Global Agricultural Lubricants Market Size, Share, And Industry Analysis Report By Type (Mineral Oil, Synthetic, Bio-Based), By Product Type (Engine Oil, UTTO, Coolant, Grease), By Application (Engines, Gears and Transmission, Hydraulics, Greasing, Implements, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2025-2034

- Published date: February 2026

- Report ID: 178874

- Number of Pages: 213

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

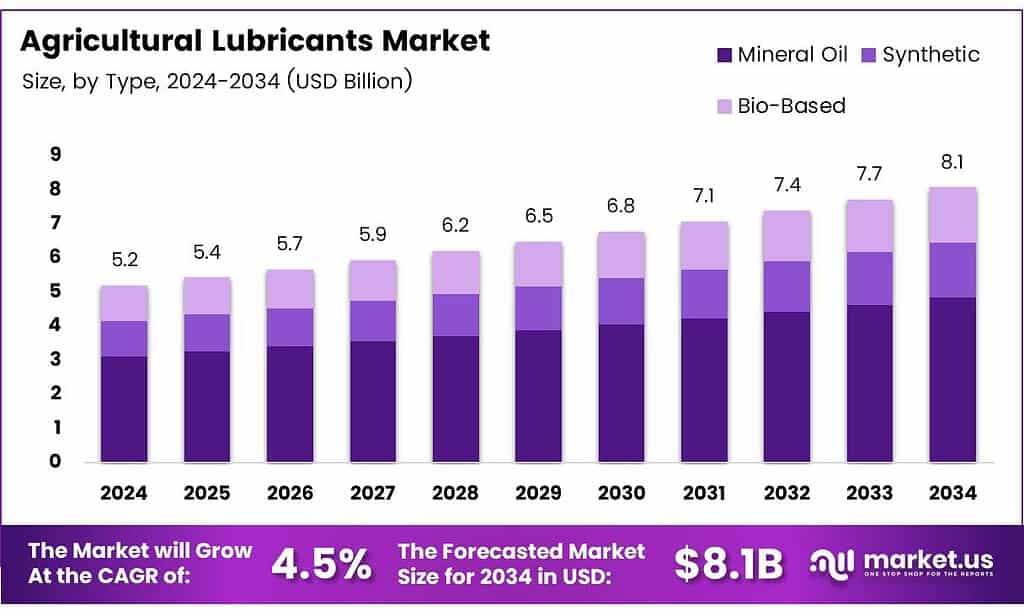

The Global Agricultural Lubricants Market size is expected to be worth around USD 8.1 billion by 2034 from USD 5.2 billion in 2024, growing at a CAGR of 4.5% during the forecast period 2025 to 2034.

Agricultural lubricants are specialized fluids designed to protect and maintain farm machinery components. They reduce friction, prevent wear, and extend equipment life across tractors, harvesters, and irrigation systems. Consequently, reliable lubrication directly supports the uptime and productivity of modern farming operations globally.

The market covers a broad range of product types, including engine oils, gear oils, hydraulic fluids, coolants, and greases. Farmers and agribusiness operators apply these solutions across engines, transmissions, hydraulic systems, and implements. Moreover, each application demands specific viscosity grades and additive packages suited to field conditions.

- Fossil fuels remain the dominant energy source for the transportation sector, accounting for nearly 97.6% of its total energy use. This sector consumes about 18% of global primary energy and contributes roughly 23% of worldwide CO₂ emissions, intensifying global warming. Growing lubricant oil spillage and poor recycling practices further damage the environment, with an estimated 50% of used lubricants released into ecosystems and around 95% of that causing harmful effects on human health and ecological balance.

Global food demand growth continues to push agricultural mechanization forward. Farmers increasingly replace manual labor with tractors, combine harvesters, and precision equipment. Therefore, the need for high-performance lubricants that support continuous machine operation in demanding outdoor environments rises steadily across both developed and emerging markets.

The market attracts investment from both multinational energy companies and specialized lubricant manufacturers. Research and development efforts focus on extending drain intervals, improving thermal stability, and meeting newer emission standards. Furthermore, the integration of smart monitoring systems opens new opportunities for lubricant suppliers aligned with digital farming platforms.

Key Takeaways

- The Global Agricultural Lubricants Market was valued at USD 5.2 billion in 2024 and is projected to reach USD 8.1 billion by 2034, at a CAGR of 4.5% during the forecast period 2025 to 2034.

- Mineral Oil dominated the market with a 56.8% share in 2025.

- Engine Oil held the largest share at 48.6% in 2025.

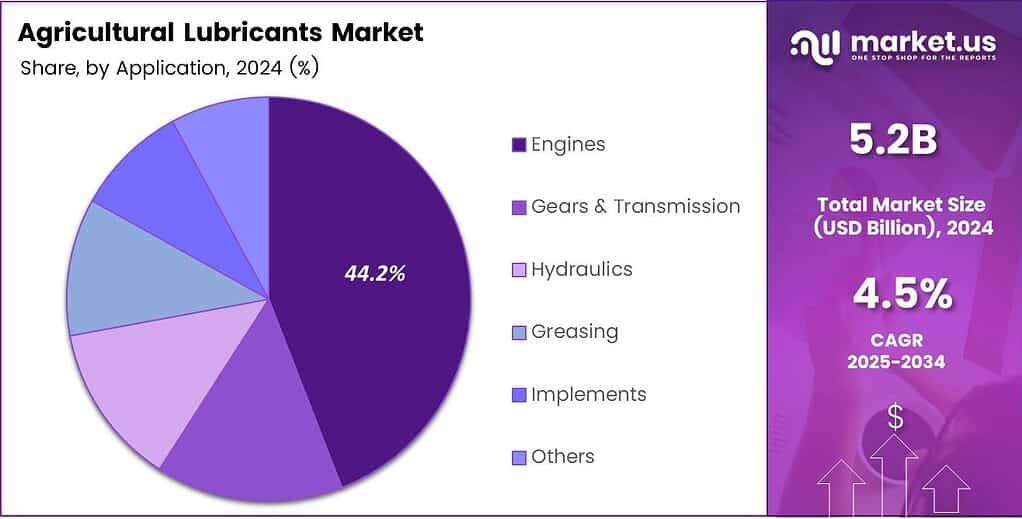

- The Engines segment led the market with a 44.2% share in 2025.

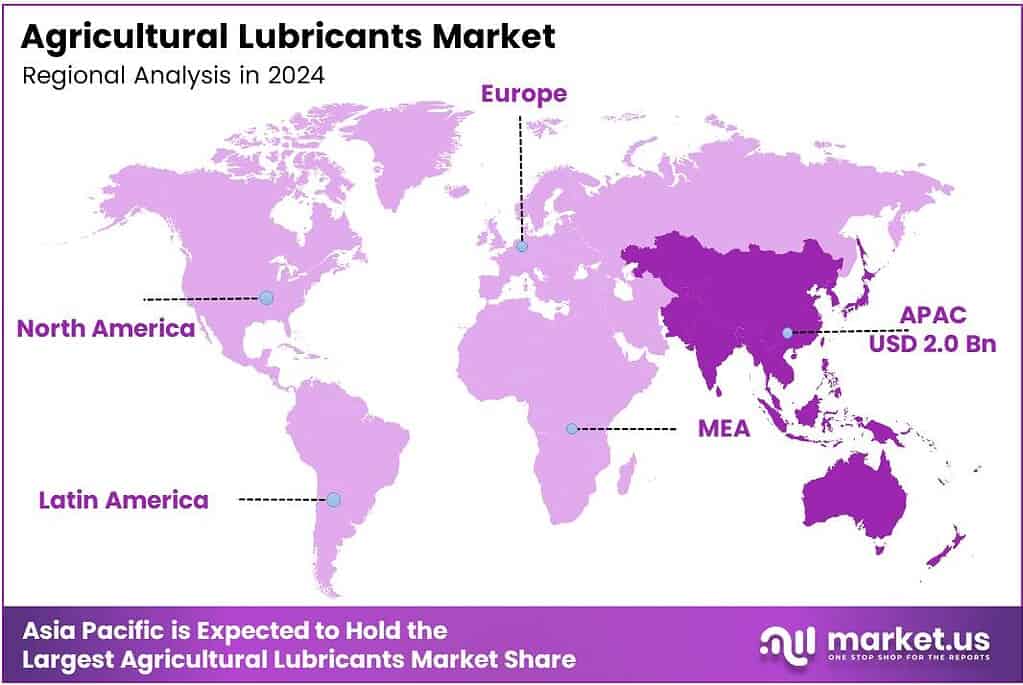

- Asia Pacific dominated the regional market with a 38.5% share, valued at USD 2.0 billion in 2025.

By Type Analysis

Mineral Oil dominates with 56.8% due to cost-effectiveness and wide availability across farming regions.

In 2025, Mineral Oil held a dominant market position in the By Type segment of the Agricultural Lubricants Market, with a 56.8% share. Mineral oil lubricants offer reliable performance at accessible price points. Consequently, smallholder and mid-scale farmers across Asia, Africa, and Latin America prefer them for routine tractor and machinery maintenance where budget constraints are common.

Synthetic lubricants represent a growing share of the agricultural lubricants segment. These advanced formulations deliver superior thermal stability, longer drain intervals, and enhanced protection under extreme operating conditions. Moreover, large-scale commercial farms and precision agriculture operators increasingly adopt synthetic oils to reduce maintenance downtime and improve overall fleet efficiency.

Bio-Based lubricants occupy an emerging position within the agricultural lubricants landscape. Derived from plant or animal oils, these products align with sustainability mandates and environmental compliance requirements. Therefore, farms operating under eco-certification programs or government green initiatives actively shift toward biodegradable lubricant options to meet regulatory and consumer-driven sustainability expectations.

By Product Type Analysis

Engine Oil dominates with 48.6% due to universal demand across all types of farm machinery engines.

In 2025, Engine Oil held a dominant market position in the By Product Type segment of the Agricultural Lubricants Market, with a 48.6% share. Engine oils serve as the most essential lubricant category for agricultural equipment. Additionally, every tractor, combine harvester, and self-propelled machine requires regular engine oil changes, sustaining consistent and high-volume demand throughout the farming season.

UTTO (Universal Tractor Transmission Oil) products serve a dual function across transmissions, differentials, wet brakes, and hydraulic systems. Their multipurpose nature reduces the need to stock multiple fluid types, simplifying farm maintenance. However, proper formulation is critical, as incorrect UTTO application can damage sensitive transmission and hydraulic components in modern farm equipment.

Coolant solutions protect engines from overheating during extended field operations in high-temperature environments. These products also prevent corrosion and scaling within engine cooling circuits. Furthermore, Grease applications protect bearings, pivot joints, and moving linkages on implements and harvesting heads, reducing mechanical wear during intensive planting, cultivation, and harvesting cycles.

By Application Analysis

The engines segment dominates with 44.2% due to the highest lubricant consumption volume across all farm machinery types.

In 2025, Engines held a dominant market position in the By Application segment of the Agricultural Lubricants Market, with a 44.2% share. Engine lubrication generates the largest consumption volumes because every motorized farm machine depends on it. Consequently, this segment attracts the most product development focus, with formulations targeting fuel efficiency, emission compliance, and extended service intervals.

Gears and Transmission systems require specialized gear oils and UTTO formulations to handle the torque loads common in heavy farm equipment. Hydraulic systems demand clean, high-viscosity fluids to maintain precise actuator control across implements and attachments. Moreover, Hydraulics has grown in importance as modern tractors increasingly rely on hydraulic-assisted steering, lifting, and remote valve functions.

Greasing applications address bearings, pins, and linkages on tillage equipment and harvesting headers. Implements such as plows, seeders, and sprayers require dedicated lubrication to withstand abrasive soil and crop contact conditions. Additionally, the Others sub-segment covers specialty applications, including chain lubrication, storage protection, and agricultural vehicle undercarriage maintenance needs.

Key Market Segments

By Type

- Mineral Oil

- Synthetic

- Bio-Based

By Product Type

- Engine Oil

- UTTO

- Coolant

- Grease

By Application

- Engines

- Gears and Transmission

- Hydraulics

- Greasing

- Implements

- Others

Emerging Trends

Sustainability, Smart Technology, and High-Performance Formulations Reshape the Agricultural Lubricants Market

A strong industry shift toward environmentally compliant, low-emission, and biodegradable lubricant innovations defines the current market direction. Lubricant manufacturers actively reformulate products to meet tighter environmental standards across major agricultural economies. System-wide store sales reached USD 3.1 billion in fiscal 2024, growing 12% year over year, signaling robust demand for premium lubricant solutions in rural and agricultural segments.

IoT-based real-time lubrication monitoring systems gain adoption across modern farm equipment fleets. These systems track lubricant condition, consumption rates, and maintenance schedules remotely. Consequently, farm operators reduce unplanned downtime and optimize lubricant change intervals, lowering the total cost of ownership across large commercial farming and agribusiness fleets that run multiple machines simultaneously.

Growing preference for high-viscosity synthetic oils suited to higher-power tractors and harvesters accelerates product premiumization. Custom hiring centers and shared machinery models further increase lubricant consumption frequency across smallholder and cooperative farming ecosystems. Therefore, lubricant suppliers expand distribution networks and introduce application-specific product lines to serve these rapidly growing service-based farm equipment markets.

Drivers

Farm Mechanization, Government Support, and Commercial Agriculture Expansion Drive Agricultural Lubricant Demand

Government subsidies and incentives for farm machinery acquisition in emerging economies like India and China directly stimulate lubricant consumption. These programs lower the cost barrier for smallholder farmers to purchase tractors and equipment. Gulf Oil Lubricants India Limited operates a Silvassa manufacturing facility with an installed capacity of 90,000 KLPA and a Chennai greenfield plant with 50,000 KLPA capacity, supporting India’s agricultural lubricant market growth.

Escalating farm labor costs accelerate mechanization across global agricultural operations. Farmers replace manual tasks with tractors, combines, and automated implements to maintain competitiveness. Consequently, every additional machine entering service creates sustained, repeat demand for engine oils, hydraulic fluids, and transmission lubricants throughout its operational lifecycle across diverse farming environments.

Expansion of large-scale commercial farming and agribusiness operations requires reliable high-performance lubrication solutions. Integration of precision and smart farming technologies also demands specialized lubricant formulations compatible with electronic and sensor-driven systems. Therefore, lubricant manufacturers invest in product development to serve both conventional large-farm operators and technology-forward precision agriculture adopters simultaneously.

Restraints

Crude Oil Price Volatility and Premium Lubricant Costs Constrain Agricultural Lubricants Market Growth

Volatility in crude oil and base oil prices directly disrupts lubricant production costs. When feedstock prices spike, manufacturers face margin pressure and struggle to pass costs to price-sensitive farm customers. BP’s Castrol brand, for example, continues to serve agricultural markets with products like Castrol Agri Grease Ultra, but premium positioning limits penetration in cost-sensitive smallholder farming regions where affordability drives purchasing decisions.

High premium pricing of synthetic and bio-based lubricants significantly limits adoption in cost-sensitive farming regions. Smallholder farmers in developing economies prioritize upfront cost savings over long-term performance benefits. Consequently, the shift toward advanced lubricant formulations slows in markets where per-unit price remains the dominant purchasing criterion rather than total lifecycle cost savings.

Additionally, limited awareness of advanced lubricant benefits among rural farming communities restrains market premiumization. Many small-scale operators rely on traditional, lower-grade products due to habit and limited technical guidance. Therefore, manufacturers must invest in farmer education, extension services, and demonstration programs to build demand for higher-performance lubricant categories in underserved agricultural markets.

Growth Factors

Biodegradable Lubricants, Automation, and Extended Drain Technologies Accelerate Market Expansion

Rising demand for biodegradable and eco-friendly lubricants aligns with sustainable farming initiatives gaining momentum globally. Regulatory mandates and voluntary eco-certification programs push farm operators toward environmentally safe fluid choices. Additionally, FUCHS SE committed a EUR 50 million investment in its Mannheim, Germany headquarters to expand the site by 25% to 135,000 square meters, enhancing production and logistics capacity for advanced lubricant supply.

Proliferation of automated and GPS-guided agricultural equipment creates a growing need for precision-compatible lubricants. These machines operate under tighter mechanical tolerances and require fluids that maintain stable viscosity and cleanliness. Moreover, the emergence of electric and hybrid agricultural machinery opens new markets for electrification-specific lubricant formulations designed to protect motors, gearboxes, and battery thermal management systems.

Development of extended drain interval lubricants reduces maintenance downtime and lowers overall operational costs for farm operators. These formulations use advanced additive chemistry to sustain protection well beyond conventional service intervals. Therefore, agribusiness operators managing large equipment fleets actively seek extended drain products to reduce the frequency of service stops and minimize productivity losses during critical planting and harvest windows.

Regional Analysis

Asia Pacific Dominates the Agricultural Lubricants Market with a Market Share of 38.5%, Valued at USD 2.0 Billion

Asia Pacific leads the global agricultural lubricants market with a 38.5% share valued at USD 2.0 billion in 2025. The region’s dominance reflects its massive farming population, rapid mechanization in China and India, and strong government subsidy programs supporting tractor and farm equipment adoption. Additionally, expanding agribusiness operations across Southeast Asia further sustains high lubricant consumption volumes.

North America is a mature, high-value segment of the global agricultural lubricants market. Large-scale commercial farming across the United States and Canada demands premium lubricant solutions for high-horsepower tractors, combines, and planters. Moreover, strict environmental regulations drive the adoption of low-emission and biodegradable fluid categories among compliance-focused farm operators in the region.

Europe maintains a strong agricultural lubricants market driven by precision farming adoption and tight environmental compliance standards. The European Union’s Farm to Fork strategy actively promotes sustainable agricultural inputs, including biodegradable lubricants. Consequently, European farmers and agribusinesses increasingly choose eco-certified products, thereby supporting premiumization and investment in innovation among regional lubricant suppliers.

The Middle East and Africa region shows gradual growth in agricultural lubricant demand as governments invest in food security and irrigation-based farming programs. Mechanization rates remain lower than in other regions but are rising steadily in South Africa, Egypt, and GCC-supported agricultural projects. Moreover, donor-funded rural development programs contribute to equipment acquisition and associated lubricant consumption growth across the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BP p.l.c., through its Castrol brand, holds a well-established position in the agricultural lubricants sector. Castrol markets specialized products, including Castrol Agri Grease Ultra, targeting farm equipment protection needs. The company leverages its global distribution infrastructure to serve both large agribusiness operators and independent farm dealers across multiple regions and equipment categories.

Chevron Corporation addresses agricultural lubrication requirements through its Delo and Texaco product lines. The company focuses on heavy-duty lubricant formulations compatible with modern tractors, combines, and mixed diesel fleets. Chevron’s ongoing Delo 600 ADF development emphasizes extended emission-control system life and fuel economy, making it relevant for farm operators managing emission-compliant equipment across major agricultural markets.

FUCHS SE delivers a comprehensive portfolio of specialty lubricants serving agricultural, industrial, and automotive applications globally. The company’s acquisition of LUBCON Group and STRUB AG strengthens its specialty product capabilities and direct market access.

Exxon Mobil Corporation competes in agricultural lubricants through its Mobil brand, offering engine oils, hydraulic fluids, and gear lubricants for farming applications. Supported by record first-half Mobil 1 sales and improved finished lubes margins. ExxonMobil’s research investment in advanced additive chemistry supports formulation development for modern precision agriculture equipment.

Top Key Players in the Market

- BP p.l.c.

- Chevron Corporation

- CLASS KGaA mbH

- CONDAT

- Cougar Lubricants International Ltd.

- Exol Lubricants Limited

- Exxon Mobil Corporation

- FRONTIER PERFORMANCE LUBRICANTS, INC.

- Fuchs

- Gulf Oil International Ltd.

Recent Developments

- In 2025, BP p.l.c. (via its Castrol lubricants brand) has maintained its long-established presence in agricultural lubricants without major new product launches specifically announced for the sector. Castrol continues to market specialized products such as Castrol Agri Grease Ultra, a high-performance grease for farm equipment.

- In 2025, Chevron Corporation focuses on heavy-duty lubricants suitable for agricultural machinery (tractors, combines, etc.) through its Delo and Texaco brands, with ongoing formulation work rather than ag-exclusive launches. Key emphasis is on Delo 600 ADF (ultra-low-ash SAE 10W-30 and 15W-40), promoted for extended emission-control system life, fuel economy, and use in mixed diesel/CNG fleets — applicable to modern farm equipment.

Report Scope

Report Features Description Market Value (2024) USD 5.2 Billion Forecast Revenue (2034) USD 8.1 Billion CAGR (2025-2034) 4.5% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Mineral Oil, Synthetic, Bio-Based), By Product Type (Engine Oil, UTTO, Coolant, Grease), By Application (Engines, Gears and Transmission, Hydraulics, Greasing, Implements, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape BP p.l.c., Chevron Corporation, CLASS KGaA mbH, CONDAT, Cougar Lubricants International Ltd., Exol Lubricants Limited, Exxon Mobil Corporation, FRONTIER PERFORMANCE LUBRICANTS, INC., Fuchs, Gulf Oil International Ltd. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Agricultural Lubricants MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample

Agricultural Lubricants MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- BP p.l.c.

- Chevron Corporation

- CLASS KGaA mbH

- CONDAT

- Cougar Lubricants International Ltd.

- Exol Lubricants Limited

- Exxon Mobil Corporation

- FRONTIER PERFORMANCE LUBRICANTS, INC.

- Fuchs

- Gulf Oil International Ltd.

Our Clients

- 178874

- February 2026