Quick Navigation

Report Overview

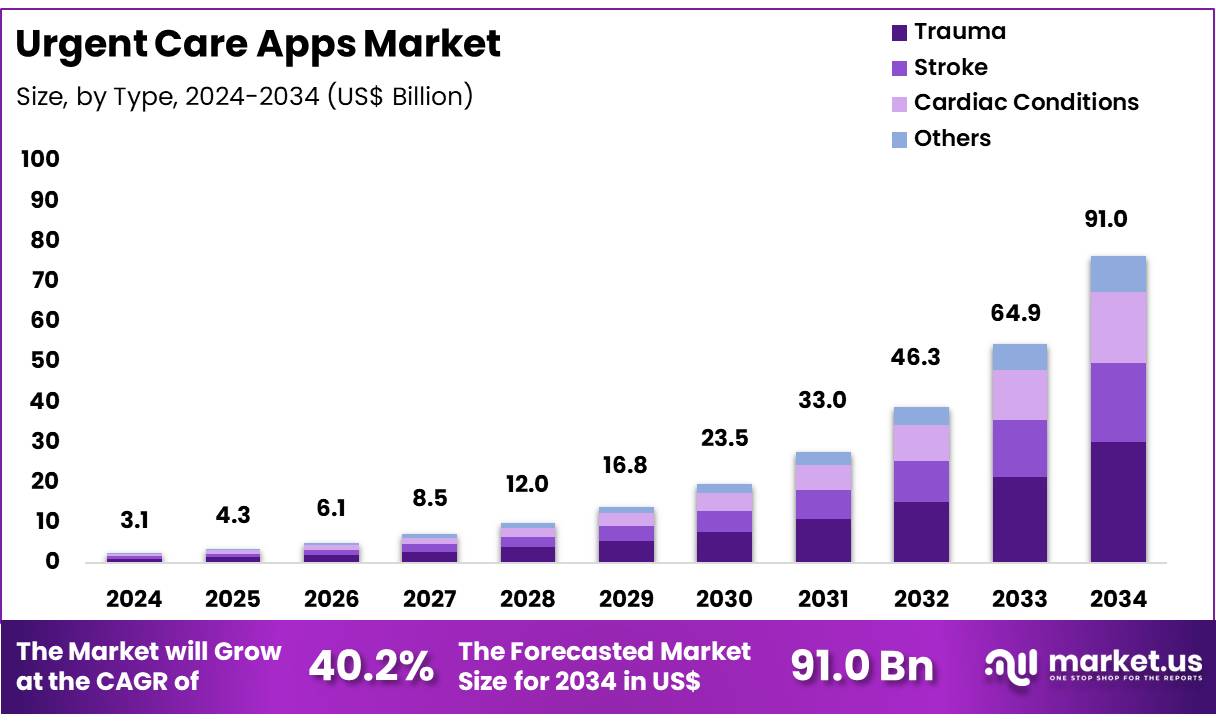

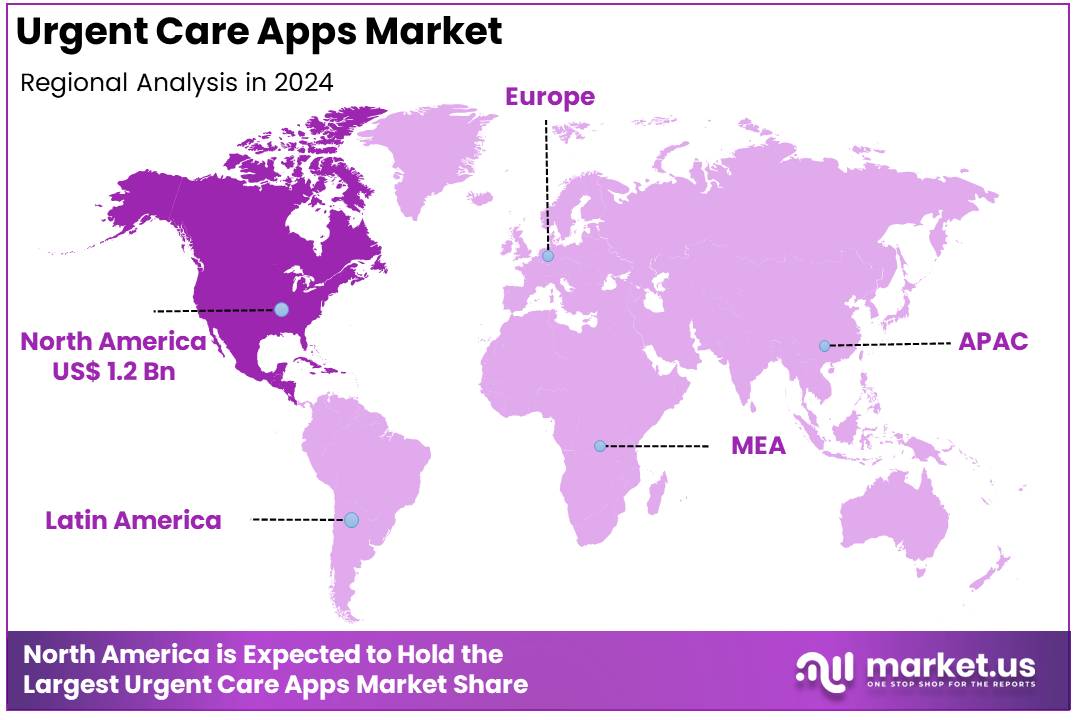

Global Urgent Care Apps Market was valued at USD 3.1 billion in 2024 and is anticipated to register substantial growth of USD 91.0 billion by 2034, with 40.2% CAGR. With a market share over 39%, North America held a strong lead in 2023, reaching US$ 1.2 Billion in revenue.

The global urgent care apps market is experiencing rapid growth, driven by increasing demand for convenient, accessible healthcare services. Key factors fuelling this market expansion include the rising adoption of smartphones and digital health technologies, which allow patients to access urgent care services remotely, reducing wait times and alleviating the strain on traditional healthcare systems.

Additionally, growing healthcare awareness and the need for timely medical intervention in non-emergency cases are contributing to the market’s expansion. Telemedicine and virtual consultations have become vital components of urgent care apps, offering patients the ability to receive consultations, diagnoses, and prescriptions without visiting physical clinics.

Furthermore, the COVID-19 pandemic accelerated the adoption of digital health solutions, as individuals sought safer, contactless healthcare alternatives. The increasing focus on cost-effectiveness, convenience, and accessibility is also propelling market growth, with consumers preferring immediate, non-emergency care over visiting crowded hospitals or emergency rooms. However, challenges such as data privacy concerns, regulatory hurdles, and integration with existing healthcare systems could hinder market growth.

Key Takeaways

- The global urgent care apps market was valued at USD 3.1 billion in 2024 and is anticipated to register substantial growth of USD 91.0 billion by 2034, with 40.2% CAGR.

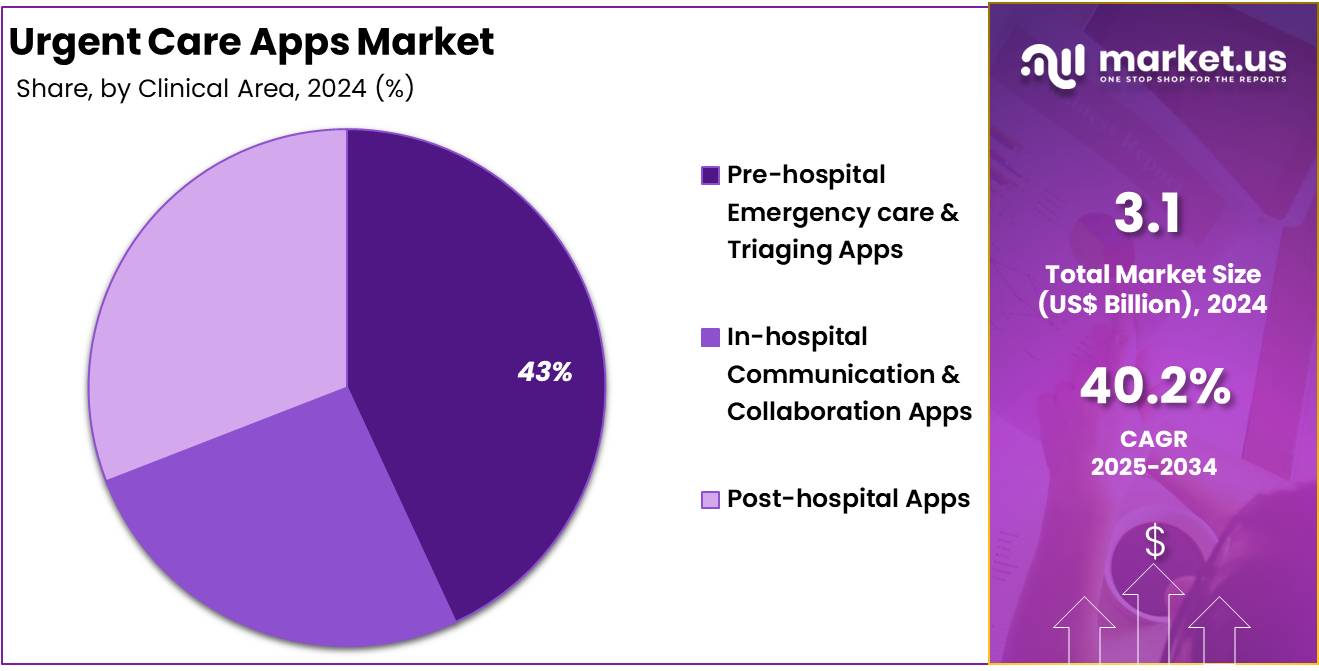

- In 2024, the Post-hospital Apps segment took the lead in the global market, securing 43% of the total revenue share.

- The trauma segment took the lead in the global market, securing 33% of the total revenue share.

- North America maintained its leading position in the global market with a share of over 39% of the total revenue.

Type Analysis

Based on Type the market is fragmented into pre-hospital emergency care & triaging apps, in-hospital communication & collaboration apps, and post-hospital apps. Amongst these, post-hospital apps dominated the global urgent care apps market capturing a significant market share of 53% in 2024.

Post-hospital apps have dominated the global urgent care apps market, driven by the growing demand for continuous care and remote monitoring after patients are discharged. These apps play a critical role in managing post-acute conditions, enhancing patient outcomes by providing ongoing support, tracking recovery progress, and reducing hospital readmissions.

- For example, the WoundZoom Light app, launched in November 2024, offers a digital solution for wound assessment and management, allowing healthcare providers to capture images, monitor healing, and collaborate remotely. This innovation reflects a broader trend in the healthcare industry towards improving post-hospital care through technology, enabling more personalized and efficient recovery processes.

By facilitating better communication between patients and healthcare providers, post-hospital apps help in managing chronic conditions and supporting rehabilitation, thereby enhancing the overall quality of care and optimizing resource allocation in the healthcare system. As these apps become more sophisticated, they are expected to further transform post-acute care management.

Clinical Area Analysis

The market is fragmented by clinical area into trauma, stroke, cardiac conditions, and others. Trauma dominated the global urgent care apps market capturing a significant market share of 49% in 2024. Trauma care has become a dominant segment in the global urgent care apps market, driven by the increasing need for rapid, efficient responses to traumatic injuries. These apps are pivotal in improving pre-hospital care, enabling faster intervention, and potentially saving lives.

- For example, the Trauma Care International Foundation’s Emergency Response app, launched in March 2021, aims to address trauma-related morbidity and mortality in Nigeria, particularly in Lagos.

By connecting emergency victims with trained volunteer responders, the app enhances the efficiency of trauma care by providing immediate assistance before hospital arrival. This app complements existing emergency frameworks, allowing for seamless coordination between responders, hospitals, and other stakeholders.

The app’s focus on real-time communication, resource optimization, and collaboration between various trauma care providers reflects a growing trend in leveraging digital health tools to improve emergency trauma management. As the global demand for trauma-related urgent care rises, such innovations are expected to shape the future of emergency response systems.

Key Segments Analysis

Type

- Pre-hospital Emergency care & Triaging Apps

- In-hospital Communication & Collaboration Apps

- Post-hospital Apps

- Medication Management Apps

- Rehabilitation Apps

- Care Provider Communication & Collaboration Apps

Clinical Area

- Trauma

- Stroke

- Cardiac Conditions

- Others

Driver

Growing Demand for Telemedicine

The growing demand for telemedicine, which was significantly accelerated by the COVID-19 pandemic, has greatly increased the need for urgent care apps that provide remote consultations and triaging services.

- According to data from the American Medical Association (AMA), the use of telemedicine surged, with virtual visits rising from 11% to 46% of all outpatient visits between 2019 and 2021.

This shift underscores a key driver for the urgent care apps market, as both healthcare systems and patients increasingly turn to remote solutions for addressing health concerns. Urgent care apps have become essential for offering virtual consultations, symptom management, and triaging, effectively reducing the need for in-person visits. These apps meet the growing demand for convenient, accessible healthcare, ensuring timely medical interventions while minimizing the risk of infection exposure. As the trend toward remote care continues to grow, the role of urgent care apps becomes even more crucial, driving continued market expansion.

Restraints

Data Security and Privacy Concerns

Data security and privacy are critical challenges in the urgent care apps market, as safeguarding sensitive patient information from breaches is essential.

- For example, Teladoc Health, which manages personal health records and offers virtual consultations, handles over 20 million patient interactions annually. A data breach involving such an app could expose extensive personal information, including detailed medical histories and identifiers. According to the 2023 Annual Data Breach Report, the number of data breaches increased by 78% in 2023, with 3,205 incidents reported compared to 1,801 in 2022.

These breaches can result in severe consequences, such as identity theft, financial fraud, and a significant loss of user trust, which could ultimately impede the growth of the market. As concerns over data privacy and security intensify, ensuring robust protection measures becomes increasingly important for the sustained development of the urgent care apps industry.

Opportunities

Technological Advancement

Technological advancements are creating significant growth opportunities for the urgent care apps market, as innovations in AI, machine learning, and mobile health technologies enhance the accuracy, efficiency, and accessibility of care.

- In June 2024, researchers in Australia introduced a groundbreaking technology that allows smartphones to detect strokes more rapidly compared to conventional methods.

By using AI to analyse facial symmetry and muscle movements, the technology identifies signs of stroke, as victims often show facial asymmetry. This kind of innovation opens new doors for urgent care apps, allowing for faster diagnosis and intervention in critical situations.

Moreover, advancements in wearable devices, remote monitoring, and telemedicine integration are enabling continuous patient tracking and immediate access to healthcare professionals. These technologies improve patient outcomes, streamline care delivery, and reduce healthcare costs, making urgent care apps an increasingly essential tool in modern healthcare systems. The ongoing development of such technologies will continue to drive market expansion globally.

Impact of macroeconomic factors / Geopolitical factors

Macroeconomic and geopolitical factors significantly influence the global urgent care apps market, shaping both demand and innovation in the sector. Economic downturns, for instance, may drive the adoption of cost-effective healthcare solutions, as individuals and healthcare providers seek affordable alternatives to traditional care settings.

During recessions, patients may turn to urgent care apps to avoid expensive emergency room visits, boosting market growth. Conversely, periods of economic growth can spur investments in healthcare technology, facilitating advancements in app features like AI-driven diagnostics and remote patient monitoring. Geopolitical factors, such as political instability or healthcare system disruptions, can further catalyze the need for urgent care apps, especially in regions with limited access to healthcare infrastructure.

Latest Trends

The urgent care apps market is evolving rapidly, driven by several key trends. One of the latest trends is the integration of Artificial Intelligence (AI) and Machine Learning (ML) for enhanced diagnostic accuracy and personalized treatment plans. These technologies enable apps to offer more precise symptom checkers, predictive analytics, and tailored health recommendations.

Another emerging trend is the expansion of telemedicine services, allowing users to consult healthcare professionals remotely, which has gained significant traction due to the ongoing demand for convenient, contactless care post-COVID-19.

Additionally, the use of wearable devices and IoT (Internet of Things) integration is becoming more prevalent, enabling real-time health monitoring and data sharing between patients and healthcare providers. Mental health support through urgent care apps is also on the rise, addressing the growing need for psychological care.

Regional Analysis

North America held a significant 39% share of the urgent care apps market driven by the region’s advanced healthcare infrastructure, high smartphone penetration, and strong adoption of digital health technologies.

The demand for urgent care apps in this region is further fuelled by the need for timely, convenient healthcare solutions that reduce the burden on traditional healthcare systems. These apps enable seamless integration with existing healthcare frameworks, providing quick access to consultations, which is especially valuable for non-emergency conditions.

- For example, in October 2023, Cedars-Sinai launched the Cedars-Sinai Connect mHealth app, leveraging AI from K Health to deliver virtual care for a range of conditions, including urgent and primary care. This app offers 24/7 access to healthcare professionals, streamlining the intake process and connecting patients to providers for video consultations

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The urgent care apps market is characterized by a diverse range of players, including established healthcare providers, tech companies, and startups, all vying to innovate and capture market share. Key players such as Amwell and Doctor on Demand offer comprehensive telemedicine services, including urgent care, with a focus on user-friendly interfaces, AI-driven diagnostics, and 24/7 access to healthcare professionals.

Emerging players are also leveraging advanced technologies like Artificial Intelligence, machine learning, and wearables to enhance diagnostic capabilities, improve patient outcomes, and increase app functionality. Additionally, partnerships between healthcare systems and tech companies are becoming common, as seen in collaborations like Cedars-Sinai’s launch of the Cedars-Sinai Connect mHealth app, which integrates AI for virtual care.

Allm Inc. is a leading provider of digital health solutions, focused on improving healthcare workflows and emergency response systems. The company specializes in developing healthcare communication platforms that enable real-time collaboration between healthcare providers, particularly in emergency and urgent care settings.

In addition, Twiage Solutions Inc. is a healthtech company focused on optimizing emergency medical response and trauma care through digital solutions. Its platform, “Twiage,” provides real-time, secure communication between first responders, emergency medical technicians (EMTs), and hospitals, facilitating faster and more accurate patient information sharing.

Top Key Players

- Allm Inc.

- Johnson & Johnson Services, Inc.

- PatientSafe Solutions (Stryker)

- AlayaCare

- Twiage Solutions Inc.

- TigerConnect

- Siilo from Doctolib

- Imprivata, Inc.

- Medisafe

- CommuniCare Technology, Inc. (Pulsara)

- Smartpatient gmbh

Recent Developments

- In June 2024, the University of Ottawa Heart Institute partnered with TELUS to introduce a smartphone app aimed at enhancing the efficiency of emergency cardiac care. The app facilitates improved communication between paramedics, emergency teams, and cardiac specialists, ensuring faster treatment for heart attack patients.

- In May 2023, Zocdoc, Inc. expanded its platform to include urgent care services, allowing patients to quickly access care for acute medical issues. The new feature connects users with nearby urgent care providers, offering same-day or next-day appointments and streamlining the process of securing immediate healthcare.

- In August 2021, the Mount Sinai Health System launched a mobile app designed to improve care for heart attack patients by streamlining communication among care teams and expediting treatment. The app provides real-time data and notifications, enabling coordination between paramedics, emergency departments, and cardiologists, ultimately improving response times during critical situations.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 3.1 billion |

| Forecast Revenue (2034) | US$ 91.0 billion |

| CAGR (2025-2034) | 40.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Pre-hospital Emergency care & Triaging Apps, In-hospital Communication & Collaboration Apps, and Post-hospital Apps), By Clinical Area (Trauma, Stroke, Cardiac Conditions, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Allm Inc., Johnson & Johnson Services, Inc., PatientSafe Solutions (Stryker), AlayaCare, Twiage Solutions Inc., TigerConnect, Siilo from, Doctolib, Imprivata, Inc., Medisafe, CommuniCare Technology, Inc. (Pulsara), and Smartpatient gmbh |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |