, which reduces data consumption and allows users to access high-quality music even in areas with limited bandwidth.

Mobile phone penetration is notably high, with over 110 mobile phones per 100 people in the United States. Major players like Spotify and Apple Music dominate the market, accounting for around 80% of subscription streaming among U.S. users, which translates to approximately 50 million subscribers for Spotify and about 88 million subscribers for Apple Music as of late 2023.

The market is segmented into various types, including downloadable services, subscription-based models, and streaming services, catering to both individual and business users across mobile and web platforms.

Furthermore, the integration of advanced technologies such as artificial intelligence (AI) and personalized content delivery is expected to enhance user engagement significantly. For example, AI-driven recommendations can increase user listening time by as much as 30%, indicating a strong potential for growth in user retention and satisfaction in the cloud music services landscape.

Key Takeaways

- Market Growth: The cloud music services market is projected to expand from USD 15.38 billion in 2023 to USD 45.68 billion by 2033, reflecting a robust CAGR of 11.50% during the forecast period.

- Dominant Type: The streaming subscription segment holds the largest share at 54% in 2023, driven by the increasing preference for subscription-based models that offer unlimited access to music libraries.

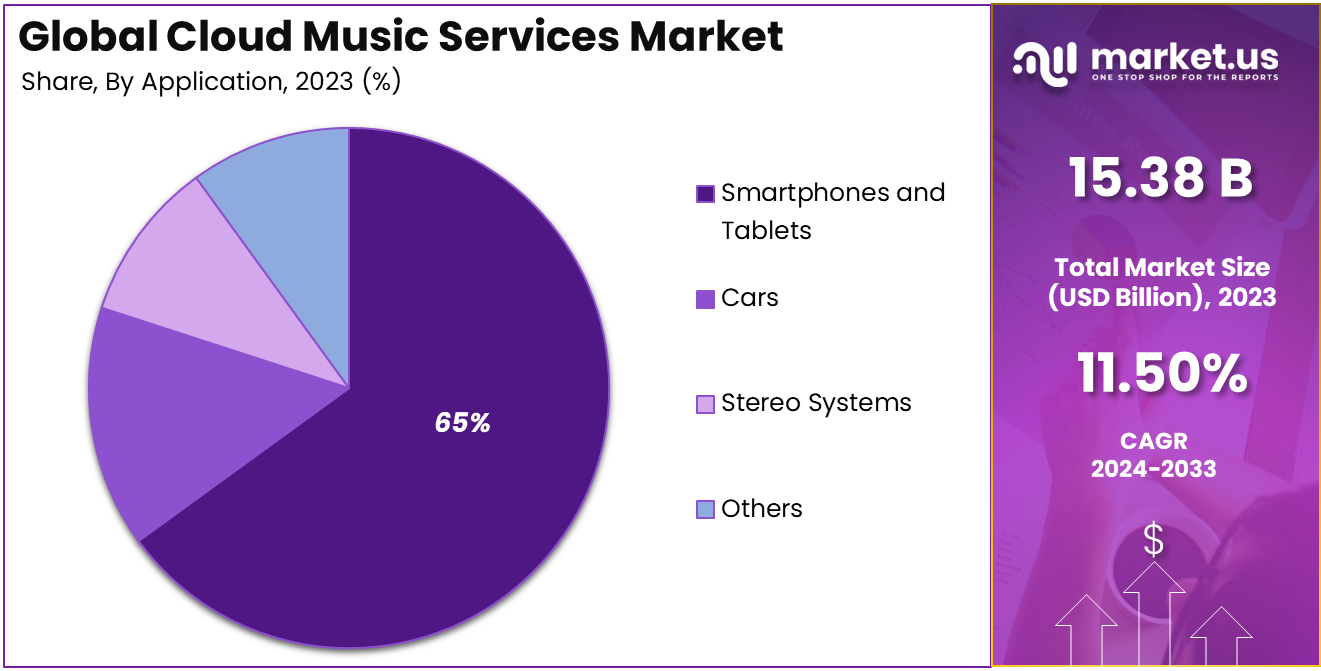

- Leading Application: The smartphones and tablets segment dominates with a 65% share, as mobile devices continue to be the preferred platform for accessing music on the go.

- End-User Dominance: The individual use segment captures 81% of the market, highlighting the growing trend of personal music consumption through cloud services.

- Regional Leadership: North America holds the largest market share at 35.3% in 2023, fueled by high internet penetration, widespread smartphone usage, and the presence of major cloud music service providers in the region.

By Type

In 2023, the Streaming Subscription segment held a dominant market position, capturing more than a 54% share of the Cloud Music Services market. This growth can be attributed to the increasing shift in consumer preferences towards subscription-based services like Spotify, Apple Music, and Amazon Music, which offer users unlimited access to an extensive library of music for a fixed monthly fee.

The convenience of on-demand music streaming, without the need for individual purchases or downloads, has significantly contributed to the rapid growth of this segment. The rise of streaming subscriptions is closely linked to the improvement in internet connectivity and the proliferation of smartphones and smart devices.

With faster internet speeds and mobile platforms, users can seamlessly stream high-quality music at their convenience, which has made paid streaming services more attractive. Additionally, the availability of offline listening features in many subscription services has further increased their appeal, especially for users in regions with inconsistent internet access.

Moreover, the business models adopted by streaming platforms, such as offering tiered pricing for individual users, families, and students, have also enhanced their accessibility, making them more appealing to a broader consumer base.

The ability to personalize playlists, create custom stations, and access exclusive content such as podcasts and artist interviews adds significant value to these subscription services, reinforcing their market dominance.

By Application

In 2023, the Smartphones and Tablets segment held a dominant market position, capturing more than a 65% share of the Cloud Music Services market. This dominance is primarily due to the widespread use of smartphones and tablets, which have become the primary devices for consuming digital content, including music.

With easy access to popular streaming platforms like Spotify, Apple Music, and YouTube Music, consumers can instantly stream their favorite songs, playlists, and albums while on the go. The convenience of having a personal music library on a portable device is a significant driver of this trend.

Smartphones, in particular, have increasingly become essential for daily life, further boosting the demand for cloud music services. As the devices themselves continue to evolve with improved hardware, longer battery life, and enhanced sound quality, they offer an optimal platform for music streaming.

This technological advancement has made music consumption more convenient, leading to a shift in consumer behavior toward digital music services, rather than traditional methods like CDs or MP3 downloads.

The segment’s growth is also fueled by the growing popularity of mobile data plans, enabling users to stream music seamlessly without relying on Wi-Fi. This trend is particularly strong in emerging markets, where smartphone adoption is rapidly increasing, and mobile data is becoming more affordable.

Moreover, the integration of voice assistants like Siri, Google Assistant, and Alexa in smartphones has enhanced the user experience, allowing users to control their music hands-free.

By End-User

In 2023, the Individual Use segment held a dominant market position, capturing more than 81% of the Cloud Music Services market share. This dominance is primarily driven by the increasing number of individual consumers subscribing to music streaming services.

Personal music consumption has become an integral part of daily life, with millions of users relying on services like Spotify, Apple Music, and Amazon Music to access their favorite music, podcasts, and playlists. As more people shift from physical media to digital content, the demand for cloud-based music services has surged, particularly among individuals seeking flexibility and convenience in their music experience.

The individual consumer segment benefits from the accessibility and affordability of subscription-based services. With options like free, ad-supported tiers and premium subscription plans to offer additional features such as offline listening and higher audio quality, individual users can select the most suitable plan for their needs.

The widespread adoption of smartphones and tablets, which provide seamless access to these services, further reinforces the preference for individual use. Additionally, the rise of personalized recommendations and curated playlists based on listening history has made music discovery more enjoyable, further driving engagement among individual users.

Another factor contributing to the dominance of the individual use segment is the increasing cultural shift toward personalized entertainment. Consumers are more inclined to spend on services that allow them to create and enjoy customized experiences. Cloud music services, by offering a vast library of songs, genres, and podcasts, cater perfectly to this growing preference for personalization and convenience.

Key Market Segments

By Type

- Cloud Music Download

- Streaming Subscription

- Ad-based Cloud Music Streaming

By Application

- Smartphones and Tablets

- Cars

- Stereo Systems

- Others

By End-User

- Individual Use

- Commercial Use

Driving Factors

Increasing Smartphone Penetration and Mobile Internet Usage

The growth of the Cloud Music Services market is heavily driven by the increasing penetration of smartphones and mobile internet worldwide. As smartphones become more affordable and accessible, they have become the primary device for streaming music.

With more than 6.8 billion smartphone users globally in 2023, cloud music services have tapped into this vast market. The proliferation of mobile internet, particularly 4G and 5G networks, has facilitated seamless access to music streaming services, improving the overall user experience by reducing latency and buffering.

The integration of cloud-based music platforms with smartphones and tablets has made it easier for users to listen to music on the go, creating a more convenient, personalized, and engaging listening experience. Moreover, the availability of music on-demand has resonated well with consumers who prefer to listen to their favorite tracks or discover new artists without the need for physical media.

This convenience is further enhanced by features such as offline listening and personalized playlists, which have become key selling points for streaming services. Additionally, the rise of mobile internet has expanded the reach of cloud music services to developing regions, where smartphones have become the gateway to digital entertainment.

As more people in regions like Asia-Pacific and Latin America gain access to affordable smartphones and data plans, the global consumer base for cloud music services continues to grow. Consequently, companies like Spotify, Apple Music, and YouTube Music are tapping into these emerging markets, offering tailored services that cater to local tastes and preferences.

Restraining Factors

High Data Consumption and Network Limitations

One of the significant restraints for the Cloud Music Services market is the high data consumption associated with streaming music, especially in high-definition audio formats. While streaming services provide convenience, the volume of data required for streaming music in high-quality formats, such as lossless audio, can place a strain on both users’ data plans and network infrastructure. For consumers, this can mean additional costs and slower streaming speeds if they do not have access to unlimited or high-speed data.

In regions where high-speed internet infrastructure is not widespread, such as rural areas in developing countries, the ability to access cloud music services becomes limited. Users in these areas may experience buffering issues or be unable to stream music altogether due to poor network connectivity.

Furthermore, while mobile carriers have started offering 5G networks, the rollout is still in the early stages in many countries, leaving large portions of the global population reliant on slower 3G or 4G networks.

Additionally, the increasing data consumption associated with music streaming also raises concerns about network congestion. During peak hours, networks can become overloaded, affecting the quality of the streaming experience and leading to customer dissatisfaction.

As more users adopt cloud-based music services and demand higher-quality content, this issue is expected to intensify unless network providers and streaming platforms work together to enhance infrastructure and optimize data usage.

Growth Opportunities

Expansion in Emerging Markets

The Cloud Music Services market has a significant opportunity for expansion in emerging markets, particularly in Asia-Pacific, Latin America, and Africa. As the middle class grows in these regions, there is an increasing demand for affordable, accessible entertainment options. With many consumers in these markets skipping traditional forms of media like cable TV and opting for digital streaming, cloud music services are well-positioned to tap into this demand.

In emerging markets, mobile phones are often the primary device for accessing the internet, and cloud music services can leverage this trend to offer affordable subscription models tailored to local needs. Services like Spotify and Apple Music have already started offering discounted or lower-priced subscription plans to attract consumers in price-sensitive markets.

In addition to this, localized content and regional music preferences are key to appealing to these users, creating opportunities for cloud music services to curate region-specific playlists and collaborate with local artists.

Furthermore, the growing internet penetration, especially with the expansion of affordable 4G and 5G networks, opens up significant opportunities for cloud music providers to increase their market share. As internet connectivity improves, consumers in these regions will have access to a broader range of content, including high-quality audio and exclusive releases that were previously unavailable to them.

Challenging Factors

Intense Competition and Market Saturation

The Cloud Music Services market faces a significant challenge in the form of intense competition and market saturation, especially in mature markets like North America and Europe. As more players enter the market, including tech giants like Amazon, Google, and smaller regional players, competition for market share has become increasingly fierce. Established players such as Spotify, Apple Music, and YouTube Music dominate the landscape, making it difficult for new entrants to gain a foothold.

The competitive landscape is further intensified by the diversity of services offered by these platforms, from exclusive content, podcasts, and personalized playlists, to high-definition audio and partnerships with popular artists. This saturation makes it challenging for platforms to differentiate themselves and attract new subscribers, particularly in regions where most consumers already have a preferred service.

Another challenge for companies in this space is the rising cost of acquiring and retaining subscribers. Music streaming services need to continuously innovate and offer unique features to justify subscription fees, and they must invest heavily in marketing campaigns to stand out from the competition.

Additionally, consumers’ price sensitivity continues to grow, with many users opting for free or ad-supported services, which do not generate as much revenue for the platforms as paid subscriptions.

Growth Factors

The Cloud Music Services market is growing rapidly due to several key factors. First, the increasing number of smartphone users and the widespread availability of affordable mobile data plans have significantly expanded access to streaming services worldwide.

The convenience of accessing music on demand, without the need for physical storage, has drawn in millions of new users. Additionally, the shift from ownership-based music consumption (e.g., CDs) to access-based consumption (streaming) has revolutionized the way people enjoy music.

Moreover, the ongoing development of high-speed mobile internet networks, such as 4G and 5G, is enhancing streaming quality and reducing latency, providing a better user experience. As more consumers in emerging markets, especially in Asia-Pacific and Latin America, gain access to mobile devices and affordable internet, the market for cloud-based music services is expected to continue expanding.

Emerging Trends

An important trend in the Cloud Music Services market is the rise of personalized content. Streaming platforms are increasingly using AI-driven algorithms to curate playlists and recommend new music based on user preferences.

This trend is making music services more tailored and engaging, which enhances user retention. Another key trend is the growth of podcasting and audiobooks within streaming services, offering users more varied content beyond music.

Business Benefits

Cloud Music Services offer numerous benefits to businesses, including access to a large and global customer base. By providing an easy-to-use platform with a wide range of content, companies can tap into subscription-based revenue models, boosting their financial stability.

Furthermore, companies can leverage customer data to improve services, target ads, and optimize content, thereby increasing user engagement and satisfaction.

Regional Analysis

In 2023, North America held a dominant market position, capturing more than a 35.3% share, holding USD 5.41 Billion in revenue. North America continues to lead the Cloud Music Services market, accounting for a substantial share of the global market revenue. This dominance can be attributed to several factors, including the high penetration of smartphones and broadband internet, making it easier for consumers to access streaming services.

The region’s tech-savvy population, alongside a well-established digital infrastructure, provides an ideal environment for cloud-based music streaming platforms to thrive. Additionally, North America has a high adoption rate of subscription-based services, with major players like Spotify, Apple Music, and Amazon Music commanding a significant portion of the market.

The rapid growth of the entertainment and media sector in North America is also a driving factor. Music streaming platforms are becoming integral to everyday life, with consumers increasingly preferring on-demand, personalized music experiences over traditional methods such as physical CDs or downloads.

Furthermore, the region’s robust spending power and high disposable income enable users to invest in premium subscriptions and ad-free experiences, contributing to the region’s strong market presence.

Technological advancements, particularly in the areas of cloud storage, artificial intelligence, and machine learning, have also enhanced the streaming experience for users. These innovations have led to the creation of sophisticated recommendation algorithms that improve user engagement and retention.

As a result, North America is expected to maintain its leadership position, with a growing number of users seeking enhanced, tailored content from their preferred streaming platforms.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

Apple Music continues to be a dominant player in the global cloud music services market. The company has strategically expanded its reach by leveraging its strong ecosystem of devices, including iPhones, iPads, and Macs, offering seamless integration with its streaming platform.

Apple Music frequently updates its features, such as personalized playlists, high-definition audio, and exclusive artist content, ensuring it remains competitive. In recent years, Apple has strengthened its market position through key acquisitions, such as the purchase of Beats Electronics, which provided access to a popular headphone brand and enhanced its music streaming capabilities.

Amazon Music is another key player, benefiting from Amazon’s massive user base and strong infrastructure. Amazon Music offers a comprehensive music streaming service that ranges from free, ad-supported options to premium services like Amazon Music Unlimited.

The company has actively expanded its portfolio by launching new features like integration with Alexa-powered devices, making it a compelling choice for consumers using smart home technology. Amazon’s acquisitions have further fueled its growth, including the purchase of the audiobook platform Audible, which adds to its overall audio content offerings.

Spotify is one of the most influential players in the cloud music services market. Known for its massive catalog and sophisticated music recommendation algorithms, Spotify continues to dominate both in terms of subscribers and engagement.

The company has made several strategic acquisitions to improve its offerings, including the purchase of podcasting platform Anchor and podcast network Parcast, marking its shift toward diversifying its content beyond music. Spotify has also integrated new features like Spotify Wrapped and exclusive artist interviews, creating a strong user engagement strategy.

Top Key Players in the Market

- Apple Inc. (Apple Music)

- Amazon.com Inc. (Amazon Music)

- Spotify Technology S.A.

- Google LLC (YouTube Music)

- Tencent Music Entertainment Group

- Pandora Media Inc.

- iHeartMedia Inc.

- SoundCloud Limited

- Deezer S.A.

- Microsoft Corp.

- JioSaavn

- Samsung Music Hub

- Other Key Players

Recent Developments

- In March 2024: Spotify introduced a new AI-driven feature called “Spotify AI Mix,” a personalized playlist curated based on users’ listening habits and real-time preferences. This development leverages machine learning algorithms to continuously refine playlist suggestions, offering a highly tailored listening experience.

- In February 2024: Apple Music announced the expansion of its high-resolution audio streaming service to more countries, including several in Asia and Europe. The upgrade allows users to enjoy a premium music experience with Dolby Atmos and spatial audio features, delivering a richer, more immersive sound quality.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 15.38 Bn |

| Forecast Revenue (2033) | USD 45.68 Bn |

| CAGR (2024-2033) | 11.50% |

| Largest Market | North America |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Cloud Music Download, Streaming Subscription, Ad-based Cloud Music Streaming), By Application (Smartphones and Tablets, Cars, Stereo Systems, Others), By End-User (Individual Use, Commercial Use) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | Apple Inc. (Apple Music), Amazon.com Inc. (Amazon Music), Spotify Technology S.A., Google LLC (YouTube Music), Tencent Music Entertainment Group, Pandora Media Inc., iHeartMedia Inc., SoundCloud Limited, Deezer S.A., Microsoft Corp., JioSaavn, Samsung Music Hub, Other Key Players |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |