Quick Navigation

Report Overview

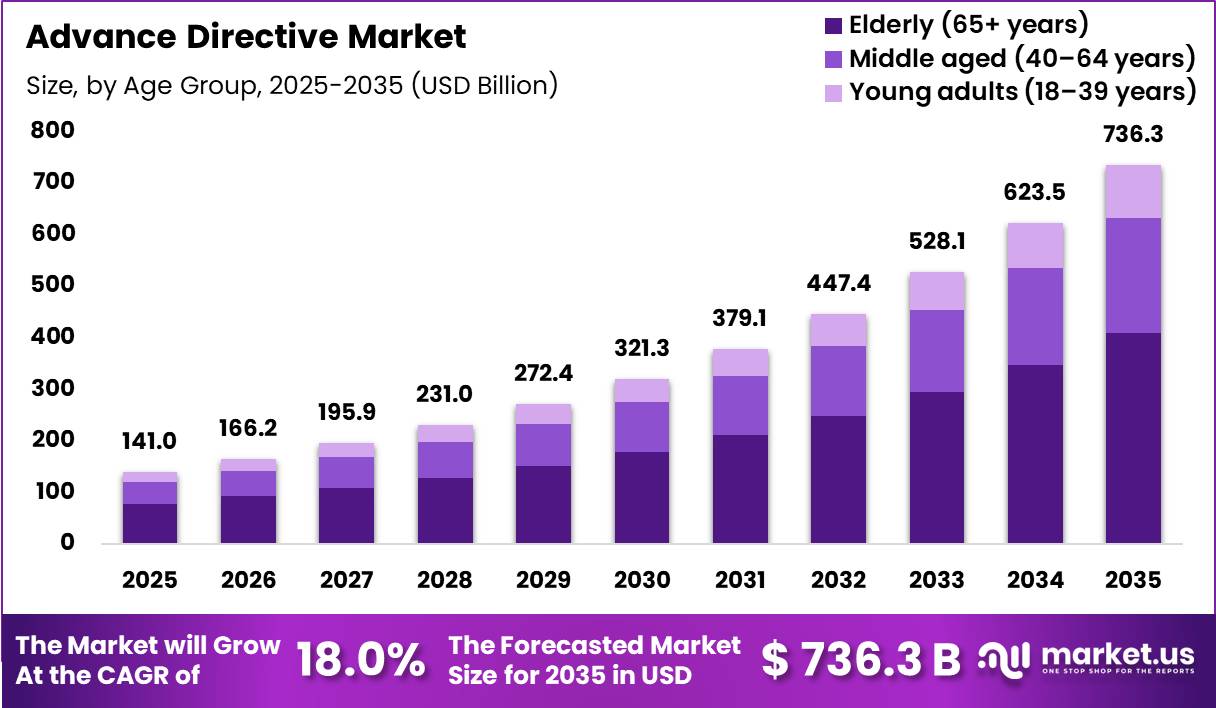

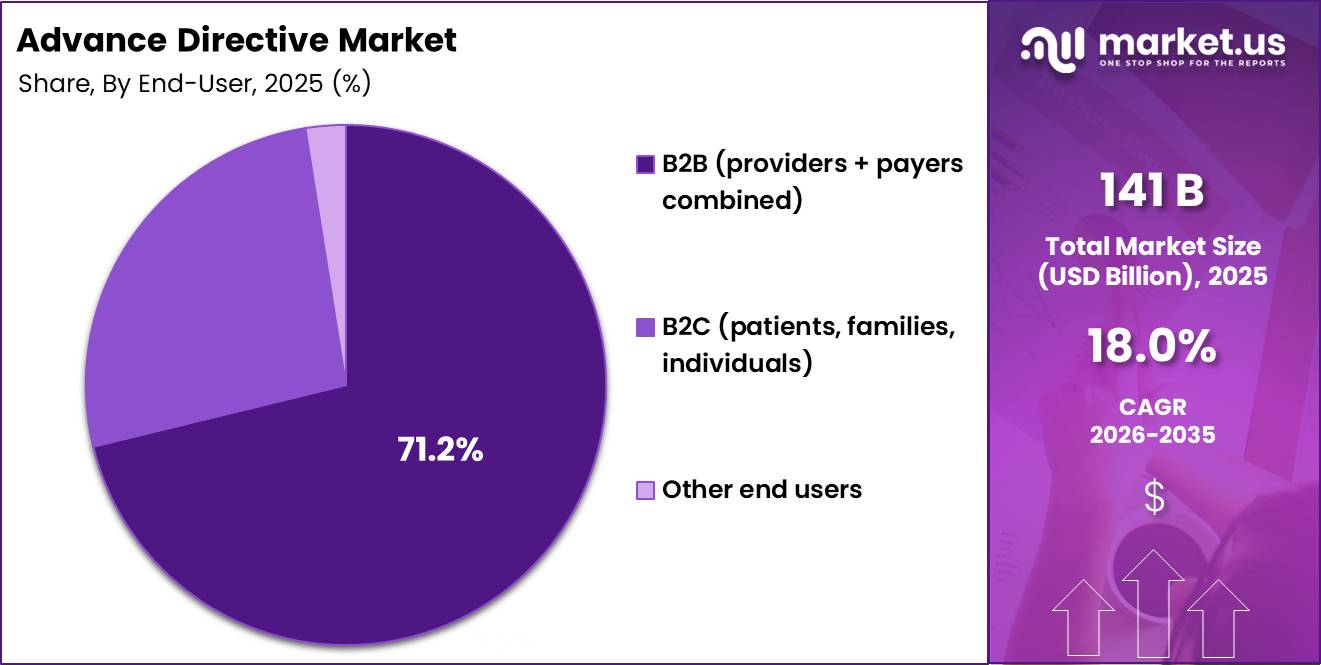

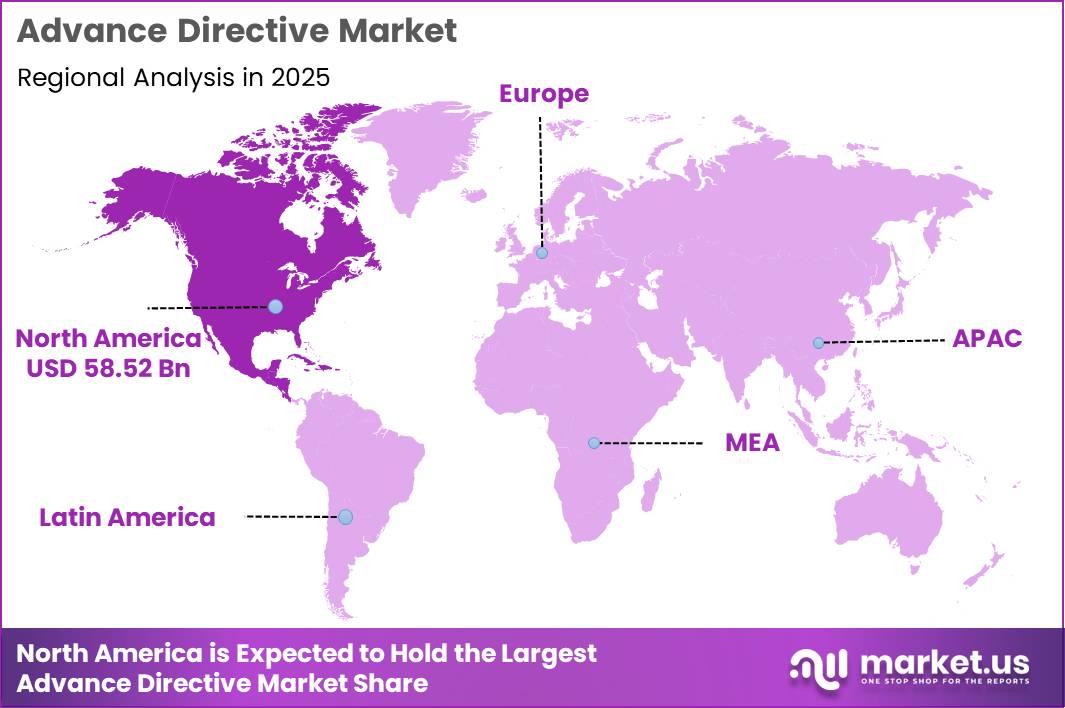

Global Advance Directive Market size is expected to be worth around US$ 736.3 Billion by 2035 from US$ 141.0 Billion in 2025, growing at a CAGR of 18.0% during the forecast period from 2026 to 2035. North America held a dominant market position, capturing more than a 41.5% share, holding USD 58.52 Billion in revenue.

The global advance directives market is increasingly being shaped by the integration of care planning into mainstream clinical workflows, where the focus has shifted from static documentation to real-time usability of patient preferences. Healthcare systems are under growing pressure to reduce unnecessary end-of-life interventions while ensuring care aligns with patient intent, which is pushing advance directives into core operational strategy rather than administrative compliance.

- In May 2025, Koda Health partnered with Medical Home Network to expand advance care planning access across select federally qualified health centers. Koda’s platform supports EMR integration and HL7 FHIR standards, helping providers access patient care preferences during critical moments. This reflects the wider market shift toward interoperable, system-wide advance care planning ecosystems where directives are not only recorded but actively surfaced at the point of care.

At the same time, demand is being reinforced by the increasing complexity of patient care pathways, particularly among aging populations with chronic conditions requiring frequent clinical decision-making. Hospitals and payers are prioritizing structured, guided conversations over self-directed tools because facilitated engagement improves accuracy, reduces legal ambiguity, and enhances alignment between patients and providers. This has strengthened the position of service-led models, where human-led consultation remains central even as software platforms scale.

Looking forward, the market is expected to continue evolving toward fully interoperable, system-wide advance care planning ecosystems, where directives are continuously accessible across emergency, inpatient, and outpatient settings. The competitive advantage will increasingly depend on the ability to integrate seamlessly into clinical infrastructure and ensure that patient preferences are not only recorded but actively surfaced at the point of care, especially in high-stakes medical situations.

Key Takeaways

- Market Size: Global Advance Directive Market size is expected to be worth around US$ 736.3 Billion by 2035 from US$ 141.0 Billion in 2025.

- Market Share: The market is growing at a CAGR of 18.0% during the forecast period from 2026 to 2035.

- Age Group Analysis: On the basis of Age Group, the Elderly (65+ years) dominated the market, constituting 55.8% of the total market share.

- Component Analysis: On the basis of Component, the Services segment dominated the market, constituting 70.2% of the total market share.

- End User Analysis: Based on the End-user, B2B (providers + payers combined) led the market, comprising 71.2% of the total market.

- Regional Analysis: North America held a dominant market position, capturing more than a 41.5% share, holding USD 58.52 billion in revenue.

Age Group Analysis

Elderly (65+) Represents the Key Revenue-Generating Segment in the Global Advance Directive Market.

On the basis of Age Group, the Elderly (65+ years) segment dominates the global advance directive market with 55.8% share, primarily driven by higher incidence of chronic diseases, frequent hospital admissions, and elevated dependency on intensive and end-of-life care decision-making. This cohort consistently represents the highest exposure to complex clinical interventions, making advance directives essential for ensuring treatment alignment with patient preferences during critical and high-risk medical events.

The dominance is also reinforced by healthcare systems prioritizing structured advance care planning to reduce unnecessary ICU utilization and improve decision efficiency for elderly patients. This trend has been further strengthened by the integration of advance care planning into digital clinical infrastructure.

- In February 2024, Sharp HealthCare continued supporting advance care planning by providing patients with advance directive resources and encouraging completed directives to be shared with medical providers for inclusion in medical records. This reflects the broader healthcare shift toward making patient care preferences more accessible within clinical documentation and care workflows.

Such system-level integration reflects a broader shift toward embedding advance directives into routine clinical operations rather than treating them as standalone administrative records. Meanwhile, the middle-aged (40–64 years) and young adult (18–39 years) segments are gradually expanding due to preventive care awareness and digital health adoption, but their overall market contribution remains secondary to the structural dominance of the elderly population.

Component Analysis

Services Segment Dominates the Global Advance Directive Market.

On the basis of Component, the Services segment holds the leading position in the global advance directive market with 70.2% share, driven by the critical need for structured, clinician-led engagement and legally compliant documentation of patient care preferences. Advance care planning is inherently sensitive and complex, requiring guided discussions between patients, families, and healthcare providers to ensure accuracy, clarity, and alignment with clinical decision-making. As a result, healthcare institutions continue to depend on service-based models rather than standalone digital tools, particularly in end-of-life and high-dependency care settings.

This dominance is further reinforced by institutional healthcare workflows, where services play a central role in embedding advance directive discussions into routine clinical pathways and value-based care programs.

- In March 2025, VyncaCare expanded its structured care planning services across healthcare systems. This milestone strengthened the adoption of facilitated advance care conversations within provider networks.

Meanwhile, the Software segment, although comparatively smaller, is steadily expanding as digital platforms and EHR-integrated solutions enhance the storage, accessibility, and interoperability of patient directives across care settings. However, it continues to function primarily as an enabling infrastructure layer supporting service-led delivery rather than replacing it.

End User Analysis

B2B Segment Leads the Global Advance Directive Market.

On the basis of End-user, the B2B segment (providers and payers combined) dominates the global advance directive market with 71.2% share, reflecting the fact that advance care planning is increasingly being driven by healthcare institutions rather than individual consumers.

Hospitals, integrated delivery networks, physician groups, and insurers are incorporating advance directives into routine care pathways as part of broader efforts to improve care quality, strengthen patient-centered decision-making, and manage healthcare costs. Because providers are typically responsible for initiating, documenting, and acting upon patient preferences during critical care situations, institutional demand remains substantially higher than direct-to-consumer adoption.

The segment’s dominance is also supported by the transition toward value-based care models, where healthcare organizations are incentivized to reduce avoidable hospitalizations, unnecessary intensive treatments, and care interventions that may not align with patient wishes. Advance directives have become an important operational tool for achieving these objectives, helping providers improve care coordination while minimizing clinical uncertainty during emergency and end-of-life situations.

- In July 2025, Koda Health expanded its deployment across provider networks by announcing a comprehensive integration with Epic Systems, embedding advance care planning directly into electronic health record workflows.

This institutional integration creates a scalable adoption model that is difficult to replicate through individual consumer engagement alone. While the B2C segment continues to benefit from growing awareness and digital accessibility, and other end users are gradually expanding through community-based initiatives, market demand remains overwhelmingly concentrated within provider- and payer-led healthcare ecosystems.

Key Market Segments

By Age Group

- Elderly (65+ years)

- Middle aged (40–64 years)

- Young adults (18–39 years)

By Component

- Services

- Software

By End-User

- B2B (providers + payers combined)

- B2C (patients, families, individuals)

- Other end users

Drivers

Healthcare Systems Are Embedding Advance Care Planning into Everyday Care Delivery

Advance directives are increasingly moving from the margins of healthcare administration into the center of clinical and operational strategy. Hospitals, physician networks, and health insurers are under growing pressure to deliver care that is both patient-centered and cost-effective, making advance care planning an important tool for improving decision-making and reducing unwanted interventions.

Rather than viewing advance directives as a compliance requirement, healthcare organizations are now treating them as a practical mechanism for improving care coordination, minimizing treatment uncertainty, and ensuring patient preferences are available when critical decisions need to be made. This shift is creating sustained demand for solutions that can integrate seamlessly into provider workflows.

Aging Populations Are Creating a Larger and More Immediate Need for Advance Care Planning

The steady growth of the elderly population is fundamentally expanding the addressable market for advance directives. Older adults account for a disproportionate share of hospital admissions, chronic disease management, and end-of-life care decisions, making proactive healthcare planning increasingly important for both patients and providers.

As healthcare systems manage growing volumes of aging patients, there is a stronger emphasis on documenting care preferences before complex medical situations arise. A key example is Iris Healthcare (an Aledade company), which utilizes population health data within primary care networks to identify high-risk elderly patients and deliver structured, virtual advance care planning services well ahead of critical hospitalizations.This not only helps improve patient outcomes but also supports more efficient use of healthcare resources by reducing ambiguity during treatment decisions.

Restraints

Workforce Limitations, Integration Complexity, and Regulatory Variability Continue to Challenge Market Expansion

Despite strong long-term growth prospects, the advance directive market faces meaningful constraints stemming from its heavy dependence on human-led care planning services. Unlike many healthcare technology solutions that can be rapidly scaled through software deployment alone, advance care planning requires skilled facilitators capable of navigating sensitive discussions around serious illness, treatment preferences, and end-of-life care.

As healthcare organizations expand ACP programs, they often encounter workforce capacity limitations that restrict the number of patients who can be effectively engaged. This creates a structural challenge where demand can grow faster than the availability of qualified professionals needed to deliver high-quality planning services.

At the same time, software adoption is often slowed by the complexity of integrating advance directive platforms into existing healthcare IT environments. Connecting ACP solutions with electronic health record systems requires significant technical resources, workflow redesign, and ongoing interoperability maintenance, increasing implementation costs and extending procurement timelines.

In addition, regulatory requirements governing advance directives frequently differ across jurisdictions, creating compliance burdens for platform providers. Companies such as MyDirectives, Inc. (formerly ADvault, Inc.). must maintain extensive jurisdiction-specific documentation and compliance capabilities to ensure legal validity across different healthcare settings.

Together, workforce constraints, integration challenges, and regulatory fragmentation continue to moderate the pace of market expansion despite growing institutional demand.

Opportunity

Payer-Led Care Management Expansion and Digital Health Adoption Create New Growth Pathways

One of the most attractive growth opportunities for the advance directive market lies in the increasing involvement of payers and value-based care organizations in advance care planning programs. As healthcare systems focus on improving patient outcomes while controlling costs, advance directives are becoming a strategic tool for reducing unnecessary hospitalizations, avoidable intensive care utilization, and treatment decisions that do not align with patient preferences. Health plans and provider networks have a strong financial incentive to invest in scalable advance care planning infrastructure that supports better care coordination and population health management.

- In November 2025, Evolent Health (operating Vital Decisions LLC) expanded its clinical counseling partnerships with major health plans to integrate goal-of-care discussions directly into payer-led care management pathways, capturing commercial growth through institutional alignment.

A second major opportunity is emerging from the continued digitization of healthcare and the expansion of advance care planning into new geographic markets and care settings. Growing adoption of electronic health records, telehealth services, and interoperable healthcare platforms is making it easier for providers to capture, store, and access patient preferences across the continuum of care.

At the same time, healthcare systems across Europe and Asia Pacific are increasingly emphasizing patient-centered care and digital health modernization, creating favorable conditions for advance directive platform adoption.

- In Aproil 2026, ThoroughCare, Inc. updated its comprehensive digital care coordination platform to natively align with evolving Medicare advance care planning codes, enabling B2B provider networks to capture, scale, and reimburse digital preference tracking globally.

Trends

AI-Driven Care Planning & Predictive Patient Identification.

Artificial intelligence is becoming a defining force in the advance directive market by addressing one of the industry’s core constraints-limited workforce capacity in facilitator-led care planning. AI-assisted tools are increasingly being used to support clinicians during goals-of-care conversations by providing structured prompts, real-time decision support, and automated documentation within electronic health records.

At the same time, predictive analytics models are helping healthcare organizations identify high-risk patients who are most likely to require near-term critical care decisions, enabling earlier and more targeted advance care planning interventions. This shift is improving both efficiency and consistency, allowing providers to scale ACP programs without proportionally increasing staffing requirements.

- In 2026, WiserCare Inc. expanded the deployment of its AI-enabled clinical agents across health systems, allowing patient-guided preference modeling to automatically synthesize clinical evidence and deliver structured, pre-visit goals-of-care summaries straight to medical teams.

Interoperability & Digital Registries Enhancing Clinical Access to Advance Directives.

A second major trend is the rapid advancement of interoperability standards and digital registry systems that ensure advance directives are accessible at the point of care. Historically, one of the key limitations of advance care planning has been that directives are often unavailable during emergency or inpatient decision-making situations due to fragmented storage systems.

The emergence of FHIR-based standards and national registry networks is addressing this gap by enabling structured, real-time access to patient preferences across healthcare settings, including emergency departments, ICUs, and surgical units.

- In March 2026, ADVault, Inc. (MyDirectives, Inc.) expanded its cloud-based registry infrastructure by driving the cross-institutional adoption of the HL7 FHIR Advance Directive Interoperability (ADI) standards, transforming static legacy files into live, queryable clinical assets accessible 24/7 across disparate hospital networks.

Geopolitical Impact Analysis

Geopolitical Drivers Reshaping Advance Directive Adoption and Healthcare Policy Alignment.

The advance directives market is increasingly shaped by national healthcare policy frameworks, reimbursement design, and regulatory governance rather than traditional trade or cross-border commercial dynamics. In the United States, the most influential geopolitical lever remains CMS-driven value-based care policy and Medicare Advantage incentive structures, which directly determine how health plans prioritize and fund advance care planning (ACP) programs.

Because ACP initiatives are often justified through quality improvement scores and downstream cost reduction, any changes to Medicare Advantage Star Ratings methodology or bonus structures immediately translate into budgetary recalibration across payer organizations. This makes federal policy direction a direct demand-shaping variable, where even incremental adjustments in quality metrics can materially alter the commercial attractiveness and scale of ACP vendor adoption.

In parallel, global regulatory harmonization and workforce constraints are reshaping the structure of ACP delivery models across developed healthcare markets. The European Health Data Space (EHDS), enacted under Regulation (EU) 2025/327, is establishing a unified interoperability framework that enables structured patient-generated health data, including advance directives, to be securely exchanged across EU member states through platforms such as MyHealth@EU. This significantly improves the feasibility of scalable digital ACP deployment across Europe by reducing fragmentation in data access and compliance standards.

At the same time, persistent healthcare workforce shortages in aging economies such as Japan and the United States are creating structural pressure to substitute scarce clinical labor with automation-enabled workflows. This shift is accelerating demand for software-driven ACP infrastructure solutions such as ThoroughCare, Inc., Honor My Decisions LLC, and Affirm Health Inc., which enable providers to scale documentation and care planning processes without proportionally increasing clinician workload.

Regional Analysis

North America Held the Largest Share of the Global Advance Directives Market.

North America accounted for 41.5% of the global advance directives market, driven by the strong integration of advance care planning (ACP) into the region’s healthcare delivery system. The United States leads the market due to favorable reimbursement policies under Medicare, widespread adoption of value-based care models, and established legal frameworks supporting advance directives.

Healthcare providers increasingly incorporate ACP discussions into routine care to improve patient outcomes, enhance care coordination, and reduce avoidable healthcare expenditures, making advance directives a key component of patient-centered care.

The region’s dominance is further supported by a large aging population, high prevalence of chronic diseases, and extensive adoption of electronic health records that facilitate the documentation and accessibility of patient preferences across care settings.

Growing awareness of end-of-life planning, increasing demand for personalized healthcare decision-making, and ongoing investments in healthcare digitalization continue to accelerate market growth. Canada complements regional expansion through advancing digital health initiatives and broader integration of advance care planning within its publicly funded healthcare system.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global advance directives market remains fragmented and in an early-to-mid commercialization phase, where competitive advantage is defined less by scale and more by clinical integration depth, interoperability capability, and ability to operationalize advance care planning within real healthcare workflows.

The market is broadly structured into three tiers: registry-led platforms with strong FHIR-based EHR connectivity and directive portability, enterprise ACP program providers embedded within health systems and payer value-based care contracts, and emerging technology innovators focused on AI-enabled engagement, predictive patient identification, and workflow automation. Across all tiers, vendors are increasingly evaluated on measurable outcomes such as directive retrieval at point of care, ACP completion rates, and demonstrated impact on utilization and cost reduction.

At the competitive core, ADvault, Inc. and MyDirectives, Inc. lead in digital registry infrastructure and interoperability, strengthening real-time access to advance directives across care settings. Vital Decisions LLC (Evolent Health) anchors payer-linked ACP delivery models with large-scale Medicare Advantage integration, while enterprise-focused providers such as VyncaCare, Iris Healthcare (Aledade, Inc.), and ThroughCare / ThoroughCare, Inc. expand adoption through workflow embedded solutions across health systems and post-acute care networks.

Meanwhile, innovation-led players including Koda Health, WiserCare Inc., Affirm Health Inc., and MIDEO are differentiating through AI-assisted decision support, predictive risk stratification, and digital engagement models designed to improve ACP uptake and scalability. Competitive dynamics are increasingly shaped by EHR integration depth, FHIR interoperability standards, and proven ROI within value-based care contracts, with ongoing consolidation further embedding ACP capabilities into broader population health management ecosystems.

The following are some of the major players in the industry

- ADvault, Inc.

- VyncaCare

- WiserCare Inc.

- Sharp HealthCare

- ACP Decisions (Nous Foundation, Inc.)

- Iris Healthcare (Aledade, Inc.)

- Bronson Health Care Group, Inc.

- Koda Health

- ThroughCare / ThoroughCare, Inc.

- Vital Decisions LLC (Evolent Health)

- Affirm Health Inc.

- MIDEO

- New Century Health

- Honor My Decisions LLC

- MyDirectives, Inc.

- Others

Recent Development

- In February 2025, MIDEO Health entered into a major cross-industry development partnership with Backline by DrFirst, Five Wishes, and MyDirectives to launch a comprehensive solution called “ACP Complete,” combining virtual medical consultation routing with legally binding, accessible video advance directive storage.

- In March 2025, Vynca (VyncaCare) announced a major leadership expansion by appointing a new Chief Commercial Officer and Senior Vice President of Marketing to accelerate its national footprint and integrate its structured palliative care plans and electronic advance care platform directly into complex provider and payer networks.

- In October 2025, Koda Health closed an oversubscribed $7 million Series A funding round led by venture capital firm Evidenced to scale its automated, interactive advance care planning workflows deeper into prominent national provider networks, including Epic Systems and Guidehealth.

- In February 2026, ThoroughCare, Inc. rolled out a comprehensive platform enhancement to natively map its care management software against CMS’s updated Medicare Advance Care Planning CPT codes, helping B2B provider networks systematically track, scale, and reimburse face-to-face preference tracking consultations.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 141.0 Billion |

| Forecast Revenue (2035) | US$ 736.3 Billion |

| CAGR (2026-2035) | 18.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Age Group (Elderly 65+ years, Middle-aged 40–64 years, Young Adults 18–39 years), By Component (Services, Software), By End User (B2B, B2C–Patients, Families, Individuals, Other End Users) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | ADvault Inc., VyncaCare, WiserCare Inc., Sharp HealthCare, ACP Decisions (Nous Foundation Inc.), Iris Healthcare (Aledade Inc.), Bronson Health Care Group Inc., Koda Health, ThroughCare / ThoroughCare Inc., Vital Decisions LLC (Evolent Health), Affirm Health Inc., MIDEO, New Century Health, Honor My Decisions LLC, MyDirectives Inc., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |