Global Aquaculture Feed Market Size, Share, And Industry Analysis Report By Product (Fish Feed, Mollusk Feed, Crustacean Feed, Others), By Form Factor (Dry, Wet), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: February 2026

- Report ID: 180038

- Number of Pages: 273

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

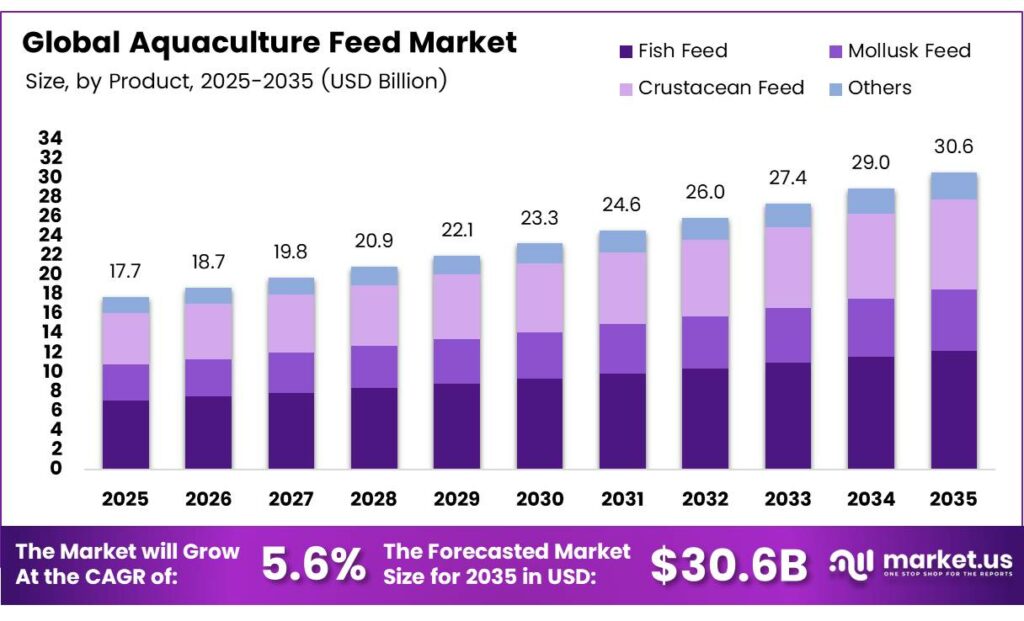

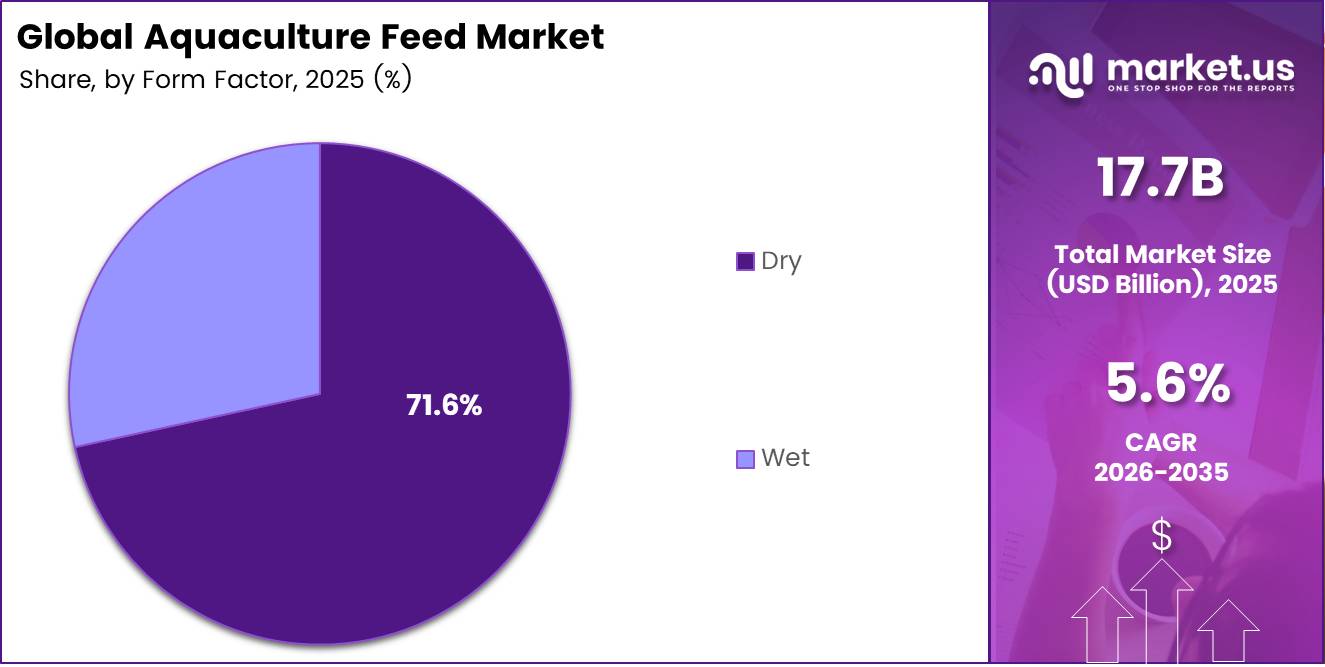

The Global Aquaculture Feed Market size is expected to be worth around USD 30.6 billion by 2035 from USD 17.7 billion in 2025, growing at a CAGR of 5.6% during the forecast period 2026 to 2035.

Aquaculture feed refers to nutritionally balanced compounds designed to support the growth, immunity, and productivity of farmed aquatic species. Manufacturers formulate these feeds to meet the specific dietary requirements of fish, crustaceans, mollusks, and other cultured organisms. Feed quality directly influences survival rates, conversion efficiency, and final product yield.

The market spans multiple product types, including dry pellets, wet feeds, and semi-moist formulations. Producers develop species-specific feed solutions for salmon, shrimp, tilapia, carp, and various shellfish. Moreover, functional additives such as probiotics, vitamins, and enzymes are increasingly integrated to boost animal health and performance.

- India’s farm-made aquafeed production reached approximately 13.95 million tonnes, with on-farm systems requiring an average of about 3 kg of feed to produce 1 kg of carp in grow-out systems. This highlights the significant scale of smallholder aquaculture activity in emerging markets and points to strong volume-driven feed demand.

Global seafood demand continues to rise as populations grow and health-conscious consumers shift toward protein-rich diets. Consequently, commercial aquaculture operations are scaling up production to bridge the gap left by stagnating wild catch volumes. This expansion directly increases the demand for high-efficiency compound feeds across all major farming regions.

- Europe accounted for 4.6 million tonnes of aquafeed compared to 52.9 million tonnes globally, giving Europe roughly a 9% share of worldwide aquafeed tonnage. This relatively modest regional share signals considerable growth headroom as European producers intensify operations and adopt higher-value formulations.

Governments across the Asia Pacific, Europe, and Latin America are actively investing in aquaculture development programs and infrastructure. Regulatory agencies promote sustainable sourcing standards and reduced marine dependency in feed formulations. Additionally, public-private partnerships support research into alternative proteins and precision nutrition technologies that improve feed conversion ratios.

Key Takeaways

- The Global Aquaculture Feed Market is projected to reach USD 30.6 billion by 2035, up from USD 17.7 billion in 2025, at a CAGR of 5.6% during the forecast period 2026 to 2035.

- Fish Feed dominates with a 67.3% market share in 2025.

- Dry feed holds the largest share at 71.6% in 2025.

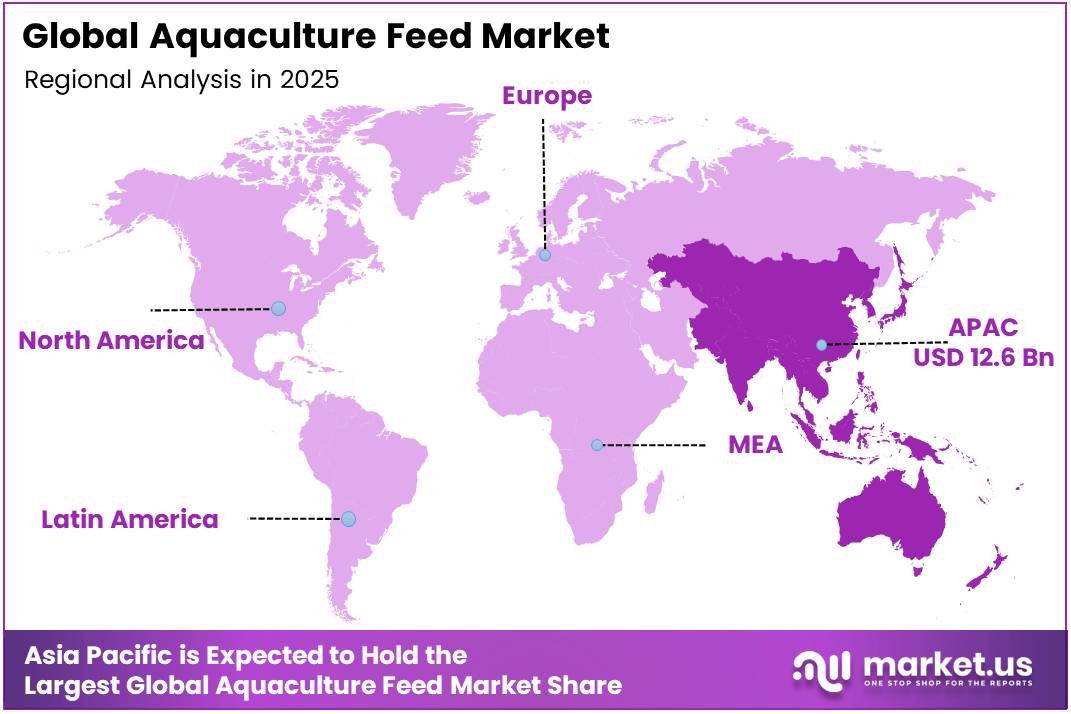

- Asia Pacific leads all regions with a 71.2% market share, valued at USD 12.6 billion.

By Product Analysis

Fish Feed dominates with 67.3% due to the large global volume of finfish farming operations.

In 2025, Fish Feed held a dominant market position in the By Product segment of the Aquaculture Feed Market, with a 67.3% share. Finfish species such as salmon, tilapia, carp, and catfish represent the largest cultured volumes worldwide. Consequently, fish feed commands the highest production and sales volumes, supported by intensive commercial farming across Asia Pacific, Europe, and the Americas.

Mollusk Feed serves the cultivation of oysters, mussels, clams, and scallops across coastal farming regions. Additionally, mollusk aquaculture requires specialized nutrition that supports shell formation and soft tissue development. Demand for mollusk feed grows steadily as export markets for premium shellfish products expand in Europe and East Asia.

Crustacean Feed covers shrimp, prawn, lobster, and crab species cultured in tropical and subtropical regions. Shrimp farming alone drives the majority of crustacean feed consumption, particularly in India, Vietnam, and Ecuador. Moreover, disease-resistant and high-protein formulations for crustaceans continue to attract strong investment from feed manufacturers.

Others include feeds for turtle, eel, frog, and other niche aquatic species. This sub-segment accounts for a smaller share but shows growth potential as specialty aquaculture diversifies globally. Therefore, manufacturers are beginning to develop targeted nutrition programs for these less conventional farmed organisms.

By Form Factor Analysis

Dry feed dominates with 71.6% due to superior shelf life, ease of handling, and large-scale compatibility.

In 2025, Dry feed held a dominant market position in the By Form Factor segment of the Aquaculture Feed Market, with a 71.6% share. Dry pellets and extruded feeds offer extended shelf life, stable nutrient profiles, and compatibility with automated feeding systems. Therefore, large-scale fish and shrimp farms widely prefer dry formulations for their operational efficiency and consistent performance.

Wet feed includes moist and semi-moist formulations used primarily in salmon farming and certain marine species cultivation. These formats deliver high palatability and superior nutrient bioavailability, especially for carnivorous finfish species. However, wet feeds require cold-chain storage and careful handling, limiting their adoption to regions with established infrastructure and smaller production batches.

Key Market Segments

By Product

- Fish Feed

- Mollusk Feed

- Crustacean Feed

- Others

By Form Factor

- Dry

- Wet

Emerging Trends

Sustainability, Smart Technology, and Customization Reshape the Aquaculture Feed Industry

Feed manufacturers are accelerating the shift toward low-carbon and eco-friendly ingredient sourcing. Companies are reducing reliance on marine-derived inputs such as fishmeal and fish oil. Instead, producers are integrating plant-based proteins, algal oils, and insect meal to improve sustainability credentials and comply with evolving environmental standards.

- Natural additives such as probiotics, organic acidifiers, and herbal extracts are gaining strong adoption in aquafeed formulations. Global aquafeed tonnage reached 52.9 million tonnes, illustrating the enormous scale at which these additive trends now apply. These ingredients improve gut health, reduce antibiotic dependency, and strengthen disease resistance across farmed species.

Digital monitoring and smart feeding systems are transforming farm management practices. Real-time sensors, AI-driven feed dispensers, and biomass estimation tools allow farmers to optimize feeding schedules and reduce waste. Additionally, manufacturers are developing life-stage and species-tailored feed solutions to match the precise nutritional requirements of each growth phase.

