Quick Navigation

Report Overview

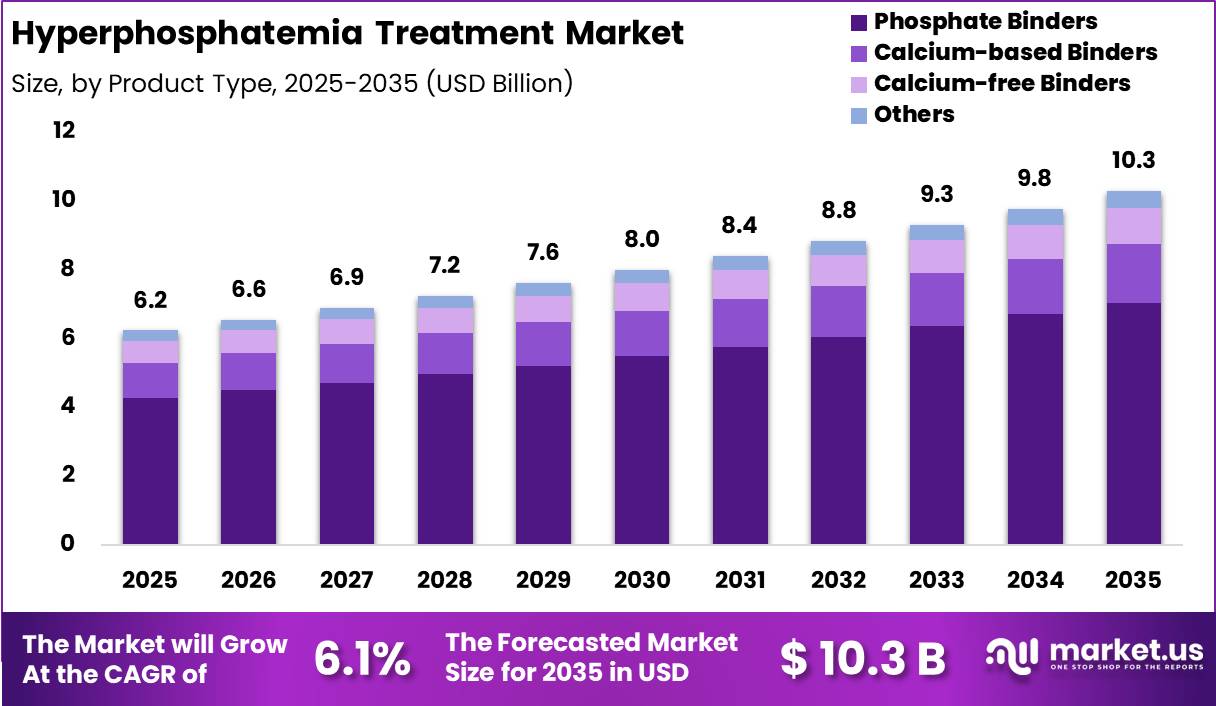

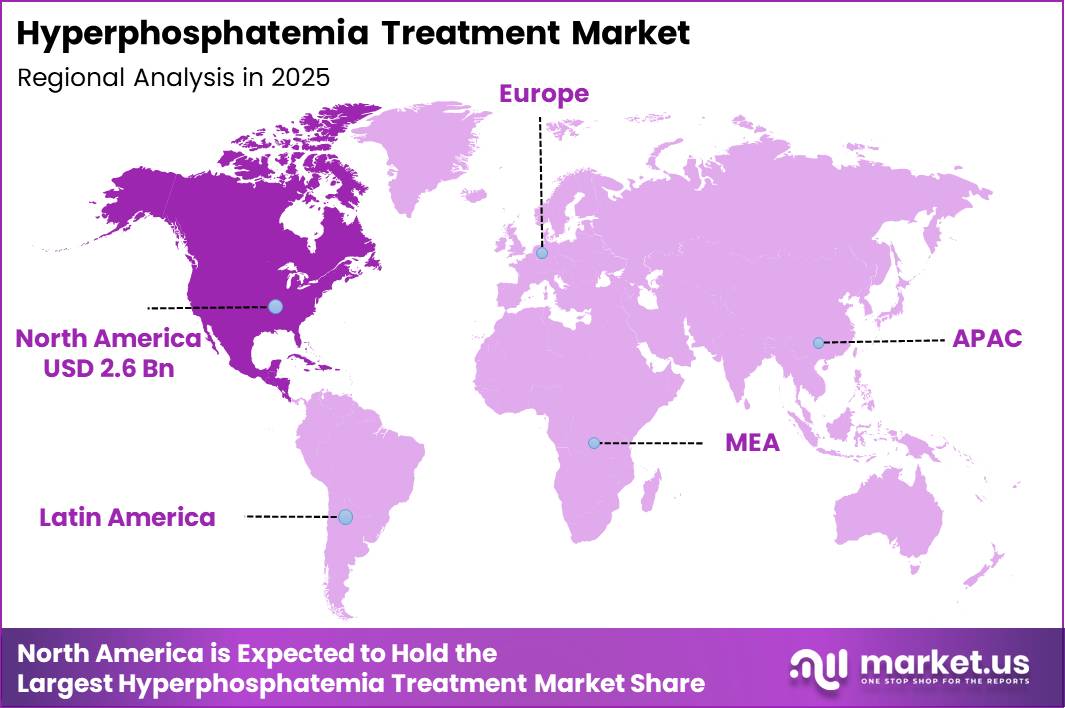

Global Hyperphosphatemia Treatment Market size is expected to be worth around US$ 10.3 Billion by 2035 from US$ 6.2 Billion in 2025, growing at a CAGR of 5.1% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 42.5% share with a revenue of US$ 2.6 Billion.

Hyperphosphatemia is a metabolic disorder characterized by abnormally elevated phosphate levels in the blood, typically defined as serum phosphate concentrations above 4.5 mg/dL in adults. Phosphate plays a vital role in numerous physiological processes, including bone mineralization, cellular energy production, and intracellular signaling. Approximately 85% of the body’s phosphate is stored in bones, while the kidneys are responsible for excreting nearly 90% of the daily phosphate load to maintain normal phosphate balance.

Impaired phosphate excretion, particularly in patients with chronic kidney disease (CKD), is the most common cause of hyperphosphatemia. According to the U.S. National Center for Biotechnology Information (NCBI), hyperphosphatemia affects approximately 50%–74% of patients with end-stage renal disease (ESRD), highlighting its significant clinical burden.

The treatment of hyperphosphatemia is essential because persistent elevation of phosphate levels can lead to calcium-phosphate crystal deposition in soft tissues, vascular calcification, cardiovascular complications, bone disorders, and impaired mineral metabolism. Research indicates that serum phosphate levels above the normal range are associated with an increased risk of adverse cardiovascular outcomes, particularly among CKD patients.

Current treatment strategies focus on reducing phosphate absorption, controlling dietary phosphate intake, and managing the underlying disease. Dietary interventions involve limiting phosphate-rich foods such as dairy products, processed foods, and phosphate-containing beverages. Clinical guidelines from the Kidney Disease: Improving Global Outcomes (KDIGO) organization recommend maintaining serum phosphate levels within or toward the normal range, generally between 2.5 and 4.5 mg/dL in CKD patients.

Phosphate binders remain the cornerstone of pharmacological treatment and are widely prescribed for patients with CKD and dialysis-dependent kidney disease. Commonly used agents include sevelamer, lanthanum carbonate, calcium acetate, and calcium carbonate. KDIGO guidelines also support the use of phosphate-lowering therapies and phosphate binders in patients with CKD-associated hyperphosphatemia.

The increasing global prevalence of CKD, growing dialysis patient population, and rising awareness regarding mineral and bone disorders are contributing to the demand for effective hyperphosphatemia management therapies, supporting continued advancements in treatment approaches and therapeutic innovation.

Key Takeaways

- Market Size: Global Hyperphosphatemia Treatment Market size is expected to be worth around US$ 10.3 Billion by 2035 from US$ 6.2 Billion in 2025.

- Market Share: The market growing at a CAGR of 5.1% during the forecast period from 2026 to 2035.

- Drug Type Analysis: Phosphate Binders accounted for the largest market share of 68.5% in 2025.

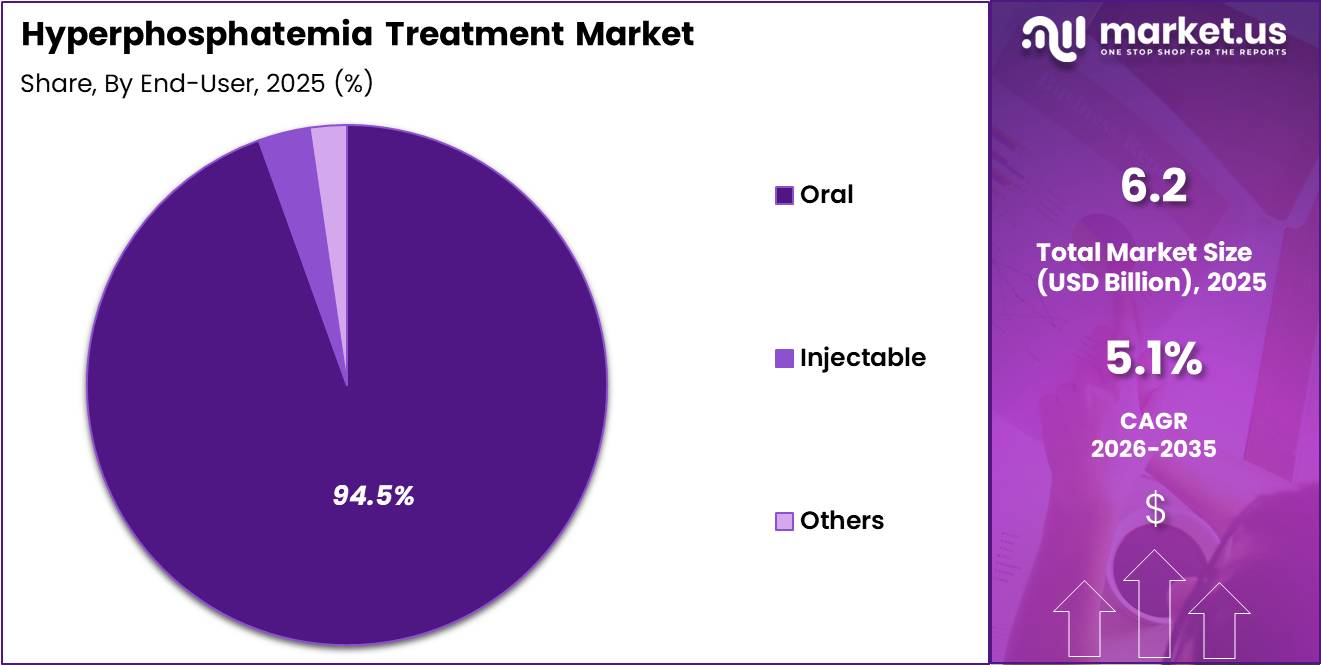

- Route of Administration Analysis: The Oral segment dominated the market with a 94.5% share in 2025

- End User Analysis: Hospitals held the largest market share of 58.4% in 2025

- Regional Analysis: In 2025, North America led the market, achieving over 42.5% share with a revenue of US$ 2.6 Billion.

Drug Type Analysis

The drug type segment of the Hyperphosphatemia Treatment Market is categorized into Phosphate Binders, Calcium-based Binders, Calcium-free Binders, and Others. Phosphate Binders accounted for the largest market share of 68.5% in 2025, owing to their established role as the primary therapeutic approach for controlling elevated serum phosphate levels in patients with chronic kidney disease (CKD) and end-stage renal disease (ESRD).

These agents effectively reduce phosphate absorption from the gastrointestinal tract, making them a standard component of long-term disease management. The growing prevalence of CKD, increasing dialysis patient population, and strong clinical recommendations supporting phosphate binder therapy continue to reinforce segment dominance.

The Calcium-based Binders segment maintains a significant position due to their affordability and widespread availability, particularly in cost-sensitive healthcare systems. However, concerns regarding calcium overload and vascular calcification have moderately limited their adoption in certain patient groups.

Calcium-free Binders are witnessing notable growth as healthcare providers increasingly prefer therapies with improved safety profiles and reduced cardiovascular risks. These products are gaining traction among patients requiring long-term phosphate control. The Others segment, including emerging therapies and combination treatments, represents a smaller share but is expected to benefit from ongoing pharmaceutical innovation and the development of next-generation phosphate management solutions.

Route of Administration Analysis

Based on route of administration, the Hyperphosphatemia Treatment Market is segmented into Oral, Injectable, and Others. The Oral segment dominated the market with a 94.5% share in 2025, primarily due to the widespread use of orally administered phosphate binders as the first-line treatment for hyperphosphatemia.

Oral formulations offer convenience, ease of administration, and high patient acceptance, making them particularly suitable for chronic disease management. The availability of multiple oral treatment options, including tablets, capsules, and chewable formulations, further supports their extensive adoption across both hospital and outpatient settings.

The increasing prevalence of chronic kidney disease and the growing number of patients undergoing long-term dialysis have significantly contributed to the demand for oral therapies. Additionally, ongoing product improvements aimed at enhancing patient compliance and reducing pill burden continue to strengthen the segment’s leading position. The Injectable segment accounts for a comparatively smaller market share but is gaining attention in specific clinical situations where rapid phosphate control or alternative administration methods are required.

Injectable therapies are particularly valuable for hospitalized patients and individuals unable to tolerate oral medications. Meanwhile, the Others segment remains limited, encompassing niche delivery approaches and emerging formulations that are currently under development. Continued innovation in drug delivery technologies may create future opportunities within these smaller segments.

End User Analysis

The Hyperphosphatemia Treatment Market, by end user, is segmented into Hospitals, Dialysis Centers, Homecare Settings, and Others. Hospitals held the largest market share of 58.4% in 2025, driven by the high volume of chronic kidney disease and end-stage renal disease patients receiving diagnosis, treatment initiation, and ongoing clinical management within hospital environments.

Hospitals provide access to specialized nephrology services, comprehensive diagnostic capabilities, and multidisciplinary care teams, making them the preferred setting for managing complex hyperphosphatemia cases. The increasing number of hospital admissions related to kidney disorders and associated complications further supports segment growth.

Dialysis Centers represent the second-largest segment, benefiting from the direct association between hyperphosphatemia and patients undergoing regular dialysis treatment. These facilities play a critical role in monitoring phosphate levels and ensuring adherence to phosphate-lowering therapies. The expansion of dialysis infrastructure globally and the rising prevalence of renal diseases continue to drive demand within this segment.

Homecare Settings are experiencing steady growth due to increasing patient preference for convenient disease management and the broader availability of oral phosphate-binding medications that can be administered independently. The Others segment includes specialty clinics and long-term care facilities, which collectively contribute a smaller share but remain important in delivering supportive and follow-up care for patients requiring ongoing phosphate management.

Key Market Segments

By Drug Type

- Phosphate Binders

- Calcium-based Binders

- Calcium-free Binders

- Others

By Route of Administration

- Oral

- Injectable

- Others

By End User

- Hospitals

- Dialysis Centers

- Homecare Settings

- Others

Driving Factors

Rising CKD and dialysis burden

A major driver of the hyperphosphatemia treatment market is the increasing global prevalence of chronic kidney disease (CKD) and end-stage renal disease (ESRD). Hyperphosphatemia affects approximately 50–74% of ESRD patients, compared with about 12% in the general population, creating a substantially larger treatment population in advanced kidney disease.

Clinical guidelines from the Kidney Disease: Improving Global Outcomes (KDIGO) recommend phosphate-lowering interventions, including dietary management, phosphate binders, and dialysis, for CKD patients with persistently elevated serum phosphate levels. As dialysis adoption continues to increase worldwide, the number of patients requiring long-term phosphate control is expanding.

Growing recognition of the association between phosphate management and reduced cardiovascular and bone-related complications is also supporting broader and earlier intervention, further increasing demand for hyperphosphatemia therapies.

Trending Factors

Shift to non-calcium and multifunctional therapies

A key market trend is the transition from traditional calcium-based phosphate binders toward non-calcium and multifunctional treatment options. Safety concerns related to vascular calcification have encouraged the use of alternatives such as sevelamer, lanthanum, iron-based phosphate binders, and emerging intestinal phosphate transporter inhibitors.

Iron-based binders are gaining traction because they can simultaneously support phosphate control and address iron deficiency, complementing anemia management strategies in CKD patients. In addition, recent CKD treatment guidelines emphasize individualized phosphate management and continuous monitoring, increasing demand for therapies that offer improved tolerability, lower gastrointestinal side effects, and better patient adherence. These factors are driving a more diversified and patient-centric treatment landscape.

Restraining Factors

Pill burden, adherence, and cost barriers

High pill burden, poor treatment adherence, and cost pressures remain key barriers to market growth. Many dialysis patients require multiple daily doses of phosphate binders, making long-term compliance difficult. Non-adherence is associated with poorer phosphorus control and worsening mineral-bone disorder outcomes.

Treatment complexity is further increased by the need to combine dietary restrictions, dialysis, and medication therapy. Despite available treatments, hyperphosphatemia remains highly prevalent among ESRD patients, indicating ongoing challenges in achieving recommended phosphate targets.

Cost also limits adoption, particularly in low- and middle-income countries where access to newer non-calcium binders may be restricted by affordability and reimbursement limitations. In developed markets, the long-term budget impact of branded therapies encourages formulary restrictions and generic substitution, which can slow uptake of innovative products.

Opportunity

Low-pill, personalized and earlier-stage management

Significant opportunities exist for therapies that reduce pill burden, improve tolerability, and support earlier intervention in CKD. Current clinical recommendations increasingly support initiating phosphate-lowering strategies in patients with persistently elevated phosphate levels rather than waiting for severe abnormalities, creating opportunities in earlier-stage CKD populations.

Novel therapies, including intestinal phosphate transporter inhibitors and simplified formulations such as chewable or reduced-tablet regimens, have the potential to improve adherence and treatment outcomes. Additionally, personalized phosphate management approaches that combine dietary counseling, optimized dialysis protocols, and tailored pharmacotherapy are creating opportunities for digital health solutions and clinical decision-support platforms. These innovations are expected to help healthcare systems manage CKD-related mineral and bone disorders more effectively while improving patient outcomes.

Regional Analysis

In 2025, North America dominated the Hyperphosphatemia Treatment Market, accounting for more than 42.5% of the global market share and generating revenue of approximately US$ 2.6 billion. The region’s leadership can be attributed to the high prevalence of chronic kidney disease (CKD) and end-stage renal disease (ESRD), both of which are major contributors to hyperphosphatemia.

The presence of a well-established healthcare infrastructure, widespread access to advanced diagnostic services, and strong reimbursement frameworks have further supported market growth across the United States and Canada.

The United States represented the largest share within the region due to the growing number of dialysis patients, increasing adoption of phosphate binders, and continuous advancements in renal care therapies. Moreover, the rising elderly population, which is more susceptible to kidney-related disorders, has increased the demand for effective phosphate management treatments. Strong investments in pharmaceutical research and development, coupled with the presence of leading biotechnology and pharmaceutical companies, have accelerated the introduction of innovative treatment options.

Additionally, favorable government initiatives aimed at improving kidney disease management and increasing patient awareness have contributed to higher treatment adoption rates. The growing focus on value-based healthcare and personalized treatment approaches is also expected to support market expansion. As a result, North America is anticipated to maintain its dominant position in the Hyperphosphatemia Treatment Market throughout the forecast period.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The Hyperphosphatemia Treatment Market is characterized by the presence of several established pharmaceutical companies focused on expanding their product portfolios and strengthening their market positions through innovation, strategic collaborations, and geographic expansion.

Key players include Sanofi, Fresenius Medical Care, Vifor Pharma, Keryx Biopharmaceuticals, and Ardelyx, Inc.. These companies are actively investing in research and development to introduce advanced phosphate binders with improved efficacy, safety, and patient compliance. The competitive landscape is driven by the growing prevalence of chronic kidney disease and end-stage renal disease, increasing demand for effective phosphate management therapies, and regulatory approvals of novel treatment options.

Market participants are also emphasizing partnerships with healthcare providers and dialysis centers to enhance product adoption. Continuous product innovation, strong distribution networks, and expansion into emerging markets remain key strategies adopted by leading companies to maintain their competitive advantage and support long-term market growth.

Market Key Players

- Sanofi S.A.

- Fresenius Medical Care AG & Co. KGaA

- Vifor Pharma Ltd.

- Takeda Pharmaceutical Company Limited

- Kyowa Kirin Co., Ltd.

- Astellas Pharma Inc.

- Bayer AG

- Pfizer Inc.

- Novartis AG

- Mylan N.V. (Viatris)

- Teva Pharmaceutical Industries Ltd.

- Sun Pharmaceutical Industries Ltd.

- Dr. Reddy’s Laboratories Ltd.

- Lupin Limited

- Ardelyx Inc.

- Others

Recent Developments

- February 2025 – Ardelyx Inc. received regulatory approval in China for tenapanor, a first-in-class phosphate absorption inhibitor indicated for the treatment of hyperphosphatemia in chronic kidney disease (CKD) patients on dialysis. The approval was achieved through Ardelyx’s partnership with Shanghai Fosun Pharma and triggered a US$5 million milestone payment to the company. This development significantly expands tenapanor’s commercial footprint in one of the world’s largest dialysis patient populations.

- February 2025 – Novartis AG announced that the European Medicines Agency’s Committee for Medicinal Products for Human Use (CHMP) issued a positive opinion for Fabhalta (iptacopan) in the treatment of C3 glomerulopathy (C3G), a rare kidney disease. Although not a direct hyperphosphatemia therapy, the advancement strengthens Novartis’ nephrology portfolio and reinforces its strategic focus on kidney disease management, a key area linked to phosphate imbalance complications.

- 2026 – Takeda Pharmaceutical Company Limited initiated a major global restructuring and operational optimization program aimed at improving efficiency and supporting future product launches. The company indicated plans to generate annual savings exceeding ¥200 billion, enabling greater investment in high-priority therapeutic areas, including nephrology and rare disease research

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 6.2 Billion |

| Forecast Revenue (2035) | US$ 10.3 Billion |

| CAGR (2026-2035) | 5.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Drug Type (Phosphate Binders, Calcium-based Binders, Calcium-free Binders, Others) By Route of Administration (Oral, Injectable, Others) By End User (Hospitals, Dialysis Centers, Homecare Settings, Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Sanofi S.A., Fresenius Medical Care AG & Co. KGaA, Vifor Pharma Ltd., Takeda Pharmaceutical Company Limited, Kyowa Kirin Co., Ltd., Astellas Pharma Inc., Bayer AG, Pfizer Inc., Novartis AG, Mylan N.V. (Viatris), Teva Pharmaceutical Industries Ltd., Sun Pharmaceutical Industries Ltd., Dr. Reddy’s Laboratories Ltd., Lupin Limited, Ardelyx Inc., Others. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |