Quick Navigation

Report Overview

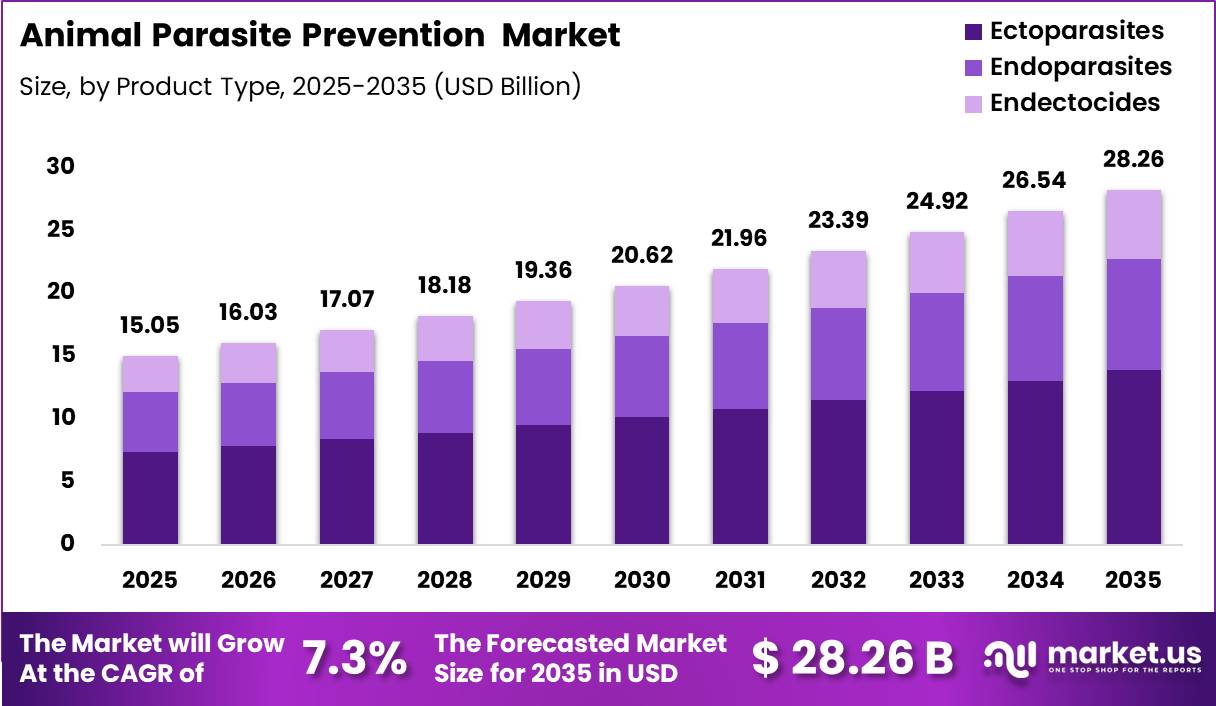

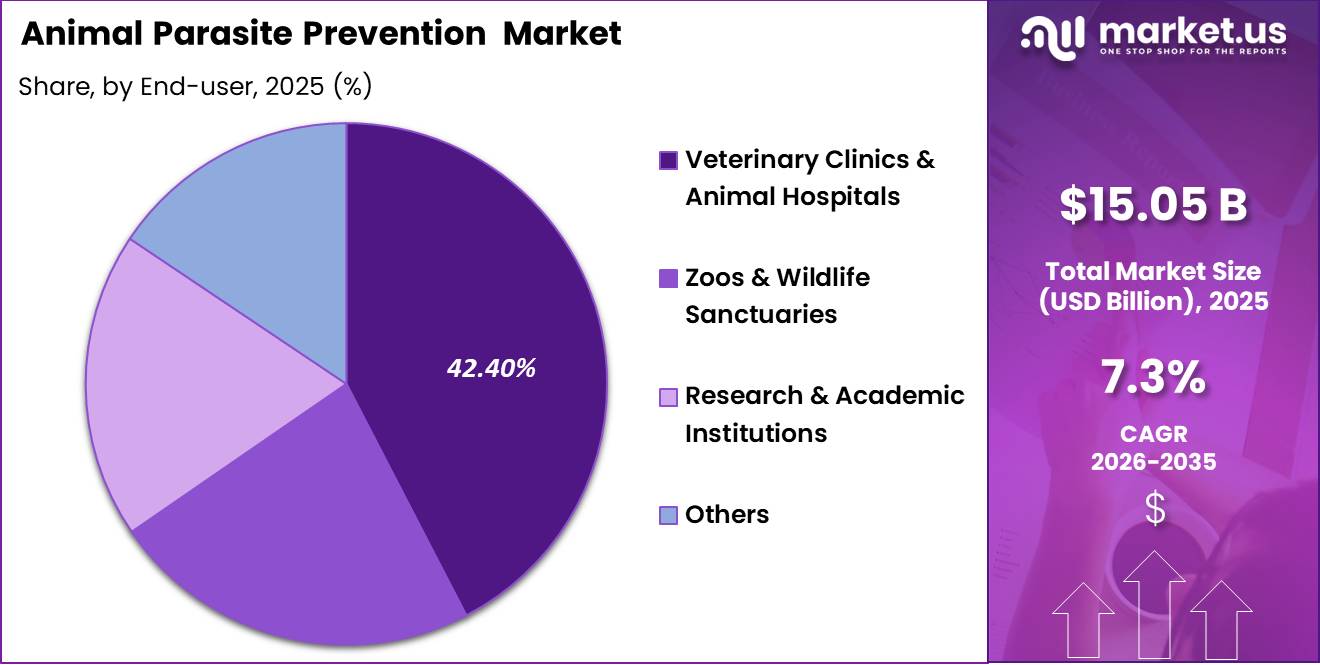

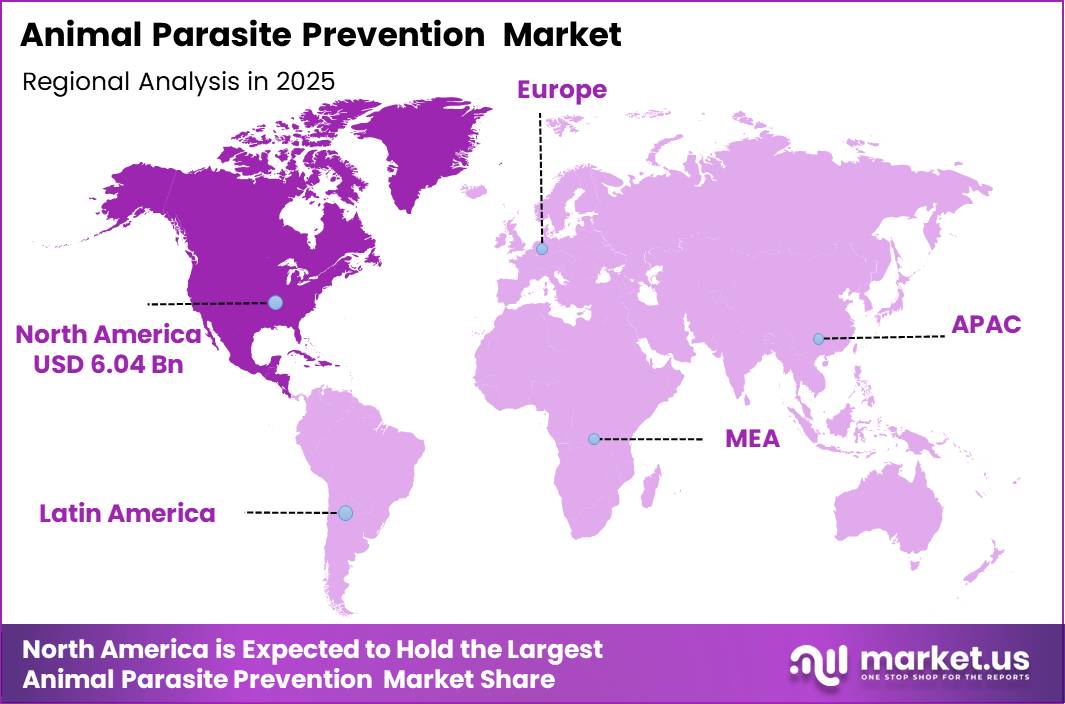

Global Animal Parasite Prevention Market size is expected to be worth around US$ 28.26 Billion by 2035 from US$ 15.5 Billion in 2025, growing at a CAGR of 7.3% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 40.14% share with a revenue of US$ 6.02 Billion.

The Global Animal Parasite Prevention Market comprises veterinary solutions designed to manage internal and external parasitic infestations in companion animals and livestock, ensuring improved health, productivity, and disease control.

- According to a Food and Agriculture Organization (FAO) report from December 2023, global demand for terrestrial animal products is projected to increase by 20% by 2050, creating a structural and expanding long-term demand base for animal parasite prevention products across production animal sectors

FAO estimates current global livestock populations at approximately 22 billion poultry, 1 billion pigs, and 1.6 billion cattle and buffalo, all requiring systematic parasite management to maintain productivity and meet food safety standards.

Technological innovation is transforming the animal parasite prevention market, as AI-powered parasite surveillance platforms and precision dosing systems are being integrated into veterinary practice management tools, improving treatment compliance and early infestation detection across both companion animal and livestock segments.

Key Takeaways

- Market Size: Global Animal Parasite Prevention Market size is expected to be worth around US$ 28.26 Billion by 2035 from US$ 15.5 Billion in 2025.

- Market Share: The market is growing at a CAGR of 7.3% during the forecast period from 2026 to 2035.

- By Product Type: Ectoparasites are identified as the dominant product type, accounting for 49.10% of the market in 2025, driven by high flea, tick, and mite infestation prevalence across companion animal and livestock populations globally.

- By Route of Administration: Topical treatments are confirmed as the dominant route of administration at 42.22%, supported by

- By Animal Type: Companion animals represent the dominant animal type segment at 59.4%, anchored by rising pet ownership rates and increasing per-pet healthcare expenditure across North America and Europe.

- By End User: Veterinary clinics and animal hospitals lead end-user adoption at 42.22%, reflecting their role as the primary point of parasite diagnosis, prescription, and preventive treatment administration.

- Regional Analysis: In 2025, North America led the market, achieving over 40.14% share with a revenue of US$ 6.02 Billion.

By Product Type

Ectoparasites Represent the Dominant Segment in the Market

In 2025, ectoparasites represent the dominant segment having 49.10% share of the global animal parasite prevention market. The segment is driven by the widespread prevalence of external parasites such as fleas, ticks, lice, and mites affecting both companion animals and livestock. These parasites are responsible for significant health issues including skin irritation, allergic dermatitis, anemia, and the transmission of vector-borne diseases such as Lyme disease.

The high frequency of infestations, along with the need for routine and seasonal treatment, contributes to sustained demand across veterinary clinics and livestock farms. Companion animals account for the largest share of treatments, supported by rising pet ownership and increasing expenditure on preventive animal healthcare in developed markets.

Endectocides are the fastest-growing segment in the animal parasite prevention market, owing to their ability to simultaneously control both internal and external parasites through a single treatment. This dual-action effectiveness improves treatment convenience, enhances compliance, and reduces the need for multiple medications.

Their adoption is increasing rapidly in both companion animal and livestock segments, particularly in large-scale farming operations where simplified parasite control protocols are preferred. Additionally, growing concerns over parasite resistance and the demand for broad-spectrum, long-acting solutions are further accelerating the shift toward endectocide-based treatments globally.

By Route of Administration

Topical Treatments Are the Most Widely Used Route of Administration

In 2025, topical treatments accounted for a leading 42.22% share of the Animal Parasite Prevention market by route of administration. This dominance is due to the pre-existing clinical knowledge, easy use without the need for veterinary supervision, and wide availability of topical, spray, and collar formulations for companion animal markets.

Oral medication is the fastest growing route of administration segment. Chewable oral parasiticides, isoxazoline formulations like NexGard, Simparica, and Bravecto, have gained significant market share relative to competing topical formulations due to superior compliance, guaranteed ingestion, and extended label claims protecting against fleas, ticks, as well as many formulations covering heartworm and intestinal parasites. Label expansions in isoxazolines, veterinarian preference for oral over topical compliance-verifiable delivery routes, and innovations driving premiums in the oral parasiticide class are key growth drivers.

By Animal Type

Companion Animals Represent the Dominant Segment in the Market

In 2025, companion animals accounted for a leading 59.4% share of the market by animal type. This dominance is due to the combination of high pet ownership trends worldwide, per-pet higher healthcare spending, and growing human-animal bonding trends that have resulted in higher preventive spending in dogs, cats, horses, and rabbits in North America, Europe, and Asia Pacific.

The dog and cat companion animal subsectors reflect the rise in the adoption of oral isoxazoline parasiticide along with the growth of preventive health treatment protocols for these animals prescribed by veterinarians. An example of such innovation is the Simparica Trio triple-combination parasiticide, which addresses fleas, ticks, heartworm, and intestinal parasites in one monthly chewable.

Livestock and production animals are projected to be the fastest-growing segment in the animal parasite prevention market during the forecast period. Growth is being driven by rising global demand for meat, milk, and other animal-derived products, which is increasing the focus on herd health and productivity.

Farmers are adopting advanced parasite control programs to reduce disease risks, improve feed efficiency, and maintain animal welfare. Growing concerns about parasite resistance and stricter food safety regulations are further supporting demand for effective preventive treatments.

By End User

Veterinary Clinics and Animal Hospitals Are Mostly Utilized in the Market.

In 2025, veterinary clinics and animal hospitals accounted for a leading 42.4% share of the market by end user segment. This dominance is due to their responsibility for diagnosing parasites, distributing parasiticide prescriptions, and administering injections of compound antiparasitics in pets and livestock animals.

In other words, revenue from the sale of veterinary parasiticides from the Simparica, Revolution Plus, and ProHeart lines of Zoetis in the U.S. companion animal market demonstrates the significance of the channel for the distribution of branded parasiticides in the industry.

Zoos and wildlife sanctuaries are emerging as a rapidly growing end-user segment in the animal parasite prevention market due to increasing investments in wildlife conservation and animal health management. Effective parasite control is essential for maintaining the health of captive and rehabilitated animals, preventing disease outbreaks, and reducing the risk of zoonotic transmission.

Growing regulatory standards, conservation funding, and a stronger focus on biodiversity preservation are encouraging wider adoption of preventive parasite management programs across wildlife care facilities worldwide.

Key Market Segments

By Product Type

- Ectoparasites

- Endoparasites

- Endectocides

By Route of Administration

- Topical Treatments

- Oral Medications

- Injectables

- Others

By Animal Type

- Companion Animals

- Livestock / Production Animals

By End User

- Veterinary Clinics & Animal Hospitals

- Zoos & Wildlife Sanctuaries

- Research & Academic Institutions

- Others

Driver

Rising pet ownership and essential care prioritization

The strongest near term volume driver is the continued expansion of the pet base combined with owners’ willingness to preserve core medical spending even when discretionary pet categories soften. In the U.S., pet industry expenditure reached $158 billion in 2025 and is projected at $ 165 billion in 2026, while 95 million households owned at least one pet in 2025.

Dog owning households rose from 51% to 53% year over year, equal to roughly 71 million households, and cat ownership reached 39% of households or about 53 million homes. That matters structurally because parasite prevention sits inside the “essential care” basket rather than impulse product spend, so a larger installed base of dogs and cats directly expands the refill pool for flea, tick, heartworm, and deworming products.

Even when households trade down, prevention is often maintained because the annual cost of parasite prevention remains materially lower than treating advanced heartworm, vector borne disease, or severe ectoparasite infestations. This dynamic preserves recurring demand and supports baseline subscription, clinic reminder, and auto ship business models.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pet ownership and essential-care prioritization | +1.6% | North America core, Western Europe, urban APAC | Short term (≤ 2 years) |

| Tick-borne and zoonotic risk intensification | +1.3% | North America core, EU, temperate APAC corridors | Short term (≤ 2 years) |

| One Health policy alignment and surveillance expansion | +1.0% | North America, EU, Latin America, Asia high-burden zones | Medium term (2-4 years) |

| Broader-spectrum combination parasiticides improving compliance | +1.4% | U.S. core, EU companion animal markets, premium APAC clinics | Medium term (2-4 years) |

| Shift toward year-round prevention in companion animals | +1.2% | U.S., Canada, Western Europe, Australia, Japan | Short term (≤ 2 years) |

| Emerging parasite threats and emergency-use treatment pathways | +0.8% | U.S. South, Latin America interface zones, tropical spill-over markets | Medium term (2-4 years) |

Challenge

Anthelmintic Resistance as a Systemic Constraint on Livestock Parasite Control

Anthelmintic resistance has evolved from isolated reports into a structural challenge for livestock parasite management. Recent studies indicate that nearly all surveyed farms show resistance to at least one drug class, with widespread multi-class resistance to benzimidazoles, levamisole, and macrocyclic lactones in small ruminants, and emerging resistance trends in cattle.

In practice, fecal egg count reduction tests often fall below the 90% efficacy benchmark, leaving 10–40% of treated animals with clinically relevant worm burdens. This translates into measurable productivity losses, including 5–10% lower weight gain, 3–7% reductions in milk yield, and a 1–2 % point increase in mortality or culling in high-exposure herds.Rather than lowering antiparasitic use, resistance has driven adoption of rotation, combination, and targeted selective treatment strategies.

These approaches raise per-animal prevention costs by 15–25% and require additional veterinary visits or diagnostics, prompting some producers to delay premium products or underdose treatments. Collectively, these dynamics reduce potential market growth by an estimated 1.2 % points.Long-term mitigation depends on resistance-aware product design, including novel modes of action, combination therapies, and broader use of on-farm diagnostics.

Standardizing best-practice protocols—accurate weight-based dosing, quarantine and triple therapy for incoming stock, and refugia management—could lower resistance prevalence and treatment variability by 20–30% over a 5–8 year horizon, supported by sustained R&D and stewardship programs.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Rising anthelmintic resistance | -1.2% | Pasture-based livestock regions | Long term (≥ 4 years) |

| Veterinary workforce capacity gap | -0.9% | North America, Europe, Oceania urban & rural | Long term (≥ 4 years) |

| Uneven product & diagnostics access | -0.8% | Emerging markets, rural corridors | Medium term (2-4 years) |

| Climate-driven parasite range shift | -1.0% | Tropics, subtropics, temperate expansion belts | Long term (≥ 4 years) |

| Data & surveillance infrastructure lag | -0.7% | Global, especially mixed farming systems | Medium term (2-4 years) |

| Cost pressure on integrated prevention | -0.6% | Low-margin livestock, low-income pet owners | Short term (≤ 2 years) |

Restraints

Regulatory Tightening as a Drag on Veterinary Antimicrobial Market Growth

Regulatory tightening on veterinary antimicrobials has emerged as a meaningful restraint on market growth, particularly in regions formalizing stewardship and surveillance frameworks. Authorities such as the U.S. Food and Drug Administration have shifted medically important antimicrobials from OTC to prescription status and imposed clearer limits on duration and indications of use. This restricts mass metaphylactic and prophylactic applications that historically supported high-volume sales.

Between 2024 and 2028, the US, EU, and advanced APAC markets are converging on stricter controls, mandatory veterinary oversight, and enhanced reporting through systems such as National Antimicrobial Resistance Monitoring System, reducing the accessible volume pool for broad-spectrum products by an estimated 10–15% in food-animal segments while increasing farm- and distributor-level compliance costs.

For manufacturers, incremental label tightening and guidance raise regulatory and pharmacovigilance opex by 1–2%, extend approval timelines by 6–12 months, and increase post-marketing surveillance costs, eroding NPV and delaying revenue realization.

Concurrently, veterinarians are shifting toward shorter courses and alternatives such as vaccines and biosecurity, cutting treatment days per animal by 10–20%. Collectively, these factors translate into an estimated 1.5 %-point CAGR reduction, particularly in North America and the EU, and are forcing a strategic pivot toward higher-value, differentiated, and service-integrated preventive offerings.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising antiparasitic resistance & AMR controls | -2.0% | EU, North America, China, India | Long term (≥ 4 years) |

| Regulatory tightening on veterinary antimicrobials | -1.5% | North America core, EU, selected APAC | Medium term (2-4 years) |

| Input cost inflation & margin compression | -1.2% | Global, with higher impact in LATAM, Africa, India | Short–Medium term (≤ 4 years) |

| Distribution & cold-chain gaps in emerging markets | -1.0% | Sub-Saharan Africa, South & Southeast Asia, rural LATAM | Long term (≥ 4 years) |

| Veterinarian capacity and compliance bottlenecks | -0.8% | North America, EU, India, China | Medium–Long term (≥ 3 years) |

| Slow adoption of preventive protocols in livestock | -1.0% | Asia (ex-Japan), Africa, parts of LATAM | Long term (≥ 4 years) |

Opportunity

Long Acting Resistance Oriented Antiparasitic Portfolios as a Future Growth Lever

Long acting antiparasitic portfolios designed explicitly for resistance management represent a significant future opportunity, as current growth remains concentrated in conventional dewormers and ectoparasiticides despite rising resistance pressure.

Regulators and bodies such as the U.S. Food and Drug Administration increasingly emphasize that antiparasitic resistance cannot be fully halted and are advancing formal resistance management frameworks. This creates scope for products optimized for stewardship rather than short term efficacy alone.

By shifting toward injectable or implant formulations that extend dosing intervals from monthly to quarterly or biannual schedules, and pairing them with non drug practices such as pasture rotation and stocking density management, manufacturers can reduce treatment frequency per animal by 20 to 30 % while maintaining control outcomes.

Although volumes decline, revenues can be preserved through premium SKUs that carry 5 to 10 % point higher gross margins and lower logistics intensity. Even modest adoption around 25 to 30 % of cattle, sheep, and goat herds in North America, the EU, and export oriented Latin America of resistance labeled stewardship lines could generate USD 1.0 to 1.5 billion in incremental revenues by 2035.

As stewardship guidance becomes more formalized and monetized through labeling, bundled diagnostics, and resistance guarantees, such portfolios could command 20 to 25 % price premiums and add roughly 1.8 % points to market CAGR in high resistance regions.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| One Health sentinel surveillance platforms | +2.0% | North America, EU, East Asia | Medium term (2-4 years) |

| Long-acting, resistance-oriented antiparasitic portfolios | +1.8% | North America, EU, Latin America | Medium term (2-4 years) |

| Digital adherence & risk-scoring subscriptions | +1.5% | North America core, EU, urban APAC | Short term (≤ 2 years) |

| Integrated herd health & pasture management bundles | +1.3% | Latin America, Sub-Saharan Africa, South Asia | Long term (≥ 4 years) |

| Human–animal co-protection and travel health channels | +1.0% | North America, EU, GCC, East Asia | Medium term (2-4 years) |

| Novel biologics & vaccines for zoonotic parasites | +1.5% | Global, with EM focus | Long term (≥ 4 years) |

Geopolitical Impact Analysis

U.S.-China Trade Tensions and New World Screwworm Outbreak Are Introducing Supply Chain and Biosecurity Pressures Across the Global Animal Parasite Prevention Market

Two developments in geopolitics and biosecurity are driving tangible short-term disruption in the Animal Parasiticide Prevention market in 2026. Firstly, the increasing trade tensions between the United States and China are adding cost pressures on the pharmaceutical ingredient and packaging supply chains, due to the sourcing of the active pharmaceutical ingredients in antiparasitic medicines from Asia being subject to increased tariffs.

Secondly, and more relevantly to the markets, the outbreak of the New World screwworm in North American cattle is causing an emergency parasiticide intervention, which is generating incremental demand for cattle parasiticide, as Zoetis confirmed in its Q1 2026 SEC filings as part of an increase in targeted parasiticide use.

USDA-APHIS has invested more than US$ 172 million since 2019 through animal disease preparedness and response programs designed to strengthen the United States’ ability to prevent, detect, and respond to high-consequence animal disease outbreaks. These investments support biosecurity measures, emergency response planning, diagnostic laboratory capacity, and vaccine preparedness.

As a result, animal health companies in 2026 are operating in an environment shaped by both heightened disease-control efforts and ongoing trade policy uncertainty, creating a market dynamic characterized by rising demand for parasite prevention solutions alongside increasing operational and supply chain costs.

Regional Analysis

North America Held the Largest Share of the Global Animal Parasite Prevention Market

In 2025, North America dominated the global Animal Parasite Prevention market, holding about 40.14% of total global revenue. This dominance is supported by high penetration of branded parasiticide products, advanced veterinary healthcare infrastructure, and strong regulatory oversight governing animal health pharmaceuticals.

The region also benefits from a large companion animal population and a significant livestock base requiring continuous parasite management. The United States plays a central role, supported by well-established veterinary diagnostic networks and widespread adoption of preventive healthcare practices for animals.

Europe represents the second-largest market, driven by strict regulatory standards for veterinary medicines under the European Medicines Agency framework, strong food safety and residue monitoring systems, and high levels of companion animal ownership.

Asia-Pacific is emerging as the fastest-growing regional market due to rising livestock production, expanding pet ownership in urban areas, and improving veterinary healthcare access in countries such as China and India. Latin America also shows steady growth, supported by its large cattle industry, while the Middle East and Africa remain developing markets with increasing focus on animal health and productivity improvements.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The Global Animal Parasite Prevention Market is an example of a competitive market that possesses the characteristics of consolidation and oligopoly, given that there are very few global companies involved in animal health with high revenue volumes in the market.

Notable companies like Zoetis Inc., Merck Animal Health, Boehringer Ingelheim Animal Health, and Elanco Animal Health dominate the market due to their wide product ranges comprising of ectoparasiticides, endoparasiticides, and endectocides used on both companion animals and livestock.

Their competitive strengths come from having efficient distribution channels, strong brand power, regulatory experience, and ongoing development of new products. The emergence of endectocides which are more versatile has increased the competitiveness of key players because of their effectiveness in controlling parasites.

Besides these top companies, other organizations such as Virbac S.A., Ceva Santé Animale, Vetoquinol S.A., Dechra Pharmaceuticals, Phibro Animal Health, Norbrook Laboratories, and Bimeda Animal Health operate within select geographic regions and animal species sectors. Most of these organizations specialize more on selective areas than global operations.

An increase in generic rivalry has been experienced in some categories of products, especially in matured markets owing to expiration of patent rights for many of the existing ectoparasiticides and anthelmintics. Despite this development, there still exists a strong oligopoly within the industry owing to domination by a few global animal health companies.

Top Key Players

- Zoetis Inc.

- Merck & Co., Inc. (Merck Animal Health)

- Boehringer Ingelheim International GmbH

- Elanco Animal Health Incorporated

- Bayer AG (Animal Health Division)

- Virbac S.A.

- Ceva Santé Animale

- Vetoquinol S.A.

- Dechra Pharmaceuticals Plc

- Phibro Animal Health Corporation

- Norbrook Laboratories Ltd.

- Neogen Corporation

- Biogénesis Bagó S.A.

- Bimeda Animal Health

- Himalaya Wellness Company

- Other Players

Key Development

- In May 2026, Zoetis reported Q1 2026 revenue of US$ 2.3 billion a 3% increase versus Q1 2025 with livestock product sales growing 7% year-on-year, driven by expanded targeted use of parasiticides in response to the New World screwworm outbreak and broad-based strength across cattle, poultry, and swine.

- In June 2026, Merck Animal Health announced the acquisition of Targan, strengthening its portfolio in advanced animal health and precision livestock solutions relevant to parasite prevention. The acquisition supports improved livestock productivity, biosecurity, and next-generation farm management technologies, aligning with growing demand for integrated parasiticide and animal health innovation across global markets.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 15.05 Billion |

| Forecast Revenue (2035) | US$ 28.26 Billion |

| CAGR (2026-2035) | 7.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Ectoparasites, Endoparasiticides, Endectocides), By Route of Administration (Topical Treatments, Oral Medications, Injectables, Others), By Animal Type (Companion Animals and Livestock/Production Animals), By End User (Veterinary Clinics & Animal Hospitals, Zoos & Wildlife Sanctuaries, Research & Academic Institutions, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Zoetis Inc., Merck & Co., Inc. (Merck Animal Health), Boehringer Ingelheim International GmbH, Elanco Animal Health Incorporated, Bayer AG (Animal Health Division), Virbac S.A., Ceva Santé Animale, Vetoquinol S.A., Dechra Pharmaceuticals Plc, Phibro Animal Health Corporation, Norbrook Laboratories Ltd., Neogen Corporation, Biogénesis Bagó S.A., Bimeda Animal Health, Himalaya Wellness Company, and Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |