Quick Navigation

Report Overview

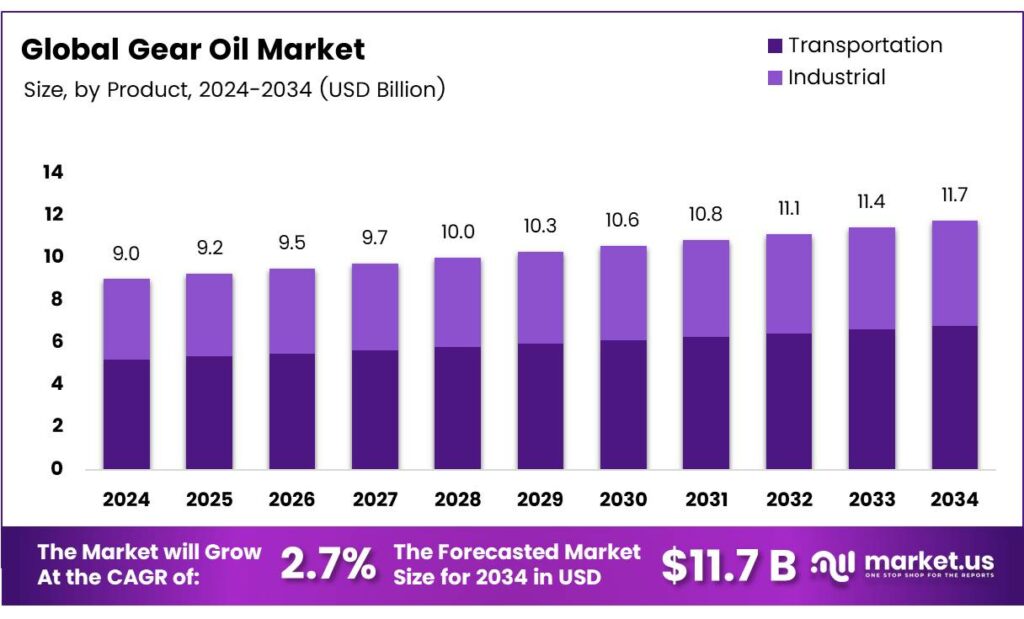

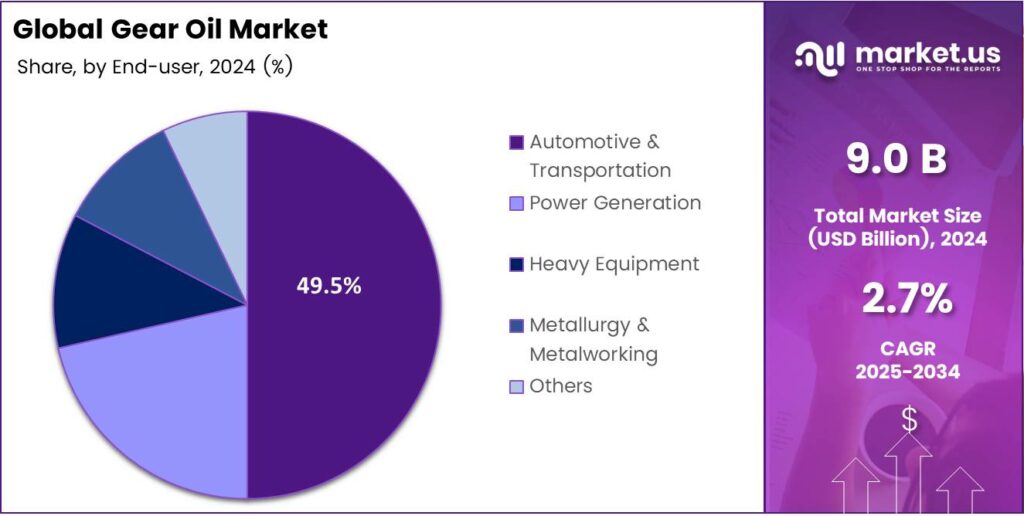

The Global Gear Oil Market size is expected to be worth around USD 11.7 billion by 2034, from USD 9.0 billion in 2024, growing at a CAGR of 2.7% during the forecast period from 2025 to 2034.

Gear oil is a broad term encompassing several types of lubricants and fluids essential for the functioning and performance of gear systems in vehicles. Similar to engine oil but distinct in purpose, it protects gears from wear and tear, dissipates heat, and reduces friction. The term gear oil is somewhat vague, as it can refer to various fluids used across different vehicle types.

Most commonly, gear oil refers to manual transmission fluid (MTF), which reduces friction within manual gear systems. In contrast, automatic transmission fluid (ATF) is used in automatic transmissions, where gear shifts occur without driver intervention. ATF supports power transfer from the transmission to the engine and has different properties from MTF due to operating under lower heat and pressure. Other specialized lubricants include differential gear oil and transfer case fluid.

Every vehicle has a differential that allows wheels to rotate at different speeds during turns. Differential gear oil lubricates the gears and bearings inside this component, with a unique additive formulation to withstand high pressures and shock loads during acceleration, braking, and cornering. In four-wheel-drive vehicles, a transfer case directs power to all four wheels, and transfer case fluid lubricates its gears and bearings. Though not exposed to the same extreme conditions as the differential, this fluid still contains protective additives to prevent premature wear.

Different types of gear oil vary in viscosity, typically graded by two numbers separated by a W, such as 75W-90. The W stands for winter, with the first number indicating viscosity at cold temperatures and the second at higher temperatures. Higher numbers denote greater viscosity, making thicker oils suitable for high-heat, high-pressure applications, particularly in manual transmissions. Automatic transmission fluid, however, is much less viscous to ensure smooth power transmission.

- Gear oil comprises base oil and additives, with the additive package driving performance by enhancing desirable traits and curbing unwanted ones. Key selection criteria include thermal stability and oxidation resistance at high temperatures to prevent sludge or varnish and prolong drain intervals, oxidation halves service life for every 18°F (10°C) rise above 140°F (60°C). In heavily or shock-loaded enclosed gearboxes, extreme pressure (EP) additives are vital for gear surface protection. The oil must also demulsify to separate and remove water contamination effectively.

Key Takeaways

- The Global Gear Oil Market is projected to reach USD 11.7 billion by 2034, up from USD 9.0 billion in 2024, at a CAGR of 2.7% (2025-2034).

- Transportation dominated the market by product type in 2024, securing a 57.9% share, driven by rising vehicle dependence on efficient gear lubrication.

- SAE 80W-90 viscosity grade held a 49.3% share, favored for its stability and versatility in light to heavy-duty applications.

- The Aftermarket channel led distribution with a 67.9% share, supported by DIY culture, service-center demand, and broad brand availability.

- Automotive & Transportation was the largest end-user segment, capturing 49.5% share as car ownership and logistics expansion raised lubricant needs.

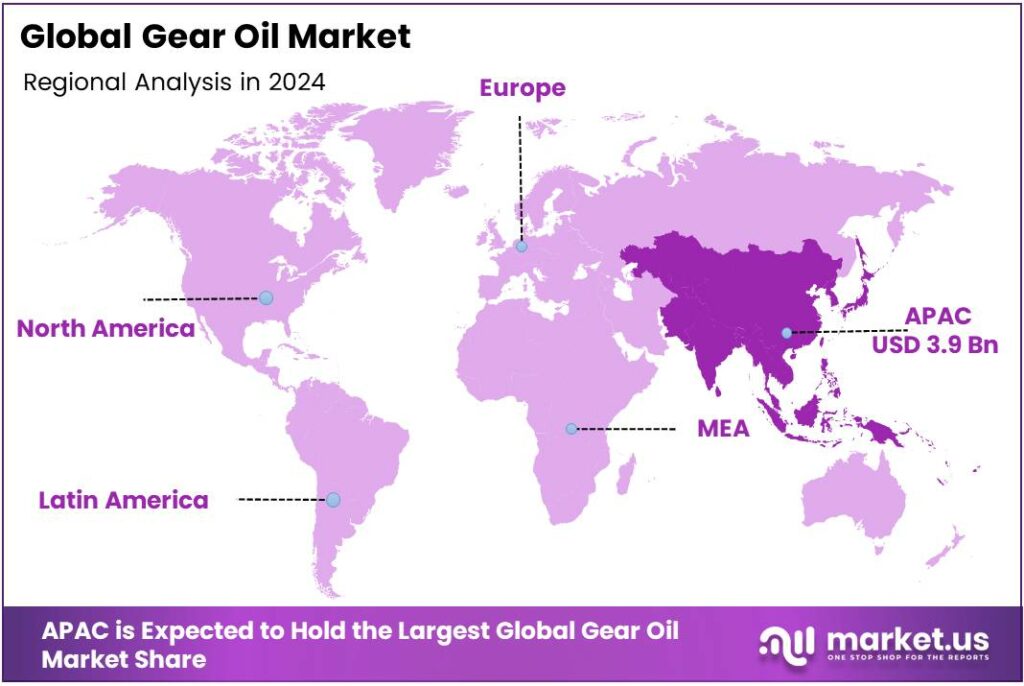

- Asia-Pacific remained the leading regional market, accounting for a 43.8% share valued at USD 3.9 billion

By Product Type

Transportation dominates with 57.9% due to its critical role in vehicle performance and high demand in mobility sectors.

In 2024, Transportation held a dominant market position in the by-product type Analysis segment of the Gear Oil Market, with a 57.9% share. This segment thrives as vehicles rely on gear oils for smooth transmission and longevity. Manufacturers prioritize advanced formulations to meet emission standards, boosting adoption. Consequently, transportation applications drive innovation in synthetic blends, enhancing fuel efficiency.

The Manual Gearbox sub-segment captures significant interest for its simplicity and cost-effectiveness in traditional vehicles. Drivers favor it in rugged terrains where manual control excels. Gear oils here focus on shear stability to withstand frequent shifts. This keeps maintenance straightforward, appealing to fleet operators. Thus, manual gearboxes maintain steady demand in emerging markets, supporting economic accessibility in transportation.

Meanwhile, the Automatic Gearbox sub-segment grows rapidly with urban driving trends. It demands multi-grade oils for seamless shifts under varying loads. Automakers integrate these for comfort, reducing wear in stop-and-go traffic. As a result, automatic transmissions gain traction in passenger cars, propelling gear oil formulations toward higher thermal resistance. This shift underscores consumer preference for effortless performance.

By Viscosity Grade

SAE 80W-90 dominates with 49.3% due to its balanced performance in diverse temperature conditions and broad compatibility.

In 2024, SAE 80W-90 held a dominant market position in the By Viscosity Grade Analysis segment of the Gear Oil Market, with a 49.3% share. This grade excels in moderate climates, offering reliable lubrication without excessive thinning. It suits a wide range of gearboxes, from light-duty to commercial uses. Formulators enhance it with EP additives for better protection.

The SAE 75W-90 sub-segment emerges as a versatile choice for all-season applications. It flows well at low temperatures while maintaining viscosity in heat. This makes it ideal for modern vehicles seeking energy efficiency. Consequently, adoption surges in regions with variable weather, optimizing gear performance. Innovations here focus on synthetic bases, extending service life effectively.

Additionally, the SAE 85W-140 sub-segment targets heavy-duty scenarios with superior film strength. It resists breakdown under extreme pressures, perfect for industrial gears. Operators select it for longevity in high-load environments. Thus, this grade supports demanding operations, ensuring minimal downtime and robust reliability in challenging conditions.

By Distribution Channel

Aftermarket dominates with 67.9% due to widespread accessibility and consumer preference for replacements.

In 2024, Aftermarket held a dominant market position in the By Distribution Channel Analysis segment of the Gear Oil Market, with a 67.9% share. This channel empowers DIY mechanics and service centers with easy procurement. It offers diverse brands at competitive prices, catering to routine maintenance. Retailers stock versatile options, encouraging bulk buys. Hence, aftermarket leads by providing flexibility and quick availability.

The Original Equipment Manufacturer sub-segment focuses on precision integration during assembly. OEMs specify exact viscosities to align with design parameters. This ensures optimal performance from the start, building trust in brands. Suppliers collaborate closely, delivering consistent quality in large quantities. As a result, OEM channels support initial fills, laying the foundation for long-term reliability in new machinery deployments.

By End-user

Automotive and Transportation dominate with 49.5% due to surging vehicle production and maintenance needs globally.

In 2024, Automotive and Transportation held a dominant market position in the By End-user Analysis segment of the Gear Oil Market, with a 49.5% share. This sector powers daily commutes and logistics, relying on gear oils for friction reduction. Rising car ownership amplifies demand for high-quality lubricants. Suppliers respond with tailored products that meet OEM specs, enhancing engine health.

The Power Generation sub-segment gains momentum in renewable energy setups. Gear oils here endure constant loads in turbines and generators. They prevent corrosion in harsh environments, ensuring uninterrupted operation. As green energy expands, this area adopts rust-inhibiting formulas. Thus, power generation drives specialized gear oil development, supporting sustainable infrastructure growth steadily.

Furthermore, the Heavy Equipment sub-segment thrives in construction and mining. It requires oils with strong anti-wear properties for rugged use. Operators prioritize demulsibility to handle contaminants. Consequently, heavy equipment boosts demand for durable grades, minimizing repairs in field operations. This focus underscores resilience in industrial applications.

Key Market Segments

By Product Type

- Transportation

- Manual Gearbox

- Automatic Gearbox

- Axle Oils

- Industrial

By Viscosity Grade

- Sae 75W-90

- Sae 80W-90

- Sae 85W-140

By Distribution Channel

- Aftermarket

- Original Equipment Manufacturer

By End-user

- Automotive and Transportation

- Power Generation

- Heavy Equipment

- Metallurgy and Metalworking

- Others

Emerging Trends

Shift to high-efficiency synthetic e-gear oils for EVs & wind

A clear trend is the move to low-viscosity, synthetic gear oils designed for electric drivelines and wind-turbine gearboxes. The reason is simple: electrification and renewables are exploding, and operators now chase every percent of efficiency and longer drain intervals.

- Electric car sales topped 17 million in 2024, up more than 25% year-on-year, so e-axles and reduction gears need fluids that cut drag, manage copper corrosion, and stay stable under high speeds and electrical fields. That momentum continues into 2025, with EVs expected to exceed 20 million sales globally, reinforcing demand for tailored e-gear lubricants with controlled conductivity and optimized additive packages.

Wind is the second push. Turbine fleets are growing fast and rely on long-life synthetic gear oils to limit downtime offshore and in remote sites. The wind industry installed a record 117 GW of new capacity, passing 1 TW cumulative for the first time; policymakers in the United States and European Union are also signaling more support, which should keep additions high and maintenance strategies focused on oil durability and condition monitoring.

Drivers

Focus on Energy Efficiency Across Machinery

One of the key driving forces behind the growing demand for gear oil is the increasing emphasis on energy efficiency in industrial and automotive systems. Efficient lubrication of gearboxes and transmissions directly contributes to lowering friction and reducing energy losses, making advanced gear oils more desirable.

The global industrial sector — which accounts for a large share of gear-use machinery — is projected to consume more than 315 quadrillion Btu of energy, and studies estimate that friction- and wear-related energy losses account for up to 60% of industrial end-use energy in many cases.

- Specifically, research into gear oils shows that energy-efficient lubricant formulations can deliver tangible improvements: one study found that when using an optimized gear lubricant in a worm gearbox, efficiency gains of up to 3.6% were recorded compared to a baseline fluid. This kind of saving matters because a gearbox may run continuously for thousands of hours, so even a 3-4% efficiency improvement adds up to measurable energy and cost savings.

Restraints

Tightening environmental rules on additives & used-oil handling

The gear oil business is running into a wall of environmental compliance. A big pinch point is the shrinking palette of extreme-pressure (EP) additives. Short-chain chlorinated paraffins—once common EP boosters—are listed for elimination under the Stockholm Convention, with only narrow exemptions; the Convention explicitly notes their historical use as lubricant additives. This forces reformulation, re-testing, and supply changes, adding cost and slowing launches.

- Five EU authorities submitted a REACH restriction proposal covering 10,000 PFAS, a very broad net that can touch certain fluorinated performance components and processing aids used around lubricants and seals. Even where final scopes narrow, manufacturers must audit chemistries, engineer alternatives, and navigate long compliance timelines effort which can restrain speed and raise costs.

End-of-life management adds pressure. In the United States, EPA materials note roughly 380 million gallons of used oil are recycled each year, yet federal analyses cite on the order of 200 million gallons still improperly disposed annually, an environmental liability that prompts stricter handling, record keeping, and take-back systems for shops and fleets. Those requirements increase operating overheads for buyers and distributors of gear oils.

Opportunity

Manufacturing build-out and automation raise gearbox hours

- A powerful growth engine for gear oils is the worldwide expansion and automation of manufacturing. More plants and robots mean more reducers and heavy gear trains running longer hours, so reliable lubrication becomes a line-stopper issue. The International Federation of Robotics reports a record 4.28 million industrial robots operating in factories worldwide (2024), up 10% year over year, with annual installations staying above 500,000 units.

Each robot typically drives precision gear stages that demand stable viscosity, anti-wear protection, and micropitting resistance—especially in high-duty assembly, packaging, and logistics lines. In parallel, the global vehicle sector, another gearbox-heavy ecosystem across final drives, transfer cases, and plant equipment, kept output high in 2024.

OICA publishes country and segment totals and downloadable tables that indicate the continued scale of production lines consuming industrial lubricants. Together, rising robot stocks and sustained auto production increase the number of gearboxes in service and the frequency of lubricant changeouts, pushing steady demand for premium gear oils.

Regional Analysis

Asia-Pacific leads with a 43.8% share and a USD 3.9 Billion market value.

In 2024, Asia-Pacific emerged as the dominant region, capturing a commanding 43.8% share of the global gear oil market, valued at around USD 3.9 billion. This dominance is driven by rapid industrialization, automotive manufacturing growth, and expanding heavy machinery operations across China, India, Japan, and South Korea.

China alone accounts for a significant portion of global automotive output. India’s industrial development and ongoing infrastructure investments under government programs such as Make in India and the National Infrastructure Pipeline (NIP) continue to propel lubricant consumption across construction and power-generation sectors.

The region’s strong manufacturing base in cement, steel, mining, and shipbuilding drives the use of heavy-duty gear oils designed to withstand high load and temperature conditions. Japan and South Korea, with advanced automation and robotics integration, are further boosting demand for synthetic and semi-synthetic gear oils that extend gearbox life and reduce maintenance frequency.

Multinational lubricant producers are expanding blending and R&D facilities across the region to meet local industrial needs and sustainability goals. As Asia-Pacific continues to industrialize and electrify its vehicle and machinery base, its commanding market share reinforces the region’s pivotal role in shaping the future of the global gear oil industry.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BP PLC is a major force in the gear oil market, renowned for its advanced industrial lubricants. The company’s Castrol brand is globally recognized for high-performance products, including a comprehensive range of synthetic and mineral gear oils. BP invests heavily in research to develop solutions that enhance equipment efficiency and durability across automotive and industrial sectors.

China Petroleum and Chemical Corporation (Sinopec) holds a formidable position in the gear oil market. It leverages its massive, integrated refining and petrochemical infrastructure to produce a wide array of lubricants, including industrial gear oils. Sinopec’s strength lies in its vast domestic market share and competitive pricing.

Chevron Corporation is a leading global competitor through its premium lubricants brand, Chevron Lubricants. The company is highly respected for its innovative formulations, including its synthetic gear oils under the Ursa and RPM brands. Chevron emphasizes delivering products that provide exceptional protection against wear, deposit formation, and thermal degradation.

Top Key Players in the Market

- BP PLC

- China Petroleum and Chemical Corporation

- Chevron Corporation

- ExxonMobil Corporation

- FUCHS

- Gazprom Neft PJSC

- Gulf Oil Corporation Limited

- Idemitsu Kosan Co. Ltd

- Indian Oil Corporation Ltd

- JX Nippon Oil and Energy Corporation

Recent Developments

- In 2025, Sinopec will deal with Algeria’s Sonatrach for the Hassi Berkine North oil block, enhancing upstream feedstock security for downstream products like gear oils. The company achieved record oil and gas output in the first half of 2024, processing of crude.

- In 2024, Chevron partnered with India’s Hindustan Petroleum Corporation Ltd (HPCL) to license, produce, and market Caltex-branded lubricants, including gear oils for industrial and commercial vehicles, marking its re-entry into the Indian market after 12 years and targeting the burgeoning automotive sector.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 9.0 Billion |

| Forecast Revenue (2034) | USD 11.7 Billion |

| CAGR (2025-2034) | 2.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Transportation, Manual Gearbox, Automatic Gearbox, Axle Oils, Industrial), By Viscosity Grade (Sae 75W-90, Sae 80W-90, Sae 85W-140), By End-user (Automotive and Transportation, Power Generation, Heavy Equipment, Metallurgy and Metalworking, Others), By Distribution Channel (Aftermarket, Original Equipment Manufacturer) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | BP PLC, China Petroleum and Chemical Corporation, Chevron Corporation, ExxonMobil Corporation, FUCHS, Gazprom Neft PJSC, Gulf Oil Corporation Limited, Idemitsu Kosan Co. Ltd, Indian Oil Corporation Ltd, JX Nippon Oil and Energy Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |