Global Viscosity Reducing Agents Market Size, Share, And Industry Analysis Report By Product (Bactericides, Fungicides), By Type (Organosulfur Compounds, Phenolic Compounds, Chlorinated Compounds), By Formulation Type (Liquid Formulation, Powder Formulation, Emulsion Formulation), By Application (Spray Application, Dip Application, Coating, Impregnation), By End User (Footwear, Garment, Automotive Leather, Furniture Industry), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180247

- Number of Pages: 326

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

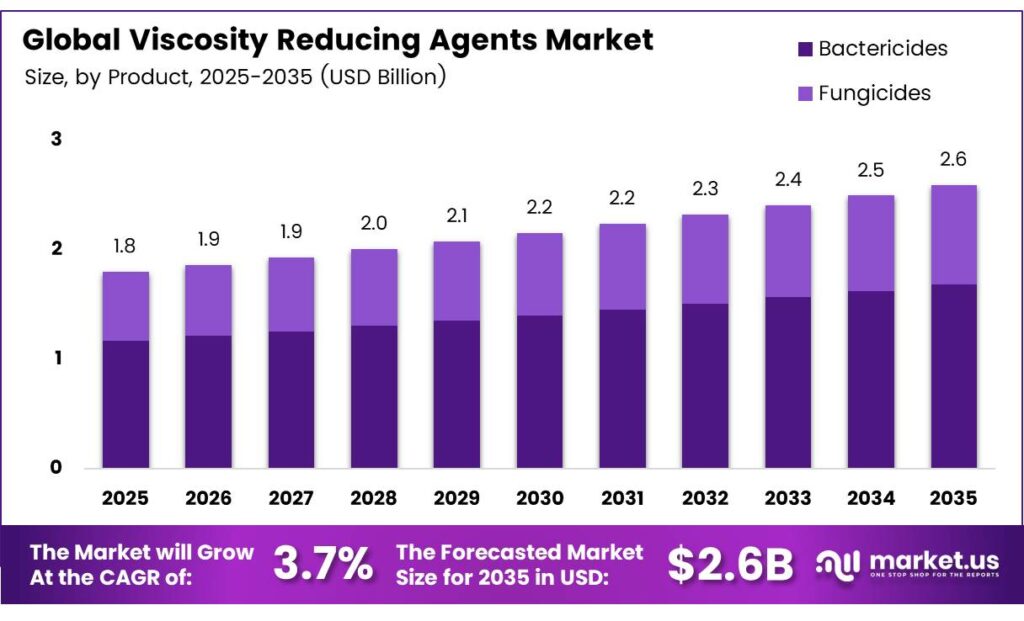

The Global Viscosity Reducing Agents Market size is expected to be worth around USD 2.6 billion by 2035 from USD 1.8 billion in 2025, growing at a CAGR of 3.7% during the forecast period 2026 to 2035.

The viscosity-reducing agents market covers chemical additives that lower the flow resistance of liquids. Industries apply these agents in oil pipelines, paints and coatings, and industrial processes. They improve material transport efficiency and reduce energy consumption during fluid handling operations.

These agents span multiple chemical categories, including organosulfur, phenolic, and polymer-based compounds. Manufacturers formulate them as liquids, powders, and emulsions to suit specific process requirements. Their versatility makes them essential across oil and gas, construction, food processing, and pharmaceutical sectors.

- China imported additives for lubricating oils worth $897,242.82K and 217,701,000 kg in 2024, confirming its position as the top importer by value. This reflects China’s massive industrial scale and its dependence on imported chemical additives to sustain manufacturing output.

- The European Union imported additives for lubricating oils worth $648,364.41K and 153,583,000 kg in 2024, positioning it among the largest importing regions globally. This high import volume underscores Europe’s deep integration with global chemical supply chains and its sustained industrial demand for performance additives.

Growing crude oil production and long-distance pipeline infrastructure drive steady demand for flow assurance solutions. Additionally, the paints and coatings industry requires advanced dispersing agents for consistent product quality. These combined industrial needs position viscosity control as a critical operational requirement globally.

Government investments in pipeline modernization across North America and the Asia-Pacific support market expansion. Regulatory frameworks increasingly favor low-dosage, eco-friendly chemical additives. Consequently, manufacturers accelerate research into bio-based and sustainable viscosity-reducing formulations that meet both performance and compliance standards.

Key Takeaways

- The Global Viscosity Reducing Agents Market is valued at USD 1.8 billion in 2025 and is projected to reach USD 2.6 billion by 2035, at a CAGR of 3.7% during the forecast period 2026 to 2035.

- Bactericides dominate with a 67.1% share in 2025.

- Organosulfur Compounds hold a leading share of 32.6% in 2025.

- Liquid Formulation leads with a 56.3% market share in 2025.

- Spray Application captures the largest share at 44.2% in 2025.

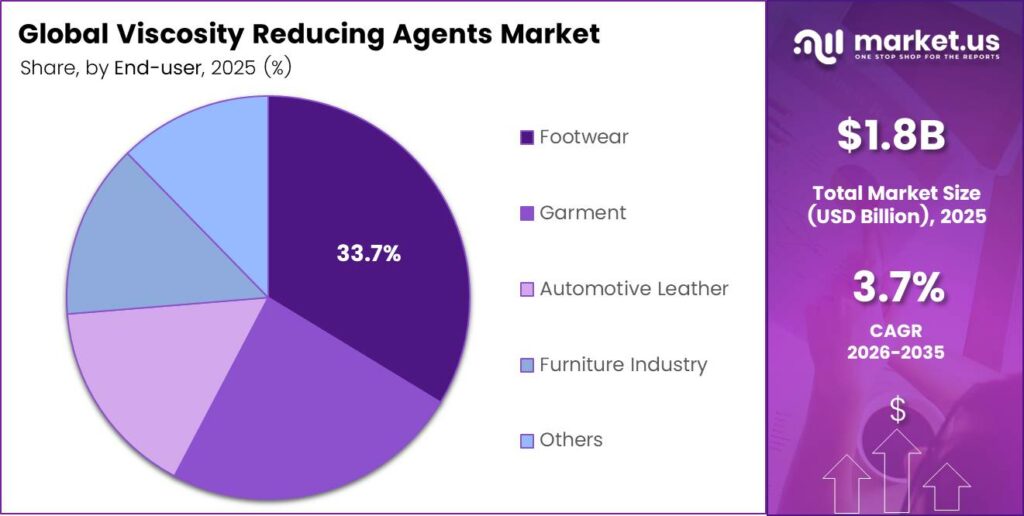

- Footwear leads with a 33.7% share in 2025.

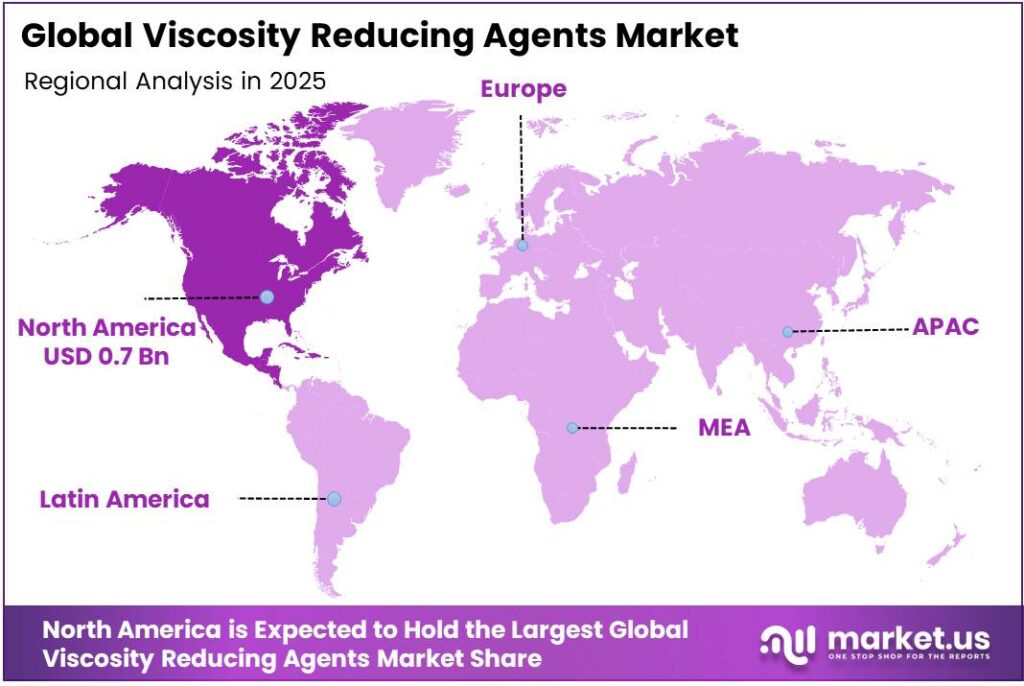

- North America dominates the regional landscape with a 36.9% share, valued at USD 0.7 billion in 2025.

By Product Analysis

Bactericides dominate with 67.1% due to widespread use as primary antimicrobial protection agents in viscosity-reducing formulations.

In 2025, Bactericides held a dominant market position in the By Product segment of the Viscosity Reducing Agents Market, with a 67.1% share. These agents protect industrial fluids and process systems from bacterial contamination. Moreover, their effectiveness at low concentrations makes them a preferred choice across oil, gas, and fluid management applications.

Fungicides represent the secondary product segment, addressing fungal degradation in storage systems and fluid-handling equipment. Formulators increasingly combine fungicides with bactericides to deliver broader-spectrum protection. Consequently, demand for multi-functional protective blends continues to rise across paints, coatings, and specialty chemical markets.

By Type Analysis

Organosulfur Compounds dominate with 32.6% due to their superior thermal stability and compatibility with petroleum-based fluids.

In 2025, Organosulfur Compounds held a dominant market position in the By Type segment of the Viscosity Reducing Agents Market, with a 32.6% share. These compounds deliver reliable performance in high-temperature pipeline environments. Additionally, their compatibility with crude oil streams makes them a favored choice in flow assurance applications globally.

Phenolic Compounds serve as effective antioxidants and viscosity-reducing agents across industrial process fluids. Their chemical stability under varying pressure conditions supports consistent performance. Therefore, formulators continue to develop advanced phenolic blends for specialized petroleum and polymer applications.

Aldehyde Compounds offer targeted reactive properties suited to specific industrial chemical processes. Manufacturers apply them in controlled-environment applications requiring precise reaction management. However, handling requirements limit their widespread adoption compared to organosulfur alternatives.

Quaternary Ammonium Compounds provide dual-function benefits as both viscosity modifiers and antimicrobial agents. Their cationic nature enables effective interaction with process fluid surfaces. Moreover, their versatility supports growing adoption in oilfield and water treatment operations.

Chlorinated Compounds maintain relevance in applications requiring strong chemical activity at lower dosages. Their cost-effectiveness supports use in commodity industrial processes. Nonetheless, increasing environmental scrutiny drives a gradual transition toward greener alternatives across regulated markets.

By Formulation Type Analysis

Liquid Formulation dominates with 56.3% due to ease of mixing, rapid dispersion, and compatibility with automated dosing systems.

In 2025, Liquid Formulation held a dominant market position in the By Formulation Type segment of the Viscosity Reducing Agents Market, with a 56.3% share. Liquid formats integrate seamlessly into continuous industrial processes. Furthermore, they reduce mixing time and handling complexity, making them the most practical choice for large-scale operations.

Powder Formulation supports applications where extended shelf life and concentrated dosing are priorities. Industries handling dry-mix systems and specialized coatings prefer this format. Additionally, powder-based agents offer cost savings in long-distance transportation and bulk storage scenarios.

Emulsion Formulation bridges the performance benefits of both liquid and solid systems. Manufacturers develop emulsions to deliver controlled release and uniform distribution within process fluids. Consequently, demand grows in advanced coating, food processing, and pharmaceutical applications requiring precise viscosity control.

By Application Analysis

Spray Application dominates with 44.2% due to efficient surface coverage and compatibility with large-scale industrial coating operations.

In 2025, Spray Application held a dominant market position in the By Application segment of the Viscosity Reducing Agents Market, with a 44.2% share. Spray systems deliver uniform agent distribution across complex surfaces. Moreover, automation compatibility enhances throughput and reduces material waste in high-volume manufacturing environments.

Dip Application provides thorough surface penetration suited for components requiring complete coverage. Industries such as automotive and furniture manufacturing rely on dip processes for consistent treatment quality. Therefore, demand for viscosity-adjusted formulations optimized for dip tanks remains steady across these sectors.

Coating applications leverage viscosity-reducing agents to achieve target film thickness and surface uniformity. Paints, industrial coatings, and protective layers require precise rheological control. Consequently, formulators develop specialized agents that maintain performance across a range of temperature and humidity conditions.

Impregnation applications require agents that penetrate substrate pores to deliver internal protection and performance enhancement. Wood, textile, and construction materials benefit from impregnation-grade formulations. Additionally, growing infrastructure investment drives steady demand for high-performance impregnation agents globally.

Others encompass niche and emerging application methods that require tailored viscosity management solutions. These include injection, foam, and hybrid treatment systems. As industries explore new processing techniques, demand for customized agent formulations in this segment continues to expand.

By End User Analysis

Footwear dominates with 33.7% due to high-volume production requirements and the critical role of consistent surface treatment in quality assurance.

In 2025, Footwear held a dominant market position in the By End User segment of the Viscosity Reducing Agents Market, with a 33.7% share. Footwear manufacturers depend on precisely controlled chemical formulations for consistent leather and synthetic material treatment. Moreover, global footwear production volumes sustain high and stable demand for viscosity-optimized processing agents.

Garment manufacturers apply viscosity-reducing agents in fabric treatment and finishing processes. Consistent fluid behavior ensures uniform dye penetration and surface coating quality. Consequently, the garment sector maintains a strong demand for liquid and emulsion-based formulations suited to textile processing lines.

Automotive Leather producers require high-performance agents that withstand elevated temperatures and mechanical stress. Seat covers, dashboards, and interior trims demand durable surface treatment solutions. Additionally, rising automotive production in the Asia-Pacific directly supports agent consumption in this end-use segment.

Furniture Industry applications focus on wood finishing and upholstery treatment processes. Manufacturers use viscosity-controlled agents to achieve consistent stain, lacquer, and protective coating results. Therefore, growth in residential and commercial furniture markets continues to generate steady agent demand globally.

Others include specialty industries such as aerospace, medical devices, and electronics manufacturing that utilize viscosity-reducing agents in niche processes. These sectors prioritize purity, regulatory compliance, and performance consistency. As these industries expand, they represent high-value growth opportunities for premium agent formulations.

Key Market Segments

By Product

- Bactericides

- Fungicides

By Type

- Organosulfur Compounds

- Phenolic Compounds

- Aldehyde Compounds

- Quaternary Ammonium Compounds

- Chlorinated Compounds

By Formulation Type

- Liquid Formulation

- Powder Formulation

- Emulsion Formulation

By Application

- Spray Application

- Dip Application

- Coating

- Impregnation

- Others

By End User

- Footwear

- Garment

- Automotive Leather

- Furniture Industry

- Others

Emerging Trends

Polymer-Based Innovations and Sustainability Drive New Direction in Viscosity-Reducing Agent Development

Manufacturers develop advanced polymer-based formulations tailored for extreme temperature and pressure pipeline conditions. These next-generation agents maintain consistent flow performance even in deepwater and arctic environments. Moreover, they extend operational life and reduce maintenance frequency, lowering overall pipeline management costs.

- Unconventional oil resource extraction, including shale and heavy oil production, drives demand for specialized flow assurance technologies. Singapore imported lubricating oil additives worth $721,980.78K and 227,285,000 kg in 2024, reflecting the region’s critical role as a refining and trading hub. This volume signals strong regional demand for high-performance viscosity management solutions.

Sustainability goals push formulators toward eco-friendly and low-dosage agent development. Companies accelerate the adoption of bio-derived ingredients that reduce environmental impact without sacrificing performance. Additionally, construction and cement industries increasingly adopt viscosity-reducing agents to optimize material flow, improving project productivity and reducing raw material waste.

Drivers

Rising Oil and Gas Activity and Industrial Expansion Drive Strong Demand for Viscosity-Reducing Agents

Escalating oil and gas exploration activities boost demand for pipeline transportation efficiency solutions worldwide. Operators require reliable viscosity management to maintain flow rates across long-distance crude pipelines. Consequently, agent adoption accelerates as producers expand upstream and midstream operations in key producing regions.

- The United States imported lubricating oil additives worth $513,680.06K and 121,103,000 kg in 2024, reflecting substantial domestic industrial demand. This import volume demonstrates the scale of additive consumption in North American manufacturing and energy sectors, driving consistent market growth. Lubrizol reported FY2024 sales volumes increasing 4% year-over-year, reflecting higher demand across both additives and advanced materials businesses.

The expanding paints and coatings sector requires advanced dispersing solutions for precise viscosity control. Growing crude oil consumption across Asia-Pacific emerging markets further fuels agent adoption. Additionally, the non-polluting nature of select agent categories enables broad utilization across food processing, pharmaceutical, and consumer goods manufacturing industries.

Restraints

Environmental Regulations and Economic Volatility Restrain Viscosity-Reducing Agents Market Growth

Stringent environmental regulations on synthetic chemical additives limit the deployment of conventional viscosity-reducing agents in regulated markets. Authorities in North America and Europe impose strict compliance requirements on chemical formulations. Consequently, manufacturers face rising reformulation costs and longer product approval timelines before market entry.

- Petroleum additives operating profit of $520.052 million in FY2025, down from $591.854 million in FY2024. This decline reflects the impact of lower shipments, pricing pressures, and one-time charges on industry profitability. Moreover, Innospec Oilfield Services’ operating income declined 40% year-over-year in FY2025, highlighting how demand softness directly impacts chemical additive sector earnings.

Volatility in oil and gas demand due to global economic uncertainties creates unstable procurement cycles for viscosity-reducing agents. Price fluctuations in crude oil affect capital allocation for pipeline operations and maintenance programs. Therefore, market participants maintain cautious inventory strategies, limiting short-term volume growth for agent suppliers.

Growth Factors

Infrastructure Investment and Bio-Based Innovation Create Significant Growth Opportunities for the Market

Heightened investments in pipeline infrastructure projects across developing regions create substantial demand for flow assurance technologies. Governments in the Middle East, South Asia, and Latin America prioritize energy distribution network expansion. Consequently, viscosity-reducing agent suppliers gain access to large-scale, long-term supply contracts in these high-growth markets.

- Lubrizol generated revenue of $6.2 billion in FY2025, demonstrating the scale and economic significance of the lubricant and performance additives industry. Rising research and development initiatives for innovative bio-based viscosity reducers reflect the industry’s commitment to sustainable solutions. BASF invested €4.0 billion in capital expenditure in FY2025, signaling a continued commitment to chemical production capacity and product innovation.

Increasing demand for high-quality crude oil transportation solutions in global trade supports agent adoption in export-oriented pipeline systems. Expansion into food processing and pharmaceutical formulations opens new high-value application markets. Additionally, construction and cement industries adopt viscosity-reducing agents to improve material flow efficiency and reduce operational energy consumption on large infrastructure projects.

Regional Analysis

North America Dominates the Viscosity Reducing Agents Market with a Market Share of 36.9%, Valued at USD 0.7 Billion

North America leads the global viscosity reducing agents market, holding a 36.9% share valued at USD 0.7 billion in 2025. The region benefits from extensive pipeline infrastructure, high crude oil production volumes, and advanced refining capacity. Moreover, strong regulatory frameworks encourage the adoption of performance-grade and environmentally compliant chemical additives across the energy and manufacturing sectors.

Europe represents a mature and innovation-driven market for viscosity reducing agents. The region’s strong chemical manufacturing base and advanced paints, coatings, and automotive industries sustain consistent demand. Additionally, European Union sustainability directives accelerate the shift toward bio-based and low-environmental-impact formulations across industrial applications.

Asia Pacific records the fastest demand growth among all regions, driven by expanding oil refining, construction, and manufacturing activity. China, India, and Southeast Asian economies increase pipeline infrastructure investments to meet growing energy distribution needs. Consequently, the region drives the highest volume consumption of viscosity-reducing agents among all global markets.

The Middle East and Africa region generates significant demand from oil-producing nations investing in pipeline and refinery modernization. Major national oil companies expand upstream and midstream capacity, requiring reliable flow assurance chemical solutions. Furthermore, growing industrial diversification programs support demand for viscosity agents beyond traditional oil and gas applications.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Lanxess AG operates as a global specialty chemicals leader with a strong focus on performance additives and industrial chemical solutions. The company develops viscosity-reducing formulations for oil and gas, rubber, and polymer processing markets. Its vertically integrated manufacturing network enables consistent product quality and supports large-scale customer supply requirements across multiple industries and geographies.

Buckman Laboratories International, Inc. delivers specialty chemical solutions focused on process optimization for industrial and manufacturing customers. The company emphasizes technical service capabilities alongside product supply, helping clients achieve precise viscosity control outcomes. Buckman’s application expertise spans pulp, paper, leather, and water treatment industries, positioning it as a trusted partner in complex fluid management challenges.

Vink Chemicals GmbH & Co. KG specializes in biocides and performance additives for the leather, textile, and coatings industries. The company develops targeted formulations that combine viscosity management with protective functions for treated materials. Moreover, Vink Chemicals focuses on regulatory-compliant product development, addressing growing customer demand for environmentally responsible chemical solutions across European and international markets.

Troy Corporation provides performance additives and preservation solutions designed for paints, coatings, and industrial chemical systems. The company develops viscosity-modifying agents that enhance product stability and application performance. Additionally, Troy’s global technical support network enables customized formulation development, helping manufacturers meet specific rheological and regulatory requirements across diverse end-use sectors worldwide.

Top Key Players in the Market

- Lanxess AG

- Buckman Laboratories International, Inc.

- Vink Chemicals GmbH & Co. KG

- Troy Corporation

- DuPont de Nemours, Inc.

- ICL Performance Products LP

- Akzo Nobel N.V.

- Archroma Management LLC

- Ashland Global Holdings Inc.

- Huntsman International LLC

Recent Developments

- In 2025, Lanxess AG has several ongoing and recently highlighted offerings tied to viscosity reduction in rubber processing and coatings applications. Global Rubber Performance Product Catalog (Rhein Chemie business) details multiple processing promoters and resins that decrease compound viscosity, improve flow/extrusion rates, filler dispersion, and homogeneity in tires and technical rubber goods.

- In 2025, Buckman Laboratories International, Inc. features Busperse, a zero-VOC, biobased (vegetal) nonionic dispersant (dimethylamides of unsaturated fatty acids) for solvent-based coatings (especially polyester and epoxy). It reduces viscosity (makes formulations thinner and easier to apply), prevents pigment agglomeration, enables higher solids content without viscosity buildup, and provides dynamic corrosion inhibition via a protective film.

Report Scope

Report Features Description Market Value (2025) USD 1.8 Billion Forecast Revenue (2035) USD 2.6 Billion CAGR (2026-2035) 3.7% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Bactericides, Fungicides), By Type (Organosulfur Compounds, Phenolic Compounds, Aldehyde Compounds, Quaternary Ammonium Compounds, Chlorinated Compounds), By Formulation Type (Liquid Formulation, Powder Formulation, Emulsion Formulation), By Application (Spray Application, Dip Application, Coating, Impregnation, Others), By End User (Footwear, Garment, Automotive Leather, Furniture Industry, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Lanxess AG, Buckman Laboratories International Inc., Vink Chemicals GmbH & Co. KG, Troy Corporation, DuPont de Nemours Inc., ICL Performance Products LP, Akzo Nobel N.V., Archroma Management LLC, Ashland Global Holdings Inc., Huntsman International LLC Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Viscosity Reducing Agents MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Viscosity Reducing Agents MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Lanxess AG

- Buckman Laboratories International, Inc.

- Vink Chemicals GmbH & Co. KG

- Troy Corporation

- DuPont de Nemours, Inc.

- ICL Performance Products LP

- Akzo Nobel N.V.

- Archroma Management LLC

- Ashland Global Holdings Inc.

- Huntsman International LLC

Our Clients

- 180247

- March 2026