Quick Navigation

Report Overview

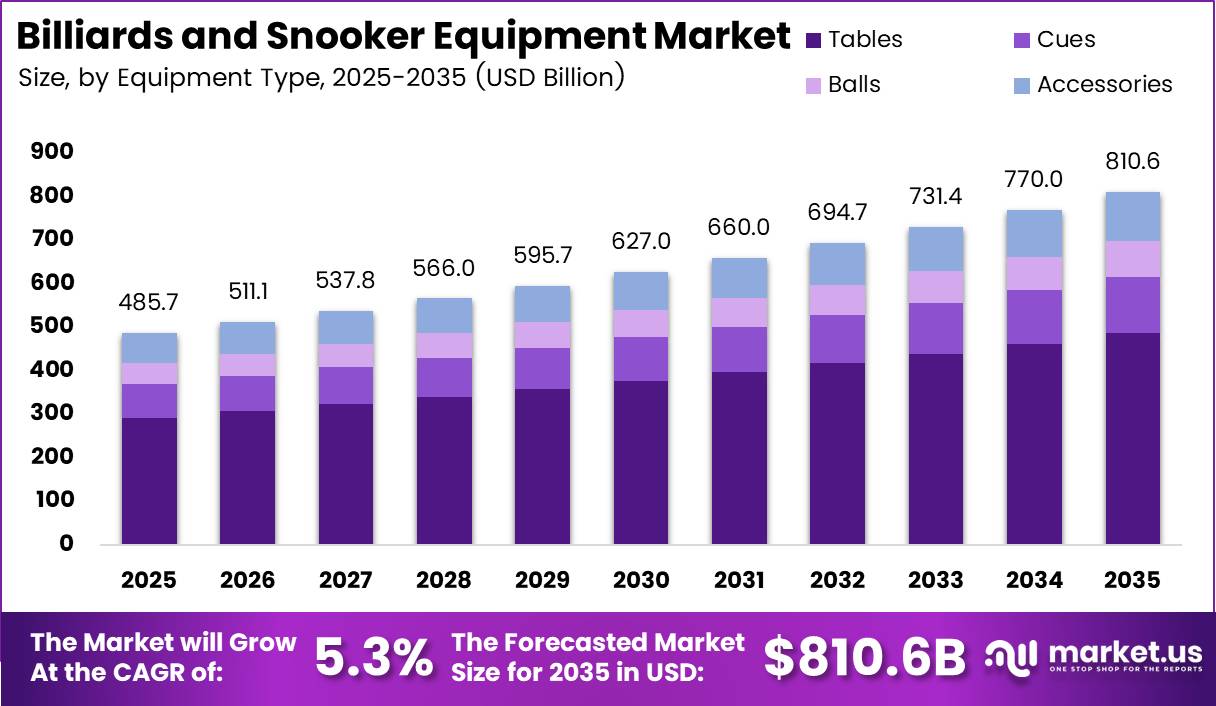

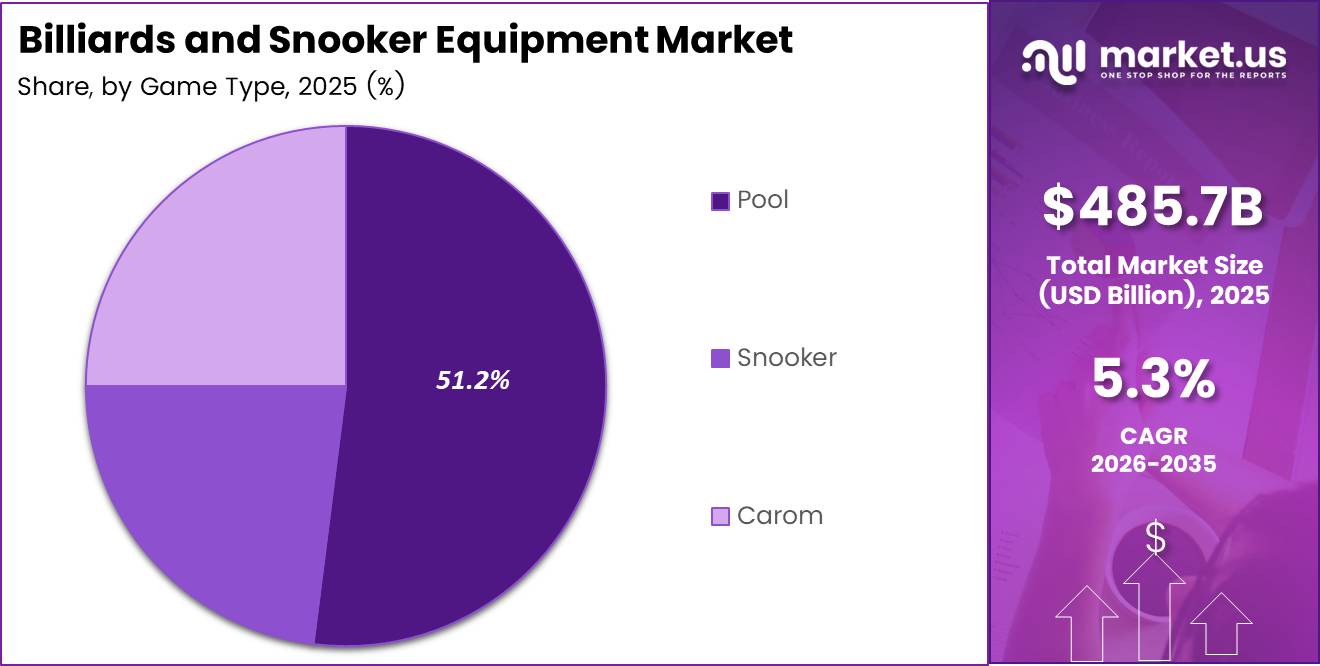

Global Billiards And Snooker Equipment Market size is expected to be worth around USD 810.6 Billion by 2035 from USD 485.7 Billion in 2025, growing at a CAGR of 5.3% during the forecast period 2026 to 2035.

The billiards and snooker equipment market covers tables, cues, balls, and accessories used in professional and recreational cue sports. This market spans offline retail outlets and online retail channels that serve clubs, homes, and commercial venues. Therefore, demand connects directly to participation levels across pool, snooker, and carom disciplines worldwide.

Key Takeaways

- Global billiards and snooker equipment market size is projected to reach USD 810.6 Billion by 2035 from USD 485.7 Billion in 2025.

- The market is expected to grow at a CAGR of 5.3% between 2026 and 2035.

- Tables dominate the By Equipment Type segment with a 60.1% share.

- Pool leads the By Game Type segment with a 51.2% share.

- Offline retail holds the largest By Facility Type share at 70.2%.

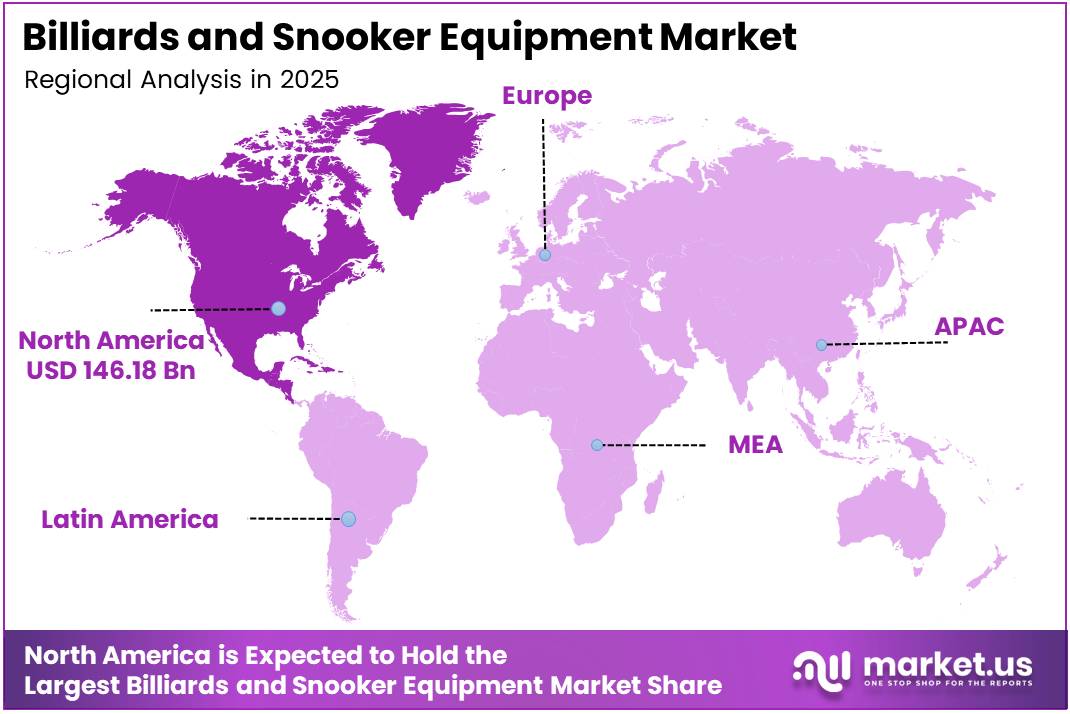

- North America dominates the regional landscape with a 30.1% share, valued at USD 146.18 Billion.

The American Poolplayers Association coordinates organized amateur competition across the United States, Canada, Japan, and Singapore. According to APA, the association counts more than 275,000 members. This scale creates a steady replacement cycle for cues, balls, and accessories among active league players.

Prize funding also supports equipment upgrades among competitive players. As reported by APA, the organization distributes nearly 2 Million dollars in guaranteed prize money each year. Consequently, competitive players reinvest winnings into higher grade cues and tournament ready equipment, sustaining premium segment demand.

Equipment Type Analysis

Tables dominates with 60.1% due to widespread commercial and residential installations.

In 2025, Tables held a dominant market position in the By Equipment Type segment of Billiards And Snooker Equipment Market, with a 60.1% share. Tables anchor both commercial venues and home installations, requiring higher unit values than other equipment categories. This structural weight makes tables the primary revenue driver for manufacturers. Therefore, table replacement cycles shape overall market revenue more than any other category.

Cues serve as the direct performance interface for players and see frequent replacement among competitive users. Cues represent 20.2% of the Equipment Type segment. This positions cues as a steady recurring revenue category tied closely to player skill progression and tournament participation.

Balls function as consumable equipment that wears through repeated commercial use. Balls hold 12.1% of the segment. Venues that host frequent play generate consistent reordering demand, supporting stable manufacturer volumes independent of new table sales.

Accessories complete the Equipment Type segment with a smaller but consistent contribution. Accessories account for 7.6% of total share. This category includes maintenance and support products that extend the usable life of tables, cues, and balls.

Game Type Analysis

Pool dominates with 51.2% due to broad amateur league participation.

In 2025, Pool held a dominant market position in the By Game Type segment of Billiards And Snooker Equipment Market, with a 51.2% share. Pool benefits from extensive league infrastructure across multiple countries. As reported by APA, the 2025 APA 8-Ball Classic attracted 883 players. This scale of organized amateur play sustains recurring cue and accessory purchases across the segment.

Snooker commands a smaller but high value share of the Game Type segment. Snooker holds 30.3% of total share. According to WST, the 2026 World Snooker Championship offered a total prize fund of £2,395,000. This professional prize scale drives demand for competition grade tables and cloth among clubs and academies.

Carom completes the Game Type segment with a smaller regional footprint. Carom accounts for 18.5% of total share. This format concentrates demand in specific regional markets, supporting niche equipment specifications rather than broad commercial volume.

Facility Type Analysis

Offline retail dominates with 70.2% due to hands-on equipment testing needs.

In 2025, Offline retail held a dominant market position in the By Facility Type segment of Billiards And Snooker Equipment Market, with a 70.2% share. Buyers prefer physical stores to test cue weight, table quality, and cloth texture before purchase. This hands-on preference limits fast online conversion for premium equipment. Consequently, specialty retailers with knowledgeable staff retain a structural advantage in this segment.

Key Market Segments

By Equipment Type

- Tables

- Cues

- Balls

- Accessories

By Game Type

- Pool

- Snooker

- Carom

By Facility Type

- Offline retail

- Online retail

Regional Analysis

North America Dominates the Billiards And Snooker Equipment Market with a Market Share of 30.1%, Valued at USD 146.18 Billion

North America leads through an established amateur league network and widespread commercial venue installations. The American Poolplayers Association operates organized competition across the United States and Canada, sustaining consistent equipment turnover. This structural depth supports both premium residential purchases and commercial table replacement cycles across the region.

Europe maintains strong cue sports infrastructure through governing frameworks such as the WPBSA coaching programme. Formal coaching pathways aligned with UK Coaching standards encourage structured equipment upgrades among developing players. This coaching led structure sustains demand for cues, cases, and maintenance accessories across European clubs.

Asia Pacific benefits from expanding federation activity and tournament hosting across China, India, and South Korea. Growing hosting infrastructure supports new venue installations and equipment procurement. This expansion positions the region as a fast developing base for commercial and academy level demand.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Market Dynamics

Market Opportunity Analysis - Online retail and emerging regions offer entry points beyond the dominant offline and North American base

Online retail remains underexploited within the Facility Type segment despite Offline retail holding 70.2% share. This gap signals room for digital first brands to build trust through virtual fitting tools and video demonstrations. New entrants that solve the testing barrier online can capture buyers currently locked into physical stores.

Carom holds the smallest Game Type share at 18.5%, leaving it underexploited relative to Pool and Snooker. This smaller base means less competitive crowding for specialized carom equipment makers. Instead of competing broadly, brands can build focused product lines for this concentrated player base.

Latin America shows developing infrastructure compared to North America’s 30.1% regional share. This gap creates room for equipment makers to establish early distribution relationships before larger competitors expand into the region. Consequently, first movers can secure venue partnerships ahead of broader market maturity.

Middle East and Africa shows emerging demand tied to tournament hosting rather than steady baseline sales. This uneven pattern means suppliers who align inventory with event calendars can capture concentrated procurement cycles. As a result, event focused supply strategies offer a practical entry path into this region.

Technology and Innovation Landscape - Carbon fiber cues and smart tables redefine equipment specification standards

Carbon fiber cue technology is rapidly replacing traditional maple cues among performance focused players. This material shift changes manufacturing specifications and pricing tiers across the cue category. Manufacturers that invest early in carbon fiber production can capture premium pricing before the shift becomes standard across the category.

Smart connected tables with integrated shot tracking and performance analytics are emerging within the premium equipment segment. This technology adds a data layer to practice and coaching sessions. Academies and serious players adopting these tables gain measurable feedback, creating a new premium price tier beyond standard table sales.

Coach discovery platforms are making structured instruction more accessible alongside the WPBSA coaching framework. Digital access to accredited coaches supports faster player progression through equipment upgrade stages. This connection between digital coaching access and physical equipment purchase creates a new channel for manufacturers to reach developing players.

Premium worsted cloth upgrades are becoming standard specification in mid tier commercial venues. This shift raises the baseline quality expectation across commercial installations. Venues upgrading cloth specification create recurring maintenance and re-clothing revenue for suppliers and certified technicians.

Drivers

Coaching pathway formalization pushes the cue sports equipment market forward by turning casual players into equipment owners. The WPBSA Coaching Programme runs three qualification levels aligned with UK Coaching standards, giving players a clear development path. As learners advance, they typically buy personal cues, cases, and maintenance accessories instead of sharing club gear.

This progression creates repeat purchasing opportunities as players move through multiple upgrade stages. Structured coaching also improves retention, keeping players active in the sport longer. Therefore, partnerships with coaches, academies, and governing bodies are becoming important sales and customer development channels for equipment brands.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tournament calendar expansion | +1.9% | UK; China; India; GCC; Europe corridors | Short term (≤ 2 years) |

| Coaching pathway formalization | +1.6% | UK; India; Europe; Commonwealth markets | Medium term (2-4 years) |

| Asia hosting and federation build-out | +1.8% | India; Southeast Asia; China; Middle East | Medium term (2-4 years) |

| Disability cue-sport integration | +1.2% | UK; Europe; North America; Australia | Medium term (2-4 years) |

| Amateur event participation density | +1.5% | U.S.; UK; India; Ireland | Short term (≤ 2 years) |

| Venue refresh and specification uplift | +1.4% | North America core; Europe; APAC urban clubs | Short term (≤ 2 years) |

Restraints

Urban space economics restrains the billiards and snooker equipment market because full size tables need substantial floor space beyond the table itself for cue movement. This requirement limits adoption in apartments, boutique venues, and mixed use spaces where floor area drives revenue. Cities such as Tokyo, Seoul, and Singapore often cannot fit standard table dimensions.

As a result, purchases are often limited by available space rather than buyer interest. Commercial venues may choose space efficient entertainment formats that generate more revenue per square foot instead. This means real estate economics place a direct ceiling on the growth of premium and full size table installations.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import cost layering | -1.3% | UK; EU import hubs; North America | Short term (≤ 2 years) |

| High install capex | -1.1% | Global clubs; hotels; bars; homes | Short term (≤ 2 years) |

| Manufacturing scale limits | -0.9% | India; SE Asia; emerging export corridors | Medium term (2-4 years) |

| Urban space economics | -0.8% | Japan; South Korea; EU cities; Tier-1 APAC | Long term (≥ 4 years) |

| Procurement standard gaps | -0.7% | Schools; academies; municipalities; clubs | Medium term (2-4 years) |

| Event-led demand concentration | -0.6% | India; UK; China; GCC host markets | Medium term (2-4 years) |

Challenges

Logistics and installation complexity challenges the billiards and snooker market because tables are heavy, precision built products that need specialized handling. A full size snooker table can weigh more than one tonne and includes multiple slate sections that must be transported and leveled with care. International shipments often involve 20 to 45 days of ocean transit plus customs clearance.

Skilled technicians must level the slate, stretch the cloth, and calibrate cushions to playing standards. Limited installer availability can delay revenue generation for venues waiting on new equipment. As a result, some clubs postpone table replacement due to the operational disruption involved.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Fragmented manufacturing and sourcing | -1.0% | India; China; SE Asia; EU import hubs | Medium term (2-4 years) |

| Logistics and install complexity | -0.9% | North America; Europe; APAC corridors | Medium term (2-4 years) |

| Venue spec and quality variance | -0.8% | Global clubs; academies; bars | Long term (≥ 4 years) |

| Inclusion and accessibility retrofits | -0.7% | Europe; UK; North America; Australia | Long term (≥ 4 years) |

| Tourism workforce pressure spill-over | -0.8% | Global tourism hubs; EU; India; Japan | Long term (≥ 4 years) |

| Digital-coaching and data gaps | -0.7% | Global; especially emerging cue markets | Medium term (2-4 years) |

Opportunities

Disability adapted product lines represent an underdeveloped opportunity as disability cue sports gain institutional support. In 2024, a formal Memorandum of Understanding was signed between international disability sport and disability cue sports organizations to expand participation pathways. Competitions already run across wheelchair, ambulant, intellectual disability, and visual impairment classifications.

Most commercial equipment portfolios still lack dedicated products for seated play and one handed cue assistance. Specialized solutions such as wheelchair accessible tables, lightweight cues, and cue guidance devices can meet these needs. Sports federations and rehabilitation centers frequently purchase for multiple participants, creating a distinct, low competition segment for certified adaptive equipment manufacturers.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Academy and school rollouts | +2.1% | India; UK; Middle East; Southeast Asia | Medium term (2-4 years) |

| Smart training equipment stacks | +1.8% | North America core; UK; China; South Korea | Short term (≤ 2 years) |

| Disability-adapted product lines | +1.4% | Europe; UK; North America; Australia | Medium term (2-4 years) |

| Tournament-hosting infrastructure | +1.9% | India; GCC; Southeast Asia; Eastern Europe | Medium term (2-4 years) |

| Home-premium compact formats | +1.6% | North America; Japan; South Korea; EU cities | Short term (≤ 2 years) |

| Equipment platform roll-ups | +2.0% | U.S.; UK; EU specialty retail; India | Long term (≥ 4 years) |

Key Company Insights

Brunswick Billiards strengthens its industry position through governance influence rather than product volume alone. In April 2025, the company’s Director of Product Development, Jacklyn Ady, was elected Chairman of the Billiard Congress of America Board. This role gives Brunswick early visibility into industry standards. As reported by WST, the 2026 World Snooker Championship winner received £500,000, a prize scale that shapes brand visibility across the professional events where established manufacturers compete for exposure.

Diamond Billiard Products, Inc. competes in a market shaped by global federation activity. As reported by WPA, 2,142 athletes competed across 76 international WPA sanctioned events during 2025. This scale of sanctioned competition creates consistent demand for tournament grade tables. Diamond’s competitive position rests on product specification credibility within this expanding sanctioned event calendar rather than confirmed regional distribution scale.

Key Players

- Brunswick Billiards

- Diamond Billiard Products, Inc.

- Riley Leisure

- Olhausen Billiard Manufacturing, Inc.

- Imperial International

- Berner Billiards

- Predator Group

- Beijing Xingpai Group

- Rasson Billiards Manufacturing Co., Ltd.

- Valley-Dynamo, Inc.

- Legacy Billiards

- American Heritage Billiards

- Chevillotte Billiards

- Billiards Breton

- Wiraka Pte Ltd

- Others

Recent Developments

- June 2025 – Predator Group and Pro Billiard Center announced a multi event World Championship Week in Bali, Indonesia, featuring the WPA Men’s World 8-Ball Championship, WPA Women’s World 10-Ball Championship, and the inaugural WPA Men’s World 10-Ball Doubles Championship.

- September 2025 – Taom Billiards became the Official Global Chalk Partner of the World Seniors Snooker Tour through a new three year agreement, expanding its presence across major international snooker events.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 485.7 Billion |

| Forecast Revenue (2035) | USD 810.6 Billion |

| CAGR (2026-2035) | 5.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Equipment Type (Tables, Cues, Balls, Accessories), By Game Type (Pool, Snooker, Carom), By Facility Type (Offline Retail, Online Retail), By Region (North America, Europe, Asia Pacific, Latin America, Middle East and Africa) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Brunswick Billiards, Diamond Billiard Products, Inc., Riley Leisure, Olhausen Billiard Manufacturing, Inc., Imperial International, Berner Billiards, Predator Group, Beijing Xingpai Group, Rasson Billiards Manufacturing Co., Ltd., Valley-Dynamo, Inc., Legacy Billiards, American Heritage Billiards, Chevillotte Billiards, Billiards Breton, Wiraka Pte Ltd, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |