Quick Navigation

- Report Scope

- Key Takeaways

- Analyst’s Review

- Key Statistics

- Regional Analysis

- By Aircraft Type

- By Propulsion

- By Flight Operation

- By Technology

- By End Use

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunities

- Challenging Factors

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Player Analysis

- Recent Developments

- Report Scope

Report Scope

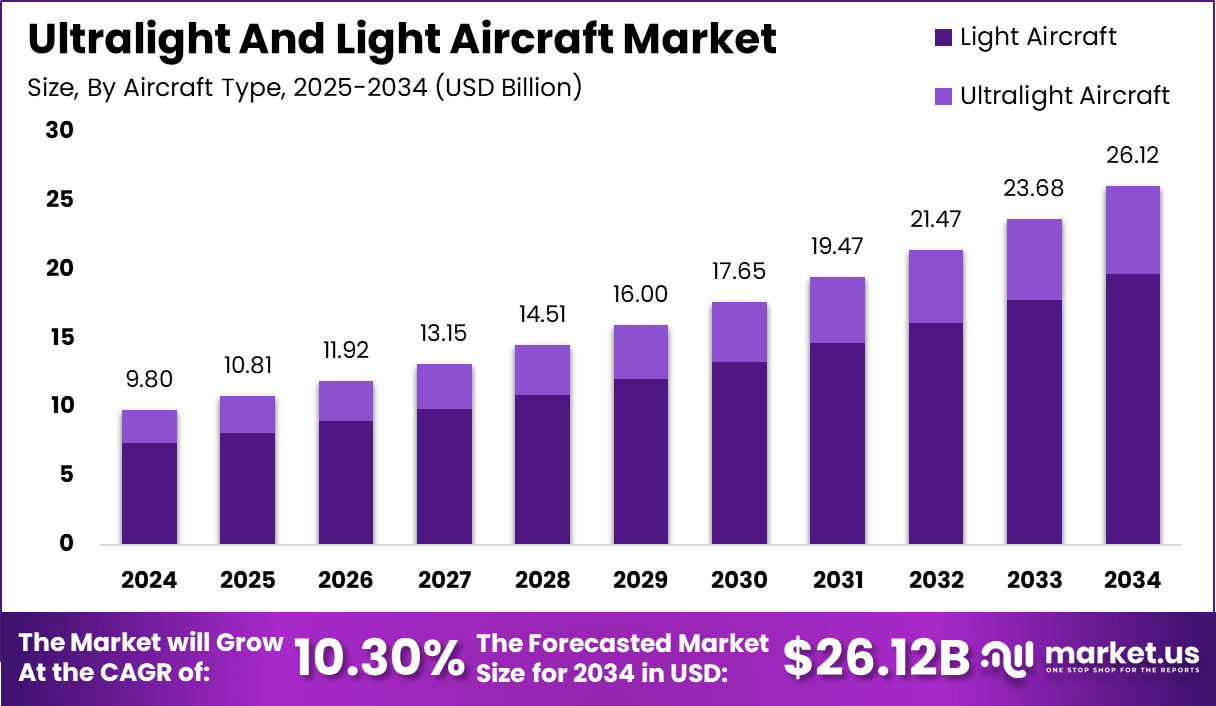

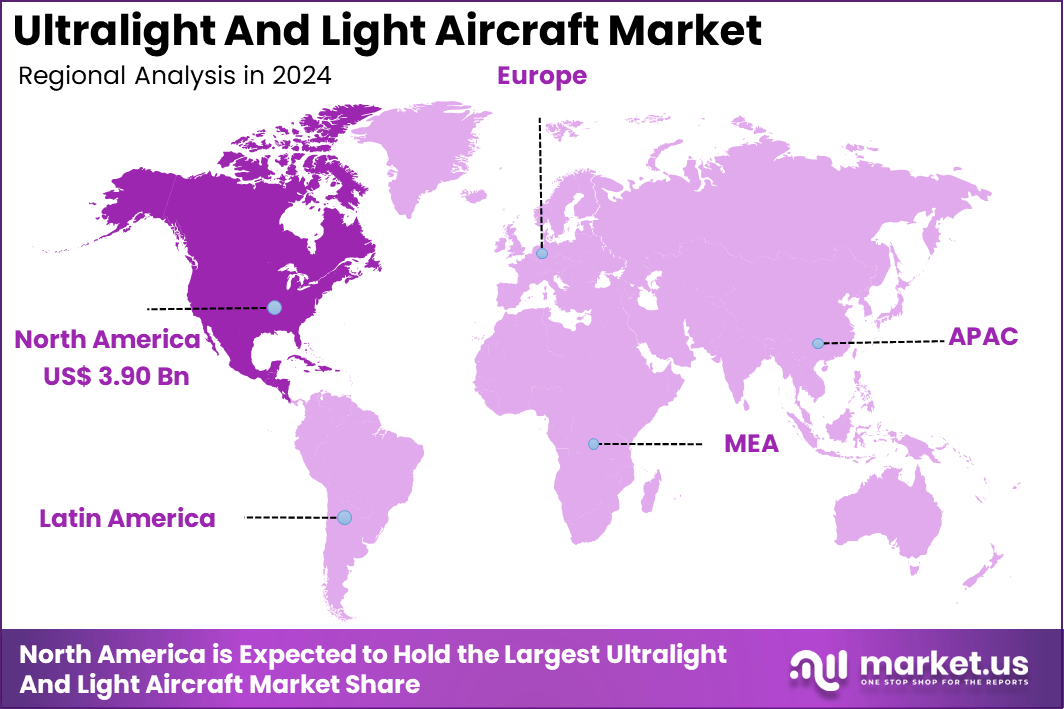

The Global Ultralight And Light Aircraft Market is expected to be worth around USD 26.12 Billion by 2034, up from USD 9.8 Billion in 2024. It is expected to grow at a CAGR of 10.30% from 2025 to 2034. In 2024, North America held a dominant market position, capturing over a 30% share and earning USD 3.90 Billion in revenue.

The ultralight and light aircraft market has grown steadily in recent years, driven by increasing interest in personal aviation, recreational flying, and low-cost air transportation solutions. Ultralight aircraft, typically weighing less than 254 pounds, and light aircraft, generally classified as weighing between 2,500 and 5,700 pounds, are gaining popularity due to their affordability, ease of operation, and versatile applications.

These aircraft are often used for leisure activities, flight training, and even short regional flights. With advancements in materials, safety technologies, and fuel efficiency, the ultralight and light aircraft market is expected to continue expanding globally.

Several key factors are driving the growth of the ultralight and light aircraft market. First, there is a growing demand for affordable air travel options, especially for recreational purposes. Many individuals are seeking alternatives to traditional, expensive forms of flying, and ultralight and light aircraft present a cost-effective solution.

Additionally, the increasing popularity of private aviation, coupled with a surge in aviation enthusiasts, has bolstered the demand. Regulatory changes in some regions have also allowed for more lenient pilot certification processes, making these aircraft more accessible to a broader audience. Moreover, improvements in fuel efficiency and the development of electric propulsion systems are further supporting the market’s growth.

Key Takeaways

- Market Value: The ultralight and light aircraft market is expected to be valued at USD 9.8 billion in 2024.

- Projected Market Value: The market is set to grow significantly, reaching USD 26.12 billion by 2034, with a CAGR of 10.30%.

- By Aircraft Type: Light aircraft dominate the market with a 75.3% share.

- By Propulsion: Conventional propulsion systems account for 89.0% of the market.

- By Flight Operation: CTOL (Conventional Takeoff and Landing) aircraft make up 77.2%.

- By Technology: Manned aircraft represent 73.5% of the market.

- By End Use: Civil and commercial aviation uses account for 68.1% of the market.

- Geographical Insights: North America holds the largest share at 39.8%, leading the global market.

Analyst’s Review

The demand for ultralight and light aircraft is rising primarily in regions where general aviation is becoming more popular, such as North America and Europe. As more people look to invest in personal aircraft, either for recreational purposes or for flying training, the demand for these lightweight aircraft is expected to continue growing. This trend is particularly prominent in the U.S., where the demand for both ultralight and light aircraft is consistently strong. Additionally, emerging markets in Asia and Latin America are showing an increasing appetite for these aircraft as they begin to develop their aviation infrastructure.

The market for ultralight and light aircraft offers several promising opportunities, particularly in the areas of electric aviation and new aircraft designs. The rise of electric propulsion systems presents significant growth potential, as these systems offer lower operating costs and reduced environmental impact compared to traditional combustion engines. This is particularly attractive in regions with stringent environmental regulations.

Furthermore, there is an opportunity for manufacturers to innovate with lighter materials and more efficient engines, improving fuel economy and extending the range of these aircraft. Another notable opportunity lies in the training sector, where flight schools are increasingly looking to incorporate light and ultralight aircraft into their training fleets, offering a more affordable entry point for new pilots.

Technological advancements in ultralight and light aircraft are helping to drive the market forward. Innovations in materials, such as lightweight composites and advanced alloys, are making aircraft more fuel-efficient and durable, contributing to both performance improvements and cost reductions. Additionally, the development of more efficient engines and hybrid-electric propulsion systems is opening up new possibilities for the industry.

These advancements not only reduce operational costs but also make the aircraft more environmentally friendly. In terms of avionics, there have been significant improvements in cockpit technologies, with enhanced flight control systems, GPS navigation, and autopilot features making these aircraft safer and easier to operate. As these technological trends continue to evolve, they will further boost the growth of the ultralight and light aircraft market.

Key Statistics

Usage and Applications

- Applications

- Used for recreational flying, flight training, aerial photography, agriculture (crop dusting), search and rescue missions, environmental monitoring, and patrolling.

- Also used for surveys, mapping, and imaging in agricultural, environmental, and defense sectors.

- User Base

- Increasing demand from high-net-worth individuals and small businesses.

- Growing interest in personal aviation and recreational flying.

Quantity and Production

- Production Volume: The production volume is increasing, with a projected growth in units from 5,548 in 2024 to 7,044 by 2029.

- Manufacturers: Key manufacturers include Cirrus Design, Textron, Pilatus Aircraft, Piper Aircraft, AutoGyro, ICON Aircraft, and Zin Aviati.

Other Statistics

- Weight and Specifications

- Ultralight aircraft typically have a maximum take-off weight of 254 pounds in the U.S..

- Light aircraft can weigh up to 12,500 pounds.

- Speed and Performance

- Ultralight aircraft have a top speed in level flight of no more than 55 knots and a power-off stall speed of no more than 24 knots.

Regional Analysis

In 2024, North America held a dominant market position, capturing more than a 39% share, equating to USD 3.82 billion in revenue. This region’s leadership is primarily attributed to the robust demand for both recreational and private aviation, as well as the increasing popularity of flight training. North America, particularly the U.S., has a well-established general aviation infrastructure, which makes it a prime market for ultralight and light aircraft.

The regulatory environment in the U.S. also plays a pivotal role, with relatively lenient pilot certification requirements making it easier for individuals to purchase and operate light aircraft. Additionally, advancements in electric propulsion technologies are being widely explored in North America, further boosting the market’s growth. The strong presence of key manufacturers and aviation companies in the region contributes to North America’s continued dominance in the ultralight and light aircraft market.

In 2024, Europe accounted for a substantial portion of the market, capturing approximately 30% share, with revenues of USD 2.94 billion. Europe’s growing aviation sector, especially in countries like the UK, Germany, and France, is driving the demand for light aircraft. With increasing interest in recreational flying and affordable personal aircraft, Europe is seeing more consumers opt for light aircraft as an alternative to more expensive traditional aviation options. Additionally, European regulations have evolved to make light aviation more accessible.

In the Asia-Pacific (APAC) region, the ultralight and light aircraft market is expected to grow at a significant pace, capturing an estimated 15% market share by 2024. This growth can be attributed to emerging markets such as China, India, and Australia, where increasing disposable income, evolving aviation infrastructure, and growing interest in private and recreational flying are driving demand. The region is seeing an influx of private aviation enthusiasts, flight schools, and businesses looking for cost-effective transportation solutions.

In Latin America, the ultralight and light aircraft market accounted for around 5% of the global share in 2024, generating USD 490 million in revenue. The demand for these aircraft is growing in countries like Brazil and Mexico, where there is increasing interest in general aviation and private flying as a viable transportation option. Latin America’s economic growth and rising interest in aviation, particularly in more remote areas where conventional transportation options are limited, are fueling the market.

In the Middle East and Africa, the ultralight and light aircraft market is still in its early stages, with a smaller market share of approximately 3-4% in 2024. However, this region is expected to witness substantial growth in the coming years. The UAE, Saudi Arabia, and South Africa are showing increasing interest in aviation as part of broader economic diversification efforts.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

By Aircraft Type

In 2024, the Light Aircraft segment held a dominant market position, capturing more than 75.3% of the market share. This dominance is largely due to the growing demand for versatile, cost-effective aircraft that cater to both recreational aviation and practical transportation needs. Light aircraft offer a balance of affordability, performance, and range, making them highly attractive for private owners, flight schools, and commercial operators.

They are suitable for a wide range of applications, including short regional flights, flight training, and even light cargo transport. Moreover, their relatively low operating costs compared to heavier commercial aircraft, combined with increasing interest in private aviation, have driven the widespread adoption of light aircraft.

Additionally, technological advancements, such as more fuel-efficient engines and improved safety features, have further boosted the appeal of light aircraft. With the global increase in aviation enthusiasts and the growing trend of personal air travel, the Light Aircraft segment is expected to continue leading the ultralight and light aircraft market in the coming years.

By Propulsion

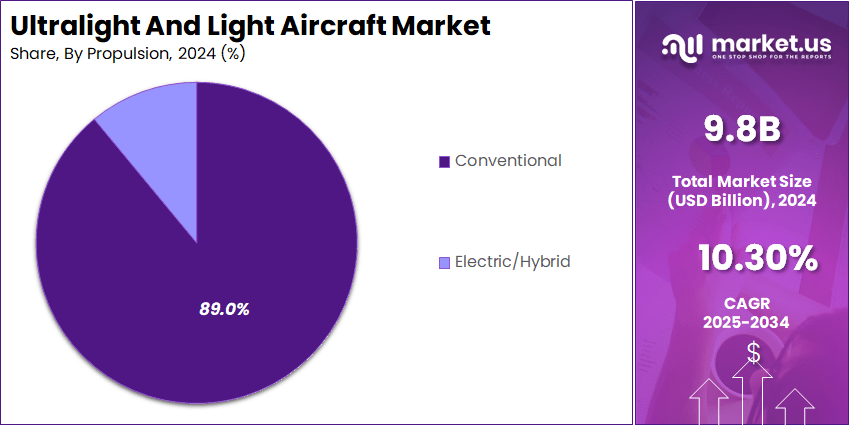

In 2024, the Conventional propulsion segment held a dominant market position, capturing more than 89.0% of the market share. The widespread dominance of conventional propulsion systems in the ultralight and light aircraft market is primarily due to their proven reliability, lower upfront costs, and established infrastructure.

Conventional engines, typically powered by gasoline or aviation fuel, are well-understood technologies with a strong support network for maintenance and servicing, making them a preferred choice for both recreational pilots and flight schools. Additionally, these propulsion systems offer longer flight ranges and more consistent performance, especially in regions where the adoption of electric or hybrid technologies is still in the early stages.

While electric and hybrid propulsion systems are gaining attention due to their environmental benefits, conventional engines remain the go-to solution due to their cost-effectiveness and availability. As the market continues to evolve, it’s expected that conventional propulsion will continue to dominate until advancements in electric propulsion make them a more viable alternative for broader adoption.

By Flight Operation

In 2024, the CTOL (Conventional Takeoff and Landing) segment held a dominant market position, capturing more than 77.2% of the market share. This segment’s dominance is driven by the wide adoption and operational simplicity of CTOL aircraft, which are well-suited for existing infrastructure.

CTOL aircraft require standard runways, which are readily available in most regions, making them the most practical and cost-effective choice for personal, training, and commercial operations. These aircraft are also easier to operate and maintain compared to VTOL (Vertical Takeoff and Landing) aircraft, which require specialized equipment and infrastructure.

Additionally, CTOL aircraft tend to have longer flight ranges, better fuel efficiency, and lower operational costs, contributing to their continued preference across the market. While VTOL aircraft hold promise for urban air mobility and future aviation needs, the cost and complexity of their technology, combined with the extensive global network of runways, keep CTOL aircraft as the dominant choice for ultralight and light aviation applications in 2024.

By Technology

In 2024, the Manned segment held a dominant market position, capturing more than 73.5% of the market share. This segment’s dominance is largely due to the longstanding tradition and widespread acceptance of piloted aircraft in the ultralight and light aircraft markets. Manned aircraft are primarily used for recreational flying, flight training, and personal aviation, with a well-established infrastructure for pilot licensing and maintenance services.

The appeal of manned aircraft lies in their versatility, allowing operators to have direct control over the aircraft and make real-time adjustments during flight. Additionally, manned aircraft have broader applications in general aviation, including short regional flights, where human oversight is critical for safety and navigation.

While unmanned aircraft systems (UAS) are gaining traction in sectors like surveillance, cargo transport, and data collection, they are not yet as widely adopted in the ultralight and light aircraft market. The continuing preference for direct human control in aviation ensures that the Manned segment remains the leading choice in 2024.

By End Use

In 2024, the Civil and Commercial segment held a dominant market position, capturing more than 68.1% of the market share. This segment’s leadership can be attributed to the increasing demand for affordable and efficient aviation solutions in personal, recreational, and business applications.

Civil and commercial aviation, particularly for short regional flights and private ownership, is growing steadily as more individuals and companies seek cost-effective alternatives to traditional air travel. Light and ultralight aircraft offer flexibility, lower operational costs, and ease of access to smaller airports, making them an attractive option for both leisure pilots and small businesses.

Additionally, the rise of flight schools, flying clubs, and tourism-related aviation activities has significantly contributed to the growth of this segment. While the military also utilizes light aircraft for specific tasks, such as training and surveillance, the civilian market’s diverse and expanding needs continue to dominate the ultralight and light aircraft industry. As more people enter the aviation market, the Civil and Commercial segment is expected to remain the largest in the coming years.

Key Market Segments

By Aircraft Type

- Ultralight Aircraft

- Light Aircraft

By Propulsion

- Conventional

- Electric/Hybrid

By Flight Operation

- CTOL

- VTOL

By Technology

- Manned

- Unmanned

By End Use

- Civil and Commercial

- Military

Driving Factors

Increasing Demand for Affordable Aviation Solutions

One of the key driving factors for the growth of the ultralight and light aircraft market is the increasing demand for affordable aviation solutions. Over the years, the cost of owning and operating an aircraft has steadily decreased, making private and recreational flying more accessible to a wider audience. Light and ultralight aircraft offer lower operational costs, fuel efficiency, and maintenance expenses compared to traditional aircraft, which has been a major draw for aviation enthusiasts, private owners, and even small businesses.

Additionally, the popularity of general aviation and the rise of flight schools looking to offer cost-effective training options have contributed significantly to the market’s growth. As more people seek alternatives to expensive commercial flights, light and ultralight aircraft are seen as an attractive option for both personal and business use. These aircraft are perfect for regional and short-distance flights, further driving demand in areas where air connectivity is limited.

Restraining Factors

Regulatory Challenges and Certification Processes

Despite the growth potential, one of the major restraining factors for the ultralight and light aircraft market is the complex regulatory landscape and certification processes. The aviation industry, particularly when it comes to aircraft safety and operations, is highly regulated, and these regulations vary across different countries. In many regions, ultralight and light aircraft are subject to stringent certification requirements and operational guidelines that can delay market entry or increase the overall cost of ownership.

In particular, the process of getting certification for new models or modifying existing designs is often long and expensive. Manufacturers need to comply with a variety of international and national aviation standards, which may include multiple rounds of testing, approval from aviation authorities, and comprehensive safety inspections. For small manufacturers or startups, this can prove to be a significant barrier, limiting the number of players in the market and reducing competition.

Growth Opportunities

Integration of Electric Propulsion Technology

One of the most promising growth opportunities in the ultralight and light aircraft market is the integration of electric propulsion technology. As the aviation industry faces increasing pressure to reduce carbon emissions and improve environmental sustainability, electric and hybrid-electric aircraft are being viewed as a viable alternative to conventional fuel-powered models. This shift could significantly reduce operating costs, especially in terms of fuel and maintenance, which has historically been one of the most expensive aspects of owning an aircraft.

Electric propulsion systems are especially appealing for ultralight and light aircraft due to their potential for quieter operations and reduced environmental impact. Moreover, the development of more efficient battery technologies and lightweight materials is enhancing the viability of electric aircraft, making them more suitable for short to medium-range flights. These advantages position electric-powered light aircraft as a significant opportunity for both manufacturers and operators looking to capitalize on the growing demand for sustainable aviation solutions.

Challenging Factors

High Initial Investment Costs

While light and ultralight aircraft offer lower operational costs, one of the biggest challenges faced by potential buyers is the high initial investment required for purchasing these aircraft. Even though these aircraft are generally more affordable than commercial airplanes, the upfront cost can still be prohibitive for many individuals and small businesses. For example, a new light aircraft can cost anywhere from tens of thousands to several hundred thousand dollars, depending on the model and specifications.

In addition to the purchase price, there are other associated costs such as training, licensing, insurance, storage, and maintenance, all of which add to the financial burden. These costs can deter many potential buyers from entering the market, particularly in developing economies or among recreational pilots who may not have the financial means for such an investment. The high cost of ownership also limits the broader adoption of ultralight and light aircraft for business or commercial applications in sectors like air tourism or regional transport.

Growth Factors

Several key growth factors are contributing to the rapid expansion of the ultralight and light aircraft market. First, the growing interest in private and recreational aviation has significantly boosted demand for affordable flying options. This growth is being driven by the increasing number of aviation enthusiasts and the rising demand for flight schools offering affordable training programs.

Another major growth factor is the continued advancement in technology, particularly in terms of fuel efficiency, lightweight materials, and electric propulsion systems. The global push for greener technologies has accelerated the development of electric and hybrid-electric aircraft, creating new growth opportunities in the market. Additionally, increased government support for the aviation industry, including tax incentives and subsidies for environmentally friendly aircraft, is further stimulating market growth.

Emerging Trends

The ultralight and light aircraft market is witnessing several emerging trends that are shaping its future. One significant trend is the integration of electric and hybrid-electric propulsion systems into aircraft designs. With increasing environmental concerns, electric propulsion is gaining traction as a sustainable alternative to traditional fuel-powered engines. By 2030, it’s expected that electric and hybrid aircraft will account for up to 5% of the global fleet, highlighting the growing shift towards greener aviation solutions.

Additionally, urban air mobility (UAM) is emerging as a key trend, with electric vertical takeoff and landing (eVTOL) aircraft gaining attention for their potential to revolutionize air transportation in congested urban environments. Companies like Joby Aviation and Lilium are advancing these technologies, and governments are investing in the necessary infrastructure to support UAM solutions.

Business Benefits

The growth of the ultralight and light aircraft market offers several business benefits, particularly for aviation companies, flight schools, and manufacturers. For businesses, one of the primary advantages is the lower operating costs of ultralight and light aircraft compared to traditional aircraft. These aircraft are more fuel-efficient, cost less to maintain, and require less expensive storage options, making them ideal for small businesses looking to operate in the aviation space.

For flight schools and training organizations, the demand for light aircraft is beneficial due to their affordability and versatility in providing flight training. By using light aircraft, flight schools can lower tuition costs for students, making flight training more accessible to a broader audience. Additionally, light aircraft’s relatively simple operating systems allow students to gain flying experience without the complexity of larger aircraft.

Key Player Analysis

Piper Aircraft, a leading manufacturer of light aircraft, has been a dominant player in the ultralight and light aircraft market for decades. The company is known for its diverse range of general aviation aircraft, including the Piper Archer and Piper Cub models, which are widely used for flight training, personal flying, and small business operations.

Cirrus Aircraft is widely recognized for its innovative approach to designing light aircraft, particularly with its flagship product, the Cirrus SR22, a high-performance single-engine aircraft favored by private pilots. One of Cirrus’ most notable achievements is the development of the Cirrus Vision Jet, the world’s first single-engine personal jet, which has disrupted the light aircraft market by offering a faster, more luxurious flying experience.

Tecnam Aircraft, an Italian aircraft manufacturer, has been carving out a significant share in the ultralight and light aircraft market, known for its high-quality and cost-effective planes. The company produces a wide variety of light aircraft, from single-engine trainers to twin-engine models, with a strong emphasis on lightweight construction and fuel efficiency.

Top Key Players in the Market

- Piper Aircraft, Inc.

- Cirrus Aircraft

- Tecnam Aircraft

- Textron Aviation Inc.

- Diamond Aircraft

- ICON Aircraft, Inc.

- Flight Design general aviation GmbH

- Honda Aircraft Company

- Vulcanair

- Pilatus Aircraft Ltd

- Other Key Players

Recent Developments

- In 2024: Piper Aircraft launched the new Piper M600 SLS, incorporating advanced safety features and Garmin Autoland technology, marking a significant step in aircraft automation.

- In 2024: Cirrus Aircraft unveiled the upgraded SR22T, featuring enhanced avionics and improved fuel efficiency, positioning it as a leading option in the high-performance light aircraft market.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 9.8 Billion |

| Forecast Revenue (2034) | USD 26.12 Billion |

| CAGR (2025-2034) | 10.30% |

| Largest Market | North America |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | Aircraft Type (Ultralight Aircraft, Light Aircraft), By Propulsion (Conventional, Electric/Hybrid) By Flight Operation (CTOL, VTOL), By Technology (Manned, Unmanned), By End Use (Civil and Commercial, Military) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | Piper Aircraft, Inc., Cirrus Aircraft, Tecnam Aircraft, Textron Aviation Inc., Diamond Aircraft, ICON Aircraft, Inc., Flight Design general aviation GmbH, Honda Aircraft Company, Vulcanair, Pilatus Aircraft Ltd, Other Key Players |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |