Quick Navigation

Report Overview

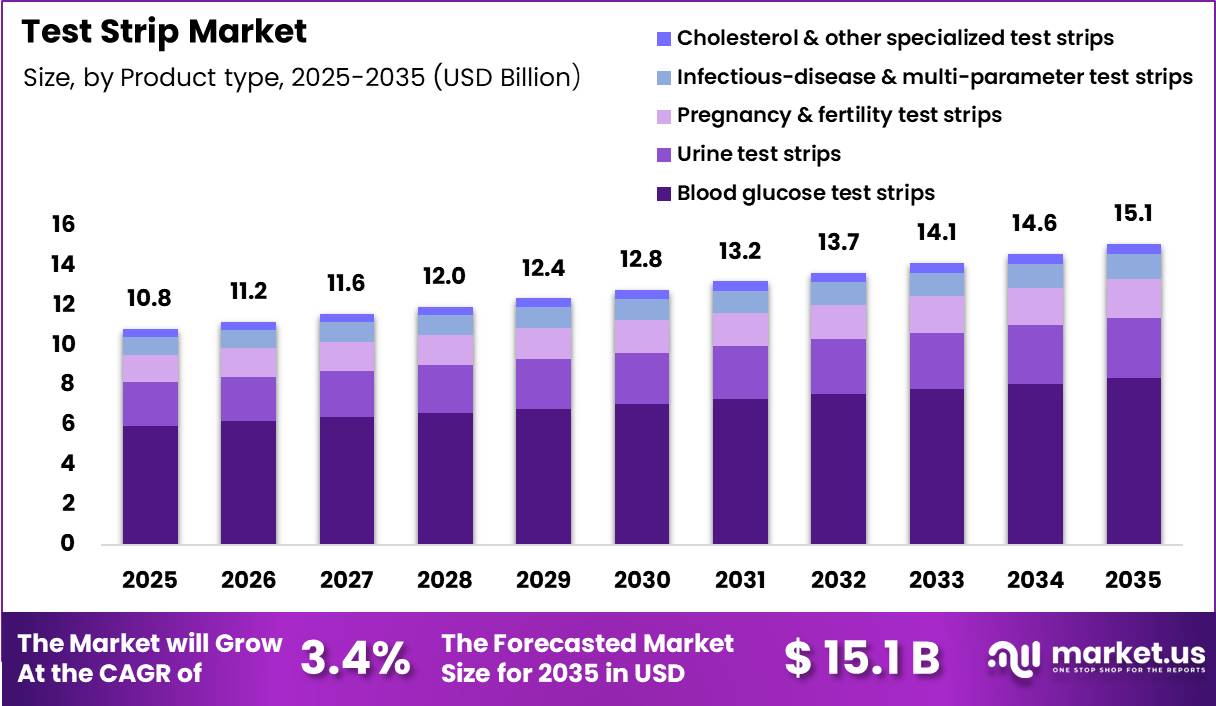

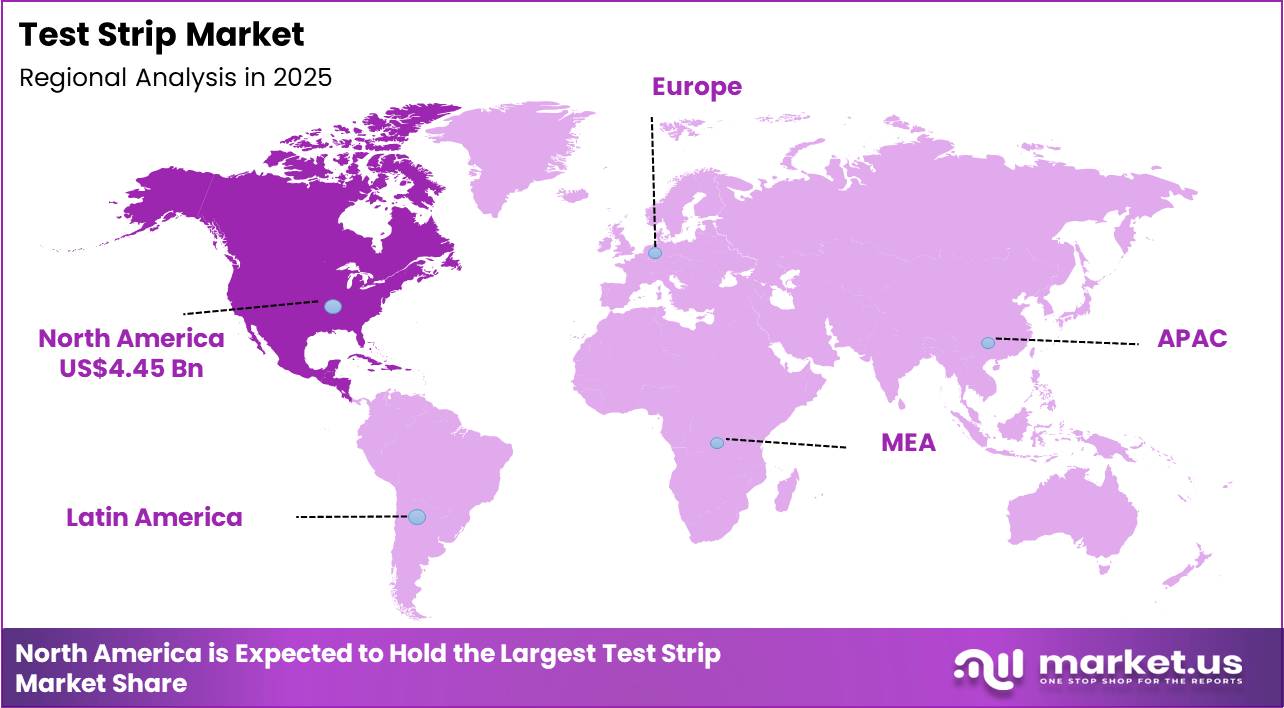

Global Test Strip Market size is expected to be worth around US$ 15.1 Billion by 2035 from US$ 10.8 Billion in 2025, growing at a CAGR of 3.4% during the forecast period from 2026 to 2035. North America held a dominant market position, capturing more than a 41.8% share, holding USD 183.2 million in revenue.

The Global Test Strip market is an important part of the in-vitro diagnostics industry. This is because many people are getting sick with long term diseases and there is a big push for people to take care of themselves at home. According to a study that the World Health Organization supported the number of adults with diabetes has gone up a lot. In fact it is now over 800 million people. That’s more than four times what it was in 1990.

The World Health Organization says that the number of people with diabetes has gone from 7% to 14% between 1990 and 2022. As of 2022 450 million adults who are 30 years old or more do not get the treatment they need. The World Health Organization says that 90 % of these people live in countries that are not very rich.

The International Diabetes Federation thinks that by 2024 more people with diabetes will live in cities than in the country. They say that 12.7% of people in cities have diabetes but 8.8 % of people, in the country have it. These trends are making people want to buy test strips and other tools that they can use to take care of themselves at home. This report looks at how the test strip market’s divided up what is happening in different parts of the world who the big players are, what is driving growth what the challenges are and what new opportunities are coming up in the global test strip market.

Key Takeaways

- Market Size: Global Test Strip Market size is expected to be worth around US$ 15.1 Billion by 2035 from US$ 10.8 Billion in 2025.

- Market Share: The market is growing at a CAGR of 3.4% during the forecast period from 2026 to 2035.

- Product Type Analysis: Blood glucose test strips make up 55.3% of the test strip market.

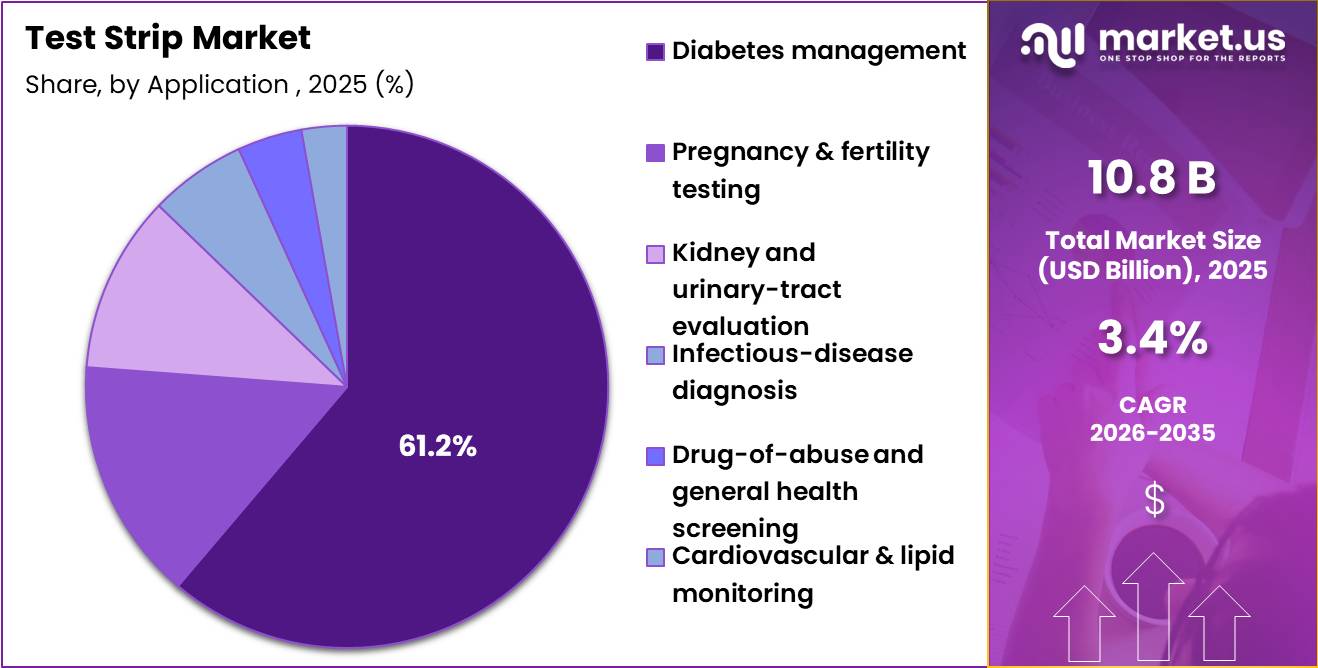

- Application Analysis: Management of diabetes is currently the leading application sector of test strips, contributing to 61.2% of the market.

- Distribution channel Analysis: The retail pharmacy channel accounts for 35.2% of all test strips sold globally.

- Technology Analysis: Electrochemical test strips dominates the market at 60.8%, attributed to their superior precision, reliability, and convenience in self-monitoring blood glucose (SMBG).

- End Use Analysis: Hospital and clinic segment has a market share of 35.1% due to large number of patients in hospitals and protocols in place within the healthcare sector to perform routine tests on them.

- Regional Analysis: North America held a dominant market position, capturing more than a 41.8% share, holding USD 183.2 million in revenue.

Product Type Analysis

Blood Glucose Test Strips Represent the Dominant Segment in the Global Test Strip Market

Blood glucose test strips make up 55.3% of the test strip market. This is because more and more people around the world are getting diabetes. According to the International Diabetes Federation Diabetes Atlas 2025 about 589 million adults have diabetes. That is one in nine people. Experts think this number will go up to 853 million by 2050.As per the International Diabetes Federation report in 2021 43 % of adults, with diabetes do not know they have it. Most of these people 90 % of them live in countries that are not very rich.

Urine test strips are growing fast. Urine test strips currently have a 20.1 % share. This is happening because more people are getting tract infections or UTIs.

- A study called Global Burden of Disease (GBD) Study 2021 says that UTIs will keep getting more common through 2050.

Application Analysis

Diabetes management a significant type.

Management of diabetes is currently the leading application sector of test strips, contributing to 61.2% of the market. Based on the data provided by the IDF, there were approximately 537 million diabetic adults across the world, most of whom needed self-monitoring of blood glucose for insulin treatment and glucose level management (IDF, 2021).

Blood glucose test strips find widespread use among patients diagnosed with either type 1 or type 2 diabetes. As reported by health departments like the CDC in the U.S., there are approximately 37 million cases of diabetes in the country, making the market for self-monitoring products more robust. Increasing screening tests conducted by governments further emphasize the leading position of this application sector up to 2026–2035.

Kidney and Urinary-Tract checks are becoming more popular fast. This area is growing because governments, around the world are focusing on keeping kidneys healthy. The World Health Organization made a resolution in 2024 WHA77.5 that asks countries to take care of people’s kidneys. They want countries to control things that can cause kidney problems so people do not get very sick.

Distribution Channel Analysis

Retail pharmacies are the most widely used Channels.

The retail pharmacy channel accounts for 35.2% of all test strips sold globally and continues to be consumers’ preferred method of access due to wide geographical availability and consumer trust in physical dispensing.

According to WHO, at least 1 in 10 medications in low and middle-income countries is either substandard or falsified, leading consumers to prefer regulated retail pharmacies to purchase diagnostic devices.

The online pharmacy channel accounts for 20.1% of sales and is expanding quickly based on increased adoption of digital health services. World Health Assembly resolution WHA76.5 (2023) explicitly mentions self-testing and access to testing at the community level as key focuses, driving demand in digital channels.

Technology Analysis

Electrochemical test strips Held a Major Share of the global test strip Market.

Electrochemical test strips dominates the market at 60.8%, attributed to their superior precision, reliability, and convenience in self-monitoring blood glucose (SMBG). These products have been identified as essential by the WHO list of Essential in Vitro Diagnostics, with personal glucose meter devices proving vital in diabetes management, backed by governmental healthcare programs in countries such as the U.S., India, and China. The portable, affordable nature of these products combined with their digital health system compatibility has ensured their market leadership.

Lateral Flow Assay Test Strips Are the most rapidly growing segment (16%), lateral flow assay test strips have witnessed significant growth in light of the rising infectious disease burden around the world. WHO reports that in 2023, tuberculosis accounted for nearly 8.2 million new infections, whereas dengue infection was reported at over 7.6 million in April 2024.

End Use Analysis

Test strip are mostly utilized in the Hospital and clinic.

Hospital and clinic segment has a market share of 35.1% due to large number of patients in hospitals and protocols in place within the healthcare sector to perform routine tests on them. WHO-sponsored studies estimate that, in 2022, 445 million adults aged 30 years or more with diabetes—constituting 59% of this age group were not undergoing any treatment for their condition, with the proportion of un-diagnosed cases constituting 84 to 97% of the total cases of diabetes that remained untreated.

The home-care segment holds a market share of 30% and is witnessing rapid growth, which can be attributed to the supportive role of WHO policies promoting self-testing. The prevalence rate of un-diagnosed diabetes to be 42.8%, with 251.7 million adults suffering from the condition and remaining undiagnosed in 215 countries around the globe.

Key Market Segments

By Product type

- Blood glucose test strips

- Urine test strips

- Pregnancy & fertility test strips

- Infectious‑disease & multi‑parameter test strips

- Cholesterol & other specialized test strips

By Application

- Diabetes management

- Pregnancy & fertility testing

- Kidney and urinary‑tract evaluation

- Infectious‑disease diagnosis

- Drug‑of‑abuse and general health screening

- Cardiovascular & lipid monitoring

By Technology

- Electrochemical test strips

- Lateral‑flow assay (LFA) test strips

- Optical / colorimetric test strips

- Biosensor‑enhanced

- Others

By Distribution Channel

- Retail pharmacies

- Hospital pharmacies

- Online pharmacies

- Direct institutional / tenders

By End Use

- Hospitals & clinics

- Home-care / self-testing users

- Diagnostic laboratories

- Pharmacies & retail clinics

- Research institutes & others

Driver

Diabetes burden expansion lifting recurring strip demand

The strongest structural driver remains the expanding diabetes population, because test strips monetize through repeat consumption rather than one-time device placement. The International Diabetes Federation reports about 590 million people living with diabetes globally in 2026, while WHO states more than 830 million people worldwide have diabetes, with the majority in low- and middle-income countries; even allowing for methodology differences, both sources point to a very large and still-growing addressable monitoring base.

In the U.S., CDC materials indicate more than 40 million Americans have diabetes, while national statistics show 11.0 million adults are still undiagnosed, which means the diagnosed base that regularly consumes strips can continue expanding as case finding improves.

For suppliers, this driver supports stable reorder economics in blood glucose strips, plus follow-on demand for lancets, meters, and control solutions; commercially, it favors installed-base strategies, pharmacy channel depth, and lower-cost strip chemistry optimized for high-frequency use in type 2 care pathways, especially in countries where CGM penetration remains constrained by cost or reimbursement.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Diabetes burden expansion lifting recurring strip demand | +2.4% | North America core, EU, China, India, Middle East, Latin America urban centers | Medium term (2-4 years) |

| Large undiagnosed and prediabetes pools widening screening volumes | +1.6% | U.S. core, EU primary care, APAC metros, Gulf states | Short term (≤ 2 years) |

| Reimbursement support preserving SMBG strip utilization despite CGM growth | +1.8% | U.S., Western Europe, Japan, Australia | Short term (≤ 2 years) |

| Ketone and pregnancy monitoring sustaining premium strip subsegments | +1.1% | U.S., UK, EU, Japan, urban APAC | Medium term (2-4 years) |

| Retail self-testing and home-based care improving access velocity | +1.3% | North America, EU, India, Southeast Asia, Latin America | Short term (≤ 2 years) |

| Prescription rationalization and compatible-meter switching reshaping volume mix | +0.9% | UK, EU tender markets, selected Asia public systems | Medium term (2-4 years) |

Challenge

Reimbursement-driven erosion of high-quality strip demand

Test strips are not being blocked from sale, but the economic quality of demand is deteriorating because payer formularies increasingly narrow preferred brands, restrict monthly strip volumes, and reserve fuller coverage for insulin-intensive populations, which compresses realized revenue per active user even when shipment volumes stay stable.

Public and managed-care supply policies already show utilization caps in CGM-linked settings, and this matters in a category where a 5% to 8% annual ASP decline, a 10% to 20% rebate spread between preferred and non-preferred SKUs, and claim rejection or step-edit friction that can delay refill conversion by 7 to 21 days can cumulatively shave about 1.1% points from addressable growth versus a friction-free adoption path.

Companies therefore need multi-tier portfolio architecture, lower-cost private-label defense, tighter tender analytics, and country-specific health-economic dossiers that justify strip frequency by patient cohort rather than relying on broad-based reimbursement persistence.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Reimbursement mix erosion | -1.1% | North America core, EU reimbursement markets, Japan | Medium term (2-4 years) |

| CGM substitution asymmetry | -1.4% | US private plans, Western Europe, urban APAC | Medium term (2-4 years) |

| Accuracy-compliance burden | -0.9% | EU regulatory hubs, US quality systems, GCC tenders | Short term (≤ 2 years) |

| Enzyme material volatility | -0.8% | APAC manufacturing clusters, EU import channels, LATAM distributors | Medium term (2-4 years) |

| Channel inventory distortion | -0.7% | US retail chains, EU pharmacy networks, emerging-market wholesalers | Short term (≤ 2 years) |

| Skilled ops talent gap | -0.6% | US and EU plants, Singapore/Malaysia hubs, India scale-up corridors | Long term (≥ 4 years) |

Restraints

Regulatory tightening under IVDR reshapes EU test strip commercialization

The enforcement of the EU In Vitro Diagnostic Regulation (IVDR 2017/746) from May 2022 onward materially raises the regulatory bar for glucose, urinalysis, and multi-analyte test strips by reclassifying a significant share of self-testing products into higher risk classes, increasing notified body involvement and requiring more robust clinical performance and post-market surveillance, which collectively extend average EU route-to-market timelines from roughly 12–18 months under the former IVDD to 24–36 months for many products and increase direct regulatory and compliance costs by an estimated 30–50 percent per SKU.

Besides the one-off cost of new technical documentation and clinical evidence packages which can add 0.5–1.0% points to COGS for low-priced strips selling at 0.20–0.40 dollars per unit, the more severe commercial impact comes from portfolio rationalization and delayed launches, with several mid-tier Asian and U.S. OEMs choosing to withdraw niche strip variants rather than invest in re-certification, effectively shrinking the competitive set in some EU sub-segments and creating mid-single-digit volume gaps for distributors over 2023–2025.

For global manufacturers exporting into the EU, IVDR-linked reallocation of quality, regulatory, and clinical resources is crowding out pipeline capacity for other regions, pushing back CE-based approvals that previously supported quicker registrations in the Middle East, Africa, and parts of Latin America by 12–24 months and creating stranded tooling and CapEx in plants configured for SKUs whose EU demand profiles are now uncertain.

Strategically, this regime compresses margins by 100–200 basis points on EU volumes as list price increases are partially offset by tighter hospital tenders and payer contracts, drives higher minimum efficient scale per assay family (forcing consolidation of low-volume SKUs), and compels manufacturers to front-load 3–5 million dollars equivalent in regulatory transformation projects over 2–3 years, delaying ROI on new strip lines and constraining capital deployment for capacity expansion in higher-growth emerging markets.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IVDR and tightening IVD approvals | -2.2% | EU, U.K., EEA exporters | Medium term (2–4 years) |

| Enzyme and nitrocellulose input volatility | -1.9% | North America, EU, APAC corridors | Short–Medium term (≤ 4 years) |

| Price caps and reimbursement pressure | -1.7% | EU, India, LATAM public payers | Medium–Long term (≥ 3 years) |

| Shift to CGM and sensor-based monitoring | -2.5% | North America core, developed APAC, EU | Long term (≥ 4 years) |

| Working capital squeeze for local manufacturers | -1.3% | Africa, South Asia, SEA LMICs | Short–Medium term (≤ 4 years) |

| Environmental and waste-handling compliance | -0.8% | OECD markets, China coastal | Medium term (2–4 years) |

Opportunity

Build women’s self-care strip ecosystems

Women’s self-care strip platforms represent future upside because the strategic monetization path is no longer the standalone pregnancy strip, which is mature, but a multi use, app linked, lifecycle portfolio covering fertility, pregnancy, gestational glucose support, and pharmacy led reproductive self-care that captures repeat purchases across multiple care episodes.

WHO explicitly recognizes self care diagnostics such as pregnancy self tests and self monitoring during pregnancy, which creates policy legitimacy for broader retail and pharmacy distribution, especially in markets where formal women’s health access remains uneven and privacy led demand is structurally under-served.

The upside comes from converting low frequency single product buyers into 3 to 5 product category users per reproductive cycle through ovulation, pregnancy confirmation, urinary health, and maternal glucose bundles, lifting annual revenue per consumer by an estimated 2.2x to 3.0x and creating cross sell economics that can expand EBITDA margins by 400 to 700 basis points relative to single SKU retail strategies, with the strongest whitespace in India, Southeast Asia, Latin America, and Africa where pharmacy access scales faster than clinic infrastructure.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| CKD screening strip expansion | +1.8% | North America core, EU, GCC, urban APAC | Short term (≤ 2 years) |

| Women’s self-care strip platforms | +1.4% | India, SEA, LATAM, Africa, US retail | Short term (≤ 2 years) |

| Infection triage at primary care | +2.1% | EU, India, Africa, LATAM | Medium term (2-4 years) |

| Hybrid strip-plus-digital care models | +1.6% | US, EU, Japan, South Korea, China urban | Medium term (2-4 years) |

| Value-tier localization roll-up | +2.4% | India, Africa, ASEAN, MENA | Medium term (2-4 years) |

| Post-glucose portfolio pivot | +1.9% | US, EU, advanced APAC | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Geopolitical Realignment and Supply Chain Fragmentation Reshaping Test strip Manufacturing.

The increasing trade tension between the US and China and the expansive tariff policies of the US are putting pressure on the international test strips market, which has the highest concentration of manufacture in China and Southeast Asia.

A national security review under Section 232 of the US Department of Commerce Bureau of Industry and Security was commenced on September 24, 2025, into medical consumables and devices imported into the United States. This could lead to tariffs being imposed by spring 2026, which will affect test strips’ importers who source their products from foreign manufacturing. White & Case LLP

Currently, there is an application of 54% duty on any medical devices and components imported from China by virtue of the US reciprocal trade measures, whereas a general 10% duty applies on all other trade partners, leading to increased costs in manufacturing test strips that require the use of products sourced from China.

Section 232 investigations include medical consumables including treatment and diagnostic devices, with China and Mexico importing about 35% of the entire US’s medical machines and devices in 2023, according to the United States International Trade Commission.

Regional Analysis

North America Held the Largest Share of the Global Battery Separator Market.

The North America segment accounts for a market leading 41.2% share of the global test strip market, based on high health care expenditures and mature testing facilities in the region. The estimated cost of diagnosed diabetes in the US expected to be $ 412.9 billion in 2022.

According to the CDC National Health and Nutrition Examination Survey (2021-2023), total diabetes prevalence in the US stands at 14.3% among adults aged 20 years or more, while it rises to a whopping 27.3% in the age group of 60 years or more.

The Asia-Pacific region represents a market share of 16.0% and is the fastest growing segment due to increasing but largely under-diagnosed diabetes prevalence. As estimated by the IDF, diabetes prevalence in South-East Asia will see a growth of 73% and reach 185 million cases by 2050, while spending on diabetes treatment remains merely $12 billion – less than 1% of global diabetes spending.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The test strip manufacturers are concentrating on innovation with regards to accuracy, compliance, and expanding into emerging markets in order to maintain competitiveness considering increasing global burden of disease.

The WHO’s Model list of essential in vitro diagnostics includes both glucose and HbA1c tests, and moreover, resolution WHA76.5 (2023) recommends that health care systems ensure availability of reliable test strips. This clearly indicates the importance of regulatory compliance as well as institutional agreements in maintaining competitiveness. IDF estimates that cases of diabetes in South-East Asia would increase by 73% up to 185 million by 2050 while accounting for just 1% of global expenditure on diabetes. This shows the need for test strips to be available in affordable and large quantities to cater to emerging markets.

Key Development:

- In January 2025, Abbott Laboratories introduced its FreeStyle Libre family of products after being granted FDA approval to sell new configurations of over-the-counter glucose strips that allowed consumers greater accessibility to self-diagnostic tools without needing prescriptions.

- In May 2025, Roche announced a USD 550 million investment in its Indianapolis diagnostics site, which currently produces approximately 5.2 billion Accu-Chek diabetes test strips annually and serves as a distribution hub for 53 countries worldwide. The expansion directly strengthens domestic test strip manufacturing capacity and supply chain resilience.

Top Key Players

- Abbott Laboratories

- Hoffmann‑La Roche Ltd (Roche Diagnostics)

- LifeScan IP Holdings (OneTouch)

- Ascensia Diabetes Care Holdings AG

- ARKRAY Inc.

- AgaMatrix Inc.

- Bionime Corporation

- Sinocare Inc.

- Trividia Health Inc.

- Ypsomed AG

- SD Biosensor Inc.

- TaiDoc Technology Corporation

- i‑SENS Inc.

- Nova Biomedical

- 77 Elektronika Kft.

- OK Biotech Co., Ltd.

- Others

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 10.8 Billion |

| Forecast Revenue (2035) | US$ 15.1 Billion |

| CAGR (2026-2035) | 3.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product type (Blood glucose test strips, Urine test strips, Pregnancy & fertility test strips, Infectious‑disease & multi‑parameter test strips, Cholesterol & other specialized test strips), By Application (Diabetes management, Pregnancy & fertility testing, Kidney and urinary‑tract evaluation, Infectious‑disease diagnosis, Drug‑of‑abuse and general health screening, Cardiovascular & lipid monitoring), By Technology (Electrochemical test strips, Lateral‑flow assay (LFA) test strips, Optical / colorimetric test strips ,Biosensor‑enhanced, Others), By Distribution channel (Retail pharmacies, Hospital pharmacies, Online pharmacies, Direct institutional / tenders), By End Use (Hospitals & clinics, Home‑care/self‑testing users, Diagnostic laboratories, Pharmacies & retail clinics, Research institutes & others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Abbott Laboratories, F. Hoffmann‑La Roche Ltd (Roche Diagnostics), LifeScan IP Holdings (OneTouch) ,Ascensia Diabetes Care Holdings AG ,ARKRAY Inc., AgaMatrix Inc., Bionime Corporation, Sinocare Inc., Trividia Health Inc., Ypsomed AG, SD Biosensor Inc., TaiDoc Technology Corporation, i‑SENS Inc. Nova Biomedical, 77 Elektronika Kft., OK Biotech Co., Ltd., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |