Quick Navigation

Market Size & Trends

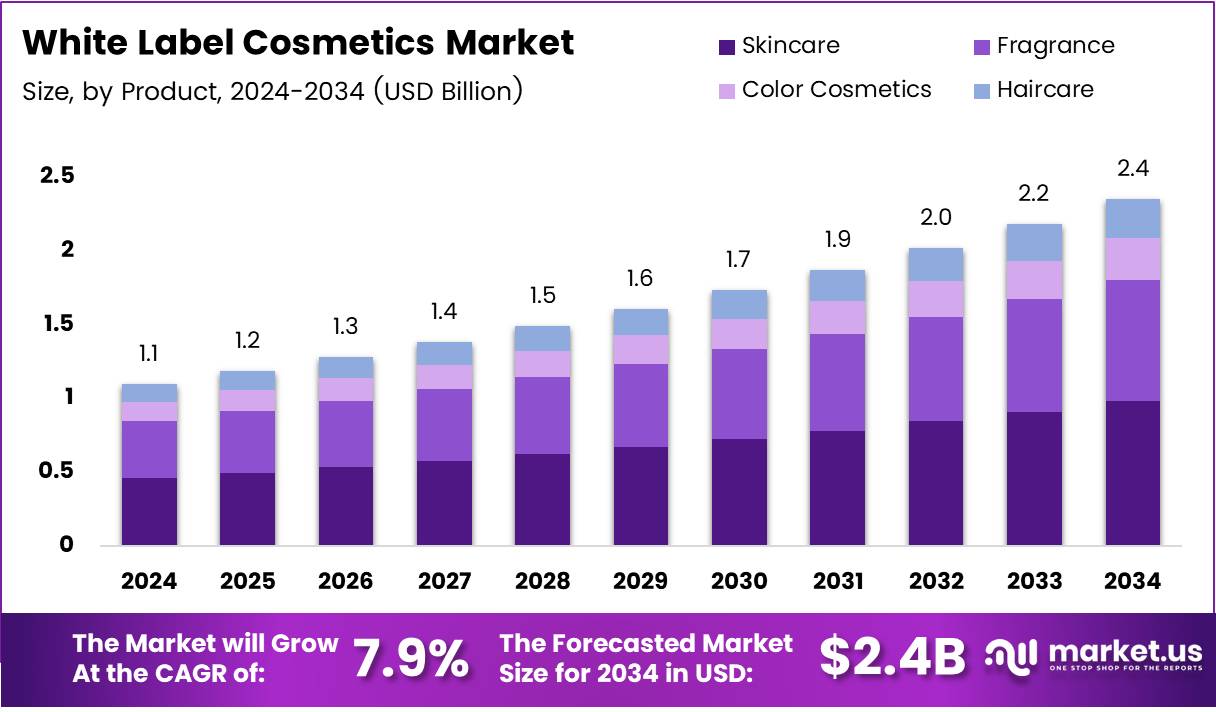

The Global White Label Cosmetics Market size is expected to be worth around USD 2.4 Billion by 2034, from USD 1.1 Billion in 2024, growing at a CAGR of 7.9% during the forecast period from 2025 to 2034. driven by rising consumer demand for personalized beauty products and the growing adoption of clean-label formulations.

Key Takeaways

- The Global White Label Cosmetics Market is projected to reach USD 2.4 Billion by 2034 from USD 1.1 Billion in 2024, growing at a CAGR of 7.9%.

- In 2024, Organic/Natural products dominated the By Type segment with an 85.7% market share.

- Skincare led the By Product segment in 2024, holding a 42.2% share.

- Women accounted for a 63.5% share in the By End Use segment in 2024.

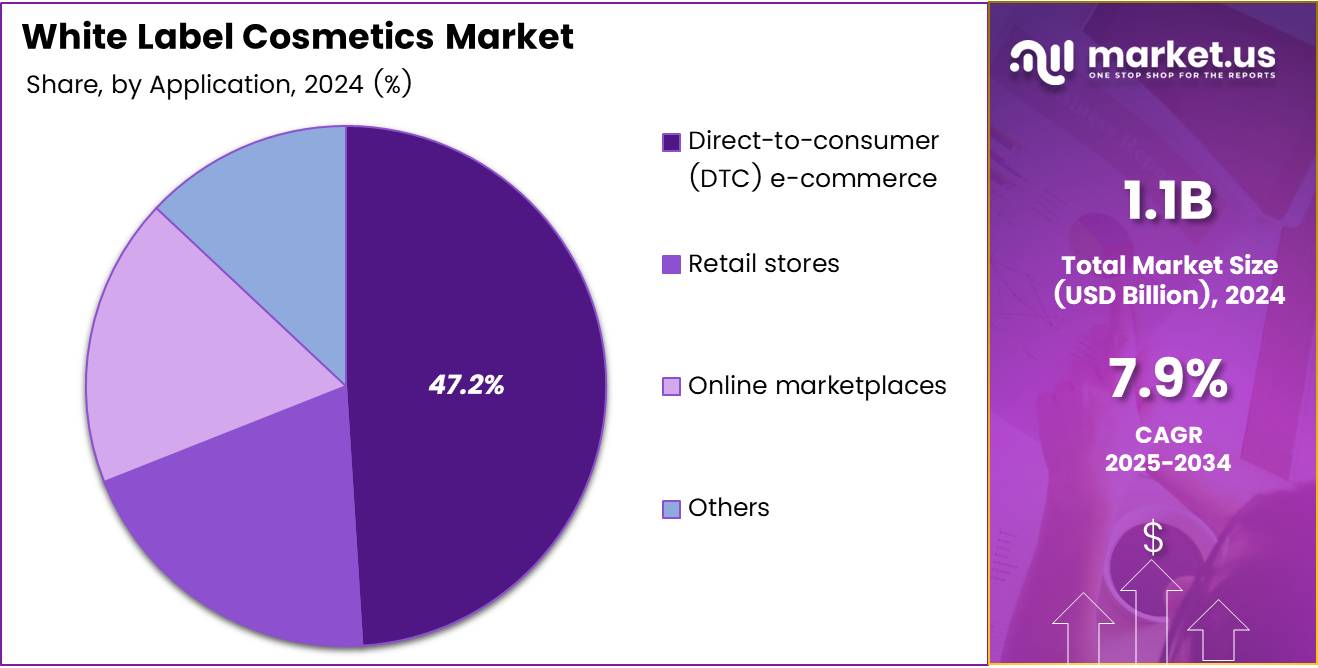

- Direct-to-consumer (DTC) e-commerce commanded a 47.2% share in the By Distribution Channel segment in 2024.

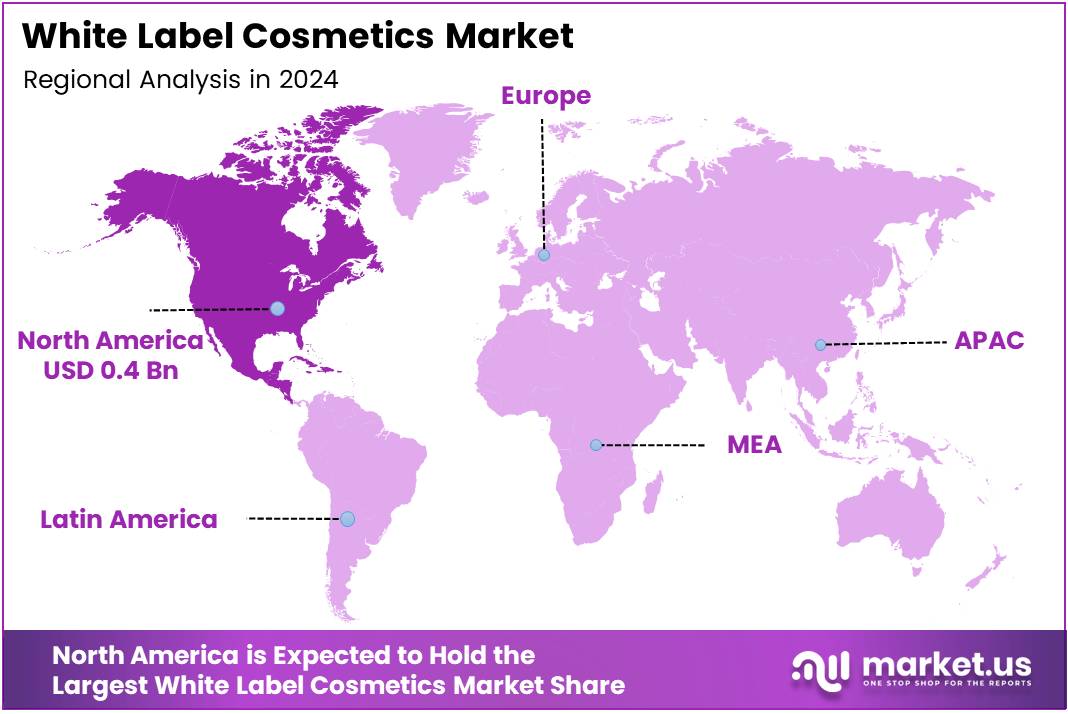

- North America led the market in 2024 with a 36.2% share, valued at approximately USD 0.4 Billion.

The White Label Cosmetics Market refers to beauty products manufactured by one company and rebranded by another for sale. This business model allows brands to offer diverse cosmetics without investing in product development, enabling faster market entry and cost efficiency. It serves as a strategic growth driver in the cosmetics industry.

According to Statistics, US sales of store-brand beauty products surged by 10.5% in 2023, highlighting the increasing consumer acceptance and demand for white label cosmetics. This growth reflects shifting consumer preferences towards affordable and quality alternatives to branded products, presenting lucrative opportunities for new entrants and established players alike.

Moreover, the average profit margin in the white label cosmetics segment ranges between 20% and 30%, as noted by BusinessPlan-Templates. This attractive margin underscores the financial viability for retailers and brands leveraging white label manufacturing to maximize returns while minimizing operational risks and overhead costs.

In Europe, the widespread daily use of cosmetic and personal care products by its 500 million consumers, according to IBEC, emphasizes the immense market potential for white label cosmetics. The region’s consumers prioritize health, well-being, and self-esteem, fueling demand for varied product offerings under private label brands that meet these evolving lifestyle needs.

Furthermore, government investments and regulatory frameworks play a critical role in shaping the white label cosmetics market. Stricter safety and quality regulations ensure consumer protection, encouraging brands to adopt compliant manufacturing practices. This fosters trust and drives the adoption of white label products in regulated markets.

Additionally, the rising inclination toward clean, organic, and sustainable cosmetics opens new growth avenues for white label producers to innovate and cater to niche demands. Companies investing in such trends can differentiate themselves, capitalizing on consumer awareness and eco-conscious purchasing behavior.

Transitioning from traditional to digital retail channels has further accelerated white label cosmetics adoption. E-commerce platforms enable brands to reach wider audiences rapidly, supported by lower production costs and customization flexibility inherent in white label models.

Overall, the white label cosmetics market is positioned for robust expansion, driven by favorable consumer trends, strong profit margins, supportive regulations, and increasing investments in product innovation. Brands leveraging these dynamics can capitalize on growing demand and enhance their competitive edge effectively.

Type Analysis

Organic/Natural leads with an 85.7% share, reflecting strong consumer preference for clean and sustainable beauty products.

In 2024, Organic/Natural held a dominant market position in the By Type Analysis segment of the White Label Cosmetics Market, with a commanding 85.7% share. This significant dominance is driven by increasing awareness among consumers about the benefits of natural ingredients and their lesser environmental impact. Brands are increasingly focusing on formulating products with organic components to meet this growing demand.

Meanwhile, the Conventional/Synthetic segment accounts for the remaining share, capturing a much smaller portion of the market. Despite lower consumer preference, this segment still holds relevance due to its cost-effectiveness and availability in certain product categories. However, regulatory pressures and shifting consumer trends continue to favor organic and natural alternatives.

The emphasis on health-conscious purchasing decisions is fueling innovation within the Organic/Natural segment, encouraging white label manufacturers to develop more plant-based, cruelty-free, and eco-friendly formulations. This trend is expected to sustain the segment’s dominance in the foreseeable future, making it a crucial focus area for market participants aiming to capitalize on evolving consumer values.

Product Analysis

Skincare dominates with a 42.2% share, driven by rising consumer focus on skin health and wellness.

In 2024, Skincare held a dominant market position in the By Product Analysis segment of the White Label Cosmetics Market, with a significant 42.2% share. The rising emphasis on personal wellness and preventative care has led consumers to invest heavily in skincare products, which are seen as essential to daily routines.

Fragrance, Color Cosmetics, and Haircare collectively form the remaining market, but none match the sheer size of the skincare segment. Fragrance products continue to appeal through personalization and luxury appeal, while color cosmetics attract consumers focused on enhancing appearance. Haircare remains a stable segment, with demand driven by both functional and aesthetic needs.

The skincare segment’s leadership is reinforced by innovations such as anti-aging formulations, natural ingredients, and multifunctional products. Brands leveraging these trends through white label partnerships are well positioned to capture this consumer interest. This dominant share highlights skincare as the growth engine of the white label cosmetics space, attracting ongoing investment and development.

End Use Analysis

Women dominate with a 63.5% share, reflecting stronger consumer engagement and spending in cosmetics.

In 2024, Women held a dominant market position in the By End Use Analysis segment of the White Label Cosmetics Market, commanding a robust 63.5% share. This reflects the traditional and ongoing market trend where women represent the largest consumer base for cosmetic products, driven by diverse needs ranging from skincare to makeup.

Men’s segment accounts for a smaller share but shows potential for growth as grooming and personal care awareness increases among male consumers. However, women remain the primary target for white label cosmetics manufacturers, influencing product development and marketing strategies.

The female consumer base’s demand for innovative, natural, and personalized products continues to shape the market landscape. White label providers benefit by tailoring product lines to meet this demographic’s evolving preferences, ensuring continued dominance in this segment.

Distribution Channel Analysis

Direct-to-consumer (DTC) e-commerce leads with a 47.2% share, driven by convenience and personalized shopping experiences.

In 2024, Direct-to-consumer (DTC) e-commerce held a dominant market position in the By Distribution Channel Analysis segment of the White Label Cosmetics Market, with a notable 47.2% share. This channel’s rise is fueled by consumers’ growing preference for convenient, contactless shopping combined with curated brand experiences online.

Retail stores and online marketplaces make up the rest of the market but lag behind in share. While physical stores continue to offer tactile experiences, shifting consumer behavior towards digital-first purchasing is clear. Online marketplaces provide a wide product range but lack the direct brand engagement found in DTC channels.

The DTC model enables brands to gather direct consumer data, customize offerings, and build loyalty, making it a favored distribution strategy. White label cosmetics companies are increasingly partnering with brands that leverage DTC e-commerce to maximize reach and profitability in an evolving retail landscape.

Key Market Segments

By Type

- Organic/Natural

- Conventional/Synthetic

By Product

- Skincare

- Fragrance

- Color Cosmetics

- Haircare

By End Use

- Women

- Men

By Distribution Channel

- Direct-to-consumer (DTC) e-commerce

- Retail stores

- Online marketplaces

- Others

Drivers

Surge in Micro-Influencer Partnerships Boosts Niche Brand Demand

In recent years, the rise of micro-influencers has played a major role in shaping the white label cosmetics market. These influencers often cater to specific niche audiences, creating authentic connections that traditional advertising struggles to achieve. Their partnerships with white label brands have significantly increased demand for niche and personalized cosmetic products.

Additionally, the rapid digitalization of B2B cosmetic ordering platforms has streamlined the purchasing process for retailers and businesses. This shift allows companies to easily access a wide range of white label products online, improving convenience and efficiency in sourcing cosmetics.

Retailers are also expanding their requirements for clean-label products. Consumers increasingly seek cosmetics made with natural and safe ingredients, pushing retailers to demand clean-label options from white label suppliers. This trend helps white label cosmetics gain broader acceptance and appeal.

Furthermore, private labels are making strong inroads into premium cosmetic formats. Once dominated by established brands, premium products under private labels are growing in popularity. This expansion indicates consumer trust and the willingness to explore quality cosmetics offered through white label channels.

Restraints

Difficulty in Establishing Unique Brand Identity with Shared Formulations

One of the main challenges in the white label cosmetics market is the struggle to build a unique brand identity. Many products share similar formulations, making it hard for brands to stand out in a crowded marketplace. This limits differentiation and can affect customer loyalty.

Consumer trust remains limited for unfamiliar private label brands. Shoppers often hesitate to try new or unknown brands, which slows the growth potential of white label cosmetics. Building recognition and trust requires time and strategic marketing efforts.

Innovation capacity is another restraint. White label brands typically rely on pre-developed stock-keeping units (SKUs), reducing opportunities for groundbreaking product development. This reliance may restrict the introduction of novel ingredients or technologies.

Additionally, intellectual property concerns pose risks. Packaging designs and product presentations can be copied or imitated easily, creating legal and competitive challenges for white label brands trying to protect their unique appeal.

Growth Factors

Increasing Demand for Halal and Vegan-Certified Private Label Products

A growing opportunity for the white label cosmetics market lies in the rising demand for halal and vegan-certified products. Consumers worldwide are becoming more conscious of ethical and religious considerations, encouraging brands to offer products that meet these standards. This trend opens new customer segments for white label suppliers.

Subscription-based cosmetic models also offer promising growth. Consumers enjoy the convenience of regular product deliveries tailored to their preferences, and white label brands can capitalize on this trend by providing customizable subscription options.

Men’s grooming and skincare represent an expanding niche. Custom white label solutions designed specifically for men’s needs are gaining traction, driven by increasing male interest in personal care products. This area presents fresh avenues for product innovation and market penetration.

Moreover, white label brands are enhancing their presence in pharmacies and wellness retail chains. These channels provide wide accessibility and foster consumer trust, allowing private labels to reach health-conscious customers effectively.

Emerging Trends

Rise of AI-Enabled Tools for White Label Product Customization

The adoption of AI-enabled tools is revolutionizing white label cosmetics by enabling personalized product customization. Brands can now use artificial intelligence to tailor formulations and packaging to individual consumer preferences, improving satisfaction and loyalty.

Sustainable refillable cosmetic packaging is another growing trend. Environmentally aware consumers prefer products that reduce waste, pushing white label brands to adopt eco-friendly packaging solutions that support refill and reuse models.

Minimalist skincare routines are influencing product development. Consumers seek simple, effective skincare with fewer steps, prompting white label manufacturers to offer streamlined product lines that match this demand.

Lastly, augmented reality (AR) technology is becoming popular for virtual cosmetic try-ons. Private label brands increasingly use AR to allow consumers to test products virtually before purchase, enhancing the buying experience and reducing hesitation.

Regional Analysis

North America Dominates the White Label Cosmetics Market with a Market Share of 36.2%, Valued at USD 0.4 Billion

In 2024, North America led the White Label Cosmetics market, holding a commanding 36.2% share, equivalent to approximately USD 0.4 billion. This dominance is driven by high consumer demand for personalized and premium cosmetic products, supported by advanced digital retail platforms. The region benefits from a mature beauty market and rising private label penetration across various retail channels.

Regional Mentions:

Europe White Label Cosmetics Market Insights

Europe holds a significant position in the White Label Cosmetics market, supported by stringent regulatory frameworks that ensure product quality and safety. The increasing consumer preference for clean and organic cosmetics further fuels growth. The market benefits from well-established distribution networks and innovation in product formulations tailored to diverse consumer needs.

Asia Pacific White Label Cosmetics Market Trends

Asia Pacific presents robust growth prospects due to rising urbanization, increasing disposable income, and growing beauty consciousness among millennials. The expanding e-commerce penetration in countries like China and India enhances accessibility to private label cosmetics. The market is also witnessing increased demand for natural and herbal cosmetic products in this region.

Middle East and Africa White Label Cosmetics Market Overview

The Middle East and Africa region is gradually emerging in the White Label Cosmetics market with rising investments in beauty and personal care sectors. Growing awareness of international beauty trends and expanding retail infrastructure contribute to the market’s expansion. However, market growth remains moderate due to economic disparities and regulatory challenges.

Latin America White Label Cosmetics Market Dynamics

Latin America is witnessing steady growth driven by increasing urban populations and a growing middle class with enhanced spending capacity on personal care. The demand for affordable and effective cosmetic solutions propels the adoption of white label products. Nonetheless, market penetration is hindered by economic volatility and limited technological adoption in some areas.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key White Label Cosmetics Company Insights

In 2024, the global White Label Cosmetics Market features several prominent players driving innovation and growth.

COSMEWAX S.A. stands out with its strong focus on sustainable ingredients and customized wax formulations, catering to niche demands in personal care products. Their emphasis on eco-friendly solutions aligns well with rising consumer preferences for clean beauty.

NF Skin has carved a niche by leveraging advanced skincare technologies, offering private label products that blend science and nature. Their ability to rapidly develop formulations that meet diverse regulatory standards across global markets gives them a competitive edge in white label skincare.

Modern Basic Cosmetics excels by providing a broad portfolio of customizable cosmetic products with an emphasis on trendy, minimalist formulations that appeal to younger demographics. Their agile production capabilities and responsiveness to market trends enable quick adaptation to shifting consumer tastes.

INTERCOS S.P.A leverages its extensive R&D capabilities and global manufacturing network to deliver high-quality, innovative cosmetic solutions under white label contracts. Their strategic partnerships with emerging brands allow for co-creation of premium products, supporting market expansion and differentiation.

These key players collectively contribute to the evolving landscape of the white label cosmetics market by focusing on sustainability, technological innovation, and rapid product development. Their strengths in meeting diverse customer needs and regulatory compliance are central to sustaining growth amid increasing competition and consumer demand for personalized beauty solutions.

Top Key Players in the Market

- COSMEWAX S.A.

- NF Skin

- Modern Basic Cosmetics

- INTERCOS S.P.A

- Audrey Morris Cosmetics International

- Onoxa LLC

- kdc/one

- Lady Burd

- HSA Cosmetics

- CarasaLab

Recent Developments

- In April 2025, beauty-tech start-up Kult successfully raised US$20 million in funding from the M3M Family Office, aiming to accelerate innovation and market expansion. This capital injection is expected to boost Kult’s product development and enhance its presence in the competitive beauty technology sector.

- In May 2024, ACT Beauty strengthened its market position by consolidating its beauty business through the acquisition of Lavay Paris. This strategic move allows ACT Beauty to diversify its portfolio and expand its reach within premium cosmetic segments.

- In May 2024, Honasa Consumer expanded its product offerings by acquiring the cosmetic formulation brand CosmoGenesis. This acquisition supports Honasa’s growth strategy to enhance its R&D capabilities and broaden its skincare innovation pipeline.

- In December 2024, Kosé Corporation completed the acquisition of Thai beauty brand Pañpuri, marking a significant step to deepen its footprint in Southeast Asia. The deal enables Kosé to leverage Pañpuri’s established local presence and eco-conscious product line.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 1.1 Billion |

| Forecast Revenue (2034) | USD 2.4 Billion |

| CAGR (2025-2034) | 7.9% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Organic/Natural, Conventional/Synthetic), By Product (Skincare, Fragrance, Color Cosmetics, Haircare), By End Use (Women, Men), By Distribution Channel (Direct-to-consumer (DTC) e-commerce, Retail stores, Online marketplaces, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | COSMEWAX S.A., NF Skin, Modern Basic Cosmetics, INTERCOS S.P.A, Audrey Morris Cosmetics International, Onoxa LLC, kdc/one, Lady Burd, HSA Cosmetics, CarasaLab |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |