Global Thermic Fluids Market Size, Share, And Industry Analysis Report By Grade (Low Temperature, Medium Temperature, High Temperature), By Product Type (Mineral Oils, Silicone, Aromatic, Glycol, Others), By Application (Heating, Cooling, Sterilization, Pollution Control, Others), By End-use (Oil and Gas, Chemicals, Pharmaceuticals, Food and Beverages, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2025-2034

- Published date: February 2026

- Report ID: 179082

- Number of Pages: 346

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

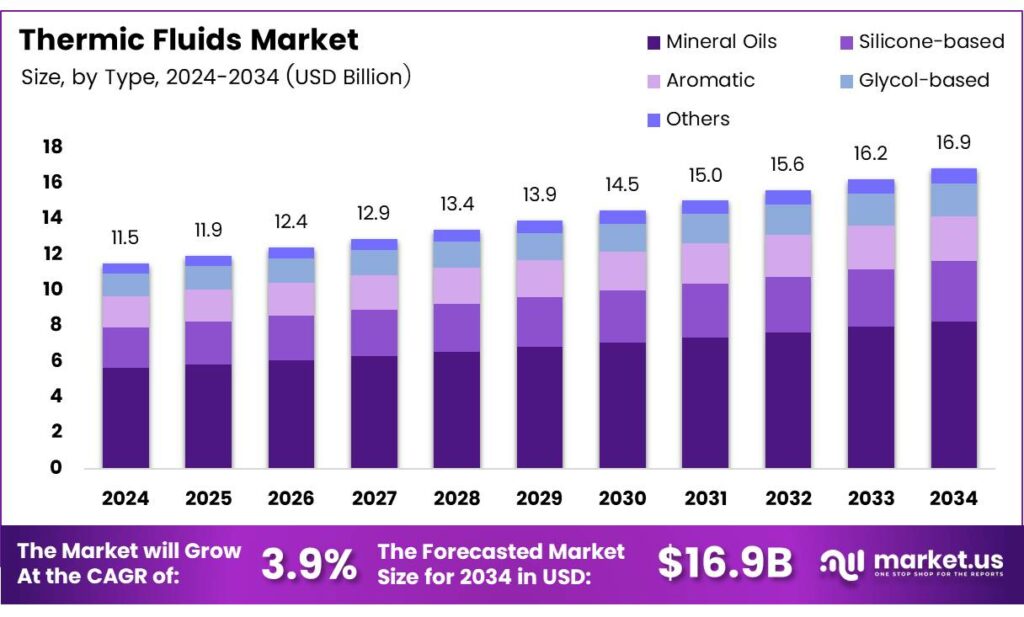

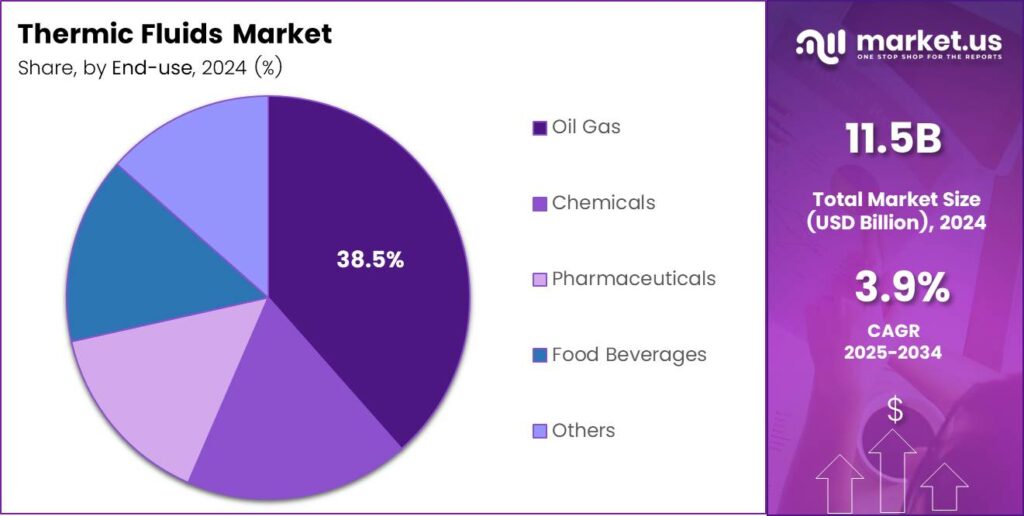

The Global Thermic Fluids Market size is expected to be worth around USD 16.9 billion by 2034 from USD 11.5 billion in 2024, growing at a CAGR of 3.9% during the forecast period 2025 to 2034.

The thermic fluids market covers a broad range of heat transfer fluids used in indirect heating and cooling systems. These fluids circulate through closed-loop systems to carry thermal energy between a heat source and a process unit. Industries depend on them to maintain precise temperature control without direct flame contact.

Thermic fluids include mineral oils, synthetic formulations, silicone-based fluids, glycol blends, and aromatic compounds. Each type serves specific temperature ranges and application conditions. Mineral oils remain widely used due to cost advantages, while synthetic variants offer higher performance at elevated temperatures.

- Heat transfer fluid exporters shipped to the U.S., with a combined shipment weight of 12,471 tons across 345 export shipments, reflecting a moderately concentrated global supply base that supports growing cross-border trade flows in thermic fluids.

- Eastman Chemical Company reported sales revenue of USD 9.4 billion in 2024, with earnings before interest and taxes of USD 1.3 billion, reinforcing its stature as a leading global supplier of specialty heat transfer fluids under the Therminol brand and signaling continued investment in this segment.

Key end-use industries include oil and gas, chemicals, pharmaceuticals, food and beverages, and power generation. These sectors rely on consistent thermal management to support safe and efficient production. Moreover, growing industrialization across emerging economies continues to expand the user base for heat transfer solutions.

Concentrated solar power projects further accelerate demand for high-stability thermal storage media. Renewable energy infrastructure requires fluids that can withstand extreme temperatures across long operational cycles. Additionally, data center expansion drives demand for immersion cooling fluids with superior heat dissipation performance.

Key Takeaways

- The Global Thermic Fluids Market is valued at USD 11.5 billion in 2024 and is projected to reach USD 16.9 billion by 2034, at a CAGR of 3.9% during the forecast period 2025 to 2034.

- Medium Temperature fluids hold the largest segment share at 56.8% in 2025.

- Mineral Oils dominate with a share of 45.1% in 2025.

- Heating leads the market with a 46.9% share in 2025.

- Oil and Gas is the leading segment with a 38.5% share in 2025.

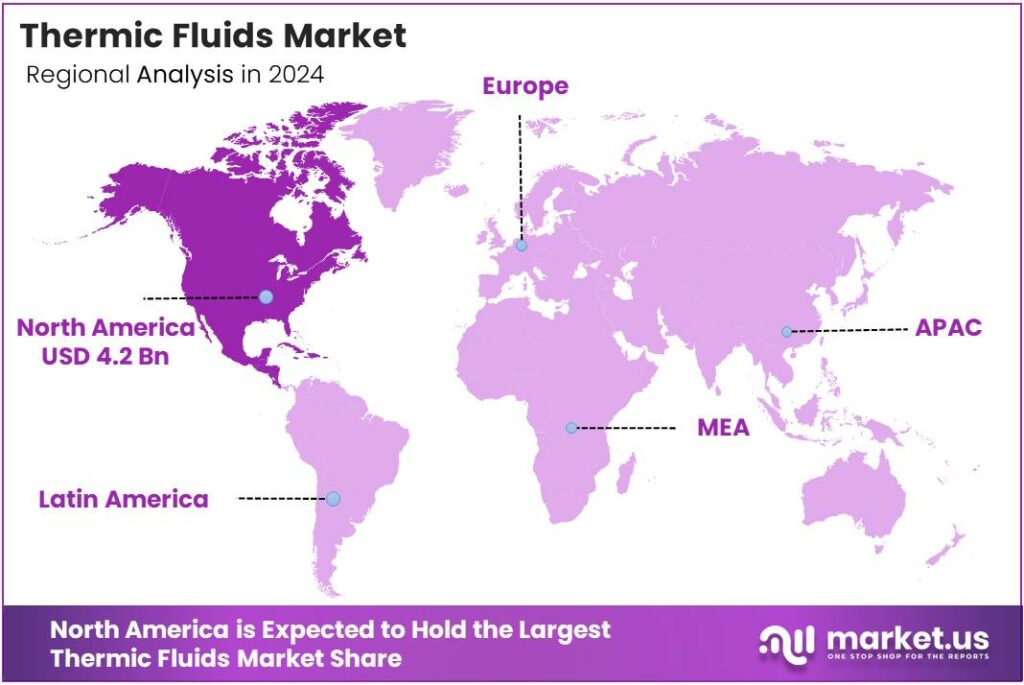

- North America dominates the regional landscape with a 36.4% market share, valued at USD 4.2 billion in 2025.

By Grade Analysis

Medium Temperature fluids dominate with 56.8% due to broad industrial applicability across chemical, pharmaceutical, and food processing sectors.

In 2025, Medium Temperature thermic fluids held a dominant market position in the By Grade segment of the Thermic Fluids Market, with a 56.8% share. These fluids serve the widest range of industrial applications, from chemical reactors to food processing lines. Their balance of thermal stability, cost efficiency, and compatibility with standard equipment makes them the preferred choice for most process industries.

Low-temperature thermic fluids serve cryogenic and cold-chain applications, including LNG storage and refrigeration systems. These solutions address growing demand in specialty industries where sub-zero temperature control is essential. Additionally, expansion of cold-chain logistics infrastructure across emerging markets creates new uptake opportunities for low-temperature heat transfer solutions.

High-temperature fluids cater to energy-intensive industries such as concentrated solar power, glass manufacturing, and petrochemical refining. These formulations withstand extreme thermal stress over extended cycles without degradation. Consequently, they command premium pricing and are gaining traction as industrial processes shift toward higher operating temperatures for efficiency gains.

By Product Type Analysis

Mineral Oils dominate with 45.1% due to wide availability, lower cost, and established use in conventional industrial heating systems.

In 2025, Mineral Oils held a dominant market position in the By Product Type segment of the Thermic Fluids Market, with a 45.1% share. Their cost advantage and widespread compatibility with existing industrial systems drive continued adoption. Moreover, well-established supply chains and easy sourcing make mineral oils the go-to choice for price-sensitive end-users in manufacturing and process industries.

Silicone-based thermic fluids offer exceptional thermal stability across wide temperature ranges and resist oxidation better than mineral alternatives. These properties make them suitable for high-precision applications in electronics, pharmaceuticals, and specialty chemicals. However, their higher cost limits adoption to industries where performance requirements justify the premium investment.

Aromatic thermic fluids, including diphenyl-diphenyl oxide blends, deliver high-temperature performance for applications such as chemical synthesis and concentrated solar power. These fluids operate reliably at temperatures exceeding 400°C, making them essential for advanced industrial processes. Additionally, Glycol-based fluids and other specialty formulations address niche cooling and food-grade heating applications across diverse industries.

By Application Analysis

Heating dominates with 46.9% due to its widespread use across chemical processing, food production, and oil refining operations.

In 2025, Heating held a dominant market position in the By Application segment of the Thermic Fluids Market, with a 46.9% share. Industrial heating processes across chemicals, textiles, and food manufacturing depend heavily on thermic fluid systems for uniform and controlled heat delivery. This broad demand base sustains the segment’s leading position across geographies.

Cooling applications represent a fast-growing segment driven by expansion in data centers, electronics manufacturing, and battery thermal management. Immersion and indirect cooling systems increasingly rely on high-performance thermic fluids to dissipate heat efficiently. Consequently, the rising deployment of high-performance computing infrastructure accelerates demand for specialized cooling fluids.

Sterilization, Pollution Control, and other applications collectively address specialized industrial needs. Sterilization systems in pharmaceutical and food processing plants use thermic fluids to achieve precise and repeatable temperature cycles. Moreover, pollution control equipment, such as thermal oxidizers, relies on heat transfer fluids to maintain consistent operating temperatures for effective emissions treatment.

By End-use Analysis

Oil and gas dominate with 38.5% due to the extensive use of heat transfer fluids across refining, processing, and pipeline heating systems.

In 2025, Oil and Gas held a dominant market position in the By End-use segment of the Thermic Fluids Market, with a 38.5% share. Refineries and petrochemical plants require precise temperature control for distillation, cracking, and separation processes. Consequently, this sector generates the highest volume demand for high-temperature and thermally stable heat transfer fluid formulations.

The Chemicals segment ranks as the second-largest end-use category, driven by the need for accurate thermal management in batch and continuous chemical reactions. Specialty chemical plants operating with complex multi-step synthesis processes rely on thermic fluid systems to maintain uniform temperatures. Additionally, rapid capacity expansion of chemical parks in the Asia-Pacific supports growing fluid consumption in this segment.

Pharmaceuticals and Food and beverage industries demand food-grade and NSF-certified thermic fluids for compliance with hygiene and safety standards. Pharmaceutical manufacturing requires validated thermal processes, while food plants need fluids that pose no contamination risk. Furthermore, Other end-use sectors such as textiles, plastics, and renewable energy contribute incremental volume to the overall thermic fluids market.

Key Market Segments

By Grade

- Low Temperature

- Medium Temperature

- High Temperature

By Product Type

- Mineral Oils

- Silicone

- Aromatic

- Glycol

- Others

By Application

- Heating

- Cooling

- Sterilization

- Pollution Control

- Others

By End-use

- Oil and Gas

- Chemicals

- Pharmaceuticals

- Food and Beverages

- Others

Emerging Trends

Shift Toward High-Performance Fluids and Digital Lifecycle Management Reshapes the Thermic Fluids Market

Nanoparticle-enhanced thermic fluids represent a significant innovation trend gaining traction in research and industrial trials. Manufacturers incorporate nanoparticles into base fluids to improve thermal conductivity and heat transfer efficiency. Consequently, these next-generation formulations attract interest from high-precision sectors such as electronics cooling and concentrated solar power installations.

- Industrial operators accelerate the transition from conventional mineral oils to high-performance glycol and silicone blends. These advanced formulations deliver superior thermal stability and broader operating temperature ranges. Moreover, the top 10 heat transfer fluid exporters account for 35% of total shipment weight, reflecting growing consolidation around high-grade suppliers.

Predictive analytics and lifecycle management services increasingly extend fluid service life and reduce unplanned downtime. Thermic fluid suppliers now offer digital monitoring platforms that track fluid degradation in real time. Additionally, low-temperature thermic solutions expand into LNG cryogenic storage and cold-chain logistics, opening new application areas beyond traditional industrial heating.

Drivers

Rising Industrial Demand and Renewable Energy Expansion Drive Thermic Fluids Market Growth

Concentrated solar power plants accelerate thermic fluid adoption for thermal energy storage and steam generation. Governments in Europe, the Middle East, and Asia invest heavily in CSP infrastructure as part of clean energy transitions. Consequently, advanced thermal storage media with high operating temperatures and long service cycles become critical inputs for renewable power projects.

- Oil and gas refineries drive the largest share of thermic fluid consumption globally. Complex high-temperature refining and separation processes require thermally stable fluids that maintain performance under extreme conditions. Dow Packaging and Specialty Plastics segment recorded net sales of USD 21,776 million in 2024, illustrating how downstream processing demand sustains volumes across heat transfer fluid value chains.

Chemical and petrochemical complex expansion creates sustained demand for precise temperature control systems. Rapid industrialization in the Asia-Pacific and the Middle East drives new plant capacity that requires thermic fluid systems from commissioning. Furthermore, high-performance data centers increasingly adopt immersion cooling fluids, adding a new and fast-growing demand vector to the broader market.

Restraints

Feedstock Price Volatility and High Maintenance Costs Restrain Thermic Fluids Market Expansion

Persistent volatility in petrochemical feedstock prices creates cost instability for thermic fluid manufacturers. Raw material costs for mineral oil and aromatic base stocks fluctuate with crude oil price cycles, directly squeezing production margins. Moreover, price unpredictability makes long-term contract pricing difficult, reducing confidence among buyers planning large-scale system investments.

Periodic fluid replacement, system flushing, and maintenance programs add substantial lifecycle costs for end-users. Industrial operators must budget for scheduled fluid analysis, disposal of degraded fluids, and cleaning of heat exchanger circuits. Consequently, the total cost of ownership for thermic fluid systems often exceeds initial purchase price expectations, slowing adoption in cost-sensitive industries.

Smaller enterprises and emerging-market operators face particular difficulty absorbing these elevated maintenance burdens. Limited technical expertise and a lack of on-site fluid monitoring capabilities increase the risk of premature fluid degradation. Therefore, the high operational discipline required for effective thermic fluid management acts as a barrier for industries with limited maintenance infrastructure.

Growth Factors

Synthetic Fluid Innovation and Asia-Pacific Infrastructure Boom Create Strong Market Growth Opportunities

NSF HT-1 certified food-grade thermic fluids penetrate processed food and pharmaceutical production lines, opening high-value niche segments. Regulatory pressure for safe and traceable thermal management in consumable-product facilities drives adoption of certified formulations.

- Manufacturers develop application-specific synthetic formulations tailored for electric vehicle battery cooling and electronics thermal management. These custom blends address the unique heat load profiles and safety requirements of EV powertrain systems. BASF’s group’s total sales reached €65.3 billion in 2024, underscoring major chemical players’ continued investment in specialty performance fluids and thermal management chemistries.

Development of bio-based and low-toxicity thermic fluid alternatives addresses decarbonization goals and REACH compliance requirements. Chemical producers reformulate product portfolios to replace high-aromatic and petroleum-derived fluids with greener options. Additionally, infrastructure growth across Asia-Pacific and the Middle East enables new industrial heating projects that create sustained long-term demand for diverse thermic fluid categories.

Regional Analysis

North America Dominates the Thermic Fluids Market with a Market Share of 36.4%, Valued at USD 4.2 Billion

North America leads the global thermic fluids market, holding a 36.4% share valued at USD 4.2 billion in 2025. The region’s dominance reflects its large oil and gas refining capacity, mature chemical processing industry, and widespread deployment of concentrated solar power projects. Moreover, strict environmental standards encourage the adoption of high-performance and low-toxicity fluid formulations across U.S. and Canadian industrial facilities.

Europe ranks as the second-largest thermic fluids market, driven by stringent REACH regulations and an active renewable energy agenda. Germany, France, and the UK operate large chemical and pharmaceutical manufacturing bases that consume significant volumes of specialty heat transfer fluids. Additionally, European CSP installations and district heating networks increasingly adopt advanced synthetic thermic fluids for improved efficiency and compliance.

Asia Pacific represents the fastest-growing region for thermic fluids, supported by rapid industrialization across China, India, and Southeast Asia. Expanding chemical parks, pharmaceutical clusters, and food processing facilities generate strong incremental demand. Furthermore, government-backed infrastructure investments and growing adoption of energy-efficient thermal systems accelerate fluid consumption across the region’s diverse industrial base.

The Middle East and Africa region benefits from large-scale oil refining capacity and growing investment in CSP and industrial infrastructure. GCC countries drive demand through petrochemical complex expansion and solar energy projects requiring high-temperature thermal fluids. Consequently, increasing local manufacturing activity and new industrial zones in Saudi Arabia and the UAE support market growth across the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Eastman Chemical Company holds a leading position in the global thermic fluids market through its Therminol brand of synthetic heat transfer fluids. The company serves specialty chemicals, renewables, and industrial processing sectors with formulations that emphasize thermal stability and closed-loop efficiency. Reflecting strong demand across performance fluids and specialty materials applications.

ExxonMobil competes in the thermic fluids market through its Mobiltherm series of paraffinic and mineral oil-based heat transfer fluids. These products serve closed indirect heating and cooling systems across industrial and marine environments. The company’s global distribution network and refining expertise allow it to supply a broad range of viscosity grades and thermal performance specifications to industrial customers worldwide.

Huntsman Corporation participates in the thermic fluids sector through its specialty chemicals and performance products divisions. The company develops aromatic and specialty base fluid formulations used in high-temperature industrial applications. Huntsman’s integrated chemical manufacturing capabilities allow it to optimize fluid performance characteristics and respond to evolving industrial customer requirements across diverse global markets.

Parathem Corporation focuses on specialty thermic fluid formulations designed for high-temperature and niche industrial applications. The company serves process industries requiring reliable and consistent heat transfer performance across demanding operating conditions. Its targeted product portfolio and technical service capabilities position it as a preferred supplier for customers seeking application-specific thermal management solutions beyond commodity mineral oil products.

Top Key Players in the Market

- Eastman Chemical Company

- ExxonMobil

- Huntsman Corporation

- Parathem Corporation

- Royal Dutch Shell

- Clariant AG

- British Petroleum Plc

- HPCL

- Thermic Fluids Pvt. Ltd.

Recent Developments

- In 2025, Eastman Chemical Company maintains a leading position in the thermic (heat transfer) fluids sector through its Therminol brand of synthetic heat transfer fluids, used for indirect process heating/cooling in industries like specialty chemicals, renewables, and more. These fluids emphasize thermal stability, low maintenance, broad temperature ranges, and closed-loop operation to minimize environmental impact.

- In 2025, ExxonMobil offers the Mobiltherm series of paraffinic/mineral oil-based heat transfer fluids for closed indirect heating/cooling systems in industrial and marine applications, focusing on thermal efficiency, oxidation stability, and pumpability.

Report Scope

Report Features Description Market Value (2024) USD 11.5 Billion Forecast Revenue (2034) USD 16.9 Billion CAGR (2025-2034) 3.9% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Grade (Low Temperature, Medium Temperature, High Temperature), By Product Type (Mineral Oils, Silicone, Aromatic, Glycol, Others), By Application (Heating, Cooling, Sterilization, Pollution Control, Others), By End-use (Oil and Gas, Chemicals, Pharmaceuticals, Food and Beverages, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Eastman Chemical Company, ExxonMobil, Huntsman Corporation, Parathem Corporation, Royal Dutch Shell, Clariant AG, British Petroleum Plc, HPCL, Thermic Fluids Pvt. Ltd. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Eastman Chemical Company

- ExxonMobil

- Huntsman Corporation

- Parathem Corporation

- Royal Dutch Shell

- Clariant AG

- British Petroleum Plc

- HPCL

- Thermic Fluids Pvt. Ltd.

Our Clients

- 179082

- February 2026