Drivers

Rising Seafood Demand, Aquaculture Expansion, and Feed Innovation Drive Strong Market Growth

Global seafood consumption continues to surge as population growth and health awareness among consumers accelerate demand for high-protein diets. Capture fisheries have largely reached their sustainable limits, making commercial aquaculture the primary growth channel for meeting this demand. Mowi’s Norwegian salmon feed mill reached a production capacity of 460,000 tonnes in 2024, with an additional 60,000-tonne line under construction, reflecting industry confidence in sustained feed demand growth.

- Commercial aquaculture operations are intensifying farming practices to achieve higher yields per unit area. Consequently, farmers are shifting from low-efficiency homemade feeds to professionally formulated compound feeds that deliver superior growth rates and feed conversion ratios. Guangdong Haid sold 5.85 million tonnes of aquafeed in 2024, confirming the enormous scale that intensive aquaculture feed production has reached globally.

Technological innovations in nutritionally balanced and species-specific feed formulations continue to expand market value. Feed scientists are developing precision nutrition programs that match the amino acid, lipid, and mineral profiles required at each life stage. Therefore, producers who invest in R&D and species-tailored formulations capture premium pricing and long-term customer loyalty in competitive aquaculture markets.

Restraints

Raw Material Volatility and Regulatory Pressure Create Significant Challenges for Feed Producers

Persistent price volatility in critical raw materials such as fishmeal and fish oil continues to pressure feed manufacturers’ margins and planning cycles. Global fishmeal supplies fluctuate significantly depending on Peruvian anchovy catch seasons and climate-driven disruptions. Consequently, producers struggle to maintain stable feed pricing, which undermines long-term supply agreements with aquaculture farmers.

- Stringent environmental regulations are raising the cost and complexity of feed production across major markets. BioMar’s consolidated aquafeed volumes declined from 1.437 million tonnes in 2023 to 1.372 million tonnes in 2024, partly reflecting the pressure that compliance costs and raw material pricing place on volumes and producer economics.

Sustainable sourcing mandates require feed companies to substitute or reduce marine-derived ingredients, increasing formulation complexity. Alternative proteins such as insect meal and algal oil involve higher production costs and inconsistent supply chains at current commercial scales. Therefore, smaller feed manufacturers face significant barriers in reformulating products to meet both regulatory requirements and farmer performance expectations simultaneously.

Growth Factors

Alternative Proteins, Precision Nutrition, and Specialized Systems Unlock New Market Opportunities

The adoption of alternative proteins from plant-based, insect, and algal sources represents one of the most transformative growth opportunities in aquaculture feed. These ingredients reduce dependence on marine resources and support environmental sustainability goals that major buyers and retailers now require. Additionally, insect-based proteins offer superior amino acid profiles that improve growth performance for multiple farmed species.

- Integration of precision nutrition technologies allows producers to optimize feed conversion ratios and reduce waste at the farm level. Mowi Feed sold 584,586 tonnes of salmon feed in 2024, up from 523,167 tonnes in 2023, with its two European plants supplying 96% of the feed requirements for Mowi’s European salmon farming operations.

The expansion of land-based recirculating aquaculture systems creates demand for highly specialized feeds tailored to controlled-environment conditions. Rising demand for functional feeds that enhance immunity and disease resistance further elevates the value of each tonne sold. Therefore, manufacturers who develop premium health-focused and system-specific formulations are positioned to capture higher margins in the evolving aquaculture feed landscape.

Regional Analysis

Asia Pacific Dominates the Aquaculture Feed Market with a Market Share of 71.2%, Valued at USD 12.6 Billion

Asia Pacific leads the global aquaculture feed market with a dominant 71.2% share, valued at USD 12.6 billion in 2025. The region hosts the world’s largest aquaculture producers, including China, India, Vietnam, and Indonesia. Moreover, high domestic seafood consumption, government support for aquaculture development, and low-cost production infrastructure sustain the region’s commanding market position.

North America presents a mature and innovation-driven aquaculture feed market supported by advanced feed technology and strong regulatory oversight. The United States and Canada focus on salmon, trout, and tilapia farming, creating demand for premium formulations. Additionally, increasing consumer preference for sustainably sourced seafood accelerates the adoption of certified and traceable aquaculture feed products.

Europe maintains a steady aquaculture feed market, led by Norway’s large-scale salmon industry and Mediterranean fish farming operations. The European Union enforces strict standards on feed ingredient safety and environmental sustainability. Consequently, European feed producers invest heavily in alternative protein research and low-marine-impact formulations to remain compliant and competitive.

The Middle East and Africa region shows emerging potential in aquaculture feed as governments invest in food security and domestic protein production. Countries such as Egypt, Saudi Arabia, and South Africa are developing freshwater and marine aquaculture sectors. Therefore, demand for locally adapted feed formulations suitable for warm-water species is gradually expanding across the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Aller Aqua AS is a Denmark-based global aquaculture feed manufacturer operating seven feed production facilities across Europe, Africa, and Asia. The company serves customers in more than 60 countries and employs approximately 700 people globally. Its diverse geographic footprint and species-tailored product range position it as a resilient competitor in premium feed markets.

Avanti Feeds Ltd. is one of India’s leading aquaculture feed producers, specializing in shrimp feed for domestic and export markets. Moreover, Avanti Feeds’ profit before tax grew, driven largely by its shrimp feed operations. Its strong domestic presence and established export network make it a significant player in the South Asian aquaculture feed segment.

Cargill Inc. is a US-based multinational with a major position in the global aquaculture feed industry. The company offers a broad range of nutrition solutions for fish, shrimp, and other aquatic species across multiple continents. Cargill’s global supply chain capabilities and research investment in alternative proteins and functional feeds reinforce its competitive strength.

Nutreco N.V. is a Netherlands-based animal and aquaculture nutrition company operating through its Skretting brand in the global aquafeed sector. The company provides complete feed programs for salmon, trout, tilapia, and shrimp with a strong emphasis on sustainability and performance. Furthermore, Nutreco invests significantly in research on alternative proteins, feed additives, and precision feeding technologies.

Top Key Players in the Market

- Aller Aqua AS

- Alltech Inc.

- Archer Daniels Midland Co.

- Avanti Feeds Ltd.

- BRF SA

- Cargill Inc.

- Charoen Pokphand Foods PCL

- Godrej and Boyce Manufacturing Co. Ltd.

- Grand Fish Feed

- Growel Feeds Pvt. Ltd.

- IB Group

- Land O Lakes Inc.

- National Aquaculture Group

- Nutreco N.V.

- Olmix SA

- Ridley Corp. Ltd.

- Schouw and Co.

- The Waterbase Ltd.

- Tyson Foods Inc.

- Viet Uc Seafood Corp.

Recent Developments

- In 2025, Aller Aqua is developing and field-testing functional aquafeeds incorporating microalgae-derived additives (protein, fatty acids, vitamins, pigments, bioactive compounds) to combat winter ulcers, enhance mucosal health, and improve welfare in farmed salmon amid climate challenges and emerging diseases.

- In 2025, ASC Feed Standard certifications Alltech Coppens (Nettetal, Germany) and Alltech Fennoaqua (Raisio, Finland) became the first feed mills in their countries to achieve ASC Feed Standard certification. This covers the responsible sourcing of all aquafeed ingredients with requirements for fair labour, safety, and reduced environmental impact.

Report Scope

Report Features Description Market Value (2025) USD 17.7 Billion Forecast Revenue (2035) USD 30.6 Billion CAGR (2026-2035) 5.6% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Fish Feed, Mollusk Feed, Crustacean Feed, Others), By Form Factor (Dry, Wet) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Aller Aqua AS, Alltech Inc., Archer Daniels Midland Co., Avanti Feeds Ltd., BRF SA, Cargill Inc., Charoen Pokphand Foods PCL, Godrej and Boyce Manufacturing Co. Ltd., Grand Fish Feed, Growel Feeds Pvt. Ltd., IB Group, Land O Lakes Inc., National Aquaculture Group, Nutreco N.V., Olmix SA, Ridley Corp. Ltd., Schouw and Co., The Waterbase Ltd., Tyson Foods Inc., Viet Uc Seafood Corp. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Aquaculture Feed MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample

Aquaculture Feed MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Aller Aqua AS

- Alltech Inc.

- Archer Daniels Midland Co.

- Avanti Feeds Ltd.

- BRF SA

- Cargill Inc.

- Charoen Pokphand Foods PCL

- Godrej and Boyce Manufacturing Co. Ltd.

- Grand Fish Feed

- Growel Feeds Pvt. Ltd.

- IB Group

- Land O Lakes Inc.

- National Aquaculture Group

- Nutreco N.V.

- Olmix SA

- Ridley Corp. Ltd.

- Schouw and Co.

- The Waterbase Ltd.

- Tyson Foods Inc.

- Viet Uc Seafood Corp.

Our Clients

- 180038

- February 2026