Quick Navigation

Report Overview

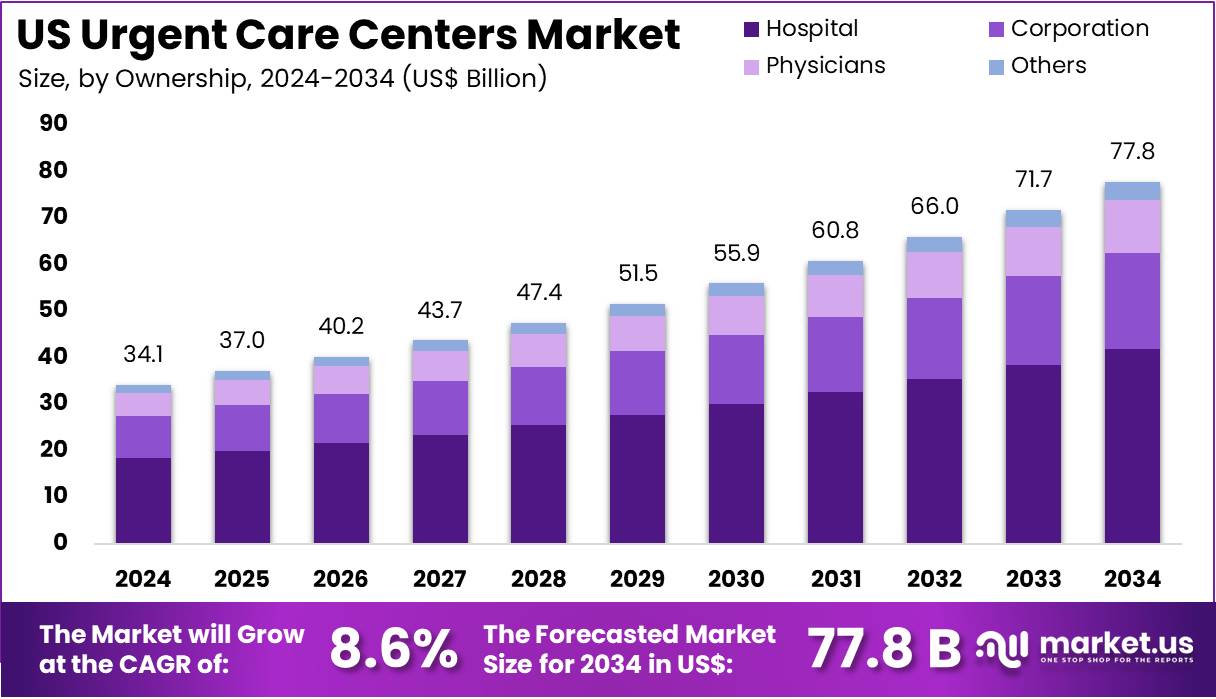

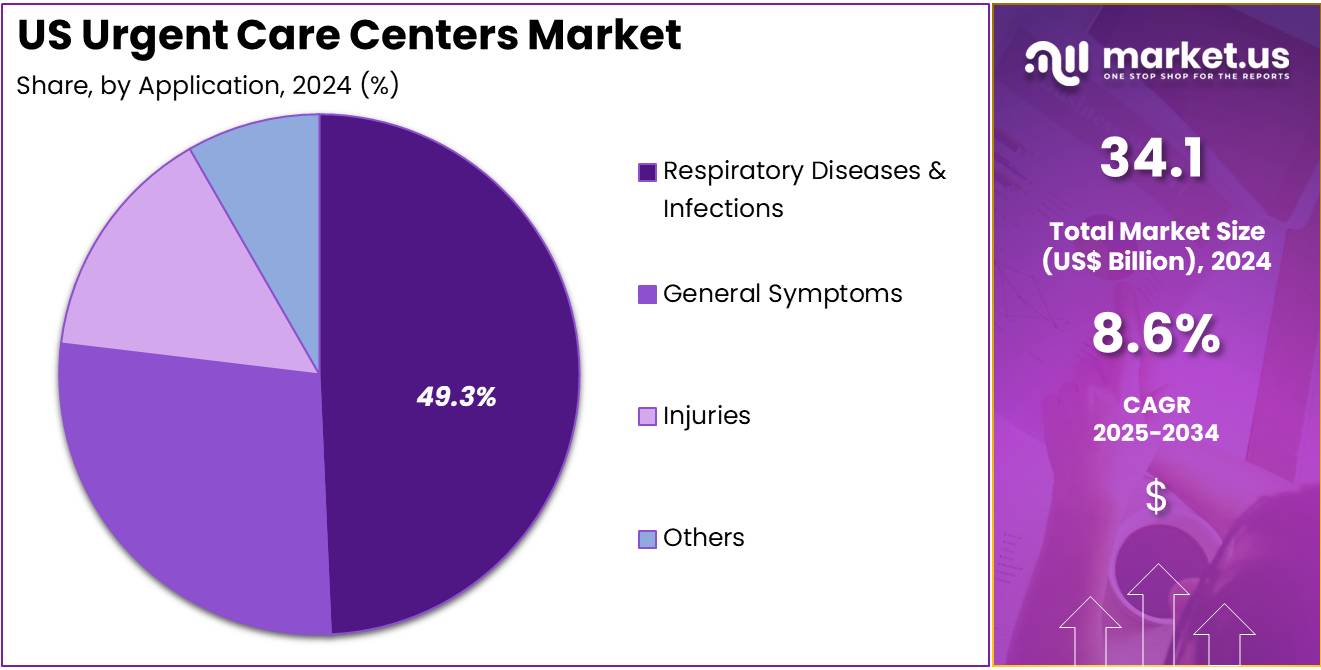

The US Urgent Care Centers Market size is expected to be worth around US$ 77.8 billion by 2034 from US$ 34.1 billion in 2024, growing at a CAGR of 8.6% during the forecast period 2025 to 2034.

Increasing demand for convenient, cost-effective healthcare solutions is driving the growth of the US urgent care centers market. These centers provide immediate, walk-in care for non-life-threatening conditions such as minor injuries, infections, and illnesses, offering patients an alternative to emergency room visits. The growing need for accessible healthcare, particularly among busy individuals seeking quick and affordable treatment options, fuels the expansion of urgent care services.

In July 2025, the University of Maryland Urgent Care will expand its services by opening two additional locations in Anne Arundel County, improving access to prompt care for non-emergency conditions. The rise in health insurance coverage, along with flexible operating hours, further boosts the popularity of urgent care centers as a viable option for after-hours medical needs.

Technological advancements, such as telemedicine integration and electronic health record systems, are improving the efficiency and quality of care provided at urgent care centers. Furthermore, as urgent care centers focus on expanding services like diagnostic testing, physicals, and immunizations, they are becoming more comprehensive healthcare providers.

The shift toward value-based care models and reimbursement incentives for urgent care services presents new opportunities for growth. As the market continues to evolve, urgent care centers are positioned to meet the increasing demand for convenient and affordable medical care, with an emphasis on patient satisfaction and timely treatment.

Key Takeaways

- In 2024, the market for US urgent care centers generated a revenue of US$ 34.1 billion, with a CAGR of 8.6%, and is expected to reach US$ 77.8 billion by the year 2034.

- The ownership segment is divided into hospital, corporation, physicians, and others, with hospital taking the lead in 2024 with a market share of 53.7%.

- Considering application, the market is divided into respiratory diseases & infections, general symptoms, injuries, and others. Among these, respiratory diseases & infections held a significant share of 49.3%.

Ownership Analysis

The hospital segment led in 2024, claiming a market share of 53.7% as hospitals increasingly expand their reach to meet the rising demand for urgent care services. Hospitals are likely to invest in urgent care centers to provide immediate care for non-emergency conditions, which alleviates the strain on emergency departments and enhances overall patient care efficiency. The rising preference for walk-in, low-cost treatment options is anticipated to drive hospital-owned urgent care centers, especially as hospitals seek to provide more accessible healthcare services.

Additionally, hospitals benefit from integrating urgent care centers into their networks, enabling seamless patient referrals and continuity of care. The increasing emphasis on cost-effective healthcare delivery and patient convenience is expected to further contribute to the growth of hospital-owned urgent care centers in the US market.

Application Analysis

The respiratory diseases & infections held a significant share of 49.3% due to the rising incidence of respiratory illnesses, such as the flu, COVID-19, and seasonal allergies. As respiratory diseases remain a major concern, particularly during flu seasons or viral outbreaks, urgent care centers are likely to see increased demand for rapid diagnostics and treatments. The ability to offer timely and cost-effective care for conditions like bronchitis, pneumonia, and asthma exacerbations is expected to drive the growth of this segment.

Furthermore, the growing public awareness about the importance of early diagnosis and treatment for respiratory infections is anticipated to increase patient visits to urgent care centers. The convenience of walk-in services, along with the ability to offer diagnostic tests such as rapid COVID-19 and flu tests, is likely to support the continued expansion of this segment.

Key Market Segments

By Ownership

- Hospital

- Corporation

- Physicians

- Others

By Application

- Respiratory Diseases & Infections

- General Symptoms

- Injuries

- Others

Drivers

Increasing demand for convenient and accessible healthcare is driving the market

Increasing demand for convenient and accessible healthcare is driving the US urgent care centers market. Patients actively seek prompt medical attention for illnesses and injuries that are not severe enough for an emergency room but require care sooner than a primary care appointment allows. Urgent care centers bridge this gap, offering walk-in access and extended operating hours, including evenings and weekends, directly addressing patient needs for timely and convenient medical services.

Data from the CDC’s National Center for Health Statistics indicates substantial utilization of urgent and unscheduled care settings; in 2022, there were an estimated 155 million emergency department visits in the US, highlighting a significant volume of episodic care encounters where urgent care provides a readily available alternative for less acute issues.

Restraints

Staffing shortages and rising labor costs are restraining the market

Staffing shortages and rising labor costs are restraining the US urgent care centers market. Urgent care centers face significant challenges in recruiting and retaining qualified healthcare professionals, including physicians, nurses, medical assistants, and radiologic technologists. Competition for these skilled workers is intense across the healthcare industry, particularly in certain geographic areas, leading to increased labor costs and difficulty maintaining adequate staffing levels.

This can impact the ability of urgent care centers to operate at full capacity, potentially leading to longer patient wait times and impacting the overall efficiency and quality of care provided. The Bureau of Labor Statistics reported that the median annual wage for healthcare support occupations was US$ 37,180 in May 2024, reflecting the significant personnel costs associated with operating healthcare facilities like urgent care centers.

Opportunities

Expansion of services offered by urgent care centers is creating growth opportunities

Expansion of services offered by urgent care centers is creating growth opportunities in the US urgent care centers market. Many urgent care facilities are strategically broadening their service offerings beyond basic urgent care. This includes integrating primary care services, providing routine physicals and vaccinations, offering occupational health services to local businesses, and expanding in-house diagnostic capabilities such as more advanced imaging or laboratory testing.

This diversification allows urgent care centers to capture a wider patient base and increase revenue streams. The US Department of Health and Human Services (HHS) has ongoing initiatives aimed at expanding access to comprehensive, community-based healthcare, aligning with the trend of urgent care centers evolving into more integrated healthcare providers and offering a broader range of services to meet community needs.

Macroeconomic and geopolitical factors influence the US urgent care centers market. Economic downturns can impact patient volumes as individuals might delay seeking care for minor conditions due to concerns about out-of-pocket costs, including deductibles and copayments, even though urgent care is generally less expensive than emergency rooms. Inflation increases operating expenses for urgent care centers, driving up the costs of medical supplies, pharmaceuticals, utilities, and labor, which directly affects their financial viability.

Geopolitical instability can indirectly impact urgent care operations by disrupting global supply chains for essential medical supplies and diagnostic equipment, potentially leading to temporary shortages or price volatility. Despite these challenges, the inherent value proposition of urgent care as a cost-effective and accessible alternative to emergency departments becomes more attractive during economic pressures, potentially driving increased utilization for certain patient segments.

Current US tariff policies impact the US urgent care centers market by increasing the cost of medical supplies and equipment. Urgent care centers rely on a wide range of imported medical goods, including diagnostic equipment like X-ray machines and lab analyzers, as well as numerous disposable supplies such as gloves, masks, bandages, and testing kits. Tariffs levied on these imported items increase the acquisition cost for urgent care operators, impacting their operational budgets and potentially influencing the cost of services passed on to patients.

Reports in April 2025 highlighted that US tariffs could increase healthcare industry costs, partly due to tariffs on imported medical products. However, tariff policies can also encourage investment in domestic manufacturing of medical supplies and equipment, potentially leading to greater supply chain resilience and more stable pricing for these critical items in the long term, offering a potential future benefit to urgent care centers.

Latest Trends

Increased integration with larger health systems and payers is creating growth opportunities

Increased integration with larger health systems and payers is creating growth opportunities in the US urgent care centers market. Hospitals and health systems are increasingly affiliating with or acquiring urgent care centers to build more integrated healthcare networks. This strategy provides health systems with convenient access points for patients, helps manage patient flow by diverting non-emergent cases from costly emergency departments, and allows for better coordination of care across the continuum.

Similarly, payers are increasingly contracting with urgent care networks to provide a lower-cost alternative for episodic care compared to emergency rooms. While comprehensive government statistics on health system ownership of urgent care centers are not specifically tracked, data from the American Hospital Association indicates that 3,525 community hospitals were part of a health system in 2023, highlighting the widespread trend of healthcare integration that includes outpatient facilities like urgent care centers.

Key Players Analysis

Key players in the US urgent care market employ strategies such as expanding service offerings, forming strategic partnerships, and enhancing accessibility to drive growth. They diversify services by incorporating specialties like occupational health, behavioral health, and wellness programs to attract a broader patient base.

Partnerships with hospitals and insurance providers enable integrated care models, improving patient outcomes and streamlining services. Additionally, expanding clinic locations in underserved areas and offering extended hours increase patient access and convenience. Adoption of telemedicine and digital health tools further enhances service delivery, catering to the growing demand for remote healthcare options.

MedExpress Urgent Care is a prominent player in the US urgent care sector, operating over 200 centers across multiple states. The company offers a wide range of services, including treatment for minor injuries and illnesses, physical exams, and vaccinations. MedExpress focuses on providing convenient, high-quality care with extended hours, aiming to reduce emergency room congestion and offer patients an alternative for non-emergency medical needs. Their commitment to accessibility and patient-centered care has positioned them as a leading provider in the urgent care industry.

Top Key Players in the US Urgent Care Centers Market

- Yale New Haven Health

- Virginia Mason Franciscan Health

- NextCare Urgent Care

- MedExpress Urgent Care

- FastMed Urgent Care

- CityMD Urgent Care

- Aurora Urgent Care

- American Family Care

Recent Developments

- In September 2024, Yale New Haven Health (YNHH) introduced a rebranded identity for its urgent care facilities, reflecting an updated approach to patient care. The first site to adopt the new Yale New Haven Health Urgent Care name was its Fairfield, Connecticut, location at 340 Grasmere Ave., signaling a fresh direction in accessible healthcare services.

- In July 2024, Virginia Mason Franciscan Health (VMFH) announced a strategic collaboration with Intuitive Health, a leader in hybrid emergency and urgent care solutions. This partnership aims to enhance healthcare accessibility across the Puget Sound area, particularly in response to persistent COVID-19 challenges and evolving patient needs.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 34.1 billion |

| Forecast Revenue (2034) | US$ 77.8 billion |

| CAGR (2025-2034) | 8.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Ownership (Hospital, Corporation, Physicians, and Others), By Application (Respiratory Diseases & Infections, General Symptoms, Injuries, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Yale New Haven Health, Virginia Mason Franciscan Health, NextCare Urgent Care, MedExpress Urgent Care, FastMed Urgent Care, CityMD Urgent Care, Aurora Urgent Care, American Family Care. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |