Quick Navigation

Report Overview

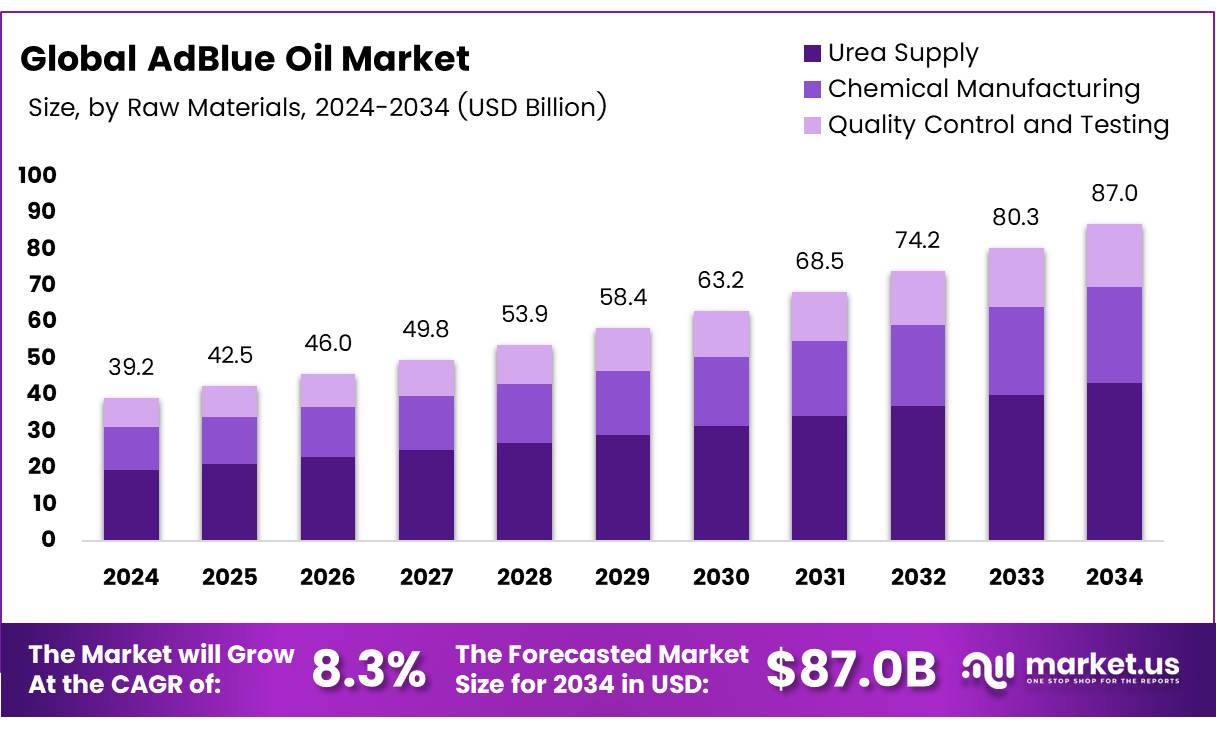

The Global AdBlue Oil Market size is expected to be worth around USD 87.0 Billion by 2034, from USD 39.2 Billion in 2024, growing at a CAGR of 8.3% during the forecast period from 2025 to 2034.

The AdBlue oil market is closely tied to the growing demand for cleaner, more environmentally friendly automotive solutions. AdBlue, a non-toxic, colorless liquid composed of 32.5% urea and 67.5% demineralized water, plays a pivotal role in reducing nitrogen oxide (NOx) emissions in diesel vehicles equipped with selective catalytic reduction (SCR) systems.

According to Neste, the use of AdBlue in these systems can reduce NOx emissions by up to 90%. As the global automotive industry increasingly shifts toward stringent environmental standards, the adoption of AdBlue as an essential component in diesel vehicles continues to rise. The market is expected to expand significantly, fueled by stricter emission regulations and a global push for sustainable transportation.

The AdBlue oil market is poised for substantial growth in the coming years. Factors such as enhanced government regulations on vehicle emissions, rising environmental awareness, and the global shift toward green technologies are accelerating the demand for AdBlue.

The introduction of more stringent emission standards, particularly in regions like Europe and North America, is pushing manufacturers to incorporate SCR systems in newer diesel vehicles. Additionally, increasing investments by governments to support cleaner technologies and the rise in vehicle production further contribute to the growth trajectory.

According to ISO 22241 standards, the consistent use of AdBlue ensures the performance and longevity of SCR systems, leading to its wider adoption. Furthermore, key industry players are capitalizing on the rising need for eco-friendly fuel additives, creating lucrative opportunities for both established and emerging businesses in this sector.

Governments worldwide are playing an instrumental role in driving the adoption of AdBlue oil. Enhanced environmental regulations, such as the Euro 6 standards in Europe, require all diesel vehicles to incorporate SCR technology, which directly increases demand for AdBlue. As per current regulatory trends, automakers are compelled to integrate SCR systems in their vehicles to meet these stringent emission guidelines.

Government investments aimed at environmental sustainability, such as tax incentives and subsidies for green technologies, have further encouraged the use of AdBlue in diesel engines. These initiatives are expected to support market growth by making AdBlue more accessible to a broader consumer base.

Moreover, regulations like ISO 22241 provide assurance in product quality and consistency, ensuring that AdBlue remains an effective tool in reducing harmful emissions, and this will continue to foster market expansion.

By addressing both environmental concerns and technological advancements, the AdBlue oil market is well-positioned for growth and innovation in the years ahead. The increasing regulatory pressures combined with the clear environmental benefits of AdBlue make this market an attractive segment for stakeholders and investors looking to capitalize on the growing demand for sustainable transportation solutions.

Key Takeaways

- The global AdBlue Oil market is projected to reach USD 87.0 billion by 2034, growing at a CAGR of 8.3% from 2025 to 2034.

- Urea is the dominant raw material for AdBlue production, driven by its availability, cost-effectiveness, and role in reducing emissions in diesel vehicles.

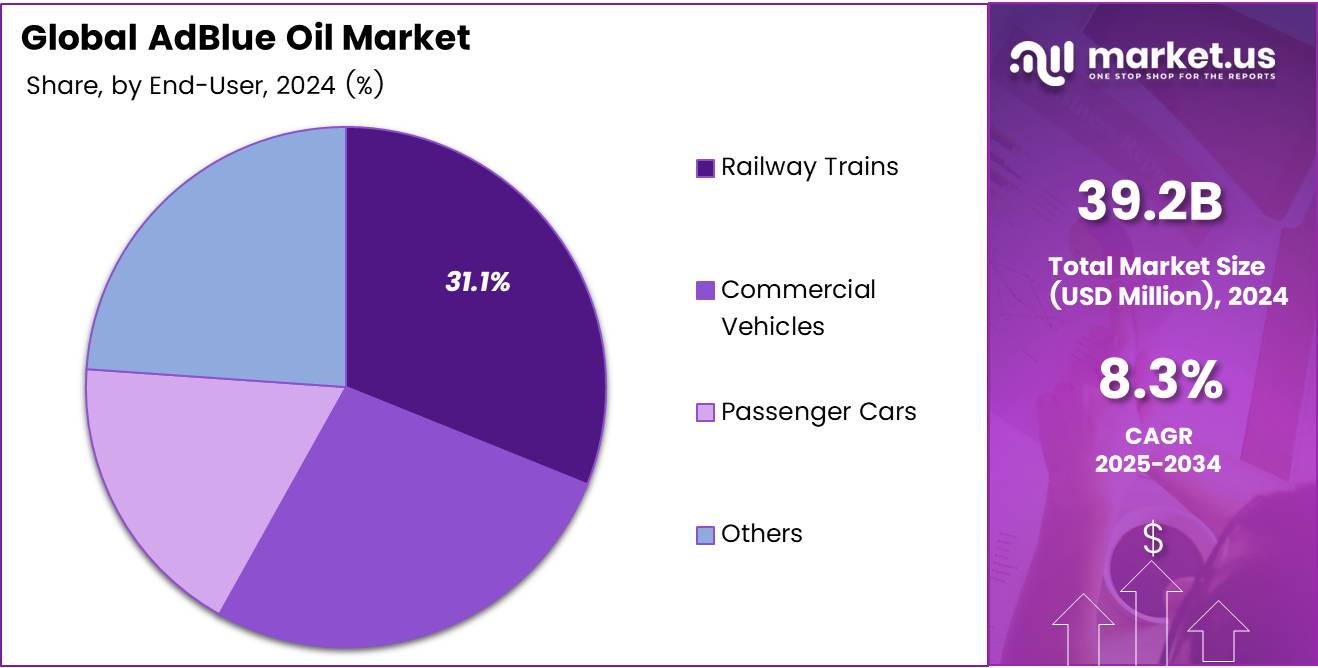

- Railway trains hold the largest share (31.1%) in the end-user segment, driven by stricter emission regulations in railway operations.

- Bulk distribution leads the market in logistics due to cost advantages and logistical efficiency for large-scale consumers.

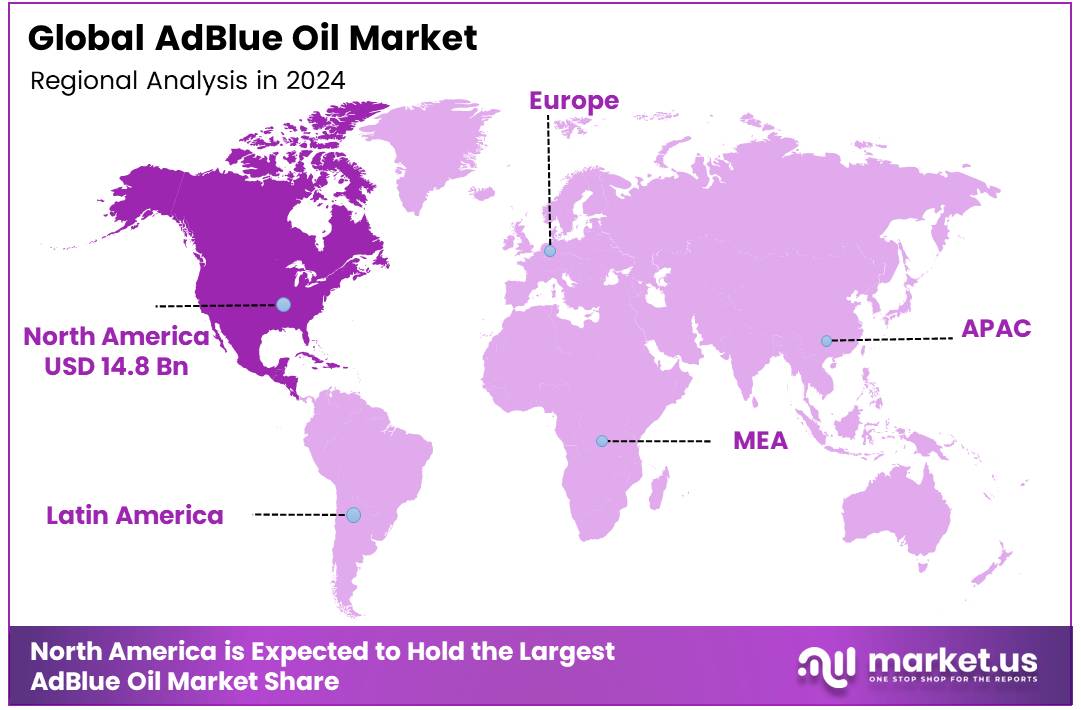

- North America dominates the global market, accounting for 38.4% of the market share, driven by stringent environmental regulations and green technology adoption.

Raw Materials and Production Analysis

Urea Supply Leads AdBlue Oil Market by Raw Materials and Production Analysis in 2024

In 2024, urea supply held a dominant position within the By Raw Materials and Production Analysis segment of the AdBlue Oil Market. Urea accounted for a significant portion of the raw material demand due to its crucial role in the production of AdBlue, a vital component for reducing emissions in diesel vehicles. Its high availability and cost-effectiveness were key factors driving this dominance.

The chemical manufacturing sector also played a critical role in shaping the AdBlue Oil market. Advanced manufacturing processes enabled efficient scaling of production while maintaining strict quality control measures. This led to enhanced product consistency and performance, contributing to the continued reliance on urea as the primary raw material.

Additionally, the growing focus on stringent emissions regulations worldwide further boosted the demand for AdBlue, with urea remaining the preferred option due to its established effectiveness in reducing nitrogen oxide (NOx) emissions.

Quality control and testing procedures remain integral to ensuring compliance with environmental standards and customer expectations. As the market continues to expand, the strong market presence of urea is likely to persist, driven by regulatory pressures and technological advancements in chemical manufacturing.

End-User Analysis

Railway Trains Lead AdBlue Oil Market with 31.1% Share in 2024, Driven by Demand for Emission Control

In 2024, Railway Trains held a dominant market position in the By End-User Analysis segment of the AdBlue Oil Market, with a significant share of 31.1%. This prominence can be attributed to the growing emphasis on reducing nitrogen oxide (NOx) emissions in railway operations.

The adoption of stringent environmental regulations across various regions has led to increased use of AdBlue in locomotives, ensuring compliance with emission standards and enhancing operational efficiency.

Commercial Vehicles followed with a substantial share, driven by the widespread application of AdBlue in heavy-duty trucks and logistics fleets, where emission control is paramount for regulatory compliance and fuel efficiency.

Passenger Cars accounted for a notable portion of the market, benefiting from the rising demand for clean diesel vehicles, particularly in European markets. The Others segment, encompassing various smaller applications, contributed to the remaining market share, though at a relatively smaller scale.

The overall market landscape reflects an ongoing shift toward more sustainable transportation solutions, with railway trains, in particular, continuing to be a key driver of demand for AdBlue in 2024.

Distribution and Logistics Analysis

Bulk Distribution leads with a dominant market share, driven by economies of scale and efficiency

In 2024, Bulk Distribution held a dominant market position in the By Distribution and Logistics Analysis segment of the AdBlue Oil Market. This strong market presence is primarily attributed to the ability of bulk distribution models to cater to large-scale consumers such as fleet operators and industrial entities. These models provide significant cost advantages due to economies of scale and offer enhanced logistical efficiencies in product delivery, especially in regions with high demand.

Packaging and Bottling followed as a crucial sub-segment. The packaging and bottling sector has benefited from growing consumer demand for smaller, more accessible quantities of AdBlue, facilitating retail sales and easier storage for end-users.

The Transportation and Storage segment, though essential, has seen more moderate growth. This segment’s development is driven by the need for specialized storage solutions and temperature-controlled transport systems to maintain the quality and consistency of AdBlue during its delivery across regions. However, transportation costs and logistical challenges have somewhat limited its larger expansion relative to bulk distribution.

Key Market Segments

By Raw Materials

- Urea Supply

- Chemical Manufacturing

- Quality Control and Testing

By End-User

- Railway Trains

- Commercial Vehicles

- Passenger Cars

- Others

By Distribution and Logistics

- Bulk Distribution

- Packaging and Bottling

- Transportation and Storage

Drivers

Stringent Environmental Regulations Drive AdBlue Market Expansion

The AdBlue oil market is primarily driven by stringent environmental regulations, such as the Euro 6 standards, which mandate lower vehicle emissions. These regulations require the use of AdBlue in diesel engines to reduce nitrogen oxide (NOx) emissions through Selective Catalytic Reduction (SCR) technology.

As governments worldwide continue to tighten emission norms, the demand for AdBlue increases as an essential component in meeting these standards.

Additionally, the growing popularity of diesel vehicles, which rely on AdBlue to comply with emission requirements, further fuels market growth. Many governments also provide financial incentives or subsidies for vehicles equipped with SCR systems, promoting the use of AdBlue.

This, coupled with rising consumer awareness regarding environmental sustainability and a shift towards eco-friendly transportation, has significantly boosted the market for AdBlue. The growing focus on reducing vehicle emissions and promoting cleaner technologies is expected to continue driving the market forward.

Restraints

High Production Costs Limit AdBlue Market Growth

The production of AdBlue involves high costs, primarily due to the complexity of its manufacturing process and the specialized chemicals required, such as urea. These elevated production costs can result in higher retail prices, which may restrict the affordability of AdBlue for both consumers and businesses, particularly small or cost-sensitive operators.

As a result, some businesses may hesitate to adopt AdBlue technologies, especially in regions where cost efficiency is a critical factor. The relatively higher cost of AdBlue may also affect its penetration in emerging markets, where price sensitivity is often more pronounced. Consequently, the market’s expansion could be constrained as potential adopters, particularly in cost-conscious sectors, may choose to delay or forgo the adoption of emission-reducing technologies.

Furthermore, the reliance on external supply chains for key components could contribute to price fluctuations, further exacerbating affordability challenges in the long term. Therefore, high production costs remain a significant restraint for the AdBlue market, limiting its broader adoption and slowing down market growth in certain regions.

Growth Factors

Advancements in SCR Technology Drive Market Expansion

The AdBlue oil market is poised for growth due to several key developments. One significant opportunity lies in the continuous advancement of Selective Catalytic Reduction (SCR) technologies, which are becoming increasingly efficient and cost-effective.

This makes it easier for manufacturers to integrate AdBlue into vehicles, driving demand for the product. Additionally, the expansion of AdBlue refilling stations and distribution networks, particularly in emerging markets, is expected to increase accessibility and further fuel demand.

Another promising growth avenue is the increasing adoption of SCR technology in heavy-duty vehicles such as trucks, buses, and commercial fleets. As environmental regulations tighten, these vehicles are required to meet stricter emission standards, which is creating a stronger need for AdBlue.

Furthermore, the introduction of AdBlue in non-automotive applications, such as agriculture, marine, and rail sectors, offers new market opportunities beyond the traditional automotive space. These trends highlight the growing versatility of AdBlue and its potential to expand into a broader range of industries, ensuring steady market growth in the coming years.

Emerging Trends

Integration of IoT in SCR Systems Drives Market Efficiency

The AdBlue oil market is experiencing several key trends, with the integration of Internet of Things (IoT) technology standing out. IoT and sensor-based solutions are now being utilized to monitor AdBlue levels in vehicles, offering real-time data and alerts, which enhance operational efficiency and help reduce wastage.

Another significant trend is the growing use of AdBlue in hybrid vehicles, especially those with both electric and diesel powertrains, as these vehicles need AdBlue to meet stringent emission standards.

Additionally, there is an increasing focus on low-emission commercial vehicles, with manufacturers prioritizing the development of such vehicles that depend on AdBlue for their Selective Catalytic Reduction (SCR) systems to minimize harmful emissions.

Alongside this, the rising popularity of electric hybrid vehicles is also driving up the demand for AdBlue, as these hybrid models require AdBlue for optimized emission control. This shift is in line with the global push for sustainability and regulatory pressure to reduce carbon emissions. These trends are shaping the future of the AdBlue oil market, pushing for greater efficiency, broader vehicle adoption, and a stronger focus on environmental regulations.

Regional Analysis

North America Leads AdBlue Market with 38.4% Share, Driven by Strict Environmental Regulations and Growing Demand for Diesel Vehicles

The global AdBlue oil market is characterized by significant regional variations in demand and consumption patterns, with North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America each contributing distinctly to market dynamics.

North America dominates the global AdBlue market, accounting for approximately 38.4% of the total market share, with a market value of USD 14.8 billion. This is largely driven by stringent environmental regulations, such as the Environmental Protection Agency’s (EPA) Tier 3 standards in the United States, which have significantly increased the demand for selective catalytic reduction (SCR) technology in diesel-powered vehicles.

The region’s adoption of green technologies, coupled with the widespread use of heavy-duty trucks and commercial vehicles, further boosts the demand for AdBlue solutions.

Regional Mentions:

Europe represents the second-largest market for AdBlue, with a notable focus on compliance with the Euro 6 emissions standard. The European market benefits from an established infrastructure for AdBlue distribution and consumption, driven by both the automotive and industrial sectors. Europe’s market share is growing steadily due to rising environmental concerns and regulatory pressures on vehicle emissions.

Asia Pacific is expected to witness substantial growth, with countries such as China and India driving the demand for AdBlue. The increasing number of vehicles, particularly commercial and freight transportation, combined with the region’s growing emphasis on reducing air pollution, are key factors propelling market growth. While the market share of Asia Pacific is smaller compared to North America and Europe, its rapid industrialization and rising environmental standards are anticipated to bolster AdBlue consumption.

Middle East & Africa and Latin America represent emerging markets with growing adoption of AdBlue, though their share remains relatively lower. The Middle East’s reliance on heavy-duty vehicles and the ongoing expansion of the industrial sector are contributing factors, while Latin America is witnessing growth driven by increasing vehicle registrations and improving environmental regulations.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The global AdBlue oil market in 2024 is poised for steady growth, driven by increasing demand for low-emission vehicles and tighter regulatory standards on nitrogen oxide (NOx) emissions in several regions. Key players in the AdBlue market, including BASF SE, CF Industries Holdings, Inc., and TotalEnergies, are strategically positioned to leverage their technological capabilities and extensive distribution networks to meet this demand.

BASF SE, as a global leader in chemical products, is expected to maintain a dominant position in the market, offering high-quality SCR (Selective Catalytic Reduction) solutions. Its strong research and development efforts in catalysts and emissions control technologies further solidify its market standing.

CF Industries Holdings, Inc. benefits from its extensive expertise in nitrogen fertilizers, which directly feeds into the production of AdBlue, positioning it as a significant supplier of urea.

CrossChem Limited and Brenntag S.p.A. stand out for their established regional distribution capabilities and tailored product offerings. These companies provide critical supply chain flexibility, particularly in emerging markets where demand for AdBlue is on the rise.

Nissan Chemical Company and Mitsui Chemical, Inc. bring considerable technological expertise to the sector, particularly with innovations in urea production and refining, helping to address the increasing need for high-efficiency solutions in emission control systems.

The involvement of global energy players like Shell plc and TotalEnergies further underscores the integration of AdBlue into the broader ecosystem of sustainable energy solutions, with both companies actively contributing to the development of cleaner emissions technologies.

Overall, the competitive landscape is shaped by technological innovation, strategic partnerships, and growing regulatory pressure, setting the stage for further expansion in 2024 and beyond.

Top Key Players in the Market

- BASF SE

- CF Industries Holdings, Inc.

- CrossChem Limited

- Bosch Limited

- Nissan Chemical Company

- S.C. OMV PETROM S.A.

- Brenntag S.p.A.

- Graco Inc.

- Komatsu

- Mitsui Chemical, Inc.

- STOCKMEIER Group

- TotalEnergies

- Nandan Petrochem Ltd.

- Shell plc

Recent Developments

- In Dec 2024, Oil stock surged by 3.5% following its strategic partnership with Nyara Energy to produce high-performance automotive lubricants, a move expected to drive growth in the automotive sector.

- In Nov 2024, New Era Energy solidified its position as a leader in sustainable fuel by acquiring a key competitor, enhancing its capacity to provide eco-friendly energy solutions worldwide.

- In Jan 2023, Gulf enhanced its commitment to environmental sustainability by ensuring convenient access to AdBlue, a vital component for reducing emissions in diesel vehicles, benefiting both consumers and the planet.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 39.2 Billion |

| Forecast Revenue (2034) | USD 87.0 Billion |

| CAGR (2025-2034) | 8.3% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Raw Materials and Production (Urea Supply, Chemical Manufacturing, Quality Control and Testing), By End-User (Railway Trains, Commercial Vehicles, Passenger Cars, Others), By Distribution and Logistics (Bulk Distribution, Packaging and Bottling, Transportation and Storage) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | BASF SE, CF Industries Holdings, Inc., CrossChem Limited, Bosch Limited, Nissan Chemical Company, S.C. OMV PETROM S.A., Brenntag S.p.A., Graco Inc., Komatsu, Mitsui Chemical, Inc., STOCKMEIER Group, TotalEnergies, Nandan Petrochem Ltd., Shell plc |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |