Quick Navigation

- Report Overview

- Key Takeaways

- Product Type Analysis

- Formulation Type Analysis

- Packaging Type Analysis

- Application Analysis

- End User Analysis

- Distribution Channel Analysis

- Price Range Analysis

- Key Market Segments

- Regional Analysis

- Key Regions and Countries

- Market Dynamics

- Drivers

- Restraints

- Challenges

- Opportunities

- Key Company Insights

- Recent Developments

- Geopolitical Impact Analysis

- Report Scope

Report Overview

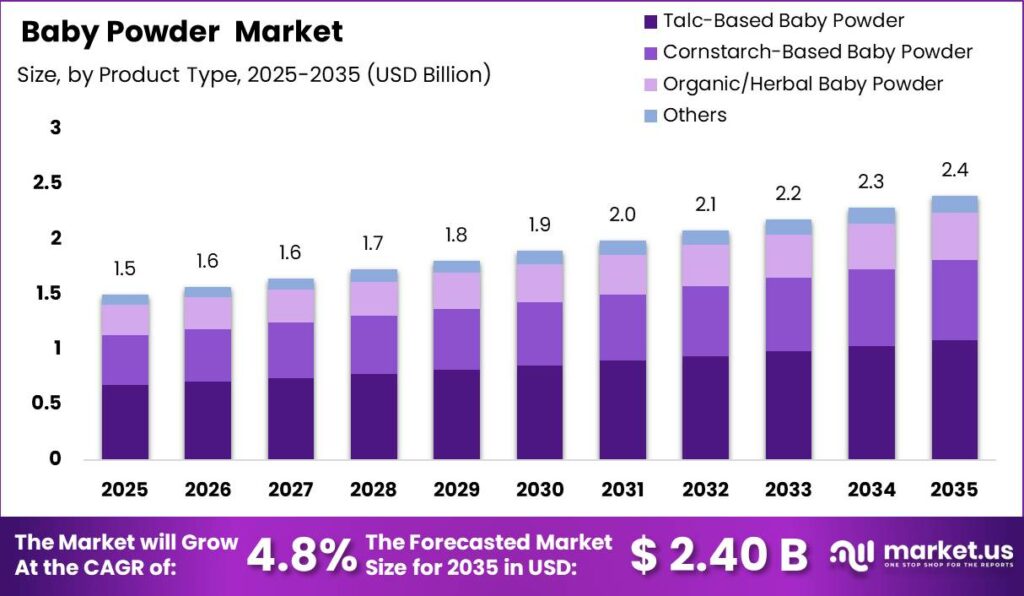

Global Baby Powder Market size is expected to be worth around USD 2.40 Billion by 2035 from USD 1.5 Billion in 2025, growing at a CAGR of 4.8% during the forecast period 2026 to 2035. This steady climb shows a category rebuilding trust after safety controversies. Brands that reformulate early will hold shelf space as older product forms exit regulated markets.

Baby powder covers absorbent skin-care powders used to keep infant skin dry and rash-free. The baby personal care structures this category by base material, format, and channel. Talc, cornstarch, and organic bases define product tiers, while shaker packs and sachets shape usage. Therefore, buyers now judge brands on formulation transparency, and clean-label positioning decides which suppliers win repeat purchases.

Key Takeaways

- Global Baby Powder Market reached USD 1.5 Billion in 2025 and will hit USD 2.40 Billion by 2035 at a CAGR of 4.8%.

- Talc-Based Baby Powder led product type with a 45.20% share in 2025.

- Fragranced Baby Powder held 52.70% of the formulation type segment.

- Shaker/Loose Powder dominated packaging with 61.40% share.

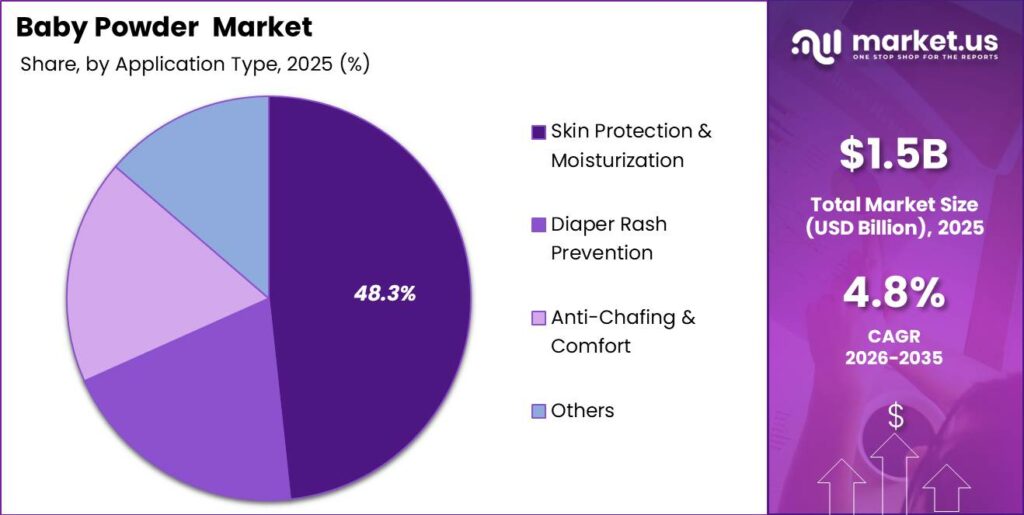

- Skin Protection and Moisturization led application with 48.30%.

- Household Consumers accounted for 92.60% of end users.

- Supermarkets and Hypermarkets led distribution with 34.80%.

- Mass Market held 53.90% of the price range segment.

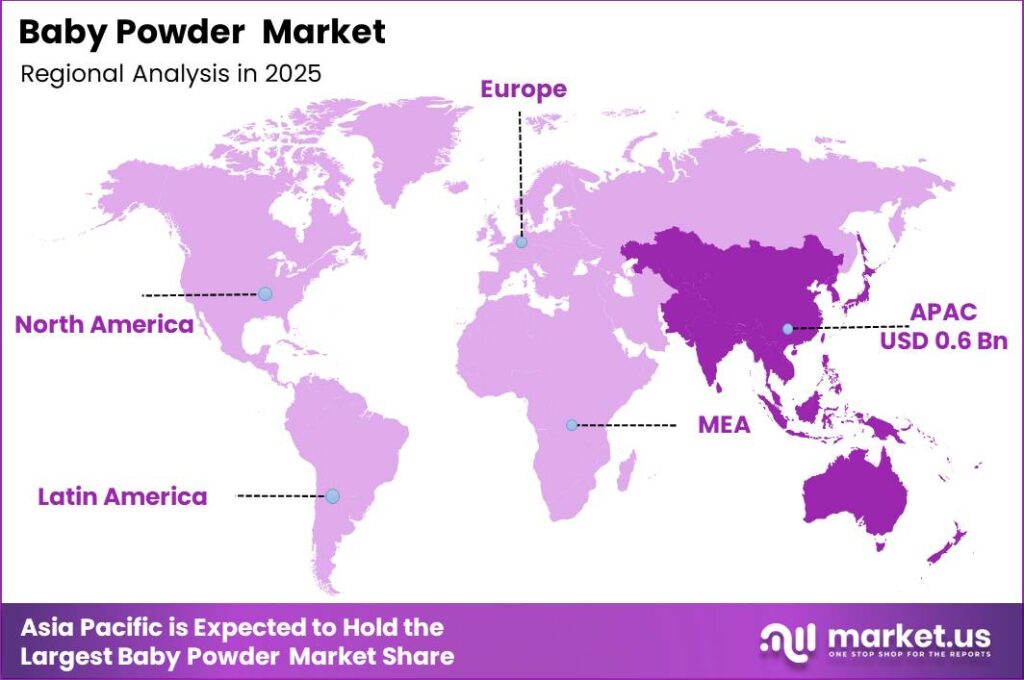

- Asia-Pacific dominated with a 40.30% share, valued at USD 0.6 Billion.

Government regulators now shape this market more than any single brand. As reported by the FDA, a proposed rule dated December 26, 2024 would require 100% batch-level asbestos testing for all talc-containing cosmetic products. This rule raises compliance costs for talc formulators. Consequently, mid-tier producers face reformulation or exit, opening shelf space for talc-free challengers that already meet the stricter testing bar.

Testing complexity adds a second entry barrier for smaller suppliers. Data from the FDA shows that 2 independent microscopy methods, Polarized Light Microscopy and Transmission Electron Microscopy, are required to confirm asbestos presence in talc cosmetic samples within the wider baby toiletries. This dual-method rule increases per-batch testing time and cost. Therefore, brands with cornstarch or organic bases avoid this burden entirely, sharpening their price and speed advantage in regulated markets.

Rising infant-care spending in Asia-Pacific links directly to product demand. Household purchasing frequency lifts volumes for diaper-rash prevention powders across the region. This creates a durable base of repeat buyers as first-time parents shift from unbranded to packaged SKUs. As a result, manufacturers that localize pricing and digital discovery capture early loyalty before premium players enter.

Product Type Analysis

Talc-Based Baby Powder dominates with 45.20% due to legacy trust and low commodity input cost.

In 2025, Talc-Based Baby Powder held a dominant market position in the By Product Type segment of Baby Powder Market, with a 45.20% share. According to the USGS, world talc and pyrophyllite mine production stayed near 7.7 million metric tons annually, keeping raw material cheap and widely available. This scale advantage lets talc brands undercut alternatives on price. However, tightening regulation means this lead will erode as reformulation accelerates.

Cornstarch-Based Baby Powder serves safety-conscious parents seeking inhalation-risk reduction and held 30.40% share within the baby skin care. Corn ranks among the largest global crops, with USDA reporting US output above 14 billion bushels per season. This wide feedstock supply supports rapid scale-up for reformulated SKUs. Therefore, brands switching to cornstarch gain a safety story that commands premium positioning without sacrificing raw material availability.

Organic and Herbal Baby Powder attracts premium buyers wanting clean labels and held 18.10% share, a fast-growing tier of the organic baby care products. ITC Trade Map records rising cross-border shipments of botanical cosmetic preparations under HS code 3304, reflecting export demand for natural formats. This trade momentum favors Indian and European herbal brands. Consequently, exporters that certify organic content can charge higher margins in Gulf and UK markets. The Others group holds the remaining 6.30% collectively.

Formulation Type Analysis

Fragranced Baby Powder dominates with 52.70% due to strong sensory preference among mass buyers.

In 2025, Fragranced Baby Powder held a dominant market position in the By Formulation Type segment of Baby Powder Market, with a 52.70% share. UN Comtrade data shows global trade in perfumed cosmetic powders growing steadily under HS 3304, with annual flows exceeding USD 30 Billion across all cosmetic categories. This scent-led demand keeps fragranced SKUs at the shelf front. Therefore, brands invest in signature scents to defend repeat purchase loyalty.

Fragrance-Free Baby Powder serves sensitive-skin and dermatologist-guided buyers and held 47.30% share, overlapping with the natural personal care products. The World Bank reports that atopic and irritant skin conditions affect roughly 20% of children globally, sustaining demand for additive-light formats. This medical need anchors a stable buyer base. Consequently, brands that pair fragrance-free claims with clinical evidence can shift from commodity pricing toward premium dermocosmetic tiers.

Packaging Type Analysis

Shaker/Loose Powder dominates with 61.40% due to easy controlled dispensing during application.

In 2025, Shaker/Loose Powder held a dominant market position in the By Packaging Type segment of Baby Powder Market, with a 61.40% share. UNIDO industrial output data shows plastic packaging manufacturing growing across Asian hubs, supporting low-cost shaker container supply at scale. This packaging familiarity keeps the format entrenched. Therefore, brands standardize on shaker packs to control unit cost and retain consumer habit.

Pressed Powder serves travel and premium buyers seeking spill-free portability and compact form. Customs databases record rising unit shipments of compact cosmetic cases under HS 9616, signaling steady demand for portable formats. This convenience angle supports higher price points. Consequently, premium brands use pressed formats to differentiate on the digital shelf.

Sachets and Travel Packs target price-sensitive and single-use buyers in emerging markets. National statistical offices in India and Indonesia report that sachet-format personal care drives over 30% of rural units sold. This low-entry pricing widens trial among first-time buyers. As a result, brands use sachets to convert unbranded users before upselling larger SKUs.

Application Analysis

Skin Protection and Moisturization dominates with 48.30% due to daily preventive infant hygiene routines.

In 2025, Skin Protection and Moisturization held a dominant market position in the By Application segment of Baby Powder Market, with a 48.30% share. The World Bank records over 130 million annual global births, creating a large recurring base for daily skin-care use. This steady birth volume anchors demand. Therefore, brands that position powder as a daily routine essential secure predictable repeat sales.

Diaper Rash Prevention serves parents managing common infant skin irritation across climates. FAO and World Bank data link tropical humidity zones to higher dermatitis incidence in South and Southeast Asia. This climate factor sustains medical-use demand in high-birth regions. Consequently, brands that market rash-prevention claims gain traction in tropical markets.

Anti-Chafing and Comfort products broaden use into older children and active daily wear across the Body Care Products Market. Retail scanner data from national statistics bodies shows multifunctional powders gaining share in urban baskets. This wider use extends volume beyond infants. As a result, brands unlock adjacent buyers, with the Others group holding the remaining application share collectively.

End User Analysis

Household Consumers dominate with 92.60% due to routine at-home infant care use.

In 2025, Household Consumers held a dominant market position in the By End User segment of Baby Powder Market, with a 92.60% share, anchoring the broader baby cosmetics market. The World Bank estimates over 2 billion households globally, with a large share including young children. This vast home base drives most unit volume. Therefore, brands prioritize retail and e-commerce reach over institutional supply channels.

Hospitals and Maternity Clinics serve newborn care within controlled clinical settings. WHO facility data shows over 80% of births in developed regions occur in institutions, creating steady clinical demand. This channel favors trusted, tested formulations. Consequently, brands that win hospital trials gain credibility that later lifts household retail sales.

Distribution Channel Analysis

Supermarkets and Hypermarkets dominate with 34.80% due to bulk visibility and instant purchase convenience.

In 2025, Supermarkets and Hypermarkets held a dominant market position in the By Distribution Channel segment of Baby Powder Market, with a 34.80% share. National retail census data shows modern grocery formats operating over 50,000 large outlets across Asia-Pacific. This physical scale keeps powder within easy reach. Therefore, brands compete hard for shelf placement in these high-traffic formats.

Pharmacies and Drug Stores serve safety-focused buyers who trust regulated retail advice within the Personal Care Products. National pharmacy registries in India count over 900,000 licensed outlets, giving powder brands deep trusted reach. This credibility supports premium and clinical SKUs. Consequently, dermatologist-endorsed brands prioritize pharmacy listings to justify higher prices.

Online Retail enables rapid comparison and direct-to-consumer discovery of new formats. ITU reports Asia-Pacific internet penetration above 60%, expanding digital baby-care access fast. This reach favors D2C launches. Specialty Baby Stores hold the remaining share collectively, serving focused premium buyers who value curated assortments.

Price Range Analysis

Mass Market dominates with 53.90% due to affordability across high-volume emerging economies.

In 2025, Mass Market held a dominant market position in the By Price Range segment of Baby Powder Market, with a 53.90% share. IMF data shows most global births occur in economies with per-capita income under USD 10,000, anchoring demand at accessible price points. This income reality keeps mass pricing central. Therefore, brands protect volume by holding entry-level tiers stable.

Premium products target higher-income parents seeking clean-label and clinical assurance. World Bank income data shows a growing global middle class crossing PPP USD 5,000 yearly, lifting willingness to trade up. This shift supports margin-rich SKUs. Consequently, brands invest in premium tiers to capture rising urban spend, while Economy holds the remaining share collectively.

Key Market Segments

By Product Type

- Talc-Based Baby Powder

- Cornstarch-Based Baby Powder

- Organic/Herbal Baby Powder

- Others

By Formulation Type

- Fragranced Baby Powder

- Fragrance-Free Baby Powder

By Packaging Type

- Shaker/Loose Powder

- Pressed Powder

- Sachets and Travel Packs

By Application

- Skin Protection and Moisturization

- Diaper Rash Prevention

- Anti-Chafing and Comfort

- Others

By End User

- Household Consumers

- Hospitals and Maternity Clinics

By Distribution Channel

- Supermarkets and Hypermarkets

- Pharmacies and Drug Stores

- Online Retail

- Specialty Baby Stores

By Price Range

- Mass Market

- Premium

- Economy

Regional Analysis

Asia-Pacific Dominates the Baby Powder Market with a Market Share of 40.30%, Valued at USD 0.6 Billion

Asia-Pacific leads the Baby Powder Market with a 40.30% share, valued at USD 0.6 Billion in 2025. High birth cohorts and rising middle-class spending in India, Indonesia, and the Philippines drive this scale. This large base of first-time branded buyers supports durable volume growth. Therefore, manufacturers that localize pricing and quick-commerce listings capture early loyalty across non-metro geographies.

North America and Europe grow through talc-free reformulation and premium clinical positioning. Regulatory scrutiny in these regions pushes buyers toward cornstarch and organic formats. This transition destroys legacy demand while opening a premium clean-label tier. Consequently, brands that lead with tested, dermatologist-backed SKUs gain the fastest margin growth in these mature markets.

Latin America and Middle East and Africa hold the remaining regional share collectively. Modern trade expansion across Nigeria, Kenya, and Brazil brings branded powder to new households. This retail buildout converts unbranded users into repeat buyers. As a result, early movers who invest in distribution now secure defensible positions before competition intensifies.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Market Dynamics

Market Opportunity Analysis - Underserved premium tiers and emerging regions offer entry points for new players

Organic and Herbal Baby Powder stays underexploited at just 18.10% of product type share. Most demand still sits in talc and commodity cornstarch, leaving botanical positioning open for export-focused brands. This gap favors Indian and European herbal makers targeting Gulf and UK buyers. Therefore, brands that certify clean-label content now can claim premium space before larger players crowd in.

Online Retail remains under-penetrated versus supermarkets holding 34.80% of distribution across the wider Baby Products Market. Digital channels enable fast comparison and D2C discovery that physical formats cannot match. This creates room for direct-to-consumer brands to bypass legacy shelf gatekeepers. Consequently, early digital-first entrants can build loyal subscriber bases in price-sensitive markets before incumbents scale online.

Middle East and Africa sits in the remaining regional share behind Asia-Pacific’s 40.30% lead. Modern trade buildout across Nigeria, Kenya, and Ghana brings branded powder to first-time buyers. This retail expansion converts unbranded users into repeat purchasers. As a result, early movers who invest in distribution now secure defensible share before competition intensifies across these markets.

Premium price tiers stay open beyond Mass Market’s 53.90% dominance. Rising urban incomes lift willingness to pay for clinical and clean-label assurance. This shift lets brands escape commodity price wars with differentiated positioning. Instead of chasing volume alone, new entrants can build margin-rich premium lines aimed at higher-income parents.

Technology and Innovation Landscape - Reformulation science and format innovation redefine competitive edges

Cornstarch reformulation stands as the category’s default innovation direction today. Brands replace talc with cornstarch to cut inhalation risk while keeping moisture control. This shift demands new stability testing and packaging redesign per SKU. Therefore, manufacturers with in-house formulation labs move faster than those relying on outsourced development, gaining first-mover shelf advantage.

Alternative starch bases like arrowroot, rice, and tapioca extend innovation options. These functional bases need 12 to 18 months of sensory validation and stability qualification before launch. This lead time rewards early investment in diversified sourcing. Consequently, brands that qualify multiple bases now protect supply and reduce dependence on volatile cornstarch pricing.

Hybrid powder-cream formats introduce multifunctional innovation for premium buyers. These formats reduce airborne particles while preserving moisture-control performance. This engineering appeals to safety-focused parents seeking modern textures. As a result, brands that master hybrid formulation unlock differentiated positioning that commodity powders cannot match on the digital shelf.

Clinical dossier development represents the most defensible innovation investment. A randomized dermatitis study costs USD 120,000 to 350,000 over a multi-year timeline. This barrier blocks commodity private-label makers while suiting capitalized brands. Therefore, firms completing clinical validation early build credibility moats that justify premium pricing for years.

Drivers

Rising middle-class birth cohorts push branded baby powder demand across Asia-Pacific. India registered over 23 million live births in fiscal year 2024 to 2025, Indonesia about 4.5 million, and the Philippines about 1.7 million. As household incomes cross the PPP USD 5,000 to USD 10,000 threshold, families shift from unbranded loose powder to packaged SKUs. This first-time brand entry event shows strong retention, rewarding early movers.

Organized retail penetration widens branded reach in non-metro India fast. Baby personal care penetration in Tier-2 and Tier-3 cities grew from about 28% in 2022 to over 41% in 2025. Quick-commerce delivery windows under 30 minutes placed branded powder within reach of new parents. Therefore, brands that win first-listing prominence convert informal buyers at margins near 52% to 65%.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Middle-Class Birth Cohorts & Organized Retail Adoption in Asia-Pacific | +1.7% | India, Indonesia, Vietnam, Bangladesh, Philippines | Short term (≤ 2 years) |

| Accelerating Shift to Talc-Free & Cornstarch-Based Premium Formulations | +1.2% | North America, Europe, Urban India, Australia, Japan | Short term (≤ 2 years) |

| Millennial & Gen Z Parental Premiumization of Daily Baby Hygiene Spend | +0.8% | United States, Western Europe, Urban India, China, Gulf States | Short term (≤ 2 years) |

| E-Commerce & D2C Channel Expansion Enabling Premium SKU Discovery | +0.5% | India, China, United States, Southeast Asia | Short term (≤ 2 years) |

| Dermatitis & Diaper Rash Prevalence Sustaining Medical-Use Baby Powder Demand | +0.3% | Global, acute in tropical climates — India, Southeast Asia, Sub-Saharan Africa | Medium term (2–4 years) |

Restraints

Talc safety litigation and regulatory bans freeze conventional baby powder sales. The FDA advanced a proposed talc ban into formal rulemaking in 2024 under the Modernization of Cosmetics Regulation Act. Health Canada classified talc as toxic, triggering a mandatory 24-month phase-out. This pricing-in of prohibition drives early shelf delistings, forcing brands to reformulate before formal effective dates.

Reformulation costs strain mid-tier and private-label producers heavily. Talc accounted for an estimated 55% to 65% of baby powder formulations by volume as recently as 2020. Producers face reformulation costs of USD 80,000 to USD 250,000 per SKU or market exit. Consequently, gross margins compress by an estimated 300 to 500 basis points during the forced transition cycle.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talc Safety Litigation & Regulatory Bans Freezing Conventional Baby Powder Sales | -2.2% | United States, Canada, European Union, Australia | Short term (≤ 2 years) |

| Declining Birth Rates in High Per-Capita Spending Developed Markets | -0.7% | South Korea, Japan, Germany, Italy, United States | Long term (≥ 4 years) |

| Raw Material Cost Inflation for Cornstarch & Specialty Botanical Alternatives | -0.4% | Global, concentrated in North America & European manufacturing | Short term (≤ 2 years) |

| Pediatric Guidelines Discouraging Routine Powder Use Near Infant Airway | -0.3% | United States, United Kingdom, Canada, Australia | Medium term (2–4 years) |

| Import Tariff Disruptions on Packaged Baby Personal Care SKUs | -0.2% | United States, European Union | Short term (≤ 2 years) |

Challenges

Cornstarch supply volatility strains the reformulated baby powder category. The litigation-driven shift to cornstarch tied the category to a crop also demanded by food, bioplastics, and bio-ethanol makers. Food-grade cornstarch costs about 2.5 to 3.5 times more per kilogram than the talc it replaces. This input pressure compresses margins by an estimated 200 to 350 basis points.

Sourcing competition forces long-term formulation diversification. Manufacturers operate on 60 to 90 day raw material buffers that cannot absorb spot spikes over 15% to 20%. Alternative bases like arrowroot and tapioca need 12 to 18 months of validation before launch. Therefore, brands adopting hedging and co-operative procurement now protect supply during volatile crop years ahead.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Cornstarch Supply Volatility & Sourcing Competition | -0.6% | Global, most acute in North America & Europe manufacturing hubs | Medium term (2–4 years) |

| Counterfeit & Adulterated Powder Penetration | -0.5% | India, Southeast Asia, Middle East, Sub-Saharan Africa | Long term (≥ 4 years) |

| Multi-Jurisdiction Cosmetics Labeling Fragmentation | -0.4% | Global cross-border exporters serving EU, US, Gulf, India markets | Medium term (2–4 years) |

| Consumer Distrust Spillover from Talc to Category | -0.3% | United States, Europe, Urban India, Australia | Short term (≤ 2 years) |

| Private Label Price Compression in Mass Retail | -0.2% | United States, Europe, India | Long term (≥ 4 years) |

Opportunities

Clinically positioned talc-free powder opens a premium white space. Most talc-free SKUs launched between 2022 and 2025 sit at commodity prices with little differentiation. Dermo-positioned clinical powders retail at USD 14 to 28 per 200g versus USD 4 to 8 for mass formats. This 200% to 400% premium rewards brands that invest in clinical claims early.

Clinical dossiers create a defensible moat for first movers. A randomized study on dermatitis reduction needs about USD 120,000 to 350,000 over a 12 to 24 month timeline. This cost blocks commodity private-label makers but suits capitalized D2C brands. Therefore, gross margins near 62% to 72% reward brands completing dossiers in the 2026 to 2028 window.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Clinically Positioned Talc-Free & Dermatologist-Endorsed Premium Powder Segment | +1.3% | United States, Germany, France, Japan, Urban India, Australia | Medium term (2–4 years) |

| Herbal & Ayurvedic Baby Powder Export Positioning in International Markets | +0.7% | GCC, United Kingdom, United States, Southeast Asia (Indian-origin brands) | Medium term (2–4 years) |

| Hybrid Powder-Cream Multifunctional Format Innovation | +0.5% | United States, Europe, Urban India, South Korea | Long term (≥ 4 years) |

| Subscription & Auto-Replenishment Model for Baby Hygiene Essentials | +0.4% | United States, Europe, India, Australia | Medium term (2–4 years) |

| Sub-Saharan Africa Branded Powder Market Penetration via Modern Trade | +0.3% | Nigeria, Kenya, Ethiopia, Tanzania, Ghana | Long term (≥ 4 years) |

Key Company Insights

Johnson & Johnson faces heavy structural risk in this market from unresolved talc litigation. As reported by Reuters, over 67,000 talc-related lawsuits were active against the company as of the 2025 reporting period. In June 2024, a coalition of 43 US state attorneys general reached a USD 700 Million settlement over talc marketing. This legal weight pushes the firm toward pharmaceutical pivots and away from consumer powder.

P&G holds a strategic advantage through scale and clean-label reformulation depth. The company leverages broad retail reach and trusted brand equity to defend shelf space during the category’s talc-free transition. This positioning lets it convert safety-conscious parents without the legacy litigation drag rivals carry. Consequently, its ability to fund reformulation at scale creates a durable edge over smaller mid-tier competitors.

Key Players

- Johnson & Johnson

- P&G (Procter & Gamble)

- Himalaya Wellness Company

- Mustela

- The Honest Company

- Chicco (Artsana Group)

- Mothercare plc

- California Baby

- Pigeon Corporation

- Dabur India Ltd.

- Weleda AG

- Kushies Baby

- Burt’s Bees Baby

- Little Remedies

- Baby Dove (Unilever)

Recent Developments

- November 2025: Johnson & Johnson completed the acquisition of Halda Therapeutics for approximately USD 3.05 Billion, strengthening its pharmaceutical pipeline after exiting most talc-based consumer products.

Geopolitical Impact Analysis

According to the WTO, global merchandise trade growth slowed to about 2.7% in recent cycles as tariff barriers rose. Baby powder makers sourcing talc from China and packaging from Asian hubs face added import costs. US Section 301 tariffs on Chinese goods reached up to 25% on many inputs. Therefore, brands reroute sourcing toward India and domestic suppliers to protect margins during trade disputes.

As reported by the World Shipping Council, Red Sea rerouting added 10 to 14 days to many Asia-to-Europe transit lanes. This delay raises freight costs for packaged baby care shipments moving between manufacturing hubs and Western retail. The IEA notes energy price swings above 20% further lift plastic packaging input costs. Consequently, brands build regional buffer stock and near-shore packaging to limit distribution disruption.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.5 Billion |

| Forecast Revenue (2035) | USD 2.40 Billion |

| CAGR (2026-2035) | 4.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Talc-Based Baby Powder, Cornstarch-Based Baby Powder, Organic/Herbal Baby Powder, Others), By Formulation Type (Fragranced Baby Powder, Fragrance-Free Baby Powder), By Packaging Type (Shaker/Loose Powder, Pressed Powder, Sachets and Travel Packs), By Application (Skin Protection and Moisturization, Diaper Rash Prevention, Anti-Chafing and Comfort, Others), By End User (Household Consumers, Hospitals and Maternity Clinics), By Distribution Channel (Supermarkets and Hypermarkets, Pharmacies and Drug Stores, Online Retail, Specialty Baby Stores), By Price Range (Mass Market, Premium, Economy) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Johnson & Johnson, P&G (Procter & Gamble), Himalaya Wellness Company, Mustela, The Honest Company, Chicco (Artsana Group), Mothercare plc, California Baby, Pigeon Corporation, Dabur India Ltd., Weleda AG, Kushies Baby, Burt’s Bees Baby, Little Remedies, Baby Dove (Unilever) |

| Customization Scope | Customization for segments, region / country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License | Multi-User License (Up to 5 Users) | Corporate Use License (Unlimited User and Printable PDF) |