Quick Navigation

Report Overview

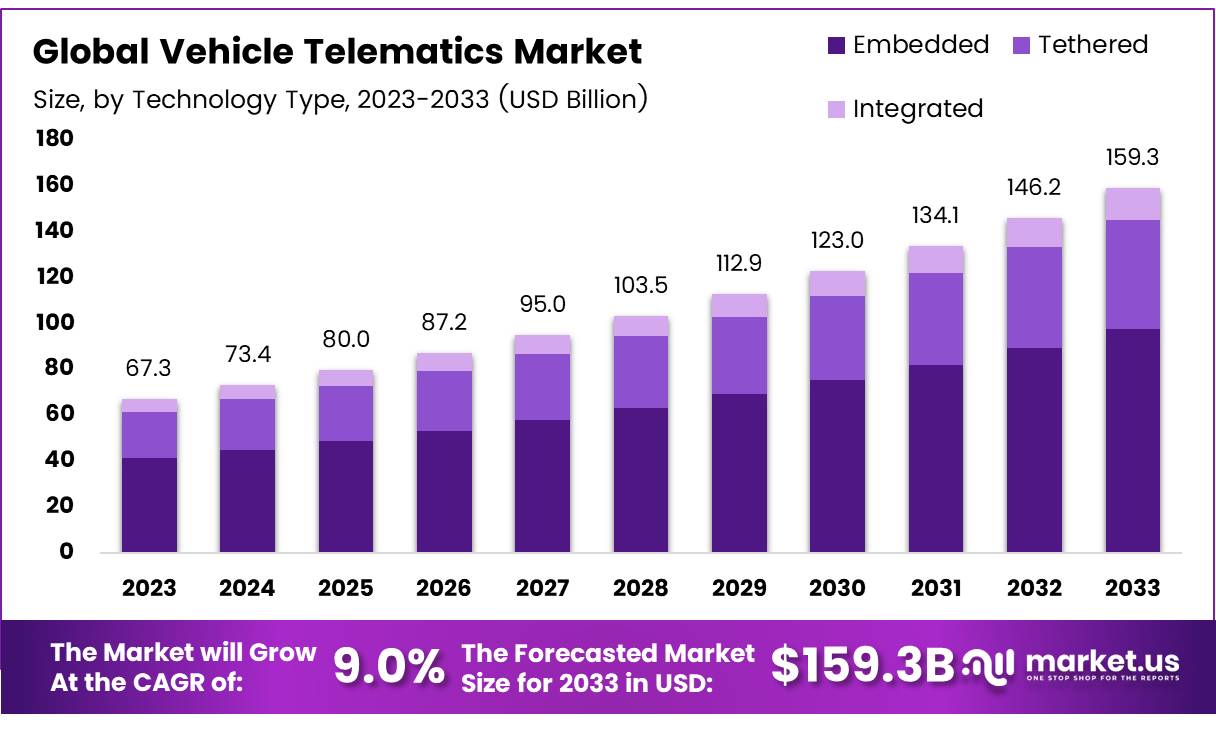

The Global Vehicle Telematics Market size is expected to be worth around USD 159.3 Billion by 2033, from USD 80.1 Billion in 2023, growing at a CAGR of 9% during the forecast period from 2024 to 2033.

Vehicle telematics involves the integration of telecommunications and informatics systems within vehicles, enabling real-time data transmission and monitoring. This technology encompasses GPS navigation, vehicle tracking, and can include mobile internet connectivity within a single platform.

The vehicle telematics market refers to the collective ecosystem of manufacturers, software developers, telecommunications companies, and service providers involved in the production and distribution of telematics solutions. This market has experienced significant expansion due to advancements in wireless technology and increasing vehicle automation.

From an analyst’s perspective, vehicle telematics is poised for substantial growth due to its integral role in enhancing vehicle safety, efficiency, and connectivity. The technology not only aids in navigation but also facilitates crucial diagnostics and predictive maintenance capabilities that can dramatically reduce operating costs.

As connectivity becomes an expected standard feature in vehicles, the demand for integrated telematics systems is projected to rise, driving further innovation and competition within this sector.

The vehicle telematics market is currently undergoing a transformative phase with numerous growth opportunities. Government investments in smart infrastructure and stringent regulations on vehicle safety and emissions are propelling the adoption of telematics solutions. These governmental frameworks are critical in shaping market dynamics, as they encourage the development of technologies that adhere to new standards of environmental and public safety.

The market’s expansion is supported by compelling data. According to Recent Statistics, the number of embedded car OEM telematics units globally is expected to rise from 130 million in 2020 to approximately 375 million by 2026, signifying a robust growth trajectory.

Furthermore, studies cited by Axaxl highlight the significant impact of video telematics on reducing both fatal crashes by 20% and injury crashes by 35%, showcasing the technology’s potential in enhancing road safety.

Additionally, Berg Insight reports that the global installed base of active off-highway vehicle telematics systems reached 8.8 million units in 2023, indicating strong adoption rates in specialized vehicle sectors.

Lastly, according to Trackobit, telematics systems have enabled predictive maintenance that reduced unplanned downtime by 30% and cut repair costs by 20%, further evidencing the operational benefits of this technology.

Key Takeaways

- The Global Vehicle Telematics Market is projected to reach USD 159.3 billion by 2033, growing at a CAGR of 9.0% from 2023.

- Embedded technology held a dominant 67.3% market share in 2023, favored for its reliability and advanced safety features.

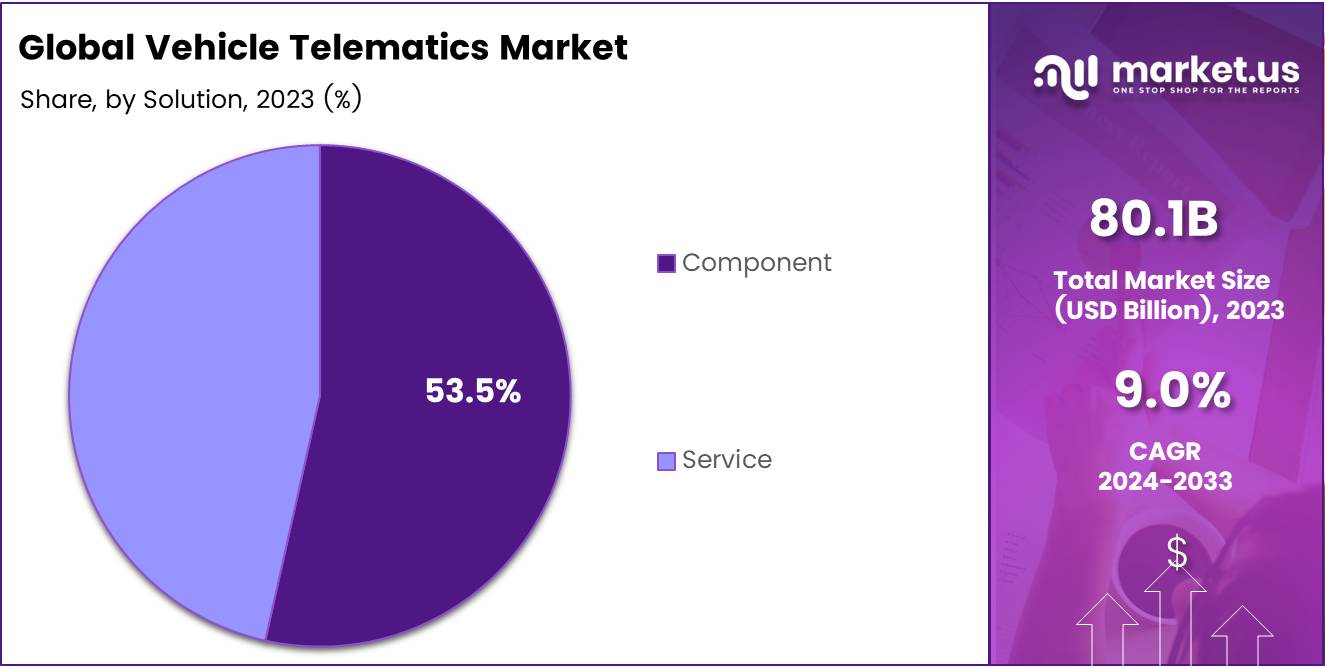

- The Component segment commanded a 53.5% share in the Solutions category of the market in 2023.

- Passenger vehicles led the Vehicle Type segment with a 75.3% share in 2023, driven by consumer demand for advanced safety and diagnostics.

- Insurance Telematics dominated the Application segment due to its role in risk assessment and cost reduction for insurers.

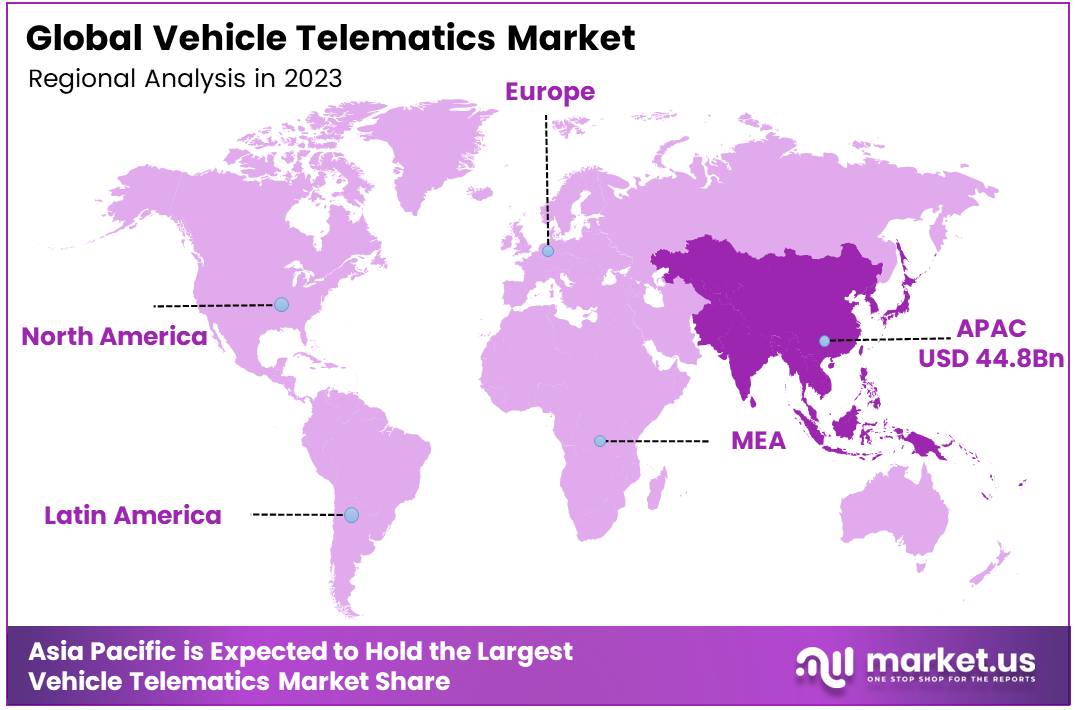

- Asia Pacific led the market with a 56.9% share, valued at USD 44.8 billion, with China, Japan, and South Korea pioneering in telematics adoption.

Technology Type Analysis

Embedded Systems Lead the Vehicle Telematics Market with a 67.3% Share in 2023

In 2023, Embedded held a dominant market position in the By Technology Type Analysis segment of the Vehicle Telematics Market, with a 67.3% share. This substantial market presence can be attributed to the robust integration of embedded systems within vehicles that offer enhanced safety features and real-time data monitoring.

Following Embedded, the Tethered systems accounted for a smaller, yet significant, portion of the market. These systems, which connect the vehicle to the driver’s smartphone, provide a cost-effective solution for consumers seeking connectivity without the full integration of an embedded system.

Lastly, Integrated technologies have started to gain traction, leveraging built-in hardware and software to offer a streamlined and user-friendly interface. These systems are increasingly preferred for their ability to integrate with other digital ecosystems, providing a more connected and interactive driving experience.

Each technology type plays a crucial role in shaping the vehicle telematics landscape, catering to diverse consumer needs and preferences within the automotive sector.

Solution Analysis

Components lead with a 53.5% market share due to increased investment in technological enhancements

In 2023, the Component held a dominant market position in the By Solution Analysis segment of the Vehicle Telematics Market, with a 53.5% share.

This segment comprises various hardware and software components essential for the functionality of vehicle telematics systems, highlighting the pivotal role these components play in the broader telematics ecosystem. The substantial market share underscores the critical dependence on advanced components that enhance vehicle connectivity and data analytics capabilities.

Conversely, the Service aspect of the By Solution Analysis segment, although vital, commanded a smaller portion of the market. This area includes various support services such as installation, maintenance, and software updates, which are crucial for the optimal operation of telematics systems.

However, it represented a less significant share, indicating a stronger market inclination towards component investments over service enhancements in 2023.

The findings suggest a strategic emphasis on technological enhancements in components over service-based solutions within the vehicle telematics sector, pointing to potential growth areas for service-oriented offerings in the coming years.

Vehicle Type Analysis

Passenger Vehicles Lead the Vehicle Telematics Market with a 75.3% Share in 2023

In 2023, the By Vehicle Type Analysis segment of the Vehicle Telematics Market was predominantly led by Passenger vehicles, holding a 75.3% share. This substantial market share is indicative of the heightened adoption of telematics systems within personal vehicles, driven by consumer demand for enhanced safety features, real-time vehicle tracking, and advanced diagnostics.

The integration of telematics in passenger vehicles not only elevates the driving experience but also contributes to more efficient vehicle management and maintenance, thus favoring market expansion.

On the other hand, Commercial vehicles accounted for the remaining market share. While this segment commands a smaller proportion of the market, it is characterized by a growing recognition of the benefits telematics offer in fleet management and logistics.

Commercial vehicle telematics is instrumental in optimizing route planning, reducing fuel consumption, and improving the overall operational efficiency of fleets. The segment is poised for growth, fueled by stringent regulatory standards for commercial vehicle operations and increasing emphasis on reducing operational costs.

Overall, the disparity in market share between Passenger and Commercial vehicles highlights diverse technological adoption rates and differing market dynamics within the Vehicle Telematics sector.

Application Type Analysis

In-Depth Analysis of Insurance Telematics Dominance in the Vehicle Telematics Market

In 2023, Insurance Telematics held a dominant market position in the By Application Type Analysis segment of the Vehicle Telematics Market. This segment outperformed others, primarily due to the increasing adoption of telematics for risk assessment and cost reduction by insurance companies.

Insurance telematics harnesses driving data to tailor insurance premiums, enhancing profitability and customer satisfaction. This approach not only mitigates risk but also incentivizes safer driving behaviors, contributing to its widespread acceptance.

Comparatively, other segments like Information & Navigation, Safety & Security, and Fleet Management, though integral, registered slower growth. The Information & Navigation segment advanced moderately, supported by enhancements in GPS technology and real-time traffic data, which are vital for route optimization. Safety & Security saw incremental growth, driven by escalating demand for emergency support and vehicle recovery services.

Meanwhile, Fleet Management continued to evolve, influenced by the need for operational efficiencies and reduced fleet expenses. The segment labeled Others encompasses additional applications such as remote control features, which are gradually gaining traction due to enhanced connectivity solutions.

Each of these segments demonstrates unique growth dynamics, underscoring the diverse applications and potential of telematics within the automotive sector.

Key Market Segments

By Technology Type

- Embedded

- Tethered

- Integrated

By Solution

- Component

- Service

By Vehicle Type

- Passenger

- Commercial

By Application Type

- Insurance Telematics

- Information & Navigation

- Safety & Security

- Fleet Management

- Others

By Sales Channel

- OEM

- Aftermarket

Drivers

Rising Adoption of Connected Vehicles

The vehicle telematics market is primarily driven by the increasing adoption of connected vehicles, which are equipped with advanced connectivity features to enhance user experience and vehicle efficiency.

Government regulations and safety standards also significantly contribute to this growth, as they mandate the installation of telematics systems in vehicles to ensure safety and compliance with policies such as the eCall system in the European Union.

Furthermore, the optimization of fleet management is a critical factor, as businesses leverage telematics technology to monitor and manage fleet performance, fuel efficiency, and driver behavior more effectively.

Additionally, there is a rising consumer demand for enhanced safety features, including real-time tracking, crash alerts, and advanced driver assistance systems, which are integral components of modern telematics solutions. These drivers collectively accelerate the integration and expansion of telematics across the automotive industry, promising improved vehicle safety, maintenance, and compliance with regulatory standards.

Restraints

Cost Concerns and Privacy Issues Slow Telematics Adoption

The vehicle telematics market faces significant restraints that could hinder its widespread adoption. Primarily, the high initial installation costs stand as a substantial barrier, particularly for businesses operating large fleets. The expense associated with equipping numerous vehicles with advanced telematics systems can be prohibitive, discouraging investment in this technology.

Furthermore, there are serious concerns surrounding data privacy. Telematics systems collect and share sensitive information pertaining to driver behavior and vehicle performance. This raises privacy issues, as both consumers and businesses may be wary of how this data is handled and who has access to it.

The apprehension about the potential misuse or unauthorized access to personal and operational data can lead to resistance against adopting telematics technology, thus impacting the growth prospects of this market. These factors collectively contribute to a cautious approach towards the telematics systems despite their benefits in fleet management and operational efficiency.

Growth Factors

Electric Vehicles Spark New Opportunities in Vehicle Telematics

The vehicle telematics market is poised for significant growth, primarily driven by its integration with the burgeoning electric vehicle (EV) sector.

As the adoption of EVs accelerates, the demand for advanced telematics to monitor battery health, vehicle range, and charging patterns increases, offering substantial opportunities for development and expansion. This integration not only enhances vehicle efficiency and user experience but also opens new avenues for data analytics and energy management solutions.

Additionally, the application of artificial intelligence (AI) and machine learning (ML) can further refine these systems, facilitating predictive maintenance and improving route optimization.

Collaborative efforts with telecom providers could also play a pivotal role in broadening the reach and efficacy of connected vehicle technologies, particularly through the enhancement of vehicle-to-everything (V2X) communication.

This technology is crucial for improving traffic management, vehicle safety, and the overall infrastructure, making it an essential component of smart city initiatives globally. Collectively, these factors depict a robust landscape for the vehicle telematics market, characterized by innovative integration and strategic partnerships.

Emerging Trends

Real-Time Data Analytics Enhances Decision-Making in Vehicle Telematics

The vehicle telematics market is increasingly influenced by the integration of real-time data analytics, which empowers both businesses and consumers to make informed decisions swiftly, based on immediate data insights. This trend is complemented by the growing adoption of cloud computing solutions, which enhance the scalability and accessibility of telematics systems.

Furthermore, vehicles are now more frequently equipped with voice assistants, leveraging telematics for enhanced navigation, hands-free communication, and entertainment functionalities, thereby improving user experience and operational efficiency.

Additionally, there is a notable shift towards monitoring driver behavior through telematics, which tracks parameters such as speed, braking habits, and fuel usage. This not only helps in promoting safer driving practices but also aids in the better management of fleet operations.

These trends collectively signify a dynamic evolution in the vehicle telematics sector, driven by technological advancements and a heightened focus on data-driven management and user-centric enhancements.

Regional Analysis

Asia Pacific Leads Global Vehicle Telematics Market with 56.9% Share Valued at USD 44.8 Billion

The vehicle telematics market exhibits significant regional variations across North America, Europe, Asia Pacific, Middle East & Africa, and Latin America, reflecting diverse levels of technological adoption, regulatory environments, and market maturity.

The Asia Pacific region, dominating the market with a 56.9% share and valued at USD 44.8 billion, leads due to its large automotive base and increasing penetration of connected services. Countries like China, Japan, and South Korea are at the forefront, leveraging telematics for commercial and passenger vehicles to enhance connectivity and real-time data monitoring.

Regional Mentions:

In North America, the market is driven by advanced technological infrastructure and stringent regulations regarding vehicle safety and emissions. The adoption of fleet management solutions and insurance telematics is particularly high, supported by a robust logistics sector.

Europe follows closely, with a strong emphasis on safety and environmental standards boosting the demand for telematics. The region benefits from the presence of leading automotive manufacturers and tech companies, which foster innovation and integration of telematics solutions.

Middle East & Africa and Latin America are emerging markets with growing potential. The Middle East shows promising growth due to increased awareness about driver safety and efficient fleet operations. Africa’s market is gradually rising with the increasing commercial vehicle segment.

Latin America, meanwhile, is experiencing growth driven by improvements in infrastructure and a rising standard of living, which are amplifying the demand for vehicle telematics solutions.

Collectively, these regions present a diverse landscape for the vehicle telematics market, each contributing uniquely to its global expansion and technological evolution. The Asia Pacific’s dominance is underscored by its substantial market share, setting the pace for innovations and adoption in other regions.

Key Regions and Countries covered іn thе rероrt

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In the global vehicle telematics market, several key players are pivotal in shaping the industry landscape in 2023. Among these, Bosch Limited stands out due to its comprehensive solutions spanning safety, security, and connectivity. Bosch’s integration of advanced diagnostics and real-time data tracking sets a benchmark in enhancing vehicle performance and driver experience.

Airbiquity Inc., with its focus on the development of the Choreo platform and over-the-air (OTA) technology, plays a critical role in facilitating seamless updates and security improvements. This capability is essential in maintaining the integrity and efficiency of telematics systems amidst rapidly evolving automotive technologies.

Teletrac Navman and Trimble Inc. are notable for their robust fleet management solutions. These companies leverage GPS tracking and analytics to offer insights that improve fleet efficiency and compliance with regulatory standards. Their tools are instrumental in reducing operational costs and enhancing the sustainability of fleet operations.

AT&T Inc. and Verizon Connect are leading in providing network solutions that support vast data transfers essential for real-time communications and cloud-based functionalities in vehicles. Their reliable connectivity solutions are vital for the operational efficacy of telematics systems across various vehicle types.

Furthermore, companies like Geotab Inc. and TomTom International B.V. are pivotal in advancing the navigational and mapping technologies, which are integral to the accuracy and usability of telematics applications.

Collectively, these companies drive innovation in the vehicle telematics market, each contributing to the advancements in vehicle technology, safety, and efficiency. Their efforts are crucial in addressing the demands of a dynamic market and in fostering an environment ripe for technological integrations in the automotive sector.

Top Key Players in the Market

- Bosch Limited

- Airbiquity Inc.

- Teletrac Navman

- AT&T Inc.

- Verizon Connect

- Trimble Inc.

- Geotab Inc.

- TomTom International B.V.

- Vodafone Automotive

- Masternaut Limited

- Omnitracs

- Continental AG

- CalAmp Corp.

- MiX Telematics

- Octo Telematics

- Others

Recent Developments

- In March 2024, Stellantis announced a significant investment of €5.6 billion in South America, marking the largest financial commitment in the region’s automotive industry to date. This investment aims to enhance manufacturing capabilities and drive economic growth in the automotive sector.

- In October 2023, the United States Department of Transportation (USDOT) opened a $40 million grant opportunity aimed at advancing connected vehicle technologies. These funds are designed to support innovations that will significantly improve safety on the nation’s roadways.

- In December 2024, Toyota was selected to receive $4.5 million in federal funding for the development of technologies that support a circular domestic supply chain for electric vehicle batteries. This initiative focuses on promoting sustainability and reducing dependency on international suppliers.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 80.1 Billion |

| Forecast Revenue (2033) | USD 159.3 Billion |

| CAGR (2024-2033) | 9% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology Type (Embedded, Tethered, Integrated), By Solution (Component, Service), By Vehicle Type (Passenger, Commercial), By Application Type (Insurance Telematics, Information & Navigation, Safety & Security, Fleet Management, Others), By Sales Channel (OEM, Aftermarket) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Bosch Limited, Airbiquity Inc., Teletrac Navman, AT&T Inc., Verizon Connect, Trimble Inc., Geotab Inc., TomTom International B.V., Vodafone Automotive, Masternaut Limited, Omnitracs, Continental AG, CalAmp Corp., MiX Telematics, Octo Telematics, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |