Quick Navigation

Report Overview

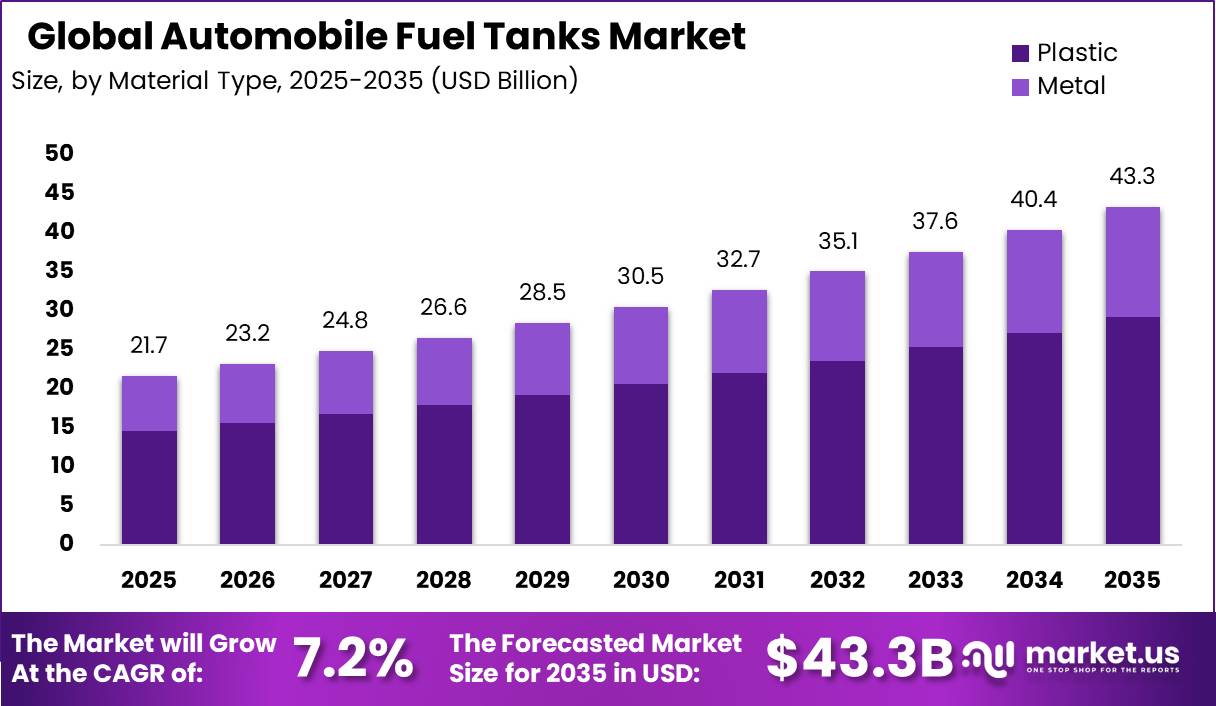

Global Automobile Fuel Tanks Market size is expected to be worth around USD 43.3 Billion by 2035 from USD 21.7 Billion in 2025, growing at a CAGR of 7.2% during the forecast period 2026 to 2035. This trajectory reflects sustained demand from vehicle production growth, emissions compliance investment, and a parallel shift toward hybrid-compatible tank architectures.

The automobile fuel tanks market covers the design, manufacture, and supply of onboard fuel storage systems fitted to passenger cars, light commercial vehicles, and heavy commercial vehicles. These systems span plastic and metal tank types across capacity ranges below 45 L, between 45 L and 75 L, and above 75 L. This means buyers include OEMs sourcing original-fit solutions and aftermarket channels supplying replacement units.

Key Takeaways

- Market size reached USD 21.7 Billion in 2025 and is forecast to reach USD 43.3 Billion by 2035.

- The market grows at a CAGR of 7.2% during 2026 to 2035.

- By Capacity Type, the 45 L–75 L segment dominates with a 48.6% share.

- By Material Type, Plastic tanks lead with a 67.4% share.

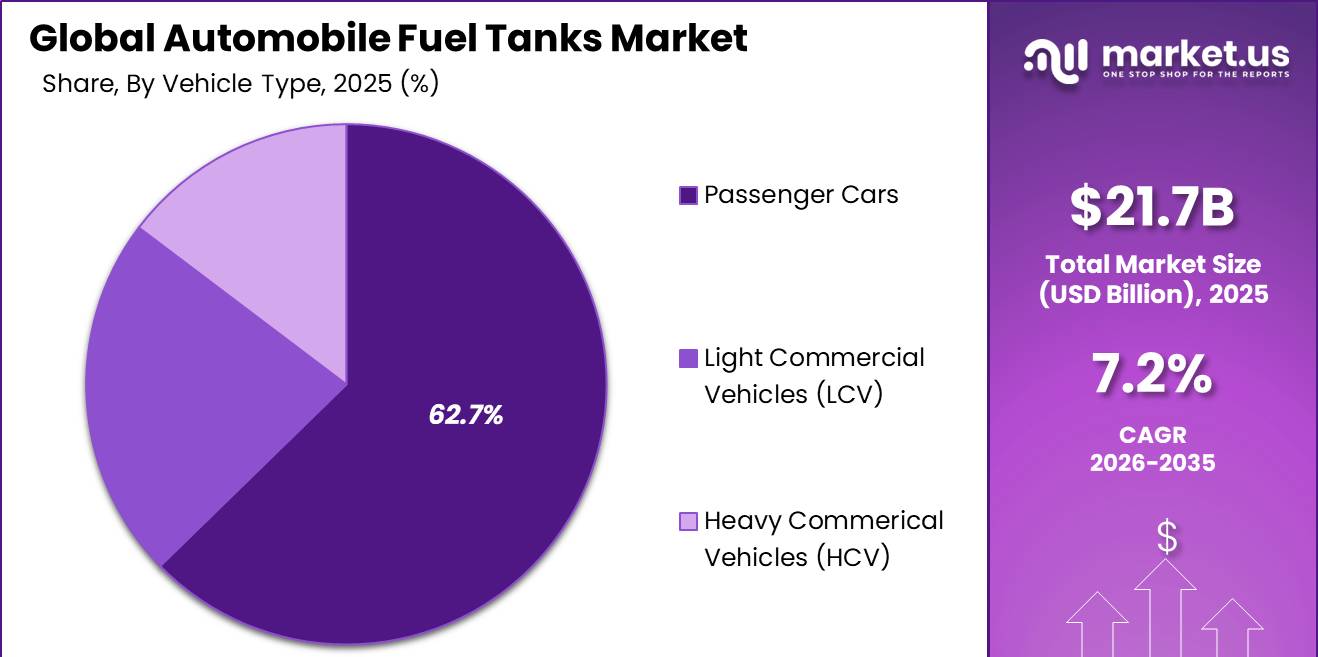

- By Vehicle Type, Passenger Cars account for 62.7% of market share.

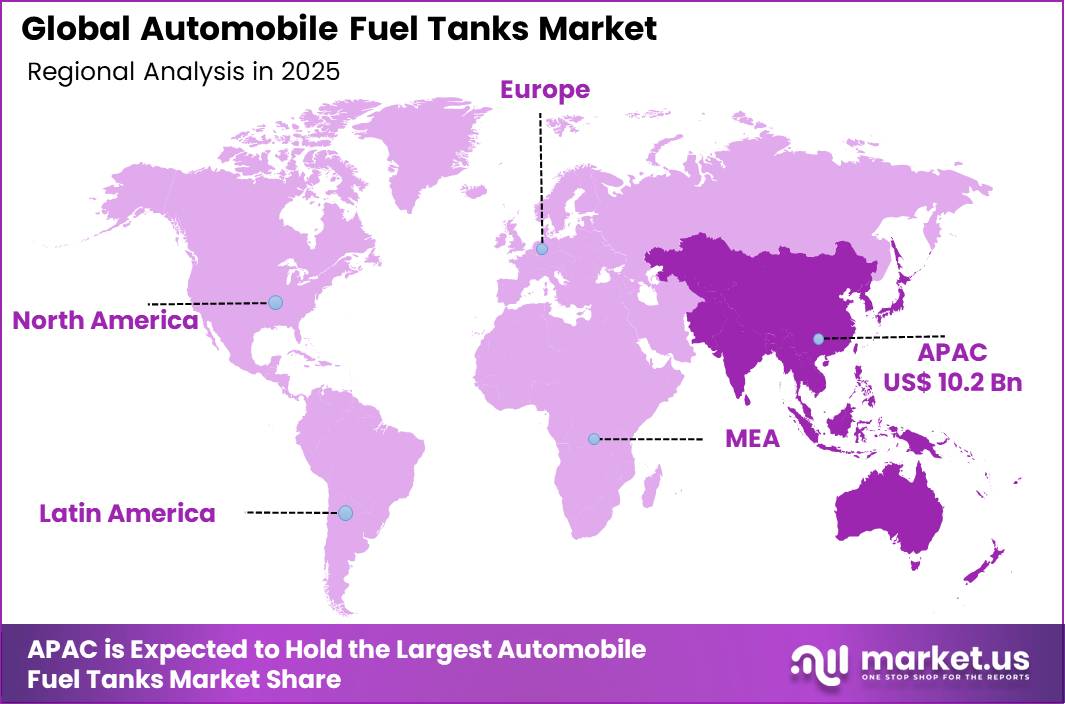

- Asia-Pacific is the dominant region with a 46.82% market share.

Emissions compliance is reshaping tank design requirements across key automotive markets. According to the US EPA, fuel tanks and fuel systems must meet strict hydrocarbon permeation limits, pushing manufacturers toward advanced multilayer barrier constructions. As a result, suppliers face higher engineering costs but also command stronger pricing power in regulated markets where compliance capability is a barrier to entry.

Ethanol blending mandates are expanding the addressable market for chemically resistant fuel tank designs. Data from the US Energy Information Administration shows more than 98% of US gasoline contains ethanol, creating baseline demand for ethanol-compatible tanks across the entire domestic vehicle parc. The US EPA has also authorized expanded summer sales of E15 gasoline in recent periods, broadening the use case for tanks rated above the standard E10 threshold.

Regulatory approvals are extending ethanol compatibility requirements to a wider vehicle population. E15 gasoline is approved for use in model year 2001 and newer light-duty vehicles in the United States, covering the vast majority of vehicles currently on US roads. This signals a structural shift toward biofuel-rated fuel storage as an engineering standard rather than a premium feature, which expands procurement volumes for compliant tank systems across all vehicle segments.

Capacity Type Analysis

45 L–75 L dominates with 48.6% due to alignment with mainstream passenger car platforms.

In 2025, the 45 L–75 L segment held a dominant market position in the By Capacity Type segment of the Automobile Fuel Tanks Market, with a 48.6% share. This range aligns directly with the fuel system requirements of mainstream passenger cars and entry-level SUVs, which together form the largest share of global vehicle output. Suppliers that optimize blow-molding tooling and barrier-layer stacks for this capacity range capture the highest volume throughput in the market.

Less than 45 L tanks serve compact and subcompact vehicle platforms, particularly those produced for high-density urban markets in Asia and Latin America. As vehicle production in India and ASEAN economies continues to expand, compact-capacity tank demand represents a volume-growth corridor that cost-focused regional suppliers are well positioned to address. E10 gasoline is sold in all 50 US states, which means compact tanks fitted to US-market small cars must still meet full ethanol-compatibility requirements regardless of their size.

Greater than 75 L tanks are engineered for full-size SUVs, pickup trucks, and heavy commercial vehicles requiring extended operating range between refueling stops. According to the IEA, SUVs accounted for 48% of global car sales in 2023, the highest share ever recorded. This structural shift in consumer preference drives sustained demand for high-capacity multi-layer tank configurations and creates pricing leverage for suppliers with certified large-format blow-molding capability. In January 2025, TI Fluid Systems announced it was adapting blow-molded plastic fuel tank technologies specifically for hybrid vehicles, reflecting active engineering investment in this transition.

Material Type Analysis

Plastic dominates with 67.4% due to weight reduction and regulatory-driven barrier-layer advantages.

In 2025, Plastic held a dominant market position in the By Material Type segment of the Automobile Fuel Tanks Market, with a 67.4% share. Plastic tanks offer up to 40% weight reduction compared to steel alternatives, directly improving vehicle fuel efficiency and supporting OEM compliance with fleet-average CO2 targets. This weight advantage makes plastic tanks the default engineering choice for passenger car and light commercial vehicle platforms globally.

Metal tanks retain relevance in applications where structural durability, puncture resistance, or extreme temperature performance outweigh the weight penalty. Heavy commercial vehicles and off-highway equipment represent the primary application base for metal fuel tanks. This means metal tank suppliers face a structurally narrowing addressable market in passenger segments while preserving volume in commercial and industrial categories where plastic cannot yet fully substitute.

Vehicle Type Analysis

Passenger Cars dominate with 62.7% due to highest global vehicle production and sales volumes.

In 2025, Passenger Cars held a dominant market position in the By Vehicle Type segment of the Automobile Fuel Tanks Market, with a 62.7% share. Global BEV and PHEV sales exceeded 17 million units in 2024, which signals a gradual shift away from pure internal combustion powertrains. However, the majority of passenger car output still requires a conventional or hybrid fuel tank, sustaining high absolute procurement volumes for fuel system suppliers through this transition period.

Light Commercial Vehicles (LCV) represent a structurally stable demand base for mid-capacity fuel tanks tied to last-mile delivery, municipal services, and light construction fleets. LCV fleet operators prioritize range, uptime, and low total cost of ownership, making tank durability and ethanol compatibility critical procurement criteria. Suppliers offering certified ethanol-rated tanks with extended warranty coverage hold a pricing advantage in commercial fleet procurement channels.

Heavy Commercial Vehicles (HCV) require large-capacity, structurally reinforced fuel tanks designed to support extended-range operation in long-haul logistics. HCV operators running trans-continental freight routes demand tanks with maximum volumetric efficiency within tight chassis packaging constraints. This creates demand for custom-engineered high-capacity configurations where engineering capability and OEM certification matter more than unit price alone.

Key Market Segments

By Capacity Type

- Less than 45 L

- 45 L–75 L

- Greater than 75 L

By Material Type

- Plastic

- Metal

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

Drivers

Global vehicle output recovery is a primary driver for fuel tank demand because tank shipments track directly with vehicle production volumes. In 2025, global motor vehicle production increased from 92.7 million to 96.4 million units, while worldwide vehicle sales rose from 95.3 million to 99.8 million units. Higher output improves fixed-cost absorption for component suppliers and accelerates platform refresh cycles that generate new fuel system procurement opportunities.

Hybrid powertrain adoption is the highest-impact driver in the forecast period, contributing an estimated +2.6% to CAGR across key markets including Europe, Japan, South Korea, and North America. Hybrid vehicles retain onboard fuel storage systems but require more compact, pressure-tolerant tank configurations than conventional ICE vehicles. This means suppliers capable of engineering hybrid-compatible tank architectures command stronger OEM relationships and higher per-unit value than standard tank producers.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid powertrain volume shift | +2.6% | EU core, Japan, Korea, North America | Medium term (2-4 years) |

| Global vehicle output recovery | +2.1% | APAC corridors, North America, EU | Short term (≤ 2 years) |

| Evaporative emissions tightening | +1.8% | U.S., EU, Japan, Korea, China | Medium term (2-4 years) |

| Lightweight plastic tank adoption | +1.6% | APAC manufacturing hubs, EU, U.S. | Medium term (2-4 years) |

| APAC-led production rebalancing | +1.5% | China, India, ASEAN, Morocco spill-over | Long term (≥ 4 years) |

| Utility vehicle fuel demand resilience | +1.3% | India, ASEAN, LATAM, Africa | Long term (≥ 4 years) |

Restraints

EVAP compliance cost inflation is a major restraint on fuel tank supplier margins across the most demanding regulatory markets. US EPA Stage II Enhanced and CARB LEVII standards limit evaporative emissions to 0.5 g/day, compared with 2 g/test under Euro 5/6 regulations. Technical studies show that increasing fuel vapor pressure from 60 kPa to 70 kPa raises daily evaporative emissions by approximately 38%, making compliance progressively harder as ambient temperature and fuel volatility rise.

BEV substitution pressure carries the highest CAGR drag in the restraints analysis, estimated at -2.7%, concentrated in the EU core, China, and North America. These three markets account for the largest share of global BEV policy support, fleet electrification mandates, and consumer charging infrastructure investment. Suppliers with heavy revenue concentration in European or Chinese passenger car platforms face the steepest long-term volume exposure as BEV penetration displaces ICE tank fitments.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BEV substitution pressure | -2.7% | EU core, China, North America | Long term (≥ 4 years) |

| Petrol-diesel share collapse | -2.1% | EU core, UK spill-over | Medium term (2-4 years) |

| EVAP compliance cost inflation | -1.6% | U.S., EU, Japan, Korea | Medium term (2-4 years) |

| Platform utilization risk | -1.4% | Europe, North America, legacy suppliers | Medium term (2-4 years) |

| Regional output concentration | -1.2% | Europe, Americas, APAC sourcing chains | Long term (≥ 4 years) |

| Small-car margin erosion | -1.0% | India, ASEAN, LATAM, entry-EU segments | Short term (≤ 2 years) |

Challenges

Production footprint rebalancing is the most structurally disruptive challenge facing fuel tank suppliers across the forecast period. Asia-Pacific output increased 7.6% to 59.2 million vehicles in 2025, representing more than 61% of global production, while European output declined 0.8% and UK production fell 15.5%. This divergence forces suppliers to duplicate tooling, relocate production, and rebuild supplier qualification networks in markets where they currently have limited presence.

Hybrid packaging complexity carries an estimated -1.6% CAGR friction drag as fuel tanks must fit within increasingly constrained underbody spaces shared with battery packs, electric motors, and power electronics. This constraint requires simulation-driven tank design with crash compliance validation, vapor management integration, and reduced cross-sectional profiles. Suppliers without advanced computational design and hybrid-specific tooling investment face extended development cycles and higher program entry costs.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Production footprint rebalancing | -1.8% | Europe, North America, APAC corridors | Long term (≥ 4 years) |

| Hybrid packaging complexity | -1.6% | EU, Japan, Korea, North America | Medium term (2-4 years) |

| EVAP engineering burden | -1.5% | U.S., EU, Japan, Korea, China | Medium term (2-4 years) |

| Resin and multilayer dependence | -1.3% | Global OEM hubs, APAC processing chains | Medium term (2-4 years) |

| Tooling stranded-asset exposure | -1.2% | Europe, U.S., legacy supplier bases | Long term (≥ 4 years) |

| Margin squeeze on small platforms | -1.0% | India, ASEAN, LATAM, entry-EU segments | Short term (≤ 2 years) |

Opportunities

APAC localized platform supply represents a high-priority commercial opportunity for fuel tank suppliers willing to invest in regional engineering and manufacturing capacity. Asia-Pacific vehicle production grew 7.6% to approximately 59.2 million units in 2025, accounting for more than 61% of global output. Industry estimates suggest local-content optimization can reduce delivered system costs by 5–12%, giving regionally embedded suppliers a durable cost and responsiveness advantage over importers.

Hybrid-optimized tank platforms carry a potential CAGR upside of approximately +2.3%, the highest of any opportunity identified in this analysis, concentrated in the EU, Japan, South Korea, and North America. Hybrid vehicles retain fuel storage systems but require pressurized, compact, low-permeation tank designs that conventional ICE tank suppliers cannot immediately serve. This technical requirement creates a qualification gap that early movers with certified hybrid tank programs can exploit for multi-year OEM supply commitments.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Hybrid-optimized tank platforms | +2.3% | EU core, Japan, Korea, North America | Short term (≤ 2 years) |

| Multilayer plastic migration | +1.9% | APAC manufacturing hubs, EU, North America | Medium term (2-4 years) |

| APAC localized platform supply | +2.1% | China, India, ASEAN, Morocco spill-over | Medium term (2-4 years) |

| Smart fuel-system sensing | +1.5% | North America, EU, premium APAC | Medium term (2-4 years) |

| Off-highway and small CV adjacencies | +1.7% | India, ASEAN, LATAM, Africa | Long term (≥ 4 years) |

| Supplier roll-up and modularization | +1.6% | EU, North America, East Asia | Long term (≥ 4 years) |

Regional Analysis

Asia-Pacific Dominates the Automobile Fuel Tanks Market with a Market Share of 46.82%, Valued at USD 10.2 Billion

Asia-Pacific commands 46.82% of the global automobile fuel tanks market, driven by the region’s position as the world’s largest vehicle production base. Asia-Pacific output reached approximately 59.2 million units in 2025, accounting for more than 61% of global vehicle production. China alone produced 34.53 million vehicles in 2025, while India contributed 6.49 million units, creating an exceptionally high-density procurement environment for fuel tank suppliers with regional manufacturing capability.

North America represents a structurally important market for fuel tank suppliers due to strict EPA evaporative emissions standards and sustained consumer preference for full-size SUVs and pickup trucks. The US EPA limits evaporative hydrocarbon emissions and requires fuel systems to meet permeation compliance thresholds, pushing suppliers toward advanced multilayer barrier-layer tank designs. This regulatory environment creates higher per-unit value and favors technically capable suppliers over low-cost alternatives.

Europe faces a dual structural pressure in the fuel tanks market, with vehicle production declining 0.8% in 2025 and the UK recording a steeper drop of 15.5%. Strict Euro 5/6 evaporative emission standards and accelerating BEV adoption are compressing the addressable market for conventional internal combustion fuel tanks. However, the transition toward hybrid powertrains sustains near-term demand for compact, lightweight fuel tank systems across European OEM platforms.

Latin America and the Middle East and Africa represent longer-horizon growth corridors for fuel tank suppliers, supported by expanding vehicle parc size, rising commercial fleet activity, and limited BEV penetration relative to global averages. These regions sustain demand for conventional and ethanol-compatible tank designs across passenger, commercial, and utility vehicle segments. Suppliers establishing regional supply chain presence early can secure preferred-supplier status as local OEM assembly capacity expands.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Yachiyo Industry Co., Ltd. is a Japan-based fuel tank specialist with deep integration into Honda’s global vehicle platforms, giving it preferred-supplier access across high-volume passenger car programs. As reported by the US EIA, more than 95% of gasoline consumed in US gasoline-powered vehicles is E10, which means Yachiyo’s tank systems must meet baseline ethanol-compatibility standards across every North American fitment. This compliance baseline protects volume but limits differentiation on material chemistry alone.

Continental AG brings an integrated systems approach to fuel storage, combining tank engineering with fuel delivery modules, sensors, and connected vehicle interfaces into unified platform solutions. In July 2025, TI Automotive announced plans to showcase ultra-light pressurized hybrid fuel tank technologies at IAA Mobility 2025. Continental’s comparable capability in hybrid fuel system integration positions it to compete for OEM contracts as automakers accelerate hybrid platform launches across Europe and Asia-Pacific. Suppliers without this systems depth will face increasing margin pressure as OEMs consolidate sourcing to fewer full-system partners. Approximately 13.73 billion gallons of fuel ethanol were blended into US gasoline in 2023, underscoring the scale of the compliant tank market these integrated suppliers must serve.

Key Players

- Yachiyo Industry Co., Ltd.

- Continental AG

- Kautex Textron GmbH & Co. KG

- TI Automotive Inc.

- Magna International Inc.

- YAPP Automotive Parts Co. Ltd.

- SMA Serbatoi S.P.A.

- The Plastic Omnium Group

- Martinrea International Inc.

- Unipres Corporation

- The Stars Group Plc.

Recent Developments

- April 2025 – ABC Technologies completed the acquisition of TI Fluid Systems, a leading manufacturer of automotive fluid storage, carrying, and delivery systems including fuel tanks. The combined business was announced to operate under the TI Automotive brand going forward.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 21.7 Billion |

| Forecast Revenue (2035) | USD 43.3 Billion |

| CAGR (2026-2035) | 7.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Capacity Type (Less than 45 L, 45 L–75 L, Greater than 75 L), By Material Type (Plastic, Metal), By Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Yachiyo Industry Co., Ltd., Continental AG, Kautex Textron GmbH & Co. KG, TI Automotive Inc., Magna International Inc., YAPP Automotive Parts Co. Ltd., SMA Serbatoi S.P.A., The Plastic Omnium Group, Martinrea International Inc., Unipres Corporation, The Stars Group Plc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |