Quick Navigation

Report Overview

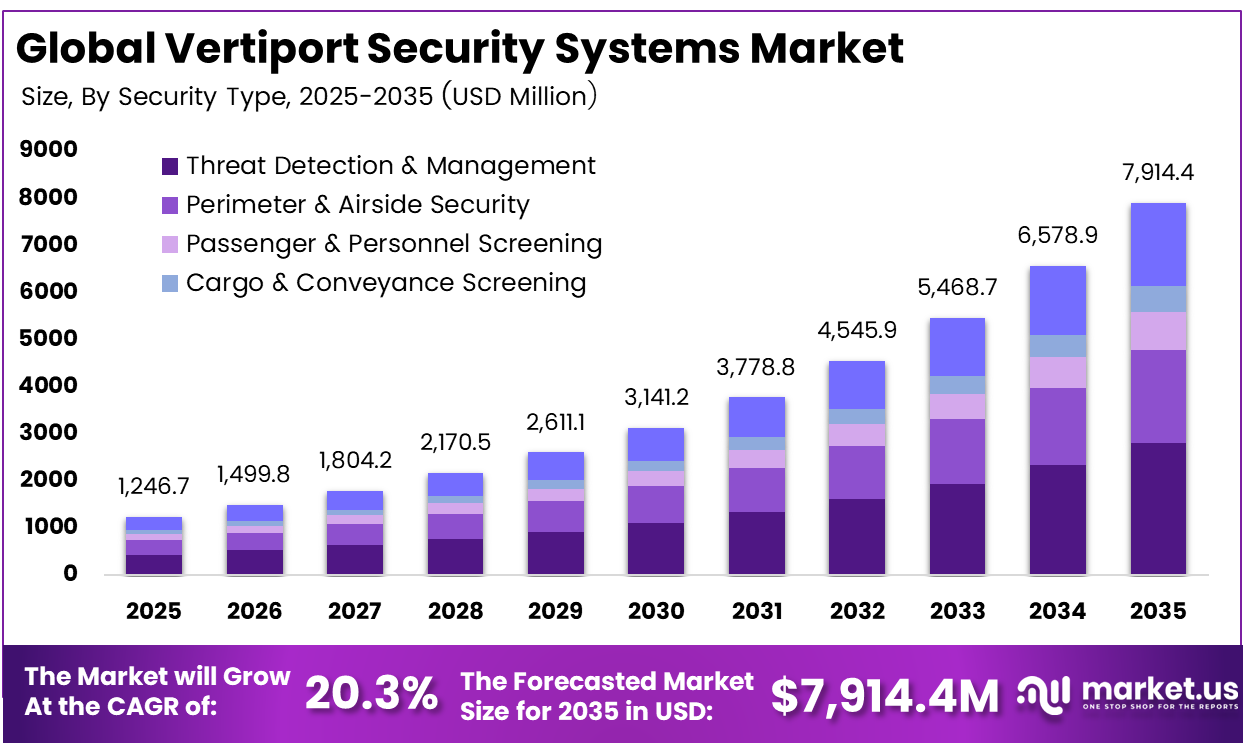

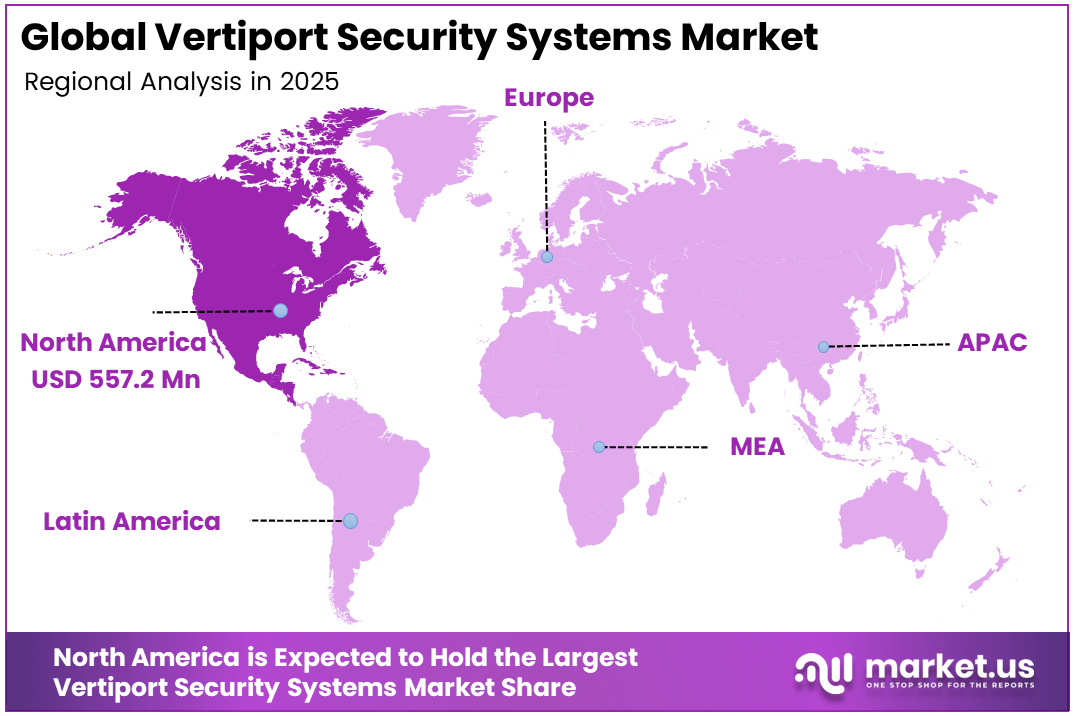

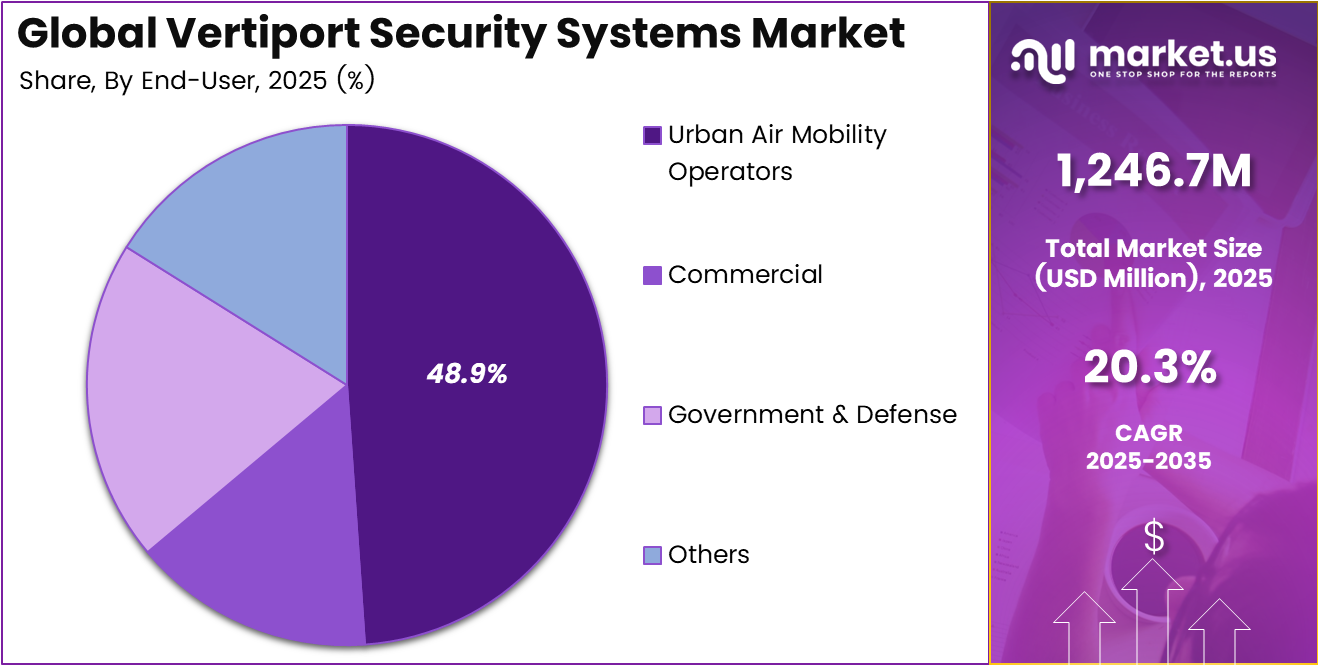

The Global Vertiport Security Systems Market size is expected to be worth around USD 7,914.4 million by 2035, from USD 1,246.7 million in 2025, growing at a CAGR of 20.3% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 44.7% share, holding USD 557.2 million in revenue.

Vertiport Security Systems refers to the technologies and procedures used to protect vertiport facilities, passengers, aircraft, staff, and digital operations. These systems include access control, surveillance, passenger screening, threat detection, and cybersecurity tools. They help ensure safe, smooth, and reliable operations for urban air mobility and electric air taxi services.

Top driving factors include stricter aviation security rules and rising urban air mobility trials, which are pushing vertiports to build stronger security layers. Access control, passenger screening, and safe movement inside small aviation hubs are becoming more important. Growing city congestion and demand for fast air taxis also increase the need for secure operations that can handle more flights per hour.

The market for Vertiport Security Systems is driven by the expansion of urban air mobility networks and growing preparation for electric air taxi services. As vertiports are planned in busy city areas, operators need strong access control, passenger screening, surveillance, and cybersecurity systems. These solutions help protect passengers, aircraft, and staff while supporting safe and smooth short-distance air travel.

Demand analysis is strongest in dense urban corridors, where vertiport locations are linked with high population zones, higher income clusters and heavy commuting routes. Studies show that such catchment zones can capture more than 60% of modeled trips. Passenger interest also improves when visible security checks are smooth and total processing time remains under 10–15 minutes from door to aircraft.

For instance, in April 2024, Axis Communications deepened its presence in aviation and future vertiport infrastructure through a partnership with GSMA to promote IP‑video and analytics‑ready cameras for critical transport hubs, giving operators smarter perimeter monitoring and crowd‑flow insights that will directly translate to upcoming vertiport deployment projects.

Key Takeaway

- In 2025, the Threat Detection & Management segment held a dominant market position, capturing a 35.6% share of the Global Vertiport Security Systems Market.

- In 2025, the Passenger Vertiports segment held a dominant market position, capturing a 76.5% share of the Global Vertiport Security Systems Market.

- In 2025, the Urban Air Mobility Operators segment held a dominant market position, capturing a 48.9% share of the Global Vertiport Security Systems Market.

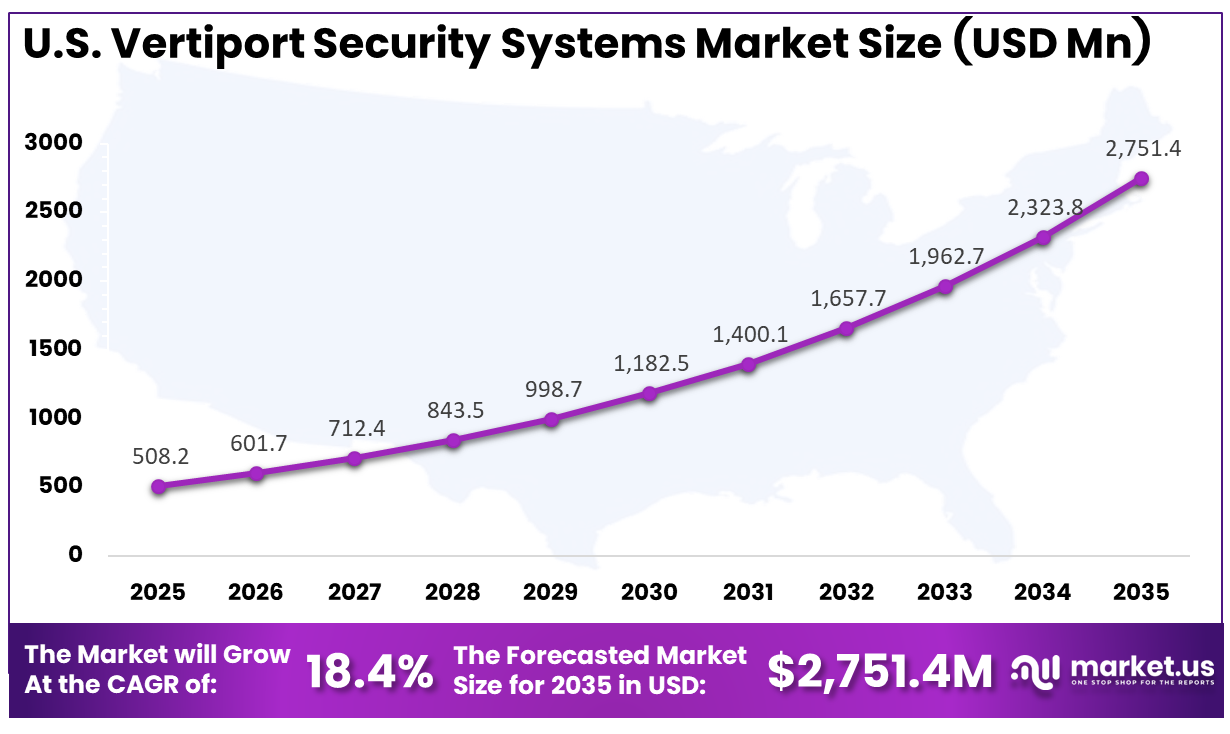

- The U.S. Vertiport Security Systems Market was valued at USD 508.2 Million in 2025, with a robust CAGR of 18.4%.

- In 2025, North America held a dominant market position in the Global Vertiport Security Systems Market, capturing more than a 44.7% share.

Role of Generative AI

Generative AI is becoming an important layer in vertiport security as operators move beyond fixed, rule-based checks. It can study passenger flow, access activity, and video patterns in real time, helping security teams detect unusual behavior faster and respond before small risks affect operations.

In airport security and border control, roughly 70% of operators are already testing or using AI-driven video analytics. This adoption is now influencing early vertiport designs, as planners aim to build smarter, more flexible security systems instead of repeating older aviation security gaps.

Investment and Business Benefits

Investment opportunities are increasing in passenger screening, perimeter detection and secure data platforms connected with flight and scheduling systems. These areas are gaining attention as vertiports move closer to real operations. Investors can benefit from solutions that meet aviation-grade rules and can be easily fitted into existing heliports, rooftops, or mixed mobility hubs.

Business benefits are seen in faster passenger movement, fewer manual checks, and better staff productivity. Well-designed systems can keep average processing time below 10 minutes per passenger during peak periods. Central analytics also help operators identify repeat incident patterns within 30 days, allowing layouts and procedures to be improved before small issues become larger operational risks.

Regional Analysis

In 2025, North America held a dominant market position in the Global Vertiport Security Systems Market, capturing more than a 44.7% share, holding USD 557.2 million in revenue. This dominance is due to strong progress in advanced air mobility, early vertiport planning, and active electric air taxi trials. The region benefits from mature aviation infrastructure, clear safety oversight, and high investment in urban mobility networks. Rising focus on passenger screening, access control, surveillance, and cyber protection is further supporting secure vertiport development across major cities.

For instance, in November 2025, Genetec, headquartered in Montreal, underlined North America’s lead in vertiport security systems by promoting unified physical security platforms that fuse video surveillance, access control, ALPR, and analytics across on‑premises, cloud, and hybrid deployments. Its roadmap around flexible cloud adoption, responsible AI, and highly integrated command centers is directly aligned with securing next‑generation vertiports.

U.S. Vertiport Security Systems Market Size

The market for Vertiport Security Systems within the U.S. is growing tremendously and is currently valued at USD 508.2 million; the market has a projected CAGR of 18.4%. The market is growing due to rising investment in advanced air mobility, stronger aviation safety planning, and increasing trials of electric air taxi services. Cities are preparing vertiport sites near airports, business districts and transit hubs, which creates demand for access control, passenger screening, surveillance and cybersecurity systems. Supportive regulatory work and private sector participation are also encouraging secure infrastructure development.

For instance, in February 2025, Honeywell expanded its role in advanced air mobility by showcasing integrated vertiport technologies that combine airfield lighting, navigation aids, secure access control, and cyber‑resilient command‑and‑control for eVTOL hubs in North America. These solutions are designed to plug into airport‑grade safety architectures, reinforcing U.S. leadership in vertiport security infrastructure for urban air mobility.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Security Type Analysis

In 2025, the Threat Detection & Management segment held a dominant market position, capturing a 35.6% share of the Global Vertiport Security Systems Market. This dominance is due to the rising need for strong threat detection and quick response across vertiport sites. These facilities must protect passengers, aircraft, staff and digital systems while operating in compact urban locations where security gaps can affect both safety and service continuity.

Threat detection and management systems help operators monitor access points, landing areas, passenger zones and control rooms in a coordinated way. Their adoption is supported by the need to identify suspicious activity early, reduce manual checks and maintain secure movement within fast-paced vertiport operations.

For instance, in April 2025, Honeywell International Inc. introduced new AI-enabled features in its Pro Watch Integrated Security Suite at ISC West, aimed at detecting threats sooner by linking access control, video, and intrusion in a single platform. These kinds of unified, analytics-driven tools are directly relevant for vertiports that need faster situational awareness with limited staff.

Application Analysis

In 2025, the Passenger Vertiports segment held a dominant market position, capturing a 76.5% share of the Global Vertiport Security Systems Market. This dominance is due to the central role of passenger vertiports in future urban air mobility services. These sites are expected to manage frequent passenger movement, identity checks, baggage screening and controlled boarding while keeping travel convenient and safe for daily users.

Passenger vertiports require security systems that are visible, reliable, and easy to operate. As these sites may be located near offices, transit hubs or rooftops, operators need smooth screening, access control and surveillance solutions that protect travelers without creating long delays.

For instance, in April 2024, Johnson Controls launched Security Operations Centers and lifecycle management services that support complex sites such as airports and stadiums with centralized monitoring. This approach aligns with passenger vertiports that need continuous oversight of multiple touchpoints, from check-in to boarding zones, often across several locations.

End-User Analysis

In 2025, the Urban Air Mobility Operators segment held a dominant market position, capturing a 48.9% share of the Global Vertiport Security Systems Market. This dominance is due to the active role of urban air mobility operators in managing vertiport security and daily operations. These operators must ensure safe passenger handling, aircraft turnaround, staff access, and coordination with airspace and ground transport systems.

Urban air mobility operators are likely to invest in integrated security platforms because they need consistent control across multiple vertiport sites. Their focus is on reducing operational risk, improving passenger trust, and supporting secure services as urban air taxi networks move toward commercial deployment.

For instance, in April 2025, Bosch’s collaboration with emerging aviation players on green air mobility platforms included testing advanced sensors and control systems for future aircraft operations. These developments help urban air mobility operators plan how aircraft, vertiports, and security systems can share data to maintain safe, efficient networks.

Key Market Segments

By Security Type

- Perimeter & Airside Security

- Passenger & Personnel Screening

- Cargo & Conveyance Screening

- Threat Detection & Management

- Others

By Application

- Passenger Vertiports

- Cargo Vertiports

- Emergency Services

- Others

By End-User

- Urban Air Mobility Operators

- Commercial

- Government & Defense

- Others

Emerging Trends

Emerging trends in vertiport security are being shaped by smaller, distributed sites located within busy cities. Unlike traditional airports, these facilities must balance strong security with fast passenger movement. Around 65% of potential vertiport users say visible and reliable checks will strongly influence their willingness to use urban air taxis.

Another major trend is the merging of cybersecurity, physical security, and airspace monitoring inside one control center. Early concept studies show that more than 50% of future vertiport security incidents may include a digital element, such as data breaches, spoofed communication, or interference with booking and navigation systems.

Growth Factors

Growth in vertiport security systems is strongly linked to the rising number of urban air mobility trials and pilot routes in major cities. Across advanced air mobility, regulators and industry bodies are tracking several hundred test flights each month worldwide, and each route increases the need for stronger security planning.

Another growth factor is the development of multimodal hubs, where vertiports are placed near airports, rail stations, or urban transit points. In such hubs, integrated security platforms already account for more than 30% of new security technology spending, creating a strong base for vertiport security adoption.

Market Dynamics

Drivers - Expansion of Urban Air Mobility Networks

The market is driven by the expansion of urban air mobility networks, as cities prepare for electric air taxi routes and compact aviation hubs. Vertiports will need secure passenger entry, controlled boarding zones, surveillance, and safe aircraft access to support smooth operations in busy urban areas.

As more pilot routes and planned vertiport sites are developed, security systems are becoming part of early infrastructure planning. Operators need solutions that can protect passengers, staff, aircraft, and digital systems while keeping travel fast and convenient for short-distance urban flights.

For instance, in April 2026, Raytheon completed a first flight test of its RAIVEN sensing system on a helicopter, demonstrating wide‑area situational awareness in complex terrain. Similar multi‑sensor technology could help secure airspace around busy vertiports as flight frequencies and approach paths increase in dense urban networks.

Restraint - High Setup Complexity

High setup complexity remains a major restraint because vertiports must fit advanced security systems into limited urban spaces. Rooftops, transit hubs, and mixed-use buildings may not have enough room for traditional airport-style screening, access control, emergency movement and passenger waiting areas.

This complexity can increase planning time and installation challenges for operators. Security systems must also connect with building management, flight scheduling, passenger identity tools and local safety requirements, making deployment more difficult for smaller operators and early-stage vertiport projects.

For instance, in June 2026, Honeywell’s participation in OT cybersecurity events highlights the effort needed to harden industrial and transport environments using automated security tools. A vertiport that combines building systems, flight infrastructure, and passenger IT would face similar complexity when aligning cybersecurity and physical security architectures.

Opportunities - Integrated Smart Security

Integrated smart security offers a strong opportunity as vertiports require connected systems for screening, surveillance, access control and incident response. A single control platform can help operators monitor passengers, staff, aircraft zones, and restricted areas more efficiently than separate security tools.

These systems can also support faster decision-making through real-time alerts and shared operational data. As vertiports become part of wider mobility networks, demand is expected to rise for flexible security platforms that can work across airports, rail stations, rooftops and urban transit hubs.

For instance, in January 2025, Teledyne FLIR’s Nexus platform connects thermal cameras, radars, and analytics into an end‑to‑end detection and tracking ecosystem. For vertiports, integrating this ecosystem with command software and flight operations creates an opportunity to deliver continuous smart surveillance in all weather conditions.

Challenges - Regulatory Uncertainty

Regulatory uncertainty is a key challenge because vertiport security rules are still developing across aviation and urban infrastructure authorities. Operators may find it difficult to choose long-term systems when final requirements for passenger screening, access control, cybersecurity, and emergency response are not fully standardized.

This uncertainty can slow investment and delay project execution. Security vendors and operators must design systems that are flexible enough to meet future rules while still being practical for daily use in dense urban locations, where space, safety, and passenger convenience must be balanced carefully.

For instance, in January 2025, Thales experts discussed how AI, quantum advances, and expanding attack surfaces are reshaping security expectations and regulations. For vertiports, evolving guidance on data use, AI analytics, and critical‑infrastructure protection can create uncertainty around which security architectures will remain compliant over time.

Key Players Analysis

One of the leading players in June 2024, Johnson Controls expanded its access‑control and building‑security offerings with more tightly integrated video, intrusion, and environmental systems, marketed to transportation and smart‑city projects. Such converged platforms are attractive for vertiport developers who want one backbone for safety, security, and building automation at high‑traffic sites.

Top Key Players in the Market

- Thales Group

- Honeywell International Inc.

- Raytheon Technologies Corporation

- Siemens AG

- Bosch Security Systems

- FLIR Systems (Teledyne FLIR)

- Johnson Controls International plc

- Leonardo S.p.A.

- Securitas AB

- Genetec Inc.

- Axis Communications AB

- ASSA ABLOY AB

- Dahua Technology Co., Ltd.

- Hikvision Digital Technology Co., Ltd.

- IDEMIA

- Others

Recent Developments

- In August 2025, IDEMIA strengthened its role in next‑generation vertiport and airport security by expanding biometric identity and access‑control deployments at major North American hubs, using facial recognition and multi‑modal biometrics to secure passenger flows and airside access, setting a benchmark for future vertiport security architectures.

- In January 2024, Teledyne FLIR updated its thermal imaging and multispectral surveillance range for perimeter and critical‑infrastructure applications, giving operators better detection of small aerial and ground threats in low‑visibility conditions. These upgrades are directly applicable to open‑air vertiport pads that require continuous, all‑weather situational awareness.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1,246.7 Million |

| Forecast Revenue (2035) | USD 7,914.4 Million |

| CAGR (2026-2035) | 20.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Security Type (Perimeter & Airside Security, Passenger & Personnel Screening, Cargo & Conveyance Screening, Threat Detection & Management, Others), By Application (Passenger Vertiports, Cargo Vertiports, Emergency Services, Others), By End-User (Commercial, Government & Defense, Urban Air Mobility Operators, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Thales Group, Honeywell International Inc., Raytheon Technologies Corporation, Siemens AG, Bosch Security Systems, FLIR Systems (Teledyne FLIR), Johnson Controls International plc, Leonardo S.p.A., Securitas AB, Genetec Inc., Axis Communications AB, ASSA ABLOY AB, Dahua Technology Co., Ltd., Hikvision Digital Technology Co., Ltd., IDEMIA, Others |

| Customization Scope | Customization at the segment and region/country levels will be provided. Moreover, customization can be tailored to the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |