Quick Navigation

Report Overview

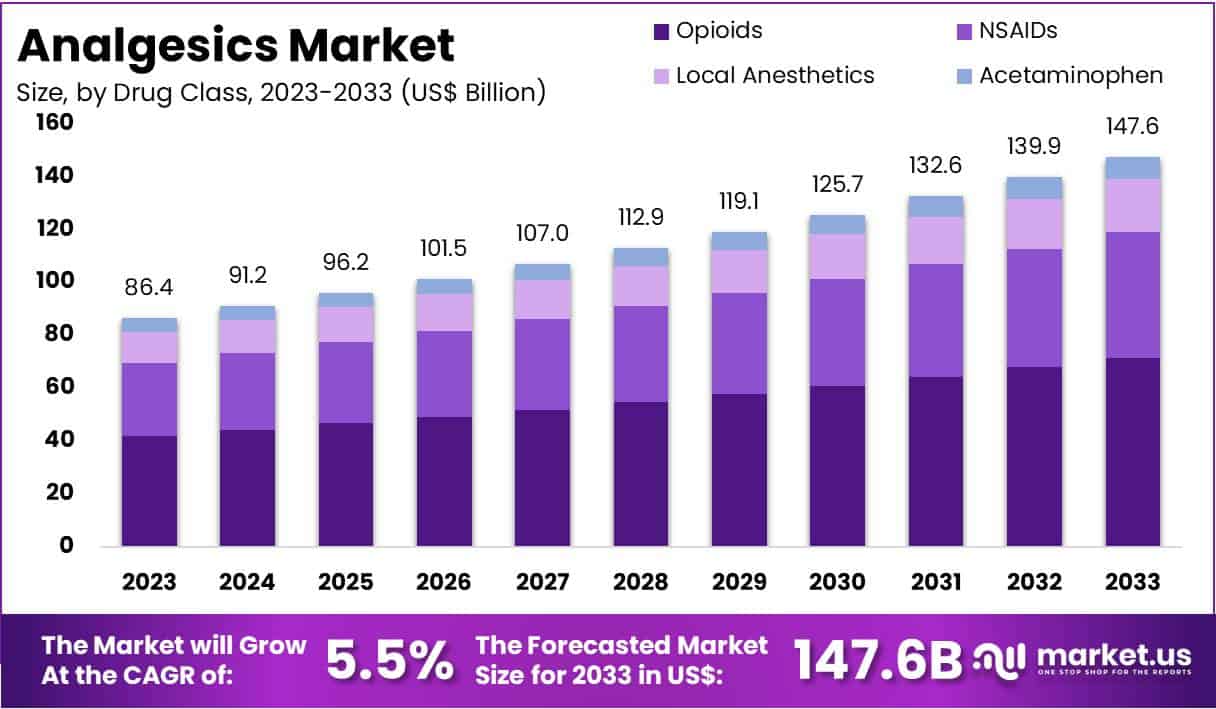

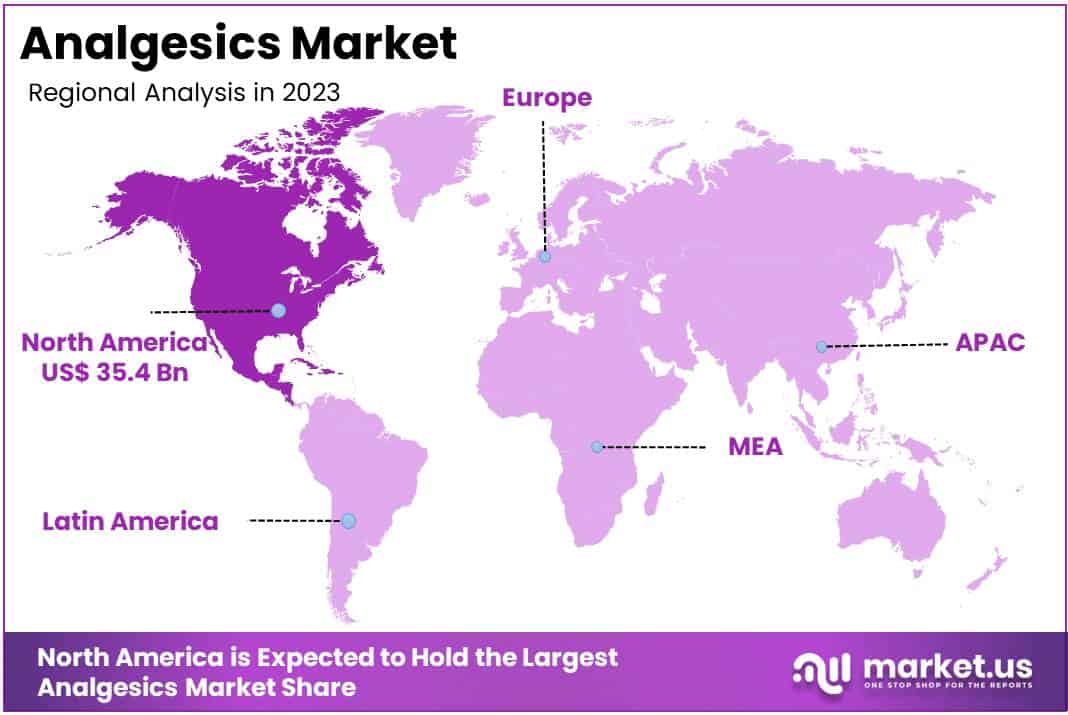

The Global Analgesics Market size is expected to be worth around US$ 147.6 Billion by 2033, from US$ 86.4 Billion in 2023, growing at a CAGR of 5.5% during the forecast period from 2024 to 2033. North America accounted for over 41% of the global analgesics market, which was valued at US$ 35.4 billion.

Analgesics, commonly referred to as pain relievers, are a class of drugs designed to alleviate pain without causing loss of consciousness. They are among the most commonly used pharmaceuticals for managing acute and chronic pain and inflammation.

The global analgesics market is experiencing robust growth, driven primarily by an aging demographic and an uptick in chronic health conditions necessitating effective pain management solutions. According to data from the Centers for Disease Control and Prevention (CDC), about 49.9% of the U.S. population used at least one prescription drug in the last 30 days between 2017 and March 2020, with analgesics being among the most frequently prescribed during physician visits. The market is delineated by type, application, and distribution channels, including hospital and retail pharmacies and online platforms.

Demand for both opioid and non-opioid analgesics is on the rise. For instance, CDC data from 2013 to 2016 reveals that approximately 6.5% of U.S. adults aged 20 and over used prescription opioid analgesics in the previous 30 days, with higher usage among older adults. Non-opioid analgesics, such as NSAIDs and acetaminophen, are preferred for mild to moderate pain due to their lower dependency risks compared to opioids, which are essential for managing moderate to severe pain despite their addiction and dependency risks.

The analgesics market faces challenges, especially regulatory obstacles related to opioids due to their abuse potential. For example, a study by Anesthesiology indicated that 20% to 56% of patients might develop chronic pain after surgery, with about 10% experiencing severe chronic pain that impairs functionality. Additionally, JAMA Network research shows that between 20% and 60% of individuals might transition from acute to chronic opioid use after surgical procedures, emphasizing the need for strict regulations.

Significant growth opportunities exist in the analgesics market, particularly through ongoing research and development aimed at creating new analgesics with fewer side effects. Advances in personalized medicine are also paving the way for more targeted pain management strategies, which could improve patient outcomes and expand market potential. According to Nutrition Facts, adopting diets rich in anti-inflammatory foods can lead to a substantial decrease in cancer risks, with a 75% reduction in cancer incidence and a 67% decrease in cancer mortality, highlighting a growing consumer awareness of holistic and preventive health approaches.

The analgesics market shows a promising future, driven by advancements in drug development and a growing focus on managing chronic and post-surgical pain. However, regulatory policies targeting prescription abuse, especially in the opioid segment, will shape its evolution. According to Adelaide Now, chronic pain affects 3.4 million Australians, with 68% of them being of working age, highlighting a substantial economic burden. For instance, innovation in pain therapies and stricter regulations will influence market dynamics, creating opportunities and challenges for industry players.

Key Takeaways

- Global Analgesics Market projected to expand from US$ 86.4 billion in 2023 to US$ 147.6 billion by 2033, at a CAGR of 5.5%.

- Opioids dominate the analgesics drug class, capturing over 48.5% of the market in 2023, primarily used for severe pain management.

- NSAIDs and Acetaminophen, used for mild to moderate pain, continue to hold significant market share due to affordability and safety.

- Local anesthetics are increasingly utilized in outpatient procedures, supporting growth in localized pain management solutions.

- Surgical pain management remains the largest segment, constituting over 48.9% of the analgesics market in 2023 due to high global surgical volume.

- Prescription analgesics hold a dominant share of over 74.2%, driven by the need to treat moderate to severe pain conditions.

- Oral analgesics are preferred for their convenience, making up more than 46.1% of the market, favored for at-home treatment.

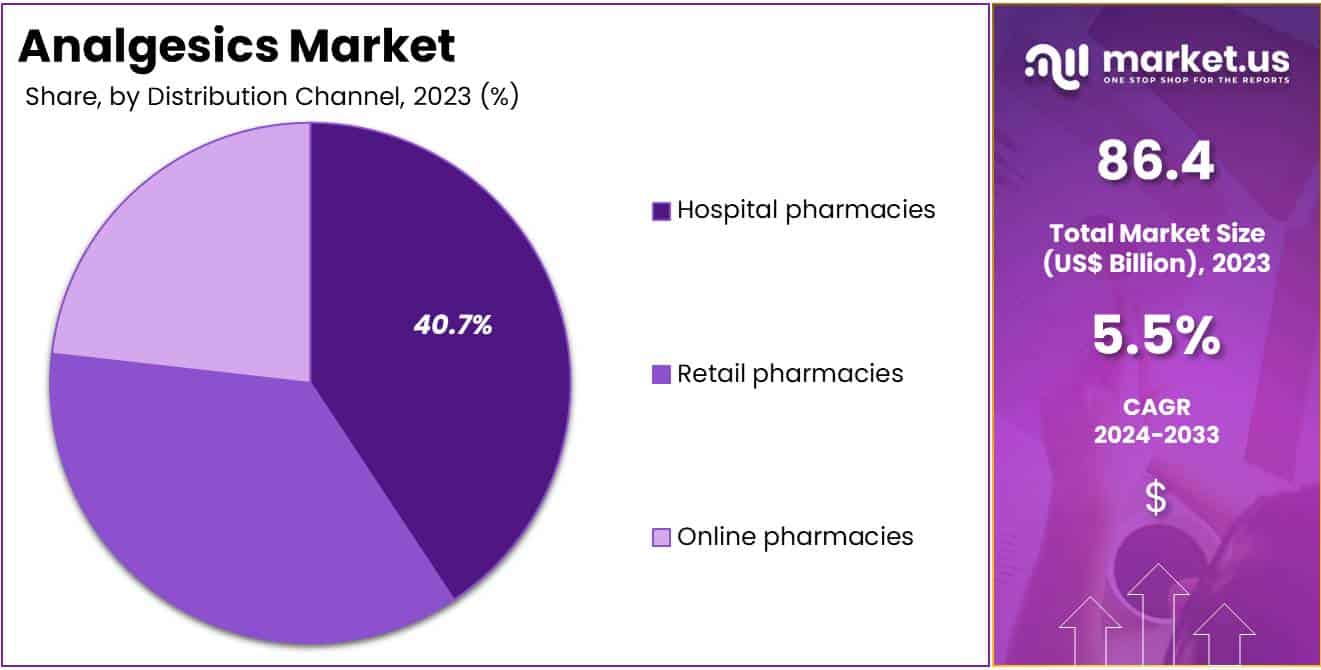

- Hospital pharmacies are the leading distribution channel, representing over 40.7% of the market, crucial for controlled pain management.

- North America leads the analgesics market with more than 41% share in 2023, propelled by advanced healthcare infrastructure and high expenditure.

Drug Class Analysis

In 2023, the Opioids segment held a dominant market position in the Drug Class Segment of the Analgesics Market, capturing more than a 48.5% share. Opioids are strong painkillers used to treat severe pain. These include Morphine, Fentanyl, Codeine, Methadone, and others. They are often prescribed for acute pain, cancer-related pain, and post-surgical pain. Despite their effectiveness, opioids face increasing scrutiny due to their addiction potential and risk of overdose.

Another significant segment is NSAIDs (Non-Steroidal Anti-Inflammatory Drugs). This class includes popular pain relievers like Ibuprofen, Naproxen, and Diclofenac. NSAIDs are used for mild to moderate pain, including headaches and joint pain. They also reduce inflammation and fever. Due to their affordability and widespread availability, NSAIDs continue to hold a strong market share. They are considered safer than opioids for managing long-term, non-severe pain.

Acetaminophen, also known as Paracetamol, remains a key player in the analgesics market. This drug is commonly used for mild pain relief and fever reduction. Acetaminophen is found in many over-the-counter products, often in combination with other drugs. It is especially popular for headaches, minor injuries, and flu symptoms. Its accessibility and low risk of addiction make it a preferred choice for treating everyday pain in the global market.

The Local Anesthetics segment also contributes significantly to the analgesics market. Local anesthetics like Lidocaine and Bupivacaine are used to numb specific areas of the body. These drugs are commonly applied during dental procedures, minor surgeries, and labor. Their growing use in outpatient settings has driven market growth. As demand for localized pain management rises, this segment is expected to see steady expansion in the coming years.

Indication Analysis

In 2023, the Surgical Pain segment held a dominant market position in the Indication Segment of the Analgesics Market, capturing more than 48.9% of the market share. Surgical pain management is critical due to the high number of surgeries conducted worldwide. Post-operative pain is common, and effective analgesics are essential for a smooth recovery. This segment remains the largest contributor to the analgesics market as patients require ongoing pain relief after surgery.

Following surgical pain, cancer pain also plays a significant role in the analgesics market. Cancer-related pain is often severe and can persist throughout treatment. Managing this pain requires a combination of medications, including opioids and non-opioids. The increasing global incidence of cancer is driving demand for specialized analgesics to provide relief to patients suffering from chronic and debilitating pain.

Neuropathic pain represents another key segment within the market. This type of pain arises from nerve damage and is notoriously difficult to treat. Analgesic treatments for neuropathic pain include anticonvulsants, antidepressants, and topical medications. With the rising prevalence of conditions such as diabetes and shingles, the demand for effective treatments to manage neuropathic pain continues to increase, contributing to market growth.

Other pain indications, such as musculoskeletal pain, arthritis, and chronic back pain, also contribute to the overall market. These conditions are widespread, especially among older populations, and they require long-term pain management. Both prescription and over-the-counter analgesics are commonly used to treat these types of pain, ensuring steady demand for pain relief solutions in the market across various demographics.

Type Analysis

In 2023, the Prescription segment held a dominant market position in the Type Segment of the Analgesics Market, capturing more than 74.2% of the share. This reflects a strong demand for prescription medications used to manage moderate to severe pain. Prescription analgesics are typically recommended for conditions like cancer pain, arthritis, and post-surgical recovery. These drugs are designed to provide effective relief for pain that cannot be controlled by over-the-counter options.

Prescription analgesics include opioids, NSAIDs, and other potent pain relievers. These medications are prescribed by healthcare professionals for their ability to treat more intense pain. The aging population and the increasing prevalence of chronic pain conditions are key factors driving the growth of this segment. As people live longer and develop more age-related ailments, the need for prescription-strength pain relief continues to rise.

The Over-the-Counter (OTC) segment also plays an important role in the analgesics market. OTC analgesics, such as ibuprofen, acetaminophen, and aspirin, are used for mild to moderate pain. These products are easily available without a prescription, making them popular for conditions like headaches, muscle aches, and minor injuries. The convenience and accessibility of OTC medications contribute to the steady growth of this market segment.

However, the Prescription segment remains the dominant force in the overall market. Stronger pain relief options, often necessary for chronic or severe pain, continue to drive the preference for prescription medications. While the OTC market grows, prescription analgesics are essential for patients requiring more specialized and potent pain management solutions. The dominance of the Prescription segment reflects its crucial role in treating complex pain conditions.

Route of Administration Analysis

In 2023, the Oral segment held a dominant market position in the Route of Administration Segment of the Analgesics Market, capturing more than a 46.1% share. Oral analgesics, such as tablets, capsules, and liquids, remain the most commonly used. This route is preferred due to its ease of use and convenience. Patients can easily take medications at home, without the need for medical assistance, making it a popular choice for treating mild to moderate pain.

The Parenteral segment includes injections and infusions, which are commonly used in hospitals and emergency settings. These analgesics offer fast pain relief, making them ideal for severe pain or situations where oral medications are not feasible. Parenteral analgesics are also crucial for patients who need immediate pain management or for those who cannot swallow pills. The demand for this segment remains strong, especially in critical care environments.

Transdermal analgesics, delivered through patches applied to the skin, are increasingly popular, particularly for managing chronic pain. These patches provide a steady release of medication, offering long-term pain relief without the need for frequent doses. Transdermal analgesics are often used for conditions like arthritis or chronic back pain. As the preference for non-invasive treatments grows, the transdermal route is expected to see continued market expansion in the coming years.

Other routes of administration, such as rectal, inhalation, and sublingual, also play a role in the analgesics market. These methods are used when oral or parenteral routes are not suitable for certain patients or specific conditions. While less common, these alternatives are essential for targeted pain relief in unique situations. Overall, the analgesics market continues to evolve, with each route of administration serving distinct needs in pain management.

Distribution Channel Analysis

In 2023, the hospital pharmacies segment held a dominant market position in the Distribution Channel Segment of the Analgesics Market, capturing more than 40.7% of the market share. This strong performance is driven by the increasing number of patients seeking pain relief in hospitals. Hospital pharmacies provide prescription analgesics for both acute and chronic pain. They also benefit from a controlled environment, where medications are administered under professional supervision, ensuring better patient adherence to prescribed treatments.

The retail pharmacies segment also plays a significant role in the distribution of analgesics. Retail pharmacies are widely accessible and cater to a broad range of customers. Over-the-counter (OTC) pain relievers, such as those for headaches or muscle pain, are commonly sold through these channels. Their accessibility and convenience have helped drive consumer demand. As a result, retail pharmacies continue to maintain a strong position in the analgesics market, meeting the needs of everyday consumers seeking pain relief.

Online pharmacies have emerged as an increasingly important distribution channel. The rise of e-commerce and digital healthcare platforms has contributed to their growth. Online pharmacies offer the convenience of home delivery, which appeals to many consumers. Customers can order analgesics from the comfort of their homes, ensuring privacy and ease. Additionally, the ability to compare prices online and access a wide variety of products has fueled the popularity of this distribution channel in recent years.

Key Market Segments

By Drug Class

- Opioids

- Morphine

- Fentanyl

- Codiene

- Methadone

- Meperidine

- Oxycodone

- Tramadol

- Dextromethorphan

- Buprenorphine

- Others

- NSAIDs

- Local Anesthetics

- Acetaminophen

By Indication

- Surgical Pain

- Cancer Pain

- Neuropathic Pain

- Others

By Type

- Prescription

- OTC

By Route of Administration

- Oral

- Parenteral

- Transdermal

- Others

By Distribution Channel

- Hospital pharmacies

- Retail pharmacies

- Online pharmacies

Drivers

Increasing Prevalence of Chronic Pain

The analgesic market is significantly influenced by the escalating prevalence of chronic pain globally. Data from the Good Body suggests that at least 10% of the world’s population suffers from chronic pain, with this figure rising to 20.9% among US adults alone. Chronic conditions such as arthritis, recognized as the leading chronic pain condition, contribute heavily to this increasing demand for pain management solutions.

The economic impact is also notable, with chronic pain costing the US economy up to $635 billion annually, a figure that underscores the extensive need for effective analgesic interventions. This growing burden of chronic pain not only enhances the demand for existing pain relief solutions but also stimulates the continuous development and dissemination of new analgesic formulations aimed at improving patient quality of life.

Advancements in Drug Development

The development of the analgesics market is further propelled by advancements in drug development, driven by the need to address the extensive burden of chronic pain. Innovations in analgesic solutions, such as targeted pain relief and extended-release formulations, are pivotal in enhancing patient compliance and outcomes. A study from the National Institutes of Health highlights the persistence of chronic pain, with a considerable percentage of patients continuing to experience pain over time, which underscores the critical need for effective long-term treatment strategies.

These advancements are not only enhancing the effectiveness of pain management but also reducing potential side effects, thereby improving the overall quality of care provided to patients with chronic pain conditions.

Restraints

Regulatory Scrutiny and Opioid Crisis

The analgesic market in North America is navigating major obstacles due to strict regulatory oversight and the opioid crisis. Recent reports indicate that in 2022, overdose deaths from both illicit and prescribed drugs exceeded 109,000. This alarming trend has prompted regulators to tighten the rules governing opioid prescriptions. These changes aim to curb the misuse of potent pain medications and address the ongoing public health crisis.

In response to the growing opioid epidemic, regulatory bodies have removed the X-waiver requirement for prescribing buprenorphine. This modification is designed to increase treatment accessibility for individuals struggling with opioid use disorder (OUD). Additionally, new regulations enhance patient rights by protecting them against insurance discrimination related to mental health and substance use disorder treatments. These efforts reflect a commitment to improve public health safety and patient care.

Adverse Effects of Pain Medication

The adverse effects of long-term pain medication usage have significantly impacted market growth. These include severe gastrointestinal problems, increased cardiovascular risks, and dependency issues. As a result, both healthcare providers and patients are becoming more cautious about using these medications. This caution is evident in their hesitancy to opt for long-term analgesic treatments unless absolutely necessary.

In response to the growing concern over opioid overdoses, the FDA approved naloxone for over-the-counter sales in 2023. This decision aims to broaden community access to immediate, lifesaving treatments. The move reflects an urgent need to address the opioid crisis and provides a significant tool for emergency response in cases of overdose.

Opportunities

Growing Demand for Non-Opioid Pain Relievers

The demand for non-opioid pain relievers is witnessing significant growth, driven primarily by the ongoing opioid crisis. With opioid-related addiction and overdose deaths becoming a public health emergency, there is a notable shift towards safer alternatives for pain management. According to the Centers for Disease Control and Prevention (CDC), nearly 70% of all drug overdose deaths in the U.S. in 2020 involved opioids, which has spurred the search for non-addictive pain management solutions. In response, there is an increasing emphasis on developing novel analgesic drugs that provide effective pain relief without the risk of dependence or addiction associated with opioids.

Non-opioid analgesics such as NSAIDs, acetaminophen, and emerging therapies like neuropathic pain agents are gaining popularity as safer alternatives. For instance, a study published by the National Institute on Drug Abuse (NIDA) found that non-opioid therapies such as lidocaine patches and cannabinoids could offer effective pain relief without the risk of addiction.

Additionally, the U.S. Food and Drug Administration (FDA) is also actively encouraging pharmaceutical companies to innovate in this area, offering regulatory incentives for drugs that reduce reliance on opioids. As healthcare providers and patients become more cautious about opioid use, the non-opioid analgesic market is expected to grow significantly.

Expansion in Emerging Markets

Emerging markets present a substantial growth opportunity for the global analgesics industry, driven by improving healthcare access, increasing disposable incomes, and rising awareness of pain management. According to the World Health Organization (WHO), nearly 80% of people in low- and middle-income countries do not have access to essential pain management services. However, the situation is rapidly changing. In countries like India, Brazil, and China, healthcare infrastructure is expanding, and a growing middle class is fueling demand for healthcare services, including pain management.

Trends

Advancements in Genomic Profiling for Pain Management

The trend towards personalized pain management is gaining momentum with genomic profiling at the forefront. This approach involves tailoring pain management strategies based on individual genetic profiles, which can significantly enhance treatment efficacy and patient satisfaction.

By analyzing genetic variations, healthcare providers can predict a patient’s response to certain pain medications, thereby minimizing trial and error and reducing adverse drug reactions. For instance, genomic data can guide the use of non-pharmacological interventions and predict chronic pain risk, which helps in applying preemptive measures for at-risk patients.

Despite the potential benefits, challenges such as the cost of genomic testing, complexity of genetic interactions, and concerns about data privacy remain significant barriers to mainstream clinical integration.

Integration of Digital Tools in Pain Management

Digital health technologies, including mobile health apps and telemedicine, are reshaping pain management landscapes. These tools facilitate continuous patient monitoring and pain assessment, enhancing compliance and treatment outcomes. The integration of digital tools allows for the collection of extensive data on patient pain levels and responses to treatments in real-time, offering a dynamic platform for personalized treatment adjustments. This trend is particularly vital in managing chronic pain, where ongoing assessment is crucial for effective treatment.

The Role of Pharmacogenetics in Pain Management

Pharmacogenetics is also pivotal in personalizing pain management. This field allows for tailored drug therapy based on genetic markers that influence drug metabolism and pain sensitivity. For example, variations in genes like OPRM1 and CYP2C9 can affect how a patient processes opioids and other analgesics, influencing both the effectiveness and risk of addiction. Pharmacogenetic testing can thus be used to optimize dosages and choose the most suitable drugs, reducing the likelihood of side effects and improving pain management outcomes.

Regional Analysis

In 2023, North America captured more than 41% of the global analgesics market, with a market value of US$ 35.4 billion. The region’s strong position is largely attributed to its advanced healthcare infrastructure and high levels of healthcare spending. With a large, aging population and an increase in chronic pain conditions, the demand for pain relief solutions continues to rise. The United States, in particular, plays a major role in maintaining North America’s dominance in the global market.

Several factors are driving this growth. North America’s healthcare system makes it easier for people to access pain management treatments. The wide availability of both prescription and over-the-counter analgesics ensures that pain relief options are readily accessible. Additionally, the rise in pain-related conditions such as arthritis and back pain is fueling demand. This is particularly true as the population continues to age, which increases the need for effective pain management solutions.

Growing awareness about pain relief options also supports market growth in North America. As more people understand the importance of managing pain effectively, they are turning to analgesics to help alleviate their symptoms. Moreover, strong distribution networks throughout the region ensure that pain relief products are easily available. Pharmaceutical companies actively market their products, reaching a broad consumer base. This further boosts the demand for analgesics in the region.

North America is expected to maintain its dominant market share in the coming years. The combination of increasing chronic pain conditions, an aging population, and a robust healthcare system ensures continued growth. Moreover, innovations in pain relief products and a rising preference for self-medication will likely support the market’s future development. North America’s position will remain crucial in shaping the global analgesics landscape moving forward.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The analgesics market is highly competitive and features several dominant players. Companies like Abbott and Pfizer Inc. are notable for their extensive range of pain management products. Abbott excels in both oral and topical analgesics, along with innovative pain relief technologies. Pfizer, recognized for its effective pain relief medications, focuses on developing new analgesic drugs that promise enhanced efficacy with fewer side effects. Both companies leverage their global reach to serve diverse markets effectively, ensuring they remain at the forefront of the industry.

Eli Lilly & Company and Endo International plc are also significant contributors to the analgesics market. Eli Lilly is renowned for its focus on both chronic and acute pain treatments, advancing pain therapy with novel compounds and non-opioid solutions. Endo, despite challenges associated with the opioid crisis, is making strides in non-addictive pain management options. Their efforts are geared towards providing safer alternatives to traditional opioid treatments, highlighting a shift towards more responsible pain management solutions.

F. Hoffmann-La Roche AG is another key player, emphasizing targeted therapies for specific pain conditions like cancer and neuropathic pain. Roche’s approach includes leadership in biologic therapies and ongoing research into novel drug delivery systems. This focus ensures they continue to offer personalized pain management solutions, keeping them competitive in a rapidly evolving market.

In addition to these major corporations, the market includes a variety of other key players, such as generics manufacturers and emerging biotech firms. Companies like Johnson & Johnson, GlaxoSmithKline, and Merck & Co. also play a pivotal role, with a broad product range that caters to different pain types. The rise of digital health solutions and over-the-counter remedies has further diversified the market, intensifying the competition and driving innovation across the board.

Analgesics Market Key Players Are

- Abbott

- Pfizer Inc.

- Eli Lilly & Company

- Endo International plc

- F. Hoffmann-La Roche AG

- Bausch Health Companies Inc.

- Merck & Co. Inc.

- AbbVie Inc.

- Novartis AG

- Johnson & Johnson

- GSK plc.

- Purdue Pharma L.P.

- Sun Pharmaceutical Industries Ltd

- Sanofi

Recent Developments

- In October 2024: Eli Lilly announced a significant investment of $4.5 billion to establish the Lilly Medicine Foundry. This new facility is designed to enhance their manufacturing capabilities and accelerate the development and global supply of their pharmaceutical products. This move reflects the company’s commitment to innovation and meeting the growing demand for their medications.

- In July 2024: Johnson & Johnson updated its financial guidance for the year, reflecting improved performance indicators and the impact from the recent acquisition of V-Wave, a move that potentially broadens its operational scope in healthcare innovations. As part of their third quarter 2024 results, Johnson & Johnson reported a global sales increase to $22.5 billion, with a significant 6.3% operational growth. This includes contributions from both their Innovative Medicine and MedTech segments, which involves products applicable to pain management.

- In September 2023: Abbott acquired Bigfoot Biomedical, a company at the forefront of developing smart insulin management systems. This move expands Abbott’s capabilities in diabetes care, complementing its existing FreeStyle Libre® portfolio of continuous glucose monitoring systems. The acquisition is aimed at advancing more personalized and precise diabetes management solutions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 86.4 Billon |

| Forecast Revenue (2033) | US$ 147.6 Billion |

| CAGR (2024-2033) | 5.5% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Drug Class [Opioids (Morphine, Fentanyl, Codiene, Methadone, Meperidine, Oxycodone, Tramadol, Dextromethorphan, Buprenorphine, Others), NSAIDs, Local Anesthetics, Acetaminophen], By Indication (Surgical Pain, Cancer Pain, Neuropathic Pain, Others), By Type (Prescription, OTC), By Route of Administration (Oral, Parenteral, Transdermal, Others), By Distribution Channel (Hospital pharmacies, Retail pharmacies, Online pharmacies) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Abbott, Pfizer Inc., Eli Lilly & Company, Endo International plc, F. Hoffmann-La Roche AG, Bausch Health Companies Inc., Merck & Co. Inc., AbbVie Inc., Novartis AG, Johnson & Johnson, GSK plc., Purdue Pharma L.P., Sun Pharmaceutical Industries Ltd, Sanofi |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |