Global Agriculture Termite Control Market Size, Share, And Industry Analysis Report By Product Type (Chemical Termiticides, Biological Termiticides), By Crop Type (Cereals and Grains, Oilseeds and Pulses, Fruits and Vegetables, Turfs and Ornamentals, Commercial Crops), By Formulation (Liquid Concentrates, Granules, Seed-Treatment Coatings, Bait Stations, Dusts and Powders), By Application (Soil Drench, Seed Treatment, Foliar Spray, In-row Baiting), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180454

- Number of Pages: 214

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

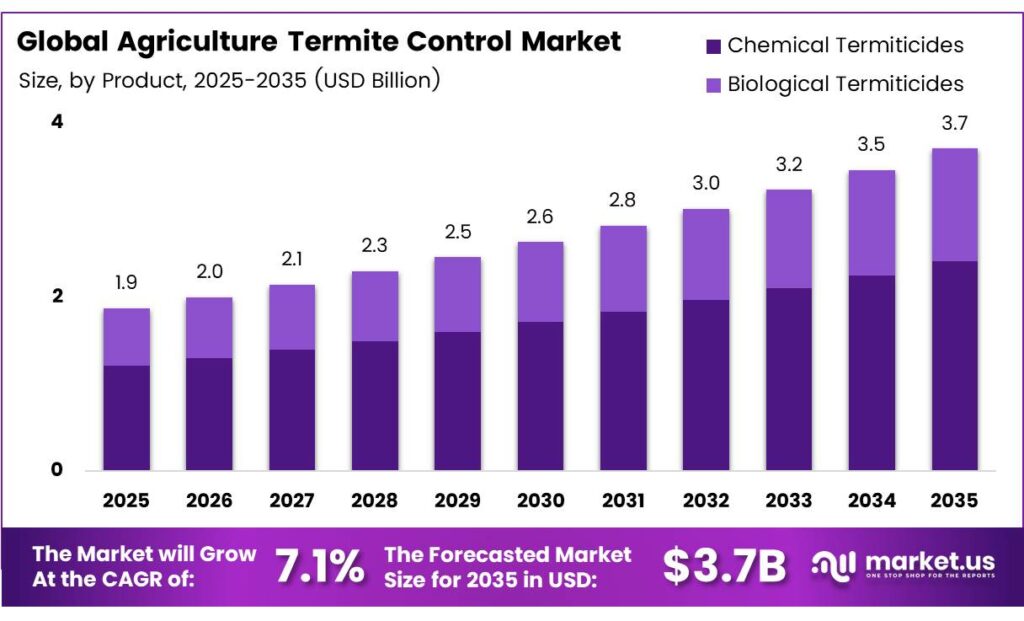

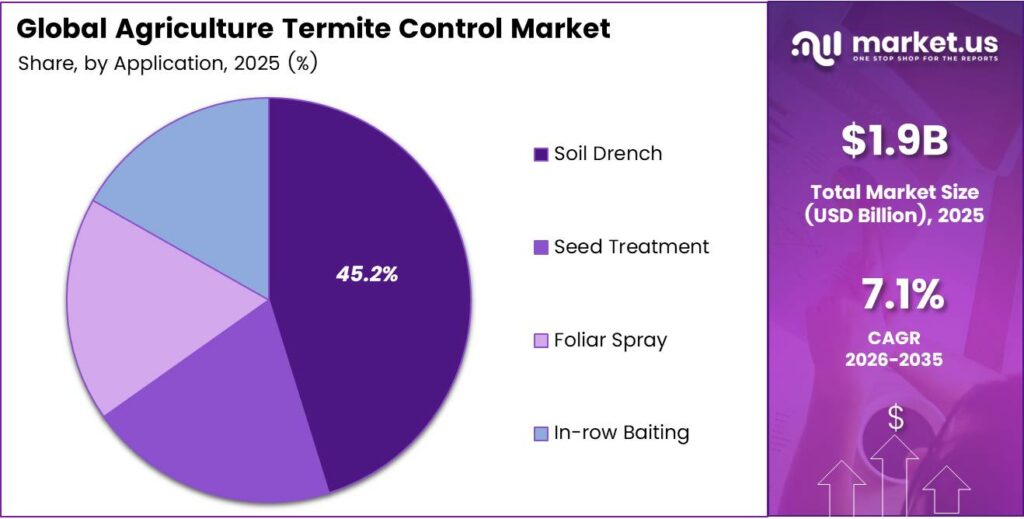

The Global Agriculture Termite Control Market size is expected to be worth around USD 3.7 billion by 2035 from USD 1.9 billion in 2025, growing at a CAGR of 7.1% during the forecast period 2026 to 2035.

Agriculture termite control refers to the range of products and methods farmers use to protect crops from subterranean and drywood termite infestations. These solutions include chemical termiticides, biological agents, seed-treatment coatings, and integrated pest management kits. They work across soil, roots, and foliage to prevent yield loss in field crops and plantations.

The market draws strong demand from cereal farming, oilseed production, and commercial crop growers. Termites cause significant underground root damage that often goes undetected until harvest losses appear. Consequently, farmers increasingly adopt preventive programs rather than reactive treatments to reduce economic risk across growing seasons.

- Brazil’s biocontrol retail sales reached approximately $924 million. This growth confirms that biological pest-control products now represent a material share of total agricultural pest management spend, validating investment in biorational termiticide development.

- Agricultural Solutions generated sales of €9,798 million in 2024, with North America contributing €3,897 million as the largest regional market. This performance highlights how major agrochemical companies prioritize the North American market for crop-protection product rollouts, including termite control chemistry.

Climate change accelerates termite migration into semi-arid agricultural zones previously considered low-risk. This geographic expansion widens the addressable market and pushes demand for both soil drench and seed-treatment products. Moreover, no-till farming practices create favorable residue environments that increase termite pressure on root systems.

Key Takeaways

- The Global Agriculture Termite Control Market was valued at USD 1.9 billion in 2025 and is projected to reach USD 3.7 billion by 2035, at a CAGR of 7.1% during the forecast period from 2026 to 2035.

- Chemical Termiticides dominate with a 78.1% market share in 2025.

- Cereals and Grains hold the largest segment share at 38.5% in 2025.

- Liquid Concentrates lead with a 44.6% share in 2025.

- Soil Drench holds the dominant position with a 45.2% share in 2025.

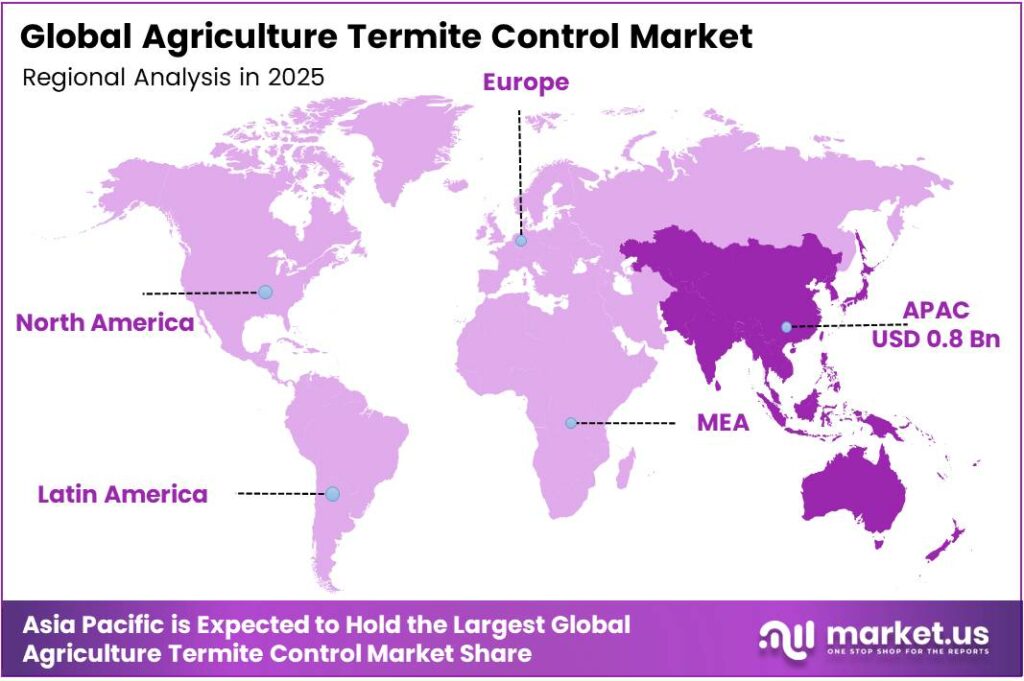

- Asia Pacific dominates the regional landscape with a 43.3% share, valued at USD 0.8 billion in 2025.

By Product Type Analysis

Chemical termiticides dominate with 78.1% due to broad-spectrum efficacy and established farmer trust.

In 2025, Chemical Termiticides held a dominant market position in the By Product Type segment of the Agriculture Termite Control Market, with a 78.1% share. Farmers rely heavily on these products because of their fast-acting and consistent field performance. Organophosphates, Neonicotinoids, Phenyl-pyrazoles, and Diamides each serve distinct crop and soil conditions.

Biological Termiticides represent the fastest-growing sub-segment within this category. Products based on Entomopathogenic Fungi, such as Metarhizium and Beauveria, offer targeted pest suppression with minimal chemical residue. Botanical Extracts and Oils further complement these solutions for export-compliant farming operations.

Integrated Treatments and IPM Kits combine chemical and biological inputs in a single program. These kits help farmers manage resistance development while meeting food safety audit requirements. Moreover, IPM-based approaches gain traction as agribusinesses seek season-long termite control with reduced environmental liability.

By Crop Type Analysis

Cereals and Grains dominate with 38.5% due to large cultivation acreage and high termite vulnerability in root zones.

In 2025, Cereals and Grains held a dominant market position in the By Crop Type segment of the Agriculture Termite Control Market, with a 38.5% share. Wheat, maize, and rice cultivation across large acreages creates consistent baseline demand for soil and seed-applied termite control products throughout the season.

Oilseeds and Pulses form the second-largest crop category for termite control spending. Soybean and canola growers face subterranean termite pressure in tropical and subtropical belts. Consequently, seed-treatment coatings and in-row baiting solutions see growing adoption among these commodity crop producers.

Fruits and Vegetables, Turfs and Ornamentals, and Commercial Crops collectively address diverse specialty segments. Horticultural growers prioritize residue-safe biological termiticides to protect export market access. Additionally, commercial plantation operators apply high-volume soil drenches to protect perennial root systems from long-term termite colonization.

By Formulation Analysis

Liquid Concentrates dominate with 44.6% due to ease of mixing, compatibility with irrigation systems, and cost efficiency.

In 2025, Liquid Concentrates held a dominant market position in the By Formulation segment of the Agriculture Termite Control Market, with a 44.6% share. Farmers prefer these formulations because they integrate easily into existing spray and drip irrigation equipment. Moreover, liquid concentrates enable flexible dosing across varying soil types and moisture conditions.

Granules and Seed-Treatment Coatings serve application-specific needs where liquid handling infrastructure is limited. Granules release active ingredients gradually into the soil profile, offering extended residual protection. Seed-treatment coatings, however, deliver targeted early-season protection directly at the germination zone.

Bait Stations, Dusts, and Powders round out the formulation landscape for precision and broadcast control. Bait stations attract and eliminate termite colonies at the source with minimal off-target impact. Dusts and powders remain relevant for enclosed or spot applications in small-scale and specialty crop settings.

By Application Analysis

Soil Drench dominates with 45.2% due to its deep root-zone penetration and broad compatibility with field crops.

In 2025, Soil Drench held a dominant market position in the By Application segment of the Agriculture Termite Control Market, with a 45.2% share. This method delivers active ingredients directly into the root zone where subterranean termites are most active. Therefore, growers achieve consistent protection across large field areas with a single well-timed application.

Seed Treatment represents the most efficient per-hectare cost application method available today. By coating seeds before planting, farmers embed protection at the point of germination. This approach also reduces the total volume of active ingredients used per crop cycle compared to broadcast applications.

Foliar Spray and In-row Baiting address above-ground and localized soil-level termite activity, respectively. Foliar sprays protect plant stems and early foliage in high-pressure environments. In-row baiting, meanwhile, uses targeted placement to intercept termite foraging trails near crop root systems with minimal disturbance to surrounding soil biology.

Key Market Segments

By Product Type

- Chemical Termiticides

- Organophosphates

- Neonicotinoids

- Phenyl-pyrazoles

- Diamides

- Biological Termiticides

- Entomopathogenic Fungi (Metarhizium, Beauveria)

- Botanical Extracts and Oils

- Integrated Treatments and IPM Kits

By Crop Type

- Cereals and Grains

- Oilseeds and Pulses

- Fruits and Vegetables

- Turfs and Ornamentals

- Commercial Crops

By Formulation

- Liquid Concentrates

- Granules

- Seed-Treatment Coatings

- Bait Stations

- Dusts and Powders

By Application

- Soil Drench

- Seed Treatment

- Foliar Spray

- In-row Baiting

Emerging Trends

Precision Agriculture and Biological Adoption Transform Termite Control Programs

Farmers across major agricultural regions shift from reactive to preventive termite management through precision agriculture tools. IoT soil probes and variable-rate application technologies now guide where and when growers apply termiticides. This shift reduces over-application, lowers input costs, and improves protection outcomes across large field operations.

- Biological termiticide adoption accelerates rapidly, driven by export certification requirements from food safety agencies. Brazil’s Mato Grosso state represented about 33% of Brazil’s domestic bioinputs market in the 2023/2024 season. This regional concentration shows how export-focused farm belts lead the transition toward residue-safe biorational pest management.

Seed-treatment coating adoption grows as diamide label expansions open new row-crop markets for early-season protection. IoT-guided bait stations now proliferate in commercial farm settings, enabling colony-level targeting with minimal chemical load. Additionally, hybrid formulations combining chemical and biologically active ingredients gain traction as growers seek season-long efficacy with lower regulatory risk.

Drivers

Climate Migration, Regulatory Approvals, and No-Till Farming Drive Agriculture Termite Control Demand

Climate-induced termite migration expands infestation zones into semi-arid agricultural belts that previously had low exposure. Warmer and drier conditions push termite colonies further into major cereal and oilseed growing regions. Consequently, farmers in these newly affected areas invest in both preventive and curative termite control programs for the first time.

- Regulatory agencies approve diamide seed treatments for an expanding range of row crops, enabling wider market adoption. FMC’s Rynaxypyr insect control technology generated approximately $1.0 billion of annual revenue in 2024. This performance confirms that diamide-class insecticides hold strong commercial positions in agricultural pest control markets globally.

No-till farming practices accelerate residue accumulation on field surfaces, creating favorable termite habitats near root zones. Farmers adopting conservation tillage systems report higher subterranean termite pressure compared to conventional tillage operations. Moreover, the surge in termite-related crop-loss insurance claims now drives bundled preventive treatment packages among commercial growers.

Restraints

Toxicology Scrutiny and Cold-Chain Costs Limit Market Expansion

Residual-toxicology scrutiny of termiticides intensifies as food-chain audits by retail buyers and export agencies set stricter maximum residue limits. Regulators in the European Union and North America review several chemically active ingredients for potential re-registration restrictions. The European Union sold approximately 292,000 tonnes of pesticides, the lowest recorded level, reflecting tighter regulatory pressure and reduced chemical input demand across member states.

High costs of biological inoculum refrigeration create major supply-chain barriers in tropical and subtropical markets. Entomopathogenic fungi products, such as Metarhizium and Beauveria, require controlled temperature storage to maintain viability. Therefore, smallholder farmers in remote tropical regions struggle to access these biological solutions due to inadequate cold-chain infrastructure and high logistics costs.

These dual restraints slow the pace of market adoption for both chemical and biological termiticide products. Chemical manufacturers face formulation reformulation costs to meet tighter residue standards in export-oriented markets. Meanwhile, biological developers must invest in heat-stable formulation technologies to overcome cold-chain limitations and expand distribution reach in high-growth developing regions.

Growth Factors

Geographic Expansion, Biorational Standards, and IoT Integration Accelerate Market Growth

Semi-arid agricultural regions newly exposed to termite pressure represent a significant untapped market opportunity for termite control product suppliers. Climate-driven geographic expansion extends demand into areas where farmers previously had no experience with termite management programs. Suppliers that enter these regions early with education-led sales approaches capture durable market share.

- BASF Agricultural Solutions’ sales in Asia reached €1,135 million in 2024, up €63 million, driven by volume gains across nearly all crop protection indications. This growth confirms that Asia-Pacific farmers increase spending on professional-grade agrochemicals, creating favorable conditions for premium termite control product introduction across the region’s expanding commercial farm sector.

On-farm IoT soil probe integration enables data-driven prophylactic drench applications timed to termite activity cycles. Farmers using these systems reduce unnecessary applications and improve active ingredient placement precision. Moreover, hybrid formulations that combine chemical and biological controls gain investment from major agrochemical companies seeking differentiated product portfolios that meet both efficacy and sustainability requirements.

Regional Analysis

Asia Pacific Dominates the Agriculture Termite Control Market with a Market Share of 43.3%, Valued at USD 0.8 Billion

Asia Pacific leads the global agriculture termite control market with a 43.3% share, valued at USD 0.8 billion in 2025. The region’s dominance reflects vast tropical and subtropical farmland across China, India, Southeast Asia, and Australia, where termite pressure on cereal and commercial crops remains persistently high. Strong government support for crop protection programs and growing farmer awareness further reinforce regional market leadership.

North America maintains a strong market position driven by large-scale commercial grain and oilseed farming operations. The region benefits from advanced regulatory frameworks that support the timely approval of new active ingredients, including diamide seed treatments. Additionally, crop-loss insurance programs that bundle preventive termite treatment uptake add a unique demand driver not present in developing regions.

Europe presents a complex market shaped by tightening pesticide regulations and growing interest in biological termite control alternatives. The European Union’s drive to reduce chemical pesticide use by 2030 pushes growers and suppliers toward biorational and IPM-based termite management solutions. However, the region’s temperate climate limits acute termite pressure to southern Mediterranean agricultural zones.

Middle East and Africa represent an emerging market where termite damage in dryland cereal and commercial crop farming drives growing demand. Arid and semi-arid conditions in Sub-Saharan Africa create persistent subterranean termite pressure on sorghum, millet, and maize root systems. Consequently, development aid programs that include integrated pest management components help introduce formal termite control practices to smallholder farm communities.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF SE operates one of the broadest agricultural chemical portfolios in the termite control segment, combining soil-applied insecticides, seed treatments, and biological crop protection products. The company invests heavily in sustainable chemistry research and precision application partnerships. Its global distribution network across more than 90 countries gives it unmatched farmer reach in both established and emerging crop protection markets.

Bayer AG brings together a comprehensive crop science division that addresses soil-borne insect pressure, including termite damage, across cereals, oilseeds, and specialty crops. Bayer integrates digital farming tools with its crop protection product line to support data-driven pest management decisions on commercial farms. The company’s investment in biological crop protection complements its established chemical portfolio for markets requiring low-residue compliance.

Syngenta Group focuses on seed treatment innovation and integrated pest management platforms that address termite pressure at the point of germination and early crop establishment. The company operates strong commercial positions across Latin America and the Asia Pacific, the two regions with the highest termite control demand growth. Syngenta’s research pipeline includes next-generation biological and chemical active ingredients designed for export-compliant farming systems.

Corteva Agriscience delivers a specialized portfolio of soil insecticides and seed-applied treatments that protect row crops from subterranean termite damage through the early and mid-season growth stages. The company prioritizes farmer-education programs that guide proper application timing and method selection across diverse soil and climate conditions. Corteva’s strong presence in North and South American grain markets positions it well for growth as termite pressure expands into new geographies.

Top Key Players in the Market

- BASF SE

- Bayer AG

- Syngenta Group

- Corteva Agriscience

- FMC Corporation

- UPL Ltd.

- Nufarm Ltd.

- Sumitomo Chemical Co., Ltd.

- Terra Agro Biotech Pvt Ltd

- Sinon Corporation

Recent Developments

- In 2025, Syngenta and Syngenta Group websites returned pages mentioning termite, termiticide, or termite control in an agriculture or crop context. Products or regulatory mentions appear on company sites or government sources (EPA, USDA, state ag departments).

- In 2025, Corteva Agriscience’s agriculture-specific termite control developments (crop pests, soil treatments, or new registrations) appear on Corteva’s official sites. All references are to the legacy Sentricon AlwaysActive / Sentricon AG / Sentricon II termite bait systems, which target structural protection for homes and buildings (urban pest management, colony elimination via hexaflumuron baits).

Report Scope

Report Features Description Market Value (2025) USD 1.9 Billion Forecast Revenue (2035) USD 3.7 Billion CAGR (2026-2035) 7.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Chemical Termiticides (Organophosphates, Neonicotinoids, Phenyl-pyrazoles, Diamides), Biological Termiticides, Integrated Treatments and IPM Kits), By Crop Type (Cereals and Grains, Oilseeds and Pulses, Fruits and Vegetables, Turfs and Ornamentals, Commercial Crops), By Formulation (Liquid Concentrates, Granules, Seed-Treatment Coatings, Bait Stations, Dusts and Powders), By Application (Soil Drench, Seed Treatment, Foliar Spray, In-row Baiting) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape BASF SE, Bayer AG, Syngenta Group, Corteva Agriscience, FMC Corporation, UPL Ltd., Nufarm Ltd., Sumitomo Chemical Co., Ltd., Terra Agro Biotech Pvt Ltd, Sinon Corporation Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Agriculture Termite Control MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Agriculture Termite Control MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- BASF SE

- Bayer AG

- Syngenta Group

- Corteva Agriscience

- FMC Corporation

- UPL Ltd.

- Nufarm Ltd.

- Sumitomo Chemical Co., Ltd.

- Terra Agro Biotech Pvt Ltd

- Sinon Corporation

Our Clients

- 180454

- March 2026