Quick Navigation

Report Overview

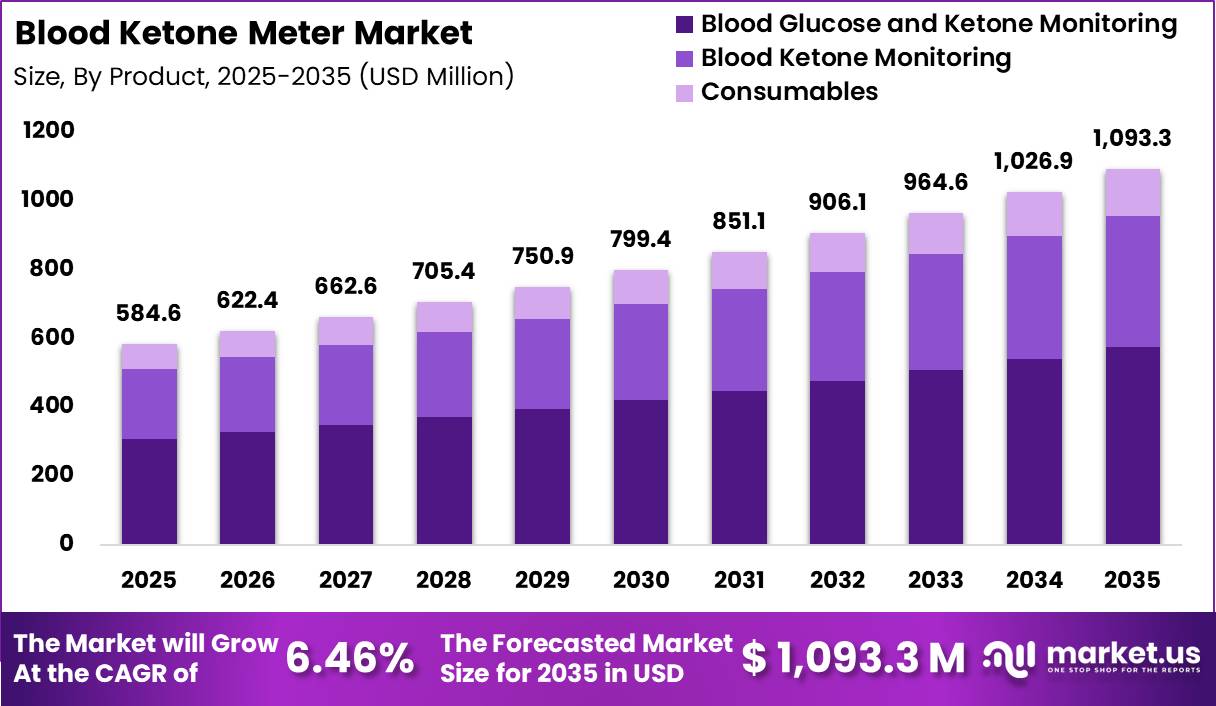

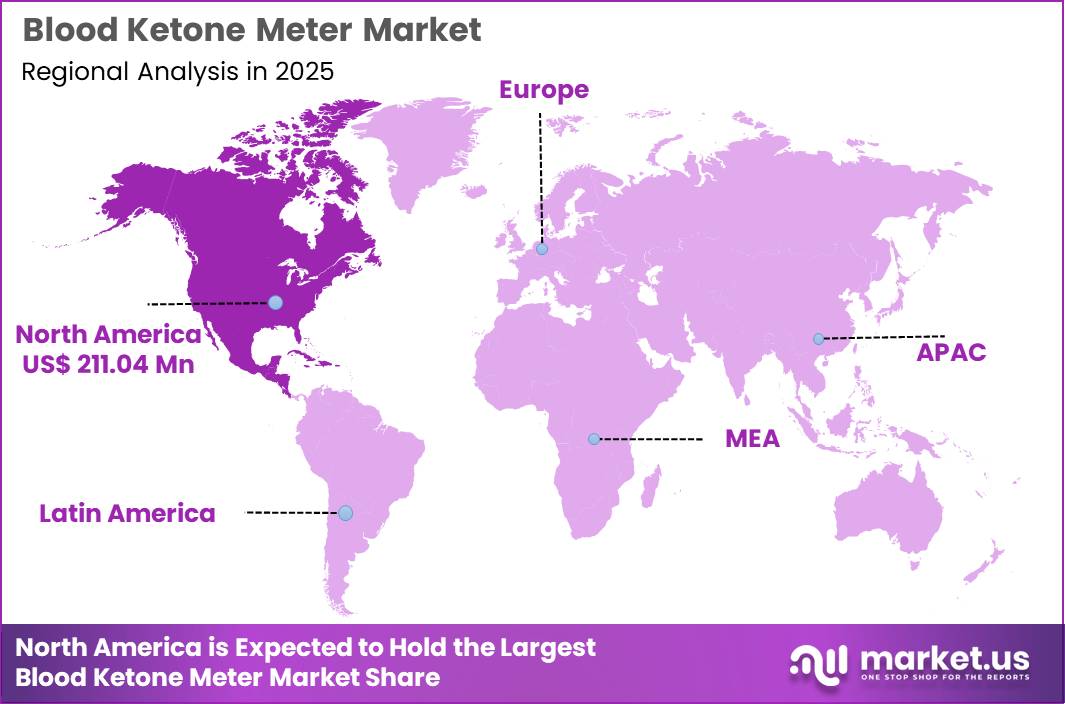

Global Blood Ketone Meter Market size is expected to be worth around US$ 1093.3 Million by 2035 from US$ 584.6 Million in 2025, growing at a CAGR of 6.46% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 36.10% share with a revenue of US$ 211.04 Million.

A blood ketone meter is a diagnostic device designed to measure ketone concentration in the bloodstream, offering the highest level of accuracy compared to alternative methods. These devices are often integrated with blood glucose meters, enabling dual monitoring of glucose and ketone levels. Market growth is primarily driven by the rising prevalence of diabetes and increasing awareness regarding ketone monitoring among patients.

Ketone meter technology has expanded significantly, with modern devices delivering rapid and precise results. Integration with digital health platforms allows real-time data tracking and sharing with healthcare providers.

While glucose remains the body’s primary energy source, ketones are produced under specific metabolic conditions and can be detected in blood or urine. Monitoring ketone levels is essential for identifying diabetic ketoacidosis (DKA), a serious complication, particularly associated with type 1 diabetes.

According to the International Diabetes Federation, approximately 536 million diabetes cases were reported globally in 2020, with projections reaching 642 million by 2030. This increase highlights the growing need for effective ketone monitoring solutions. Additionally, the rising adoption of ketogenic and low-carbohydrate diets has expanded the consumer base beyond diabetic patients.

Blood ketone monitoring is gaining traction due to its role in metabolic health management and preventive care. These devices provide real-time insights, supporting informed dietary and lifestyle decisions. Furthermore, research into ketosis for neurological disorders such as epilepsy and Alzheimer’s disease is contributing to market expansion.

Technologically, ketone meters utilize electrochemical biosensors or photometric analysis to detect beta-hydroxybutyrate (BHB). Compared to urine and breath tests, these devices offer superior accuracy, convenience, and timeliness, reinforcing their adoption across diverse user segments.

Key Takeaways

- Market Size: Global Blood Ketone Meter Market size is expected to be worth around US$ 1093.3 Million by 2035 from US$ 584.6 Million in 2025.

- Market Share: The market growing at a CAGR of 6.46% during the forecast period from 2026 to 2035.

- Product Analysis: In 2025, the Blood Glucose and Ketone Monitoring segment is projected to dominate the market, accounting for approximately 52.6% of the total share.

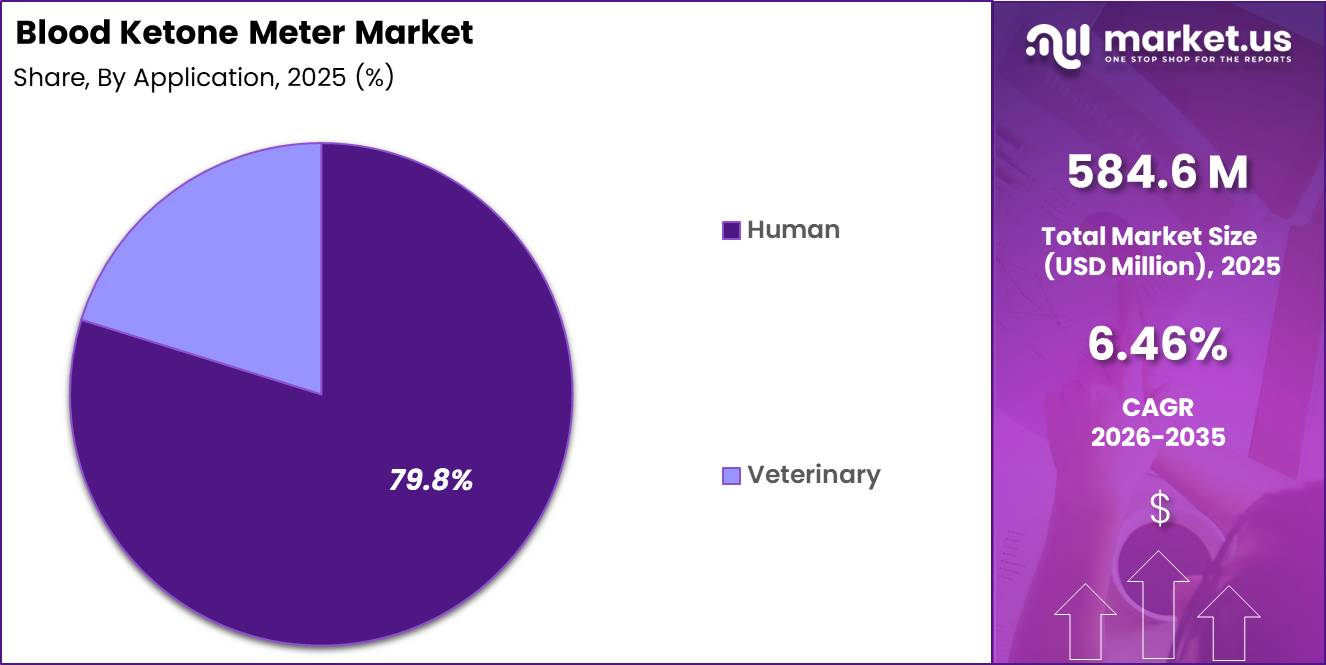

- Application Analysis: The Human segment is expected to lead the market with a 79.8% share in 2025

- End-Use Analysis: Hospitals are anticipated to hold the largest share of 41.6% in 2025.

- Region Analysis: In 2025, North America led the market, achieving over 36.10% share with a revenue of US$ 211.04 Million.

Product Analysis

The Blood Ketone Meter Market is segmented into Blood Glucose and Ketone Monitoring, Blood Ketone Monitoring, and Consumables. In 2025, the Blood Glucose and Ketone Monitoring segment is projected to dominate the market, accounting for approximately 52.6% of the total share.

This dominance can be attributed to the increasing demand for dual-function devices that enable simultaneous monitoring of glucose and ketone levels, particularly among diabetic patients at risk of ketoacidosis.

The integration of multi-parameter monitoring enhances clinical efficiency and supports better disease management outcomes. The Blood Ketone Monitoring segment is also experiencing steady growth, driven by rising awareness of ketone tracking in diabetes care and ketogenic diet adoption.

Additionally, the Consumables segment, including test strips and lancets, represents a recurring revenue stream and is supported by the growing installed base of monitoring devices. Continuous usage requirements and frequent replenishment cycles contribute to its stable growth trajectory. Overall, product innovation and increased accessibility of portable monitoring devices are expected to sustain segment expansion.

Application Analysis

Based on application, the Blood Ketone Meter Market is categorized into Human and Veterinary segments. The Human segment is expected to lead the market with a 79.8% share in 2025, primarily driven by the rising global prevalence of diabetes and the increasing need for effective monitoring of diabetic ketoacidosis (DKA).

The growing adoption of ketogenic diets for weight management and therapeutic purposes has further strengthened demand for ketone monitoring in human healthcare. Technological advancements in handheld and user-friendly devices have enhanced patient compliance and expanded usage in homecare settings.

Meanwhile, the Veterinary segment is gaining traction, supported by increasing awareness of metabolic disorders in animals, particularly in livestock and companion animals. Conditions such as ketosis in dairy cattle have necessitated the adoption of ketone monitoring solutions in veterinary practice.

Although comparatively smaller, this segment is expected to witness moderate growth due to expanding animal healthcare expenditure and improved diagnostic capabilities in veterinary medicine.

End-Use Analysis

The market, by end-use, is segmented into Hospitals, Diagnostic Centers, Homecare Settings, and Others. Hospitals are anticipated to hold the largest share of 41.6% in 2025, supported by the high volume of patient admissions requiring critical monitoring of ketone levels, especially in cases of diabetic emergencies. The availability of advanced diagnostic infrastructure and skilled healthcare professionals further strengthens hospital-based adoption.

Diagnostic Centers also represent a significant segment, benefiting from the increasing demand for routine and specialized testing services. These centers play a crucial role in early detection and disease management, contributing to steady demand for ketone monitoring devices.

Homecare Settings are emerging as a rapidly growing segment, driven by the shift toward decentralized healthcare and increased patient preference for self-monitoring solutions. The Others segment, including research institutions and ambulatory care units, contributes marginally but supports overall market expansion through specialized applications.

Key Market Segments

By Product

- Blood Ketone Monitoring

- Blood Glucose and Ketone Monitoring

- Consumables

By Application

- Human

- Veterinary

By End-use

- Hospitals

- Diagnostic Centers

- Homecare Settings

- Others

Driving Factors

Rising Diabetes Burden and Clinical Need for Early Ketone Detection

The growth of the blood ketone meter market is strongly driven by the increasing global burden of diabetes and the clinical necessity to prevent diabetic ketoacidosis (DKA).

According to clinical evidence from Indian Council of Medical Research, individuals with type 1 diabetes are at high risk of ketosis, where the β-hydroxybutyrate ratio can increase from a normal 1:1 to as high as 10:1 during DKA episodes.

Additionally, DKA has been reported as an initial presentation in up to 30% of type 1 diabetes cases in earlier studies, indicating significant diagnostic reliance on ketone monitoring. Blood ketone testing is recommended when glucose exceeds 13.9 mmol/L (250 mg/dL), reinforcing its role in emergency prevention.

Government-backed guidelines emphasize that point-of-care ketone monitoring reduces hospital admissions and improves patient outcomes. As diabetes prevalence continues to expand, particularly in emerging economies, demand for accurate, rapid, and home-based ketone monitoring devices is expected to increase significantly.

Trending Factors

Shift Toward Blood-Based and Continuous Ketone Monitoring Technologies

A key trend shaping the blood ketone meter market is the transition from urine-based testing to blood-based and continuous monitoring technologies. Clinical guidelines from National Health Service recommend blood ketone measurement as the preferred method due to higher accuracy and real-time assessment capability.

Blood ketone monitoring has demonstrated improved clinical outcomes, with studies showing higher patient compliance (91%) compared to urine testing (61%) during sick days. Furthermore, hospitalization rates were reduced from 75 to 38 per 100 person-years with blood ketone monitoring, indicating strong healthcare system benefits.

Another emerging trend is the development of continuous ketone monitoring (CKM) systems, which provide real-time tracking of metabolic status over extended periods. These systems align with the broader digital health ecosystem, integrating with wearable devices and mobile applications.

The trend toward precision monitoring and early intervention is expected to accelerate adoption, particularly among high-risk diabetic populations and technologically advanced healthcare systems.

Restraining Factors

Cost, Accessibility, and Limited Adoption in Routine Care

Despite clinical advantages, the adoption of blood ketone meters is constrained by cost factors, limited accessibility, and inconsistent usage in routine care. Evidence indicates that adherence to ketone monitoring remains relatively low due to device costs and operational limitations. Blood ketone strips and meters are generally more expensive than urine-based alternatives, creating affordability challenges, particularly in low- and middle-income regions.

Additionally, healthcare system limitations persist; studies have highlighted that availability of bedside ketone meters in hospitals is still restricted, and trained personnel may not be accessible 24/7. Quality assurance systems for ketone meters are also less developed compared to glucose monitoring devices, affecting reliability and adoption.

While clinical guidelines recommend ketone testing for individuals with hyperglycemia or illness, actual implementation remains inconsistent. These structural and economic barriers are expected to limit market penetration, especially in public healthcare systems with constrained budgets and limited diagnostic infrastructure.

Opportunity

Expansion of Home-Based Monitoring and Preventive Healthcare

Significant opportunities exist in the expansion of home-based monitoring and preventive healthcare initiatives. Guidelines from global health authorities recommend ketone testing for individuals experiencing hyperglycemia, illness, or symptoms of ketosis, emphasizing its role in self-management.

Blood ketone levels below 0.6 mmol/L are considered normal, while levels above 1.5 mmol/L indicate increased clinical risk, highlighting the importance of regular monitoring. The increasing focus on patient-centered care and remote disease management is creating demand for portable and easy-to-use devices.

Government and healthcare systems are promoting self-monitoring to reduce hospital burden and improve early intervention outcomes. Additionally, rising awareness of metabolic health, including ketogenic diets and preventive screening, is expanding the user base beyond diabetic patients.

Integration with digital health platforms and telemedicine services further enhances growth potential. As healthcare systems prioritize cost reduction and early diagnosis, blood ketone meters are expected to play a critical role in decentralized and preventive care models.

Regional Analysis

North America led the market, achieving over 36.10% share with a revenue of US$ 211.04 Million.

North America continues to maintain a dominant position in the blood ketone meter market, supported by advanced healthcare infrastructure and strong adoption across the United States and Canada. High healthcare expenditure, favorable reimbursement systems, and early integration of advanced monitoring technologies have contributed significantly to market expansion.

Increased awareness of metabolic health and effective management of diabetic ketoacidosis has led to higher routine ketone testing, particularly among insulin-dependent patients. Additionally, the rising popularity of ketogenic diets and preventive healthcare practices has broadened consumer adoption.

Demand remains strong across hospitals, outpatient facilities, and home-care settings, where accurate point-of-care devices are increasingly utilized. Ongoing strategic collaborations, mergers, and acquisitions among key industry participants further enhance innovation and product availability, supported by well-defined regulatory frameworks.

In contrast, Asia Pacific is emerging as a high-growth region, driven by the increasing burden of diabetes and metabolic disorders. Rapid urbanization, evolving dietary habits, and sedentary lifestyles have accelerated disease prevalence across major economies.

Improving healthcare infrastructure, expanding access to diagnostic services, and rising disposable incomes are facilitating wider adoption of monitoring devices. Government-led health initiatives and digital healthcare integration are also strengthening early diagnosis and continuous monitoring.

Market participants are focusing on cost-effective solutions, local manufacturing, and technologically advanced portable devices, positioning the region as a key growth contributor in the coming years.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The blood ketone meter market demonstrates a moderately competitive structure, where companies are assessed based on product range, financial stability, recent strategic initiatives, geographic footprint, and overall market positioning.

Innovation remains a key competitive factor, with manufacturers focusing on dual-function devices that measure both glucose and ketone levels, alongside improvements in strip accuracy, faster results, and user-friendly designs. Integration of digital connectivity features, including app-based tracking and data sharing, has further enhanced product differentiation.

Strategic partnerships with hospitals, diabetes care centers, and digital health platforms are increasingly being adopted to strengthen market presence. Additionally, mergers, acquisitions, and regional expansion strategies are actively pursued to improve distribution capabilities and access emerging markets.

Investments in regulatory compliance, production capacity expansion, and online sales channels are also being prioritized. These initiatives collectively enable companies to address rising demand across home-care settings, wellness monitoring, and acute-care environments, thereby sustaining competitive growth in the global market.

Market Key Players

- Abbott

- Apex Biotechnology Corp.

- TaiDoc Technology Corporation

- EKF Diagnostics Holdings plc.

- Nova Biomedical

- Keto-Mojo

- ForaCare, Inc.

- Nipro

- i-SENS, Inc

- Others

Recent Developments

- January, 2026 – Abbott announced continued investment in biosensor innovation and strategic acquisitions of emerging diagnostic startups to strengthen its ketone-monitoring portfolio and accelerate R&D capabilities in connected metabolic monitoring solutions.

- April, 2026 – Nova Biomedical expanded its presence in advanced metabolic testing by enhancing its point-of-care ketone monitoring systems, focusing on multi-analyte capabilities to improve clinical decision-making in acute-care settings.

- March, 2026 – EKF Diagnostics Holdings plc. strengthened its diabetes care portfolio by promoting advanced dual glucose-ketone analyzers, supporting rapid and accurate testing in decentralized and near-patient environments.

- February, 2026 – TaiDoc Technology Corporation focused on expanding its global footprint through partnerships and distribution agreements, targeting emerging Asia-Pacific markets with cost-effective ketone monitoring devices.

- September, 2025 – Nipro Corporation expanded manufacturing capabilities to meet rising global demand, particularly across North America and Asia-Pacific regions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 584.6 Million |

| Forecast Revenue (2035) | US$ 1093.3 Million |

| CAGR (2026-2035) | 4.46% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Blood Ketone Monitoring, Blood Glucose and Ketone Monitoring, Consumables) By Application (Human, Veterinary) By End-use(Hospitals, Diagnostic Centers, Homecare Settings, Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Abbott, Apex Biotechnology Corp., TaiDoc Technology Corporation, EKF Diagnostics Holdings plc., Nova Biomedical,Keto-Mojo, ForaCare, Inc., Nipro, i-SENS, Inc,Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |