Global Bone Densitometer Devices Market By Product Type (Axial Bone Densitometer and Peripheral Bone Densitometer), By Technology (Dual Energy X-Ray Absorptiometry (DXA), Absorptiometry (pDXA), Peripheral Dual Energy X-Ray, Quantitative Ultrasound (QUS) and Others), By End-User (Hospitals, Diagnostic Centers and Orthopedic Clinics), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 178456

- Number of Pages: 230

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

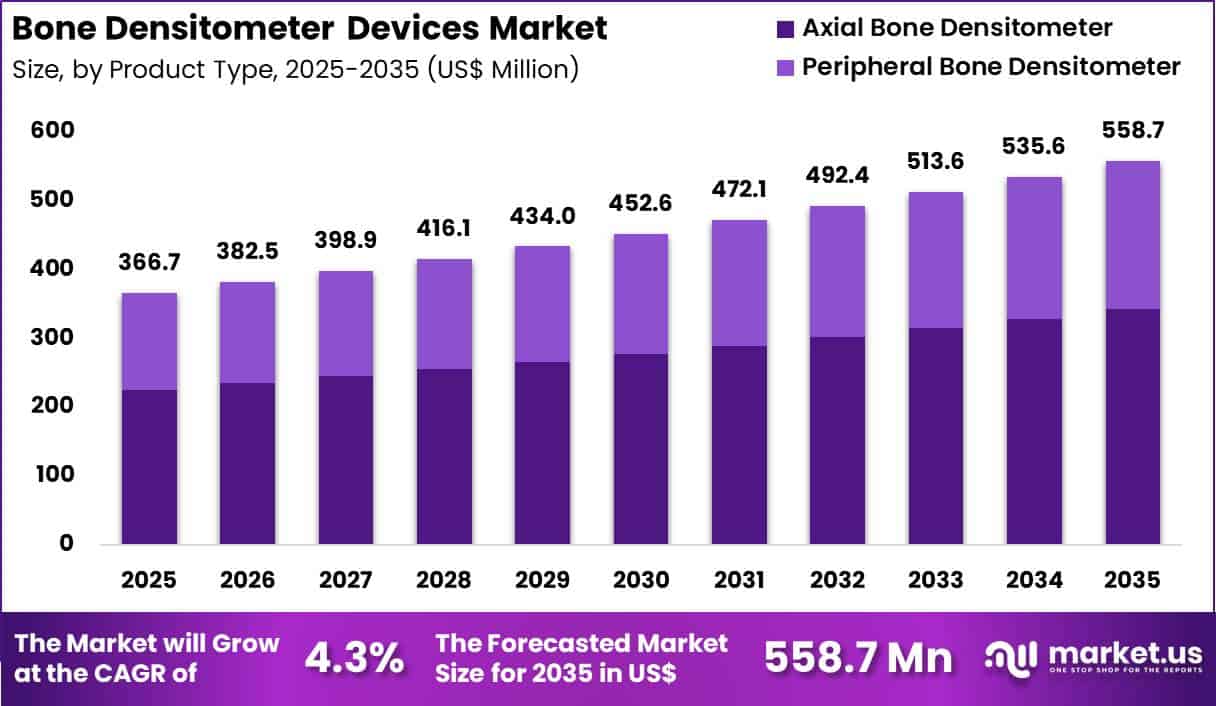

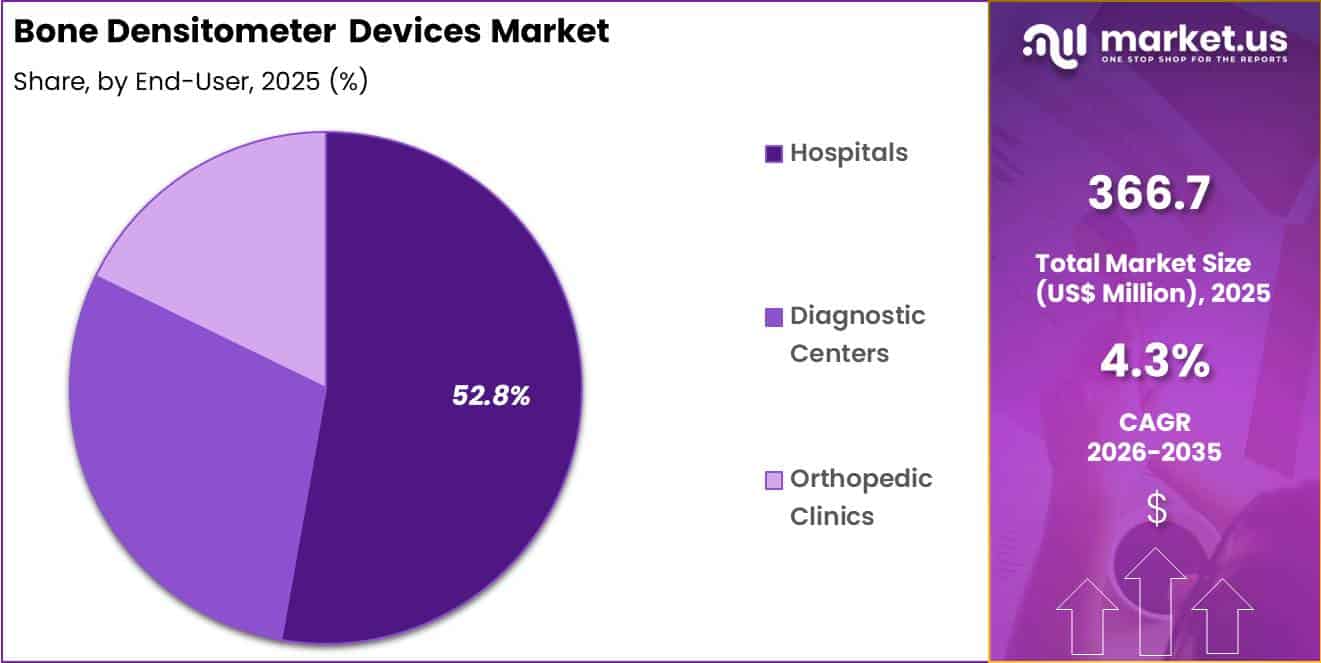

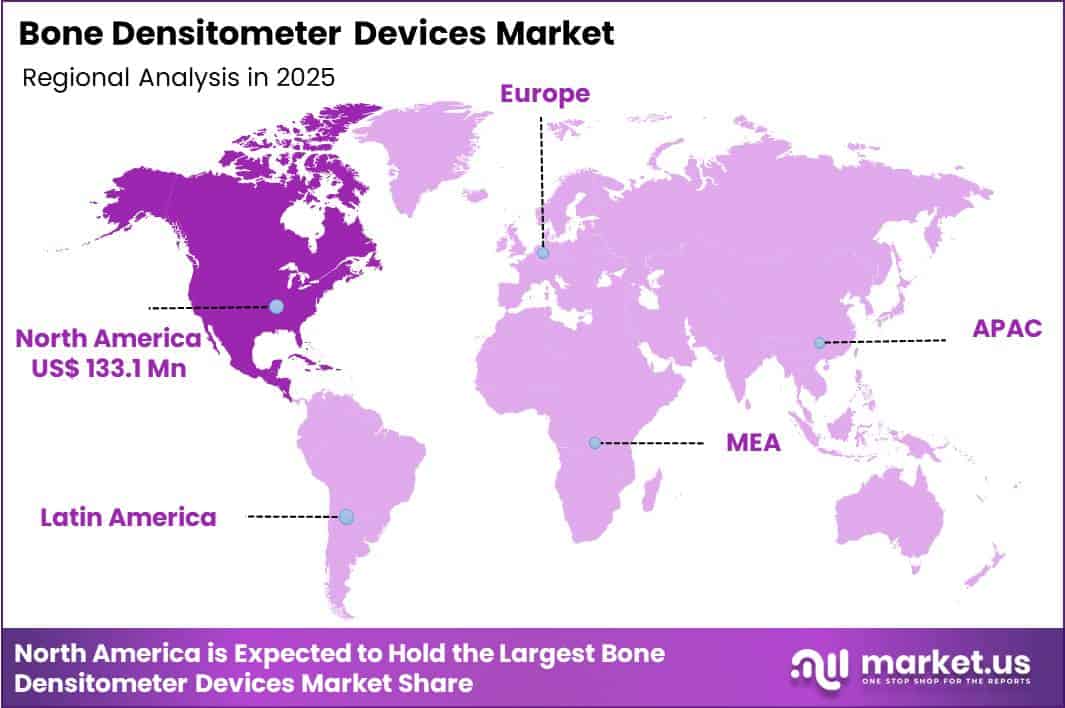

The Global Bone Densitometer Devices Market size is expected to be worth around US$ 558.7 Million by 2035 from US$ 366.7 Million in 2025, growing at a CAGR of 4.3% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 36.3% share with a revenue of US$ 133.1 Million.

Increasing prevalence of osteoporosis and age-related bone loss drives the bone densitometer devices market as healthcare providers prioritize early detection and ongoing monitoring to prevent fragility fractures and associated morbidity. Clinicians increasingly utilize dual-energy X-ray absorptiometry systems to measure bone mineral density at the hip and spine in postmenopausal women, guiding initiation of antiresorptive or anabolic therapies to reduce fracture risk.

These devices support fracture risk assessment in men over 50 years of age, where low bone density combined with clinical risk factors prompts preventive interventions. Endocrinologists apply peripheral quantitative computed tomography to evaluate trabecular and cortical bone compartments in patients with secondary osteoporosis caused by glucocorticoid use or hyperparathyroidism.

Rheumatologists employ bone densitometry in inflammatory arthritis patients to monitor glucocorticoid-induced bone loss and adjust treatment regimens accordingly. Pediatric specialists use these tools to track bone accrual in children with chronic illnesses or nutritional deficiencies, ensuring timely nutritional and pharmacologic support during critical growth periods.

Manufacturers pursue opportunities to integrate artificial intelligence algorithms that automate scan analysis and fracture risk prediction, expanding applications in high-volume screening programs and primary care settings. Developers advance portable, low-dose peripheral devices that enable point-of-care assessments in community health centers and mobile screening units.

These innovations facilitate body composition analysis alongside bone density measurements, supporting comprehensive evaluations in bariatric surgery candidates and metabolic disorder patients. Opportunities emerge in hybrid systems combining densitometry with vertebral fracture assessment, enhancing diagnostic yield in elderly populations.

Companies invest in radiation-reduction technologies and ergonomic designs that improve patient comfort during repeated scans. Recent trends emphasize cloud-based platforms for longitudinal data tracking and multidisciplinary collaboration, positioning bone densitometer devices as essential tools in preventive skeletal health management across diverse clinical indications.

Key Takeaways

- In 2025, the market generated a revenue of US$ 366.7 Million, with a CAGR of 4.3%, and is expected to reach US$ 558.7 Million by the year 2035.

- The product type segment is divided into axial bone densitometer and peripheral bone densitometer, with axial bone densitometer taking the lead with a market share of 61.4%.

- Considering technology, the market is divided into dual energy x-ray absorptiometry (DXA), absorptiometry (pDXA), peripheral dual energy x-ray, quantitative ultrasound (QUS) and others. Among these, dual energy x-ray absorptiometry (DXA)held a significant share of 54.7%.

- Furthermore, concerning the end-user segment, the market is segregated into hospitals, diagnostic centers and orthopedic clinics. The hospitals sector stands out as the dominant player, holding the largest revenue share of 52.8% in the market.

- North America led the market by securing a market share of 36.3%.

Product Type Analysis

Axial bone densitometers contributed 61.4% of growth within product type and led the bone densitometer devices market due to their ability to measure bone mineral density at clinically significant sites such as the spine and hip.

Physicians rely on axial systems for definitive osteoporosis diagnosis and fracture risk assessment. These sites provide higher predictive value for future fractures, which strengthens clinical preference. Rising incidence of age-related bone disorders increases demand for accurate axial assessment.

Growth strengthens as screening guidelines recommend hip and spine evaluation for high-risk populations. Hospitals and diagnostic centers invest in advanced axial systems to improve throughput and reporting accuracy.

Integration with fracture risk assessment tools enhances clinical utility. Increased awareness of preventive bone health further supports adoption. The segment is expected to remain dominant as axial measurements continue to serve as the gold standard in osteoporosis diagnosis.

Technology Analysis

Dual energy X-ray absorptiometry generated 54.7% of growth within technology and emerged as the leading segment due to its established accuracy and low radiation exposure. Clinicians prefer DXA because it delivers reliable and reproducible bone density measurements across major skeletal sites.

Regulatory guidelines recognize DXA as the reference method for osteoporosis evaluation, which reinforces demand. Technological improvements enhance scan speed and patient comfort, increasing clinical efficiency.

Growth accelerates as healthcare providers expand screening programs for postmenopausal women and elderly populations. DXA systems integrate with digital health records and automated analysis software, improving workflow.

Cost-effectiveness compared to alternative imaging modalities strengthens procurement decisions. Training familiarity among radiology staff supports widespread use. The segment is anticipated to maintain leadership as DXA continues to represent the standard diagnostic approach in bone density assessment.

End-User Analysis

Hospitals accounted for 52.8% of growth within end-user and dominated the bone densitometer devices market due to their comprehensive diagnostic infrastructure. Hospitals manage large volumes of patients with osteoporosis, endocrine disorders, and fracture risk concerns. Centralized imaging departments enable efficient scheduling and multidisciplinary care coordination. Institutional screening programs further increase device utilization rates.

Growth continues as hospitals expand geriatric and orthopedic services. Accreditation standards and preventive health initiatives encourage routine bone density screening. Teaching hospitals further drive adoption through research and resident training programs.

Referral patterns concentrate complex cases within hospital settings. The segment is projected to remain the primary growth driver as hospitals continue to anchor advanced diagnostic and preventive bone health services.

Key Market Segments

By Product Type

- Axial Bone Densitometer

- Peripheral Bone Densitometer

By Technology

- Dual Energy X-Ray Absorptiometry (DXA)

- Absorptiometry (pDXA)

- Peripheral Dual Energy X-Ray

- Quantitative Ultrasound (QUS)

- Others

By End-User

- Hospitals

- Diagnostic Centers

- Orthopedic Clinics

Drivers

Increasing prevalence of osteoporosis is driving the market.

The rising incidence of osteoporosis among aging populations has significantly increased the demand for bone densitometer devices to enable early detection and monitoring of bone mineral density loss. Improved awareness campaigns and screening guidelines have led to more routine bone density assessments in at-risk groups.

Healthcare providers are prioritizing these devices to reduce fracture risks and associated healthcare costs. The correlation between postmenopausal women and higher osteoporosis rates underscores the need for accurate diagnostic tools. Government health organizations are promoting preventive screening programs to address this public health concern.

Bone densitometers, particularly dual-energy X-ray absorptiometry systems, remain the gold standard for diagnosing osteoporosis. National health surveys document the growing burden of low bone mass in older adults. Key manufacturers are developing portable and high-precision models to meet clinical requirements.

This driver supports broader adoption across hospitals, clinics, and outpatient facilities. According to the Centers for Disease Control and Prevention, the age-adjusted prevalence of osteoporosis among adults aged 50 and older was 12.6% in 2022 and 13.1% in 2023.

Restraints

High cost of advanced bone densitometer systems is restraining the market.

The substantial pricing of state-of-the-art dual-energy X-ray absorptiometry and quantitative computed tomography systems limits their acquisition in facilities with constrained budgets. Manufacturing requirements for high-resolution detectors and radiation safety features contribute to elevated production costs.

Smaller clinics and public hospitals often delay purchases, favoring older or refurbished equipment. Regulatory compliance for calibration and quality assurance adds to ongoing operational expenses. In resource-limited settings, these costs restrict routine screening programs. Providers may rely on less precise alternatives to manage financial pressures.

This restraint particularly affects adoption in developing regions with limited healthcare funding. Industry efforts to introduce compact, lower-cost models provide partial mitigation. Despite superior diagnostic accuracy, economic barriers slow widespread replacement of legacy systems. Addressing affordability through financing options remains essential for overcoming this market limitation.

Opportunities

Growth in osteoporosis screening revenues is creating growth opportunities.

The consistent increase in revenues from bone density screening services indicates strong potential for bone densitometer devices in preventive healthcare programs. Enhanced reimbursement policies support expanded utilization in primary care and specialized clinics. Strategic partnerships with radiology networks facilitate broader deployment of densitometry equipment.

The substantial screening volume in aging populations amplifies prospects for device upgrades and new installations. Policy advancements in fracture prevention strengthen infrastructure for densitometer adoption. Leading manufacturers are pursuing geographic expansions to capitalize on rising demand. This opportunity aligns with efforts to reduce osteoporosis-related fractures through early intervention.

Focused initiatives can generate notable progress in integrated bone health management. Hologic reported bone health segment revenues of $318 million in fiscal year 2023 and $342 million in fiscal year 2024. This growth reflects increasing clinical adoption of densitometer systems worldwide.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions influence the bone densitometer devices market through hospital capital planning, outpatient imaging volumes, and reimbursement discipline. Inflation and higher interest rates increase financing costs for diagnostic equipment, which slows replacement cycles and new installations in smaller clinics.

Geopolitical tensions disrupt supplies of detectors, X ray components, electronics, and shielding materials, creating procurement risk and longer delivery timelines. Current US tariffs on imported imaging systems and subcomponents raise acquisition and service expenses, which compresses vendor margins and extend buyer approval processes.

These pressures weigh more heavily on community hospitals and diagnostic centers with limited capital flexibility. On the positive side, trade exposure encourages domestic assembly, diversified sourcing, and stronger service networks.

Rising osteoporosis screening initiatives and aging population trends sustain clinical demand for bone health assessment. With disciplined sourcing, workflow efficiency, and technology refinement, the market remains positioned for stable and confident growth.

Latest Trends

Introduction of portable bone densitometer devices is a recent trend in the market.

In 2024, manufacturers launched compact, portable bone densitometer systems designed for point-of-care use in clinics and mobile health units. These devices incorporate lightweight designs and battery-powered operation for greater accessibility in non-hospital settings. Clinical evaluations in 2024 confirmed comparable accuracy to traditional stationary systems.

The trend emphasizes ease of transport and quick setup for community screening programs. BeamMed introduced the Sunlight MiniOmni portable bone densitometer in 2024, featuring ultrasound technology for radiation-free measurements. This launch targets primary care and remote healthcare facilities.

Regulatory clearances in 2024 for these portable models have accelerated their clinical integration. Industry collaborations focus on user-friendly interfaces and automated reporting. These developments aim to improve screening rates in underserved populations. Portable densitometers position the market for expansion beyond centralized imaging departments.

Regional Analysis

North America is leading the Bone Densitometer Devices Market

North America accounted for a 36.3% share of the Bone Densitometer Devices market in 2024, supported by expanding osteoporosis screening and preventive care initiatives. Healthcare providers increased dual energy X ray absorptiometry testing to identify low bone mineral density at earlier stages, particularly among postmenopausal women and older adults.

Hospitals and specialty clinics upgraded imaging systems to improve diagnostic precision and workflow efficiency. Growing awareness of fracture risk and its economic burden encouraged routine screening in primary care settings. Reimbursement coverage for diagnostic scans strengthened patient access across the US and Canada.

Sports medicine and endocrinology practices also incorporated densitometry to monitor treatment outcomes. A clear supporting indicator comes from the Centers for Disease Control and Prevention, which reported in 2023 that about 12.6% of US adults aged 50 and older have osteoporosis at the femur neck or lumbar spine, underscoring sustained demand for bone health diagnostics.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

The Bone Densitometer Devices market in Asia Pacific is expected to grow steadily during the forecast period as aging populations expand rapidly across key countries. Governments promote early detection of osteoporosis to reduce long term fracture related healthcare costs. Urban hospitals invest in advanced diagnostic imaging systems to strengthen preventive screening programs.

Rising life expectancy increases the number of elderly individuals vulnerable to bone density loss. Public awareness campaigns encourage routine bone health assessments, particularly among women. Private healthcare providers also introduce comprehensive wellness packages that include densitometry testing.

A verifiable signal of demographic momentum appears in 2023 data from the World Health Organization, which confirmed that the Western Pacific Region contains one of the fastest growing aging populations globally, reinforcing long term demand for bone mineral density assessment technologies across Asia Pacific.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key competitors in the bone densitometer devices market grow by enhancing imaging precision, faster scan protocols, and advanced software analytics that support osteoporosis risk assessment and comprehensive skeletal health profiling. They also strengthen value propositions by integrating connectivity with electronic health records and physician reporting tools that improve clinical workflow and patient follow-up.

Firms pursue strategic partnerships with orthopedic and endocrinology clinics, imaging centers, and preventive health networks to embed their solutions into routine care pathways and expand recurring demand.

Geographic expansion into North America, Europe, and fast-growing Asia Pacific broadens addressable markets while balancing demand across mature and emerging healthcare systems. **Hologic, Inc.** exemplifies a diversified medical technology company with a strong portfolio of densitometry and imaging solutions supported by global distribution channels and coordinated commercial strategies tailored to bone health and women’s health priorities.

The company advances its competitive position through disciplined investment in product innovation, targeted collaborations with clinical specialists, and a customer-centric approach that aligns technical enhancements with evolving provider needs.

Top Key Players

- Hologic

- GE HealthCare

- Medtronic

- Siemens Healthineers

- Furuno Electric

- OsteoSys

- DMS Group

- Lunar (GE)

- Osteometer MediTech

- D & R Ferreol

Recent Developments

- In February 2024, Fujifilm India marked the launch of its FDX Visionary-DR dual-energy X-ray absorptiometry system during the inauguration of the Center for Sports Injury in Delhi. The system incorporates advanced 3D capabilities that transform standard bone mineral density scans into three-dimensional representations of the femur, supporting enhanced orthopedic assessment.

- In November 2023, Bupa Hong Kong, together with Quality Healthcare Medical Services Limited, unveiled the Alpha Medical Diagnostic Center in Mong Kok at Pioneer Center. Spanning approximately 6,000 square feet, the newly established facility delivers a range of advanced imaging and diagnostic services, including bone densitometry for comprehensive skeletal health evaluation.

Report Scope

Report Features Description Market Value (2025) US$ 366.7 Million Forecast Revenue (2035) US$ 558.7 Million CAGR (2026-2035) 4.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Axial Bone Densitometer and Peripheral Bone Densitometer), By Technology (Dual Energy X-Ray Absorptiometry (DXA), Absorptiometry (pDXA), Peripheral Dual Energy X-Ray, Quantitative Ultrasound (QUS) and Others), By End-User (Hospitals, Diagnostic Centers and Orthopedic Clinics) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Hologic, GE HealthCare, Medtronic, Siemens Healthineers, Furuno Electric, OsteoSys, DMS Group, Lunar (GE), Osteometer MediTech, D & R Ferreol Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Bone Densitometer Devices MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Bone Densitometer Devices MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Hologic

- GE HealthCare

- Medtronic

- Siemens Healthineers

- Furuno Electric

- OsteoSys

- DMS Group

- Lunar (GE)

- Osteometer MediTech

- D & R Ferreol

Our Clients

- 178456

- Feb 2026