Quick Navigation

- Report Overview

- Key Takeaways

- Fleet and Flight Statistics

- Analysts’ Viewpoint

- US Tariff Impact Analysis

- North America Private Aircraft Market Size

- Type Analysis

- Size Analysis

- Ownership Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Player Analysis

- Recent Developments

- Report Scope

Report Overview

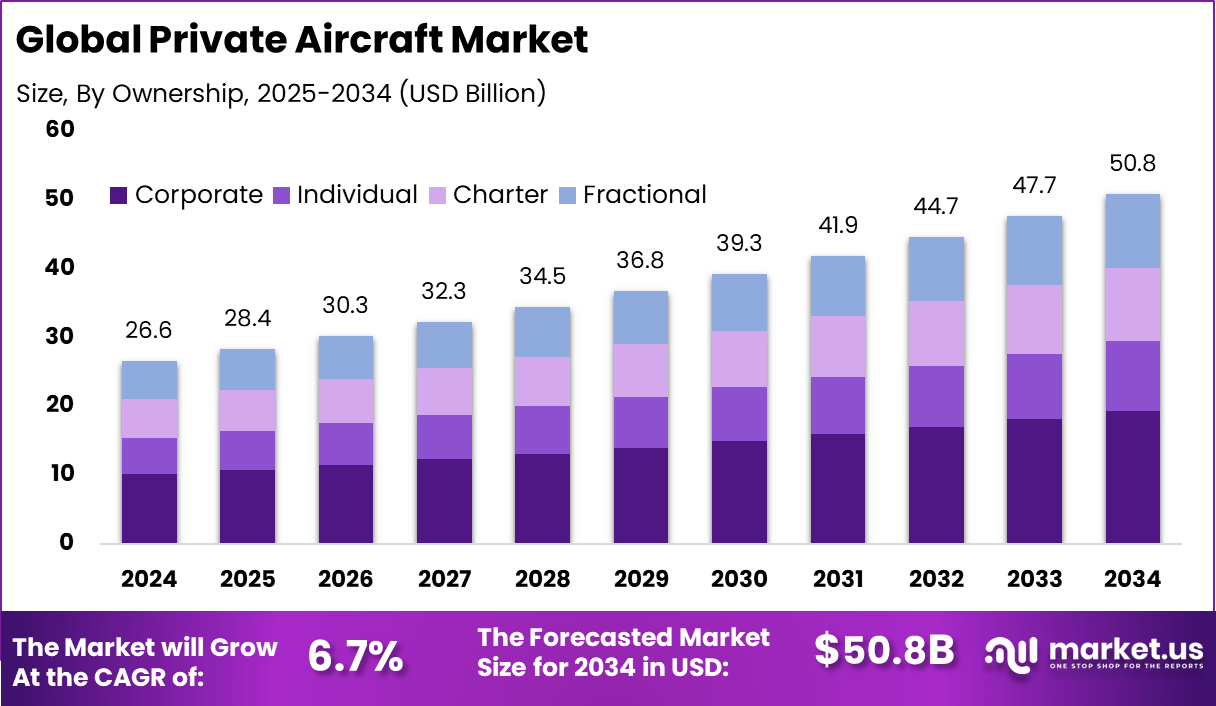

The Global Private Aircraft Market size is expected to be worth around USD 50.8 Billion By 2034, from USD 26.6 billion in 2024, growing at a CAGR of 6.7% during the forecast period from 2025 to 2034.

The private aircraft market has expanded as high net worth individuals, corporations and charter operators increase their use of business jets for fast, flexible and point to point travel. Growth reflects rising demand for personalised aviation, improved cabin technologies and stronger interest in private mobility solutions for business and leisure. The market includes light jets, mid size aircraft, long range models and turboprops used for both ownership and charter services.

Top driving factors include rising disposable incomes and global economic growth that encourage luxury travel and quick access to multiple destinations. Demand analysis shows that business jets represent over 34% market share due to corporate needs for flexible, direct travel, while light aircraft account for more than 40%, favored for operational flexibility and affordability. Technological advances like safety systems, noise reduction, and predictive maintenance boost confidence and lower long-term costs, encouraging adoption.

According to Market.us, The Global Aircraft Market is expected to grow steadily, reaching approximately USD 596.5 billion by 2033, up from USD 414.8 billion in 2023, at a compound annual growth rate (CAGR) of 3.7% during the forecast period from 2024 to 2033. This growth is being driven by increasing air travel demand, fleet modernization programs, and technological advancements in fuel-efficient aircraft models.

For instance, In March 2023, Flexjet, a prominent player in the US market for fractional aircraft ownership and jet card services, strategically initiated its private helicopter service in Europe by incorporating the Sikorsky S-76 helicopter into its fleet. This launch marks the beginning of Flexjet’s expansion across European skies, enhancing its service offerings and operational capabilities within the region.

Key Takeaways

- The Global Private Aircraft Market is on a strong growth path, projected to reach USD 80.8 Billion by 2034, up from USD 26.6 Billion in 2024.

- This growth reflects a solid CAGR of 6.7% from 2025 to 2034, driven by rising demand for personalized air travel and time-saving mobility.

- In 2024, Business Airplanes accounted for more than 34% of the market share, highlighting their continued popularity among executives and entrepreneurs.

- Light Aircraft led the market in 2024, holding a dominant 40%+ share, thanks to their affordability, operational flexibility, and ease of ownership.

- The Corporate segment secured over 38% of the market in 2024, showing how businesses are investing more in private aviation for convenience and efficiency.

Fleet and Flight Statistics

- Global private aircraft count reached about 26,000 as of December 2023.

- More than 4.3 million flights were conducted in 2023 across the global private aviation sector.

- Total flight time reached 6,474,710 hours, resulting in an average of 249 flight hours per aircraft.

- Average flight distance was 865.7 km, and 47.4% of all flights were under 500 km, indicating strong demand for short-haul private travel.

Analysts’ Viewpoint

The market’s expansion is creating numerous investment opportunities, particularly in the areas of advanced aircraft technologies and infrastructure to support the growing fleet of private aircraft. Investments in new manufacturing capabilities for sustainable technologies and the expansion of airport facilities to accommodate private jets are particularly promising.

Regulatory standards are also evolving, particularly with an emphasis on environmental compliance. Stricter emissions regulations are anticipated, which will drive the adoption of cleaner technologies and fuels in the aviation sector.

For businesses, using private aircraft can significantly enhance operational efficiency by reducing travel time and providing flexibility in scheduling. The ability to conduct meetings privately in-flight and reach multiple destinations quickly is a substantial advantage for corporate users.

Key factors influencing the market include technological advancements, regulatory changes, and shifts in consumer preferences towards more personalized and safe travel options. Additionally, economic factors such as global wealth distribution and corporate profits play crucial roles in shaping demand within this market.

US Tariff Impact Analysis

The US tariff policies implemented in 2025 have had a notable impact on the private aircraft sector, creating multiple challenges and strategic shifts across the industry.

Key impacts and strategic responses observed in the sector include:

- Increased Costs and Pricing Pressures: The imposition of tariffs has escalated the costs of manufacturing and importing private aircraft. Notably, materials like aluminum and steel, essential for aircraft production, have seen price increases due to tariffs. This has led to higher overall costs for manufacturing private jets, particularly those constructed with significant amounts of these materials.

- Supply Chain and Operational Disruptions: The global supply chains, highly integrated across countries, are facing disruptions due to these tariffs. This includes increased costs and complexities in procuring aviation parts and components that frequently cross borders during the manufacturing process. The increased administrative burden for compliance with customs documentation and inspections further adds to the operational challenges.

- Shifts in Demand and Market Dynamics: The increased costs might deter potential buyers, leading to shifts in demand from new purchases to alternatives like leasing or chartering. This shift could potentially boost the market for jet charters and fractional ownership models as buyers seek cost-effective alternatives to outright ownership.

- Strategic Industry Responses: Manufacturers and operators in the private aircraft sector are adopting various strategies to mitigate the impact of tariffs. This includes reassessing supply chains, considering reshoring of some production activities, and exploring new markets for aircraft sales. Moreover, there’s an increased focus on domestic production to reduce reliance on imported parts, which are subject to tariffs.

- Long-Term Industry Implications: The tariffs are likely to have lasting effects on the competitive dynamics within the global aviation industry. U.S. manufacturers may benefit from increased domestic demand if tariffs make foreign competitors more expensive. However, they face challenges in terms of increased production costs and potential retaliation from other countries that could impose their own tariffs on U.S. made aircraft.

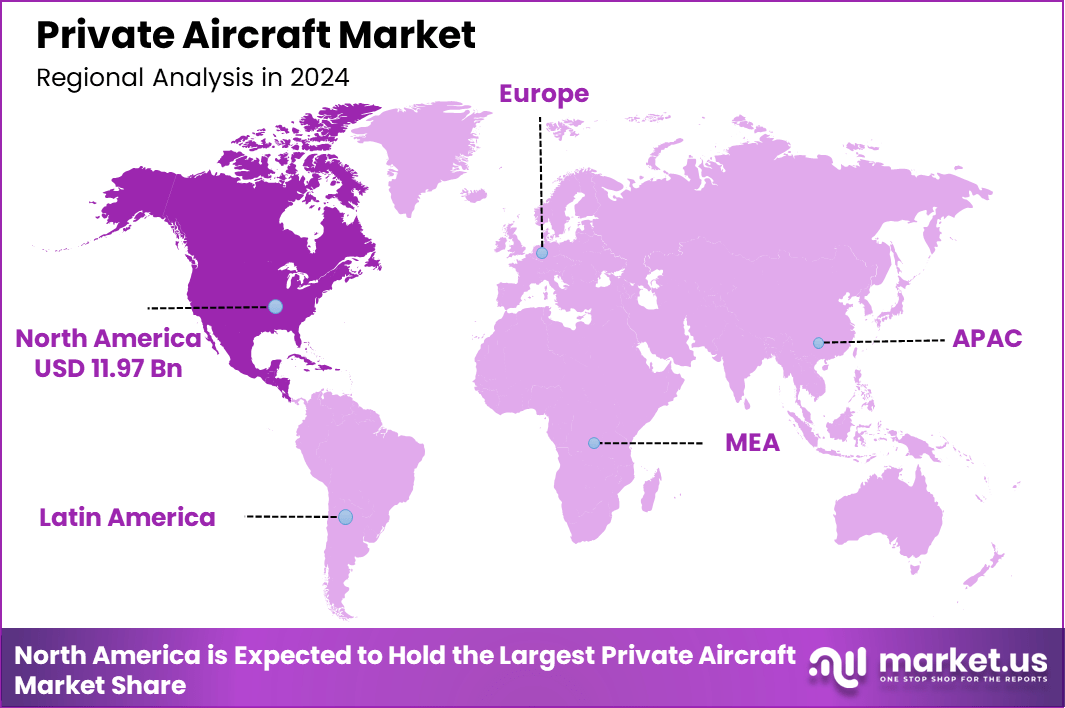

North America Private Aircraft Market Size

In 2024, North America maintained a dominant position in the private aircraft market, securing more than a 45% share with revenues amounting to USD 11.97 billion. This robust market presence can be attributed to several key factors.

North America boasts a mature aviation infrastructure and a high concentration of high-net-worth individuals who drive demand for private aircraft for both personal and business travel. The region is home to some of the world’s leading private jet manufacturers, such as Gulfstream and Bombardier, which continue to innovate in jet technology and customer experience.

The dominance of North America is also reinforced by its advanced regulatory environment and strong culture of private aviation. The market benefits from a well-established ecosystem that includes extensive maintenance facilities, training centers, and a wide network of airports capable of accommodating private jets.

Furthermore, the region’s emphasis on enhancing the sustainability and efficiency of aviation plays a crucial role in maintaining its market leadership, appealing to environmentally conscious consumers. Europe and the Asia-Pacific regions also exhibit significant activity in the private aircraft market, with Europe focusing on sustainability and luxury, while Asia-Pacific shows rapid growth due to increasing economic prosperity and expanding aviation infrastructure.

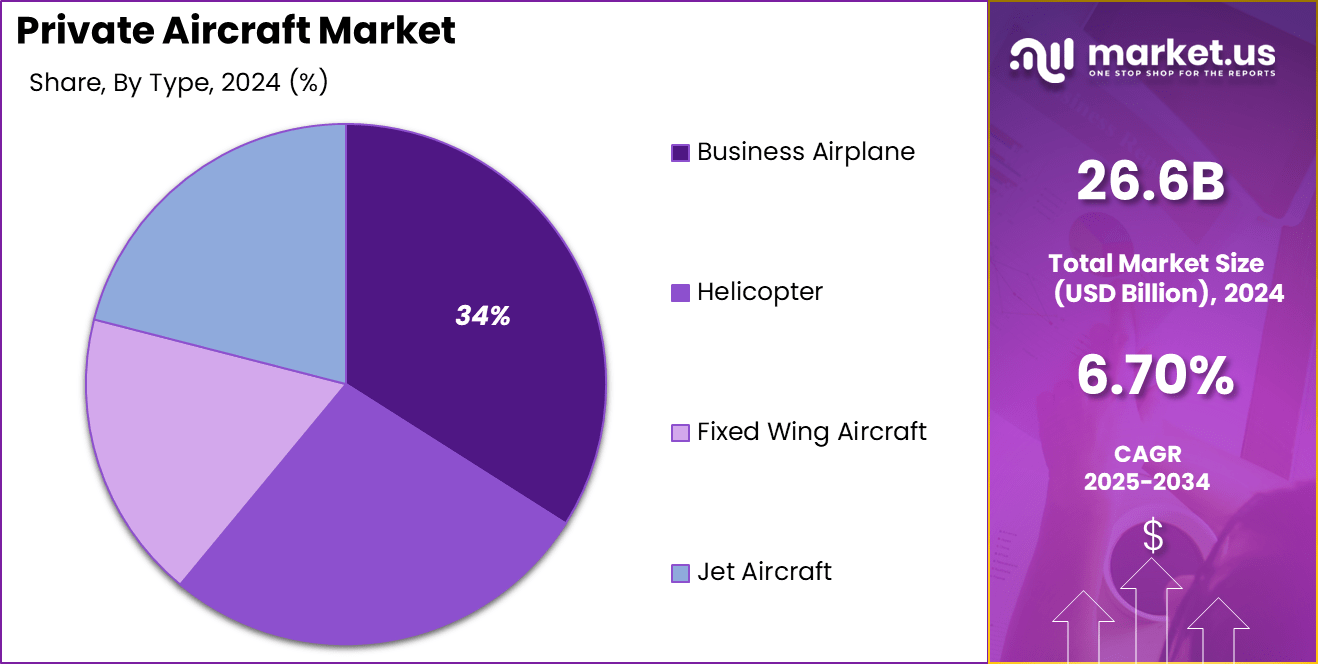

Type Analysis

In 2024, the Business Airplane segment of the private aircraft market held a significant market position, capturing more than a 34% share. This dominance is primarily driven by the escalating demand for business travel and the growing preference among high-net-worth individuals for private and efficient travel solutions.

The segment’s strength is further bolstered by the global economic growth, which has enabled a greater number of individuals and corporations to invest in private aircraft for their travel needs. Additionally, the expansion of international travel and the increasing availability of fractional ownership programs have made private flying more accessible, contributing to the growth of the business airplane segment.

These programs allow individuals to own a share of a jet, significantly reducing the cost barrier and enhancing the segment’s appeal to a broader audience. Technological advancements in aircraft efficiency and safety are also key factors driving the popularity of business airplanes, as they ensure both the performance and sustainability of travel, meeting the modern demands of business aviation.

Size Analysis

In 2024, the Light Aircraft segment dominated the private aircraft market, capturing more than a 40% share. This significant market presence is attributed to several factors that cater to a broad spectrum of users, from private individuals to flight training schools.

North America, in particular, has a substantial impact due to its deep-rooted aviation culture and extensive infrastructure, supporting a high number of flight schools and private aviation enthusiasts. The light aircraft are especially favored for their cost-effectiveness and operational efficiency, making them ideal for personal use, flight training, and recreational flying.

These aircraft types benefit from technological advancements that enhance their appeal, such as improvements in fuel efficiency and the incorporation of sustainable aviation technologies, which align with the growing environmental consciousness among consumers and corporations alike.

Moreover, the global expansion of the light aircraft market is supported by rising disposable incomes and increasing interest in personal aviation in regions like Asia-Pacific, which is witnessing rapid growth due to these factors. The versatility and accessibility of light aircraft continue to drive their popularity, ensuring their leading position in the private aircraft market landscape.

Ownership Analysis

In 2024, the Corporate segment of the private aircraft market held a significant position, securing over a 38% share. This leading stance can be attributed to the continued expansion of global business activities which necessitate efficient and flexible travel options for executives.

Additionally, the segment benefits from a strong demand for bespoke, on-demand travel solutions that align with the needs for confidentiality and customized schedules, which are particularly valued in the corporate world. Furthermore, the integration of advanced technologies and increased emphasis on sustainability within corporate fleets are enhancing the appeal of private aircraft for corporate use.

Companies are progressively prioritizing eco-friendly and technologically equipped aircraft to support their business operations and corporate responsibility goals. This trend towards high-tech, sustainable aviation solutions is expected to drive further growth in the Corporate segment of the market, reflecting a broader shift towards more responsible business travel practices.

The robust infrastructure and services tailored for corporate aviation, including luxury fittings and connectivity solutions that facilitate productive and comfortable travel, are also key factors contributing to the dominance of this market segment. As corporations continue to globalize and seek efficient travel solutions, the demand within this segment is anticipated to maintain its strong market presence.

Key Market Segments

By Type

- Helicopter

- Fixed Wing Aircraft

- Business Airplane

- Jet Aircraft

By Size

- Light

- Mid-size

- Large

By Ownership

- Individual

- Corporate

- Charter

- Fractional

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Increased Demand for Business and Leisure Travel

The private aircraft market is primarily driven by a substantial increase in both business and leisure travel. This rise is closely linked to the growing global economy, which has led to greater wealth among high-net-worth individuals and a surge in international business activities.

The need for flexible, efficient, and personalized travel options has never been higher, with many turning to private aviation as a solution to the limitations and inconveniences of commercial flying. This trend is bolstered by the wider availability of fractional ownership models, which make private flying more accessible by allowing individuals to purchase shares of aircraft, reducing the financial burden of sole ownership.

Restraint

High Costs of Ownership and Operation

One of the primary challenges facing the private aircraft market is the high cost associated with owning and operating a private jet. These costs include hefty initial purchase prices, ongoing maintenance, crew salaries, insurance, and hangar fees, which can collectively reach millions of dollars annually.

The financial burden of these expenses makes private aircraft a less viable option for a broader audience, restricting market growth predominantly to the wealthiest individuals and corporations. Additionally, the private aviation sector faces pressures from environmental regulations and increasing scrutiny over carbon emissions and noise pollution, adding further operational challenges and costs that can deter potential buyers and affect market expansion.

Opportunity

Technological Advancements and Emerging Markets

Emerging markets such as China, India, and the UAE represent a significant growth opportunity for the private aircraft sector. These regions are experiencing rapid economic development, leading to an increased number of affluent individuals and a demand for personalized travel solutions.

Moreover, the industry is poised to benefit from advancements in aircraft technology, particularly through the development of sustainable aviation fuels (SAF) and innovations in electric and hybrid aircraft. These technologies promise to enhance the efficiency and environmental friendliness of private jets, making them more appealing to a broader audience.

Challenge

Supply Chain and Talent Retention Issues

The private aircraft industry faces ongoing challenges related to supply chain disruptions and talent retention. The complexity of manufacturing and maintaining advanced aircraft requires a highly skilled workforce, which is becoming increasingly difficult to sustain.

Moreover, disruptions in the aerospace supply chain have led to delays and increased costs, complicating operations for private aircraft manufacturers and service providers. Overcoming these hurdles is crucial for maintaining the industry’s growth trajectory and meeting the evolving demands of private jet users.

Growth Factors

The private aircraft market is poised for substantial growth, driven by several key factors. One of the primary growth drivers is the increasing demand for business and leisure travel. As global economic conditions improve and wealth among high-net-worth individuals rises, there is a marked increase in the purchase of private jets for both personal and corporate use.

This trend is further fueled by the desire for more personalized, flexible, and efficient travel options, which private aircraft can provide. Additionally, the adoption of fractional ownership programs has made private flying more accessible, allowing more individuals to experience the benefits of private aviation without the need for full ownership.

Technological advancements also play a critical role in driving market growth. Innovations in aircraft efficiency, safety, and sustainability, including the development of sustainable aviation fuels (SAF) and electric aircraft, cater to a growing consumer base that is increasingly environmentally conscious. These advancements not only enhance the operational aspects of private aircraft but also contribute to broader acceptance by addressing environmental concerns.

Emerging Trends

Several emerging trends are shaping the future of the private aircraft market. The shift towards sustainable aviation, with increased adoption of sustainable aviation fuels and the development of hybrid and electric aircraft, reflects the industry’s response to environmental challenges. This trend is gaining traction as stakeholders in the aviation sector aim to reduce carbon footprints and meet stringent global emissions standards.

Additionally, there is a noticeable increase in the customization and luxury offerings within the aircraft interiors, catering to the high expectations of luxury travelers. Personalized cabins, advanced in-flight entertainment systems, and bespoke services are becoming standard features that enhance the passenger experience.

Business Benefits

The use of private aircraft provides numerous business benefits, particularly in terms of efficiency and flexibility. For corporate users, private jets offer significant time savings by allowing direct flights to destinations that may not be serviced by commercial airlines. This capability is crucial for high-level executives whose time is extremely valuable.

Moreover, private aircraft can serve as functional business spaces, equipped with connectivity and privacy, enabling in-flight productivity which is often not feasible on commercial flights. Overall, the private aircraft market is growing robustly, supported by technological innovations, emerging market demands, and changing consumer preferences. These factors collectively contribute to a dynamic and evolving market landscape, providing both challenges and opportunities for industry stakeholders.

Key Player Analysis

Top Key Players in the Market

- The Boeing Company

- Airbus Group Inc.

- Bombardier Inc.

- Gulfstream Aerospace Corporation

- Textron Aviation Inc.

- Embraer Executive Aircraft Inc.

- Dassault Aviation SA

- Honda Aircraft Company LLC

- Pilatus Flugzeugwerke AG

- Daher

- Cirrus Design Corporation

- Piper Aircraft Inc.

- Diamond Aircraft Industries

- Nextant Aerospace LLC

- Volocopter GmbH

- Other Key Players

Recent Developments

- November 2024: Embraer announced plans to strengthen its supply chain by engaging Chinese suppliers, aiming to enhance its market presence and explore strategic partnerships for new passenger jet projects.

- November 2024: AMSL Aero, an aviation start-up, completed the first free flight of its Vertiia aircraft, a hydrogen-powered plane capable of vertical take-off and landing. The company raised $55 million and plans to commence commercial flights by 2027.

- November 2024: ATR decided to halt the development of its ATR 42-600S Short Take-Off and Landing (STOL) model to focus on its existing aircraft range, following a detailed market review and supply chain challenges.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 26.6 Bn |

| Forecast Revenue (2034) | USD 50.8 Bn |

| CAGR (2025-2034) | 6.7% |

| Largest Market | North America |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Type (Helicopter, Fixed Wing Aircraft, Business Airplane, Jet Aircraft), By Size (Light, Mid-size, Large), By Ownership (Individual, Corporate, Charter, Fractional) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | Boeing Company, Airbus Group Inc., Bombardier Inc., Gulfstream Aerospace Corporation, Textron Aviation Inc., Embraer Executive Aircraft Inc., Dassault Aviation SA, Honda Aircraft Company LLC, Pilatus Flugzeugwerke AG, Daher, Cirrus Design Corporation, Piper Aircraft Inc., Diamond Aircraft Industries, Nextant Aerospace LLC, Volocopter GmbH, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |