Quick Navigation

Report Overview

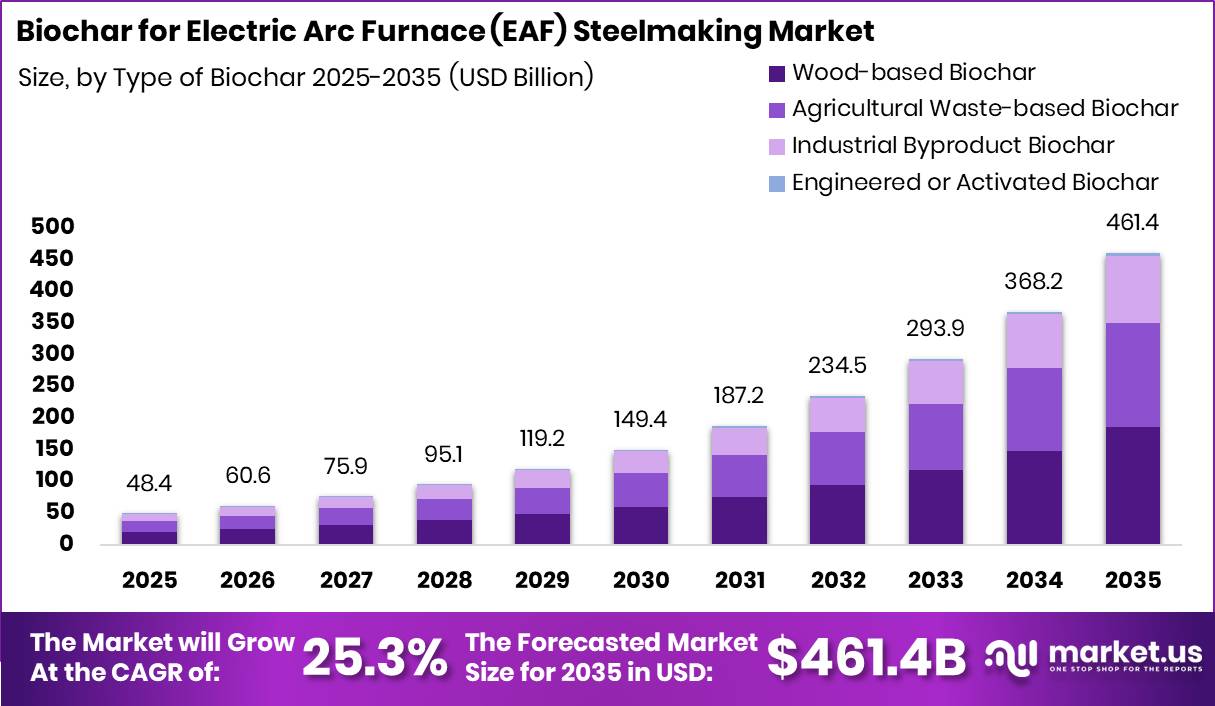

Global Biochar for Electric Arc Furnace (EAF) Steelmaking Market size is expected to be worth around USD 461.4 Billion by 2035 from USD 48.4 Billion in 2025, growing at a CAGR of 25.3% during the forecast period 2026 to 2035. As per our research, a 2026 EAF steelmaking case study confirmed that replacing coke fines with wood biochar reduced CO₂ emissions by 83.8 kg CO₂-eq per tonne of crude steel, a 20.9% reduction versus the baseline process. This result converts biochar from a sustainability signal into a measurable, commercially defensible input.

The biochar for EAF steelmaking market covers the production, qualification, and commercial supply of biogenic carbon materials used as charge carbon, carbon injectants, recarburizers, and slag foaming agents inside electric arc furnace steelmaking operations. The market spans wood-based, agricultural waste-based, industrial byproduct, and engineered or activated biochar, produced through slow pyrolysis, fast pyrolysis, gasification, torrefaction, hydrothermal treatment, and related conversion technologies. This structure positions the market at the intersection of industrial decarbonization and metallurgical raw material supply.

Key Takeaways

- Market size in 2025: USD 48.4 Billion

- Market forecast for 2035: USD 461.4 Billion

- CAGR (2026–2035): 25.3%

- Dominant segment by Type of Biochar: Wood-based Biochar with a 40.2% share

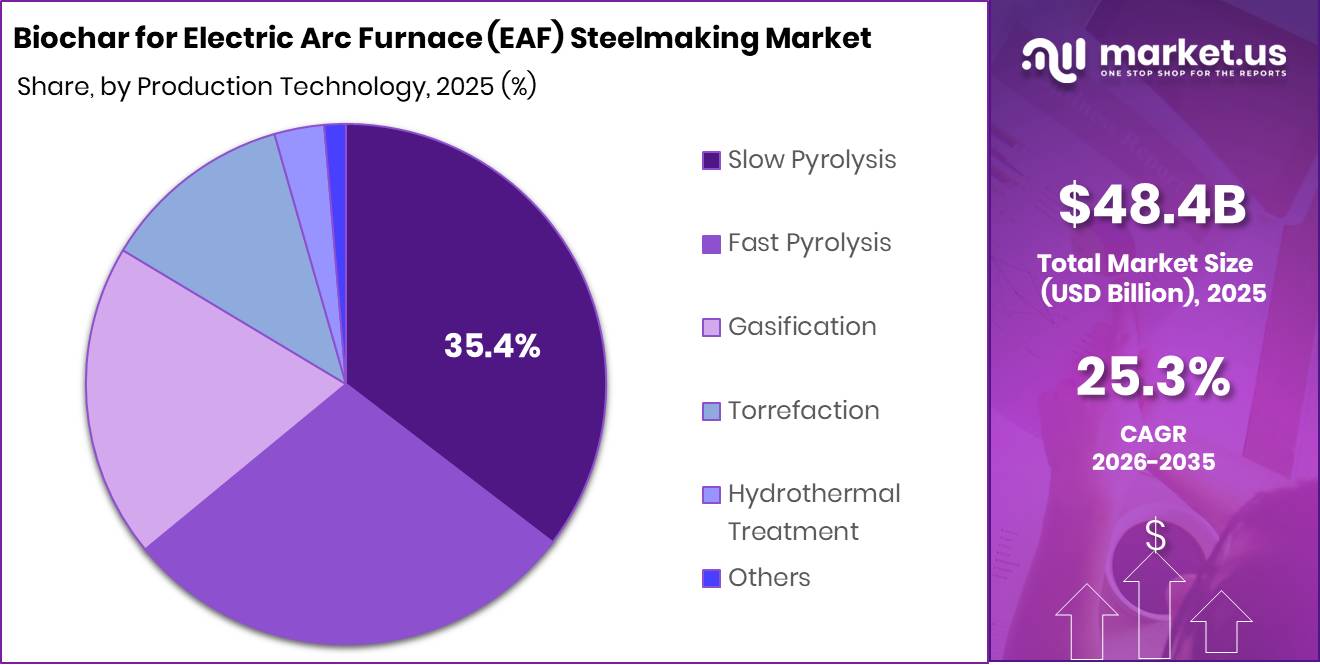

- Dominant segment by Production Technology: Slow Pyrolysis with a 35.4% share

- Dominant segment by Application: Carbon Injectant with a 35.6% share

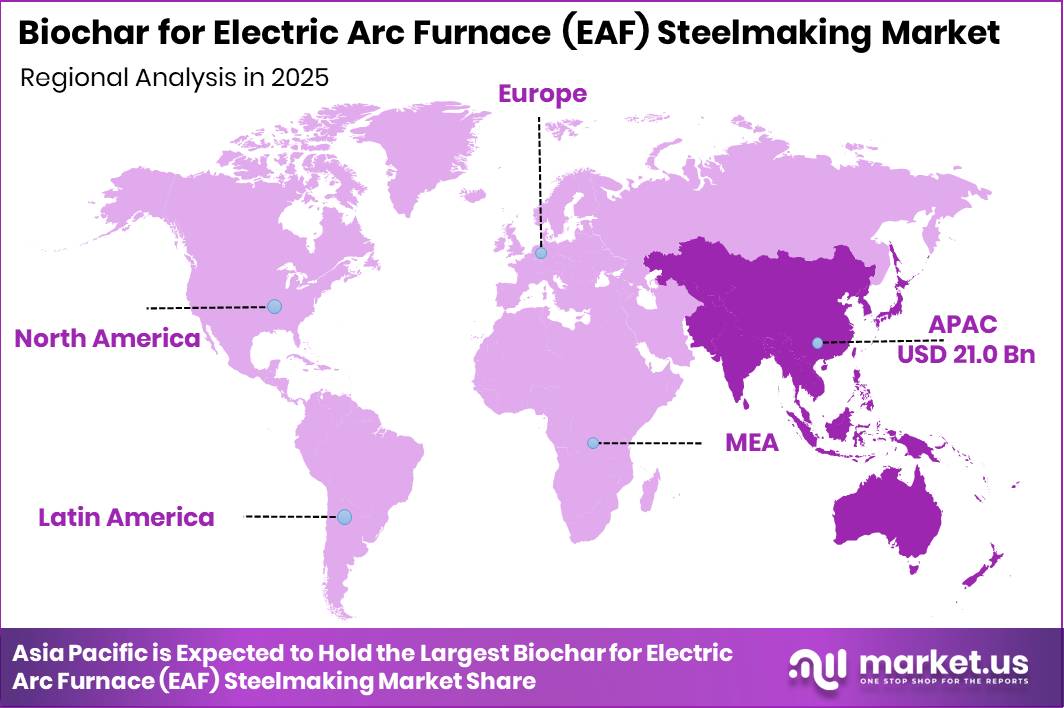

- Dominant region: Asia Pacific with a 43.5% share, valued at USD 21.0 Billion

The EU Carbon Border Adjustment Mechanism entered its definitive regime on 1 January 2026, covering iron and steel with mandatory embedded-emissions declarations. Average 2025 EU ETS auction prices reached EUR 73.43 per tCO₂e, with a six-month average of EUR 75.65 through May 2026. These price levels make even partial fossil carbon displacement financially material across billet, long-product, and specialty steel volumes.

According to worldsteel, average CO₂ intensity stands at approximately 0.70 tCO₂ per tonne for scrap-EAF routes and 1.43 tCO₂ per tonne for DRI-EAF routes. As per our research, China produced only 10% of its crude steel via EAF in 2023 against a national target of 15% by 2025, signaling a structural expansion gap for biochar demand in the world’s largest steel market. Data from worldsteel shows global crude steel production reached 158.8 million tonnes in May 2025 alone, establishing the scale of the addressable decarbonization opportunity for biochar suppliers.

In January 2026, CHAR Technologies reported the transition of its Thorold project from pilot operations toward full commercialization, with biocarbon production underway for heavy industrial sectors including steelmaking. This shift represents the first major commercial-scale biocarbon supply node in North America. As a result, qualification timelines for EAF mills in the region are shortening, reducing the lag between trial adoption and multi-site offtake contracts.

Type of Biochar Analysis

Wood-based Biochar dominates with 40.2% due to superior fixed-carbon content and consistent particle sizing.

In 2025, Wood-based Biochar held a dominant market position in the By Type of Biochar segment of the Biochar for Electric Arc Furnace (EAF) Steelmaking Market, with a 40.2% share. Wood-derived feedstocks consistently produce biochar with high fixed-carbon purity and stable particle geometry, meeting the tight metallurgical specifications EAF operators require. As per our research, full coke-fines substitution requires 25.6 kg of wood biochar per tonne of crude steel, a loading rate that EAF procurement teams can model directly into input cost calculations.

Agricultural Waste-based Biochar serves as an alternative input for mills seeking lower-cost or regionally available feedstocks. However, performance benchmarks differ from wood-derived material. As per our research, rice husk biochar requires 39.4 kg per tonne of crude steel to achieve complete coke-fines replacement, a 54% higher loading rate than wood biochar. This higher volume requirement increases logistics costs and blending complexity, creating a clear cost-efficiency disadvantage versus wood-based material at equivalent carbon output targets.

Industrial Byproduct Biochar and Engineered or Activated Biochar collectively address the remaining share. Industrial byproduct material captures low-cost conversion economics from existing waste streams, while engineered and activated grades target precision applications such as slag chemistry control and emissions measurement. These segments remain at earlier commercialization stages but offer higher margin potential as specification standards tighten under CBAM-linked procurement frameworks.

Production Technology Analysis

Slow Pyrolysis dominates with 35.4% due to superior fixed-carbon yield and metallurgical consistency.

In 2025, Slow Pyrolysis held a dominant market position in the By Production Technology segment of the Biochar for Electric Arc Furnace (EAF) Steelmaking Market, with a 35.4% share. Slow pyrolysis operates at lower temperatures over extended residence times, producing high fixed-carbon biochar that meets the approximately 80% carbon threshold required for EAF charge use. This yield consistency reduces rejection risk at the plant gate and supports multi-site offtake contracts where metallurgical repeatability is a procurement requirement.

Fast Pyrolysis produces biochar as a co-product of bio-oil generation, offering suppliers dual revenue streams. However, the biochar fraction from fast pyrolysis typically carries lower fixed-carbon content than slow pyrolysis output. This tradeoff limits direct substitution in charge-carbon applications but creates viable supply for lower-specification uses such as supplemental carbon blending or feedstock for further upgrading into engineered grades.

Gasification, Torrefaction, and Hydrothermal Treatment address specific feedstock or product requirements that standard pyrolysis cannot optimize. Hydrothermal treatment in particular is relevant to high-moisture agricultural residues, expanding the usable feedstock base in regions where woody biomass is constrained. The Others category captures emerging hybrid conversion technologies. Together these routes serve as structural complements to slow pyrolysis-led supply rather than direct challengers to its dominant position.

Application Analysis

Carbon Injectant dominates with 35.6% due to direct integration into existing EAF injection infrastructure.

In 2025, Carbon Injectant held a dominant market position in the By Application segment of the Biochar for Electric Arc Furnace (EAF) Steelmaking Market, with a 35.6% share. Carbon injection into the EAF bath is a well-established operational step, and biochar-based injectants replace fossil coke fines within the same equipment and feed systems already installed at most plants. As per our research, carbon injection materials for EAF slag foaming require particle sizes between 0.5 mm and 1.0 mm, a specification that biochar processors must consistently meet to qualify for this application.

Recarburizer applications cover the addition of carbon to adjust steel chemistry after primary melting, a step that gives EAF operators granular control over final product grades. Biochar recarburizers must achieve high carbon purity with low sulfur and ash to avoid contaminating melt quality. This quality threshold creates a meaningful barrier for lower-grade biochar producers, concentrating supply for this segment among established converters with consistent pyrolysis operations.

Slag Foaming Agent and Insulating Material applications address specific process efficiency functions rather than primary carbon addition. Slag foaming reduces heat loss and improves energy efficiency within the furnace, creating a direct operating cost benefit for the mill. The Others category includes experimental and niche uses under active trial. These segments, while currently smaller, carry higher commercial value per tonne as they target process performance outcomes rather than commodity carbon replacement.

Key Market Segments

By Type of Biochar

- Wood-based Biochar

- Agricultural Waste-based Biochar

- Industrial Byproduct Biochar

- Engineered or Activated Biochar

By Production Technology

- Slow Pyrolysis

- Fast Pyrolysis

- Gasification

- Torrefaction

- Hydrothermal Treatment

- Others

By Application

- Carbon Injectant

- Recarburizer

- Slag Foaming Agent

- Insulating Material

- Others

Regional Analysis

Asia Pacific Dominates the Biochar for Electric Arc Furnace (EAF) Steelmaking Market with a Market Share of 43.5%, Valued at USD 21.0 Billion

Asia Pacific commands 43.5% of the global market, anchored by the region’s dominant share of EAF steelmaking capacity across China, Japan, South Korea, and India. China’s stated target of raising EAF output to 15% of national steel production creates a structural demand signal for biochar suppliers, even as the country’s current 10% EAF share reveals an execution gap that translates into near-term procurement opportunity for qualified carbon input providers.

Europe holds the second-largest regional position, driven by the EU Carbon Border Adjustment Mechanism and EU ETS allowance prices averaging EUR 73.43 per tCO₂e in 2025. German EAF plants alone generate approximately 570,000 tonnes of CO₂ annually from fossil carbon consumption, quantifying the abatement opportunity for biochar suppliers targeting the EU’s core steel-producing corridor. This emissions baseline gives biochar vendors a credible commercial argument for procurement conversations with export-oriented mills.

North America is an emerging but structurally important region, benefiting from dedicated government funding for steel decarbonization and a high share of EAF capacity in the US steel mix. In January 2026, CHAR Technologies advanced its Thorold Renewable Energy Facility from pilot to commercial production, establishing the first major biocarbon supply node targeting North American steelmakers. This infrastructure development shortens qualification timelines for US and Canadian mills considering fossil carbon displacement.

Latin America, the Middle East and Africa, and remaining Asia Pacific markets represent earlier-stage adoption zones where biomass availability and steel production overlap creates long-term supply development potential. Brazil and Australia stand out within this group given their agricultural and forestry residue bases. However, weaker carbon pricing frameworks and lower near-term EAF expansion rates place these regions outside the primary commercial window for the 2026 to 2028 period.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Drivers

The EU Carbon Border Adjustment Mechanism entered its definitive regime on 1 January 2026, covering iron and steel with mandatory embedded-emissions declarations tied to EU ETS certificate pricing. Average 2025 EU ETS auction prices reached EUR 73.43 per tCO₂e, with a six-month average of EUR 75.65 through May 2026. These price levels convert partial fossil carbon displacement from a sustainability gesture into a financially material procurement decision for export-oriented mills.

worldsteel reports average CO₂ intensity of approximately 0.70 tCO₂ per tonne for scrap-EAF routes and 1.43 tCO₂ per tonne for DRI-EAF routes, establishing the quantifiable abatement potential that biochar suppliers can package into procurement proposals. Importers above the 50-tonne CBAM threshold must operate within the certificate system, giving upstream mills a direct commercial reason to lower reported emissions intensity. This shifts biochar from a pilot input to an auditable decarbonization lever in EU-facing supply contracts.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Carbon-cost pass-through in EAF raw mix | +2.4% | EU core, UK follow-on, Türkiye export corridors, North America premium steel niches | Short term (≤ 2 years) |

| EAF route expansion lifts biogenic carbon demand | +2.1% | North America core, EU, India, Middle East, Türkiye | Medium term (2-4 years) |

| Scrap-DRI-EAF balancing increases reductant flexibility | +1.8% | US core, Gulf DRI hubs, India, Southern Europe | Medium term (2-4 years) |

| Trial validation of coke substitution de-risks adoption | +1.5% | Australia, North America, EU pilot clusters, APAC innovators | Short term (≤ 2 years) |

| Steel decarbonization funding accelerates qualification | +1.3% | US, Canada, EU, Australia | Short term (≤ 2 years) |

| Biomass-rich supply hubs improve delivered economics | +1.1% | Brazil, Australia, Southeast Asia, Nordics spill-over | Long term (≥ 4 years) |

Restraints

The most immediate restraint is the narrow availability of specification-compliant biochar for EAF charge-carbon or injection use. Steelmakers require material reaching approximately 80% carbon for EAF use, with particle-size windows around 10 mm for top charge and 3 to 5 mm for injection. These thresholds sharply limit usable output from early-stage pyrolysis networks, keeping delivered biochar costs structurally above incumbent fossil carbon on a per-effective-carbon basis.

High-profile commercial expansion projects in Australia are only now being funded and deployed in the 2025 to 2029 window rather than operating at mature industrial scale. This supply immaturity forces mills to over-order for blending tolerance and delays multi-site offtake contracts. Together these constraints justify an estimated -2.4 percentage-point drag on 2026-based CAGR until supply chains prove repeatability at industrial tonnage.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spec-grade biochar shortage | -2.4% | EU, Australia, Japan, Korea | Short term (≤ 2 years) |

| High EAF power-cost volatility | -1.9% | EU core, Turkey-linked corridors, India selective | Short term (≤ 2 years) |

| Scrap quality and carbon substitution limits | -1.6% | North America core, EU, APAC corridors | Medium term (2-4 years) |

| Biomass traceability and EUDR burden | -1.5% | EU, Southeast Asia supply links, LatAm export routes | Medium term (2-4 years) |

| Slow qualification and furnace retrofits | -1.8% | EU, Australia, North America | Medium term (2-4 years) |

| Weak steel spreads and CapEx hesitation | -1.7% | Europe, developed APAC, selected North America mills | Short term (≤ 2 years) |

Challenges

Certified feedstock volatility creates a recurring operational constraint for biochar producers targeting steel-grade output. World Steel notes that biomass deployment in steel depends on sustainably produced feedstock, full supply-chain accounting, and robust logistics chains from harvesting through char delivery. Annual variance in usable feedstock availability runs 8% to 15%, while incoming moisture swings reach 10 to 25 percentage points for residue-heavy baskets.

Procurement radius creep from roughly 150 to 200 km toward 300+ km once nearby residue pools are contracted adds 20 to 45 dollars per tonne of renewable carbon equivalent to delivered cost. This cost escalation can lower effective plant utilization by 5% to 12%. The market faces a modeled -1.6 percentage-point friction drag on achievable 2026 to 2030 growth until multi-basin sourcing and digital chain-of-custody systems mature across key supply regions.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Certified Feedstock Volatility | -1.6% | EU regulatory hubs, Australia, North America core, Brazil biomass belts | Medium term (2-4 years) |

| Carbon Quality Standardization Gap | -1.3% | APAC pilot clusters, EU specialty mills, Australia demonstration sites | Medium term (2-4 years) |

| Pyrolysis Scale-Up Reliability | -1.8% | Australia, North America emerging projects, EU innovation corridors | Long term (≥ 4 years) |

| EAF Process Integration Instability | -1.1% | Scrap-intensive EAF regions, India, Turkey, EU mini-mills | Short term (≤ 2 years) |

| Delivered Cost Competitiveness Swings | -1.5% | Europe high-power markets, import-dependent Asia, inland steel clusters | Medium term (2-4 years) |

| Auditability and LCA Burden | -0.9% | EU carbon-accounting markets, export-oriented producers, premium green steel chains | Long term (≥ 4 years) |

Opportunities

Building certified low-emissions input platforms for scrap-based EAF mills represents a high-value commercial pathway as OEM and construction buyers seek auditable emissions reductions. The Global Steel Climate Council is advancing a technology-agnostic emissions standard with third-party verification, while worldsteel has identified harmonized disclosure, labeling, and buyer offtake commitments as mechanisms to expand low-carbon steel demand. These frameworks create structured procurement channels for verified biochar suppliers.

CBAM and carbon-accounting regimes increasingly reward verified actual emissions over generic defaults, rewarding suppliers who embed digital mass-balance accounting and furnace-specific emissions factors into their product documentation. As per our research, even a 0.02 to 0.05 tCO₂e per tonne steel reduction that is credibly measured can create premium capture if it keeps a mill below a customer procurement threshold. Suppliers who function as certification infrastructure partners rather than material vendors can expand revenue per customer by 15% to 30% through data services, compliance support, and premium-sharing contracts.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Carbon-credit stacked supply | +2.6% | EU, Australia, North America | Short term (≤ 2 years) |

| Premium certified green steel inputs | +2.2% | EU core, Japan, South Korea | Short term (≤ 2 years) |

| Scrap-EAF mini-mill retrofit kits | +1.9% | North America core, EU, Turkey, India | Medium term (2-4 years) |

| Biomass-waste cluster roll-ups | +2.8% | Australia, Brazil, Southeast Asia, Nordics | Medium term (2-4 years) |

| CBAM export arbitrage platforms | +1.7% | India, MENA, Turkey to EU | Medium term (2-4 years) |

| Syngas-power integrated plants | +2.1% | Australia, Brazil, South Africa, India | Long term (≥ 4 years) |

Key Company Insights

In May 2025, CHAR Technologies signed a strategic partnership with The BMI Group and announced a C$2 million private placement to accelerate commercial biocarbon production at its Thorold Renewable Energy Facility. The BMI Group followed in July 2025 with an $8 million project-level equity investment in the same facility. These consecutive capital commitments signal that institutional investors are treating CHAR Technologies as a first-mover infrastructure play rather than a materials experiment.

Carbo Culture targets industrial-scale biochar production through a modular conversion platform designed for deployment across diverse biomass feedstock environments. In March 2026, the company received a €3.5 million Dutch grant to launch the ARC Middenmeer project in the Netherlands, directly targeting industrial decarbonization markets including green steel. This grant-backed European foothold positions Carbo Culture to qualify for EU-facing steel mill procurement programs ahead of competitors without established continental supply nodes.

Key Players

- Airex Energy

- Carbo Culture

- MYNO Carbon Corp.

- Karmanterra

- Envigas

- Pyrochar

- CharTechnologies

- SARRALLE

- Other Key Players

Recent Developments

- December 2025 – CHAR Technologies received a C$2.25 million non-repayable grant from the Government of Ontario to accelerate commercialization of low-carbon biocarbon pellets designed as a drop-in replacement for fossil carbon in steelmaking.

- January 2026 – The BMI Group reaffirmed an approximately $10 million commitment toward development of the Espanola Biocarbon Project, expanding future renewable carbon supply for metallurgical and steelmaking applications.

- March 2026 – Carbo Culture was awarded a €3.5 million Dutch grant to launch the ARC Middenmeer project in the Netherlands, supporting scale-up of its biochar production platform for industrial decarbonization markets including green steel.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 48.4 Billion |

| Forecast Revenue (2035) | USD 461.4 Billion |

| CAGR (2026-2035) | 25.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Type of Biochar (Wood-based Biochar, Agricultural Waste-based Biochar, Industrial Byproduct Biochar, Engineered or Activated Biochar); By Production Technology (Slow Pyrolysis, Fast Pyrolysis, Gasification, Torrefaction, Hydrothermal Treatment, Others); By Application (Carbon Injectant, Recarburizer, Slag Foaming Agent, Insulating Material, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Airex Energy, Carbo Culture, MYNO Carbon Corp., Karmanterra, Envigas, Pyrochar, CharTechnologies, SARRALLE, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |