Quick Navigation

Report Overview

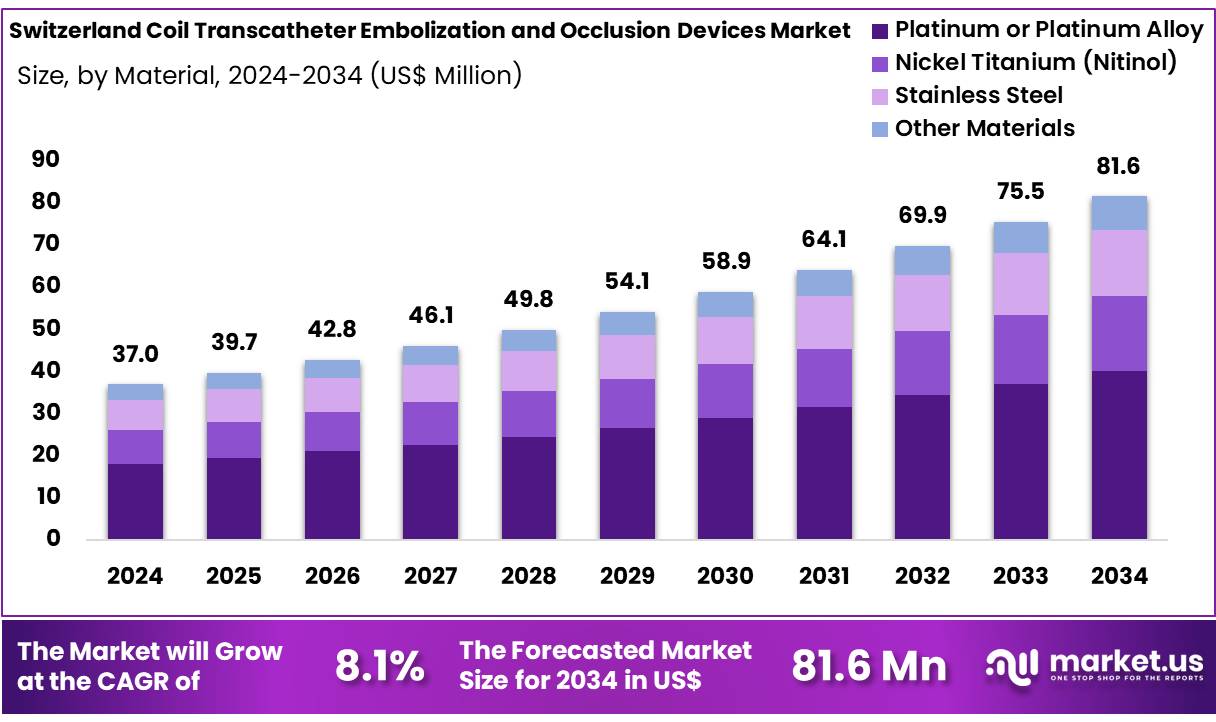

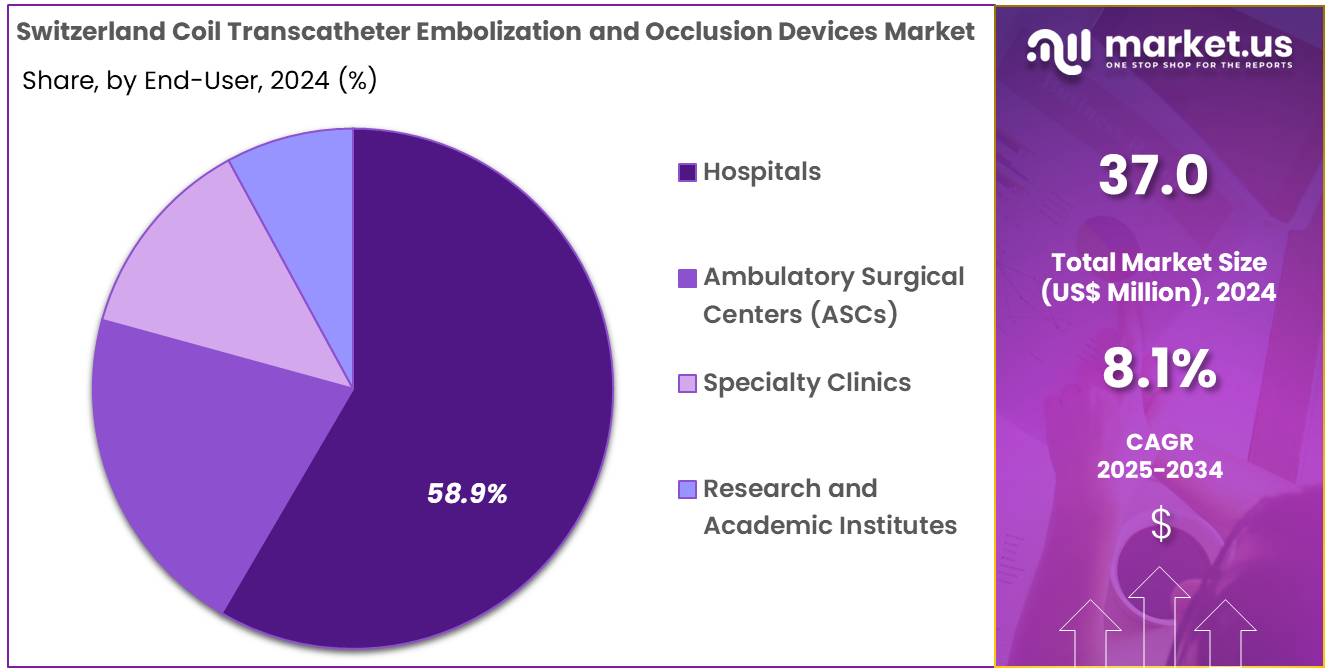

The Switzerland Coil Transcatheter Embolization and Occlusion Devices Market size is expected to be worth around US$ 81.6 Million by 2034 from US$ 37.0 Million in 2024, growing at a CAGR of 8.1% during the forecast period from 2025 to 2034.

Switzerland Coil Transcatheter Embolization and Occlusion Devices, 2020-2024 (US$ Million)

| Switzerland | 2020 | 2021 | 2022 | 2023 | 2024 | CAGR |

|---|---|---|---|---|---|---|

| Revenue | 29.9 | 31.1 | 32.6 | 34.6 | 37.0 | 8.1% |

Transcatheter embolization is a minimally invasive medical procedure in which a catheter is guided through blood vessels to reach a target area. Once in position, embolic materials such as coils, vascular plugs, amplatzer devices, balloons, flow diverters and closure devices are delivered through the catheter to block or reduce blood flow within a specific blood vessel or vascular structure. This technique is used to treat conditions such as aneurysms, arteriovenous malformations, and bleeding vessels by causing vessel occlusion and promoting clot formation.

The first coil technology was developed in the 1970s. In the beginning, they were devices like stripped guidewires, which could only treat large vessels or aneurysms and were difficult to deploy precisely. The first transarterial coil embolization carried out by Dr. Josef Rosch, who successfully embolized the artery of the gastroepiploic bleeding an individual suffering from chronic coagulopathy and liver failure.

They are designed to occlude or block blood vessels, either for therapeutic purposes or to prevent abnormal blood flow. This technology has significantly improved patient outcomes and reduced the need for invasive surgical procedures. It involve the placement of embolization coils into blood vessels or abnormal vascular structures to block blood flow, promoting the formation of blood clots, and ultimately treating or managing the underlying medical conditions. The minimal chances of danger and high success rate of procedures involving coil transcatheter embolization encourages the individuals to opt for these procedures.

- According to study published in March 2021 by National Library of Medicine, the percutaneous transcatheter embolization for pulmonary arteriovenous malformations has reported a 100% immediate technical success rate.

Key Takeaways

- The Switzerland coil transcatheter embolization and occlusion devices market was valued at USD 37.0 million in 2024 and is anticipated to register substantial growth of USD 81.6 million by 2034, with 8.1% CAGR.

- In 2024, the detachable coils segment took the lead in the global market, securing 53.2% of the total revenue share.

- The hemorrhage control segment took the lead in the global market, securing 26.9% of the total revenue share.

- The platinum or platinum alloy segment took the lead in the global market, securing 40.9% of the total revenue share.

- The hospitals segment took the lead in the global market, securing 58.9% of the total revenue share.

Product Type Analysis

Based on product type the market is fragmented into detachable coils, pushable coils, and other product types. Amongst these, detachable coils segment dominated the Switzerland coil transcatheter embolization and occlusion devices market capturing a significant market share of 53.2% in 2024. The detachable coils segment dominates the Switzerland coil transcatheter embolization and occlusion devices market, capturing a significant market share due to its high precision, safety, and effectiveness in embolization procedures.

These coils are widely used in treating aneurysms, vascular malformations, and tumors, offering controlled deployment and repositioning before detachment, reducing procedural risks. Their flexibility and compatibility with advanced imaging technologies enhance procedural accuracy, making them the preferred choice among interventional radiologists and neurosurgeons.

Technological advancements, such as bioactive coatings and hydrogel-based coils, further enhance their efficiency by promoting faster occlusion and long-term stability. Increasing prevalence of neurovascular disorders, along with growing adoption of minimally invasive procedures, continues to drive demand. Additionally, rising healthcare investments and favorable reimbursement policies support market expansion. As a result, detachable coils remain the leading segment, with continuous innovation and product enhancements strengthening their position in the global embolization market.

Switzerland Coil Transcatheter Embolization and Occlusion Devices Market, Product Type Analysis, 2020-2024 (US$ Million)

| Product Type | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| Pushable Coils | 11.2 | 11.9 | 12.7 | 13.9 | 15.3 |

| Detachable Coils | 16.8 | 17.3 | 17.9 | 18.7 | 19.7 |

| Other Product Types | 1.9 | 1.9 | 2.0 | 2.0 | 2.0 |

Procedure Type Analysis

The market is fragmented by procedure type into hemorrhage control, vascular occlusion, aneurysm treatment, tumor embolization, and other procedure types. Hemorrhage control dominated the Switzerland coil transcatheter embolization and occlusion devices market capturing a significant market share of 26.9% in 2024. The hemorrhage control segment dominates the Switzerland coil transcatheter embolization and occlusion devices market, capturing a significant market share due to the increasing need for minimally invasive solutions for acute bleeding management.

Hemorrhage, caused by trauma, gastrointestinal bleeding, postpartum hemorrhage, and vascular abnormalities, requires rapid and effective intervention, making coil embolization a preferred treatment option. These devices provide precise vascular occlusion, reducing blood flow to the affected area while preserving surrounding tissues.

The growing incidence of trauma cases, aneurysms, and chronic liver diseases, along with advancements in catheter-based embolization techniques, has accelerated adoption. Additionally, the shift towards minimally invasive procedures due to their reduced recovery time and lower complication rates further boosts demand.

Increasing investments in interventional radiology, emergency care infrastructure, and favorable reimbursement policies contribute to market growth. As a result, hemorrhage control remains the leading application, driving continued innovation and expansion in the coil embolization market.

Switzerland Coil Transcatheter Embolization and Occlusion Devices Market, Procedure Type Analysis, 2020-2024 (US$ Million)

| Procedure Type | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| Vascular Occlusion | 5.6 | 5.9 | 6.2 | 6.6 | 7.1 |

| Aneurysm Treatment | 5.1 | 5.3 | 5.6 | 6.1 | 6.6 |

| Tumor Embolization | 7.2 | 7.5 | 7.9 | 8.4 | 9.0 |

| Hemorrhage Control | 8.3 | 8.6 | 8.9 | 9.4 | 10.0 |

| Other Procedure Types | 3.7 | 3.8 | 4.0 | 4.1 | 4.3 |

Material Analysis

The market is fragmented by material into platinum or platinum alloy, nickel titanium (nitinol), stainless steel, and other materials. Platinum or platinum alloy dominated the Switzerland coil transcatheter embolization and occlusion devices market capturing a significant market share of 40.9% in 2024. The platinum or platinum alloy segment dominates the Switzerland coil transcatheter embolization and occlusion devices market, capturing a significant market share due to its superior radiopacity, flexibility, and biocompatibility.

Platinum-based coils allow precise visualization under fluoroscopy, enabling interventional radiologists to accurately position and deploy the coils during embolization procedures. Their high durability, corrosion resistance, and excellent thrombogenic properties enhance long-term occlusion effectiveness, making them the preferred choice for treating aneurysms, vascular malformations, and hemorrhages.

Additionally, platinum alloy coils, often combined with materials like tungsten or nickel-titanium (nitinol), improve strength, elasticity, and conformability, providing better vessel wall adherence and reducing the risk of coil migration. The growing adoption of minimally invasive procedures, rising prevalence of neurovascular and peripheral vascular diseases, and continuous technological advancements in coil design further fuel demand. As a result, platinum and platinum alloy coils continue to lead the market, driving innovations in embolization therapy.

Switzerland Coil Transcatheter Embolization and Occlusion Devices Market, Material Analysis, 2020-2024 (US$ Million)

| Material | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| Platinum or Platinum Alloy | 12.4 | 13.1 | 9.3 | 14.0 | 15.1 |

| Nickel Titanium (Nitinol) | 10.9 | 11.4 | 8.4 | 12.1 | 13.0 |

| Stainless Steel | 6.3 | 6.6 | 5.2 | 6.9 | 7.2 |

| Other Materials | 1.4 | 1.5 | 1.1 | 1.6 | 1.6 |

End-User Analysis

The market is fragmented by end-user into hospitals, ambulatory surgical centers (ASCs), specialty clinics, and research and academic institutes. Hospitals dominated the Switzerland coil transcatheter embolization and occlusion devices market capturing a significant market share of 58.9% in 2024.

The hospital segment dominates the Switzerland coil transcatheter embolization and occlusion devices market, capturing a significant market share due to the high volume of complex interventional procedures performed in these settings. Hospitals are equipped with advanced imaging technologies, specialized catheterization labs, and skilled healthcare professionals, enabling efficient diagnosis and treatment of aneurysms, hemorrhages, and vascular malformations using coil embolization.

The increasing prevalence of neurovascular disorders, trauma cases, and cancer-related vascular conditions has driven the demand for minimally invasive embolization procedures, which are primarily conducted in hospitals. Additionally, hospitals benefit from higher patient inflow, improved reimbursement policies, and better access to cutting-edge embolization devices.

The integration of hybrid operating rooms and robotic-assisted procedures further enhances treatment precision. Moreover, the rising investments in healthcare infrastructure and specialized interventional radiology departments contribute to market expansion.

Switzerland Coil Transcatheter Embolization and Occlusion Devices Market, End-User Analysis, 2020-2024 (US$ Million)

| End-User | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| Hospitals | 17.3 | 18.1 | 19.1 | 20.3 | 21.8 |

| Ambulatory Surgical Centers (ASCs) | 7.3 | 7.5 | 7.8 | 8.3 | 8.9 |

| Specialty Clinics | 3 | 3.1 | 3.3 | 3.4 | 3.7 |

| Research and Academic Institutes | 2.3 | 2.4 | 2.4 | 2.5 | 2.7 |

Key Segments Analysis

Product Type

- Detachable Coils

- Pushable Coils

- Other Product Types

Procedure Type

- Hemorrhage Control

- Vascular Occlusion

- Aneurysm Treatment

- Tumor Embolization

- Other Procedure Types

Material

- Platinum or Platinum Alloy

- Nickel Titanium (Nitinol)

- Stainless Steel

- Other Materials

End-User

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Specialty Clinics

- Research and Academic Institutes

Market Dynamics

Expansion of Minimally Invasive Procedures

The shift towards minimally invasive procedures in Switzerland’s healthcare landscape is bolstering the growth of market. Patients and physicians prefer these procedures due to their ability to offer effective vascular interventions with reduced surgical risks, shorter hospital stays, and faster recoveries. As the healthcare system continues to prioritize less invasive treatment options, the demand for these devices will continue to grow.

The treatment of Abdominal Aortic Aneurysm (AAA) has been revolutionized by minimally invasive procedures. Coil transcatheter embolization may be employed during EVAR to address issues such as endoleaks, which can occur when there is persistent blood flow into the excluded aneurysm sac.

- A cohort study of observational retrospectives comprised all patients who had been who received elective endovascular aneurysm repair (EVAR) for Abdominal Aortic Aneurysm (AAA) in the period between January of 2001 until the December 2020 in a secondary treatment center located in Switzerland. Patients who had complex aneurysm repair such as fenestrated, branched or parallel grafts, were not included in the study. The study concluded that mortality rates could be decreased by conducting EVAR for the healthiest patients with AAAs of large size and the cost can be decreased by not undergoing EVAR for patients who have the greatest risk profile but less aneurysms.

These minimally invasive procedures offer benefits such as quicker recovery, reduced post-operative discomfort, and minimal scarring. Healthcare providers have invested in training and specialization to ensure safe and effective procedures, contributing to improved patient outcomes. The expansion of minimally invasive techniques aligns with cost-effective healthcare delivery, making them a prominent and transformative element of modern medical practice in Switzerland.

Market Restraints

High Cost of Devices

The high cost of coil transcatheter embolization and occlusion devices is a major factor restraining market growth. These devices, particularly detachable platinum coils, are expensive, often costing between US$500 to US$3,000 per unit, and multiple coils are required for a single procedure. This significantly increases the overall treatment cost, making it financially burdensome for hospitals, healthcare providers, and patients, especially in low- and middle-income countries with limited healthcare budgets.

Additionally, the lack of adequate reimbursement policies in several regions further limits accessibility, forcing hospitals to bear higher expenses. Smaller healthcare facilities and developing markets struggle to adopt these advanced embolization technologies due to budget constraints. High manufacturing costs, R&D investments, and stringent regulatory requirements contribute to sustained high prices. While technological advancements aim to improve cost-effectiveness, the pricing barrier remains a key challenge, restricting widespread adoption and slowing market expansion.

Market Opportunities

Growth in Medical Tourism

The growth in medical tourism is creating significant opportunities for the Switzerland coil transcatheter embolization and occlusion devices market, as patients seek cost-effective, high-quality treatments in countries with advanced healthcare infrastructure. Many developing nations, such as India, Thailand, and Mexico, offer affordable interventional procedures, including embolization treatments for aneurysms, hemorrhages, and vascular malformations, at a fraction of the cost compared to developed nations.

Medical tourism is also driven by the availability of skilled specialists, state-of-the-art medical facilities, and shorter wait times, making these countries attractive destinations for complex neurovascular and peripheral vascular procedures. Additionally, international patients benefit from comprehensive treatment packages, including hospital stays, diagnostics, and post-procedure care, further fuelling demand for advanced embolization devices.

Impact of macroeconomic factors / Geopolitical factors

The Switzerland coil transcatheter embolization and occlusion devices market is significantly influenced by macroeconomic and geopolitical factors, which impact production, pricing, supply chains, and overall market growth. Economic stability and healthcare expenditure play a crucial role in the market’s expansion, as higher healthcare budgets in developed economies drive the adoption of advanced embolization technologies. However, in developing regions with constrained healthcare funding, the high cost of embolization devices and limited reimbursement policies hinder widespread adoption.

Geopolitical factors such as trade restrictions, international conflicts, and tariffs on medical devices affect the global supply chain, leading to potential shortages of essential materials like platinum coils and catheter components. Regulatory disparities between regions also create barriers, delaying product approvals and market entry. Moreover, fluctuations in currency exchange rates, inflation, and global economic downturns impact healthcare investments, slowing procurement and adoption rates in certain markets.

Latest Trends

The Switzerland coil transcatheter embolization and occlusion devices market is evolving rapidly, driven by advancements in minimally invasive procedures, technological innovations, and increasing prevalence of vascular disorders and cancer. The rising demand for non-surgical embolization treatments is leading to greater adoption of next-generation coils with improved flexibility, biocompatibility, and radiopacity. Hydrogel-coated and bioactive coils are emerging as key innovations, enhancing occlusion efficiency and reducing procedure times.

Additionally, automation and AI-driven imaging technologies are improving procedural accuracy, making embolization safer and more effective. The growing focus on personalized medicine is leading to the development of customized embolization solutions tailored to individual patient needs.

Furthermore, expanding healthcare infrastructure in emerging markets, coupled with increasing awareness among healthcare providers about the benefits of embolization, is boosting global adoption. Regulatory advancements and strategic collaborations among medical device companies are further accelerating research and development efforts, shaping the future of the market.

Key Players Analysis

The Switzerland coil transcatheter embolization and occlusion devices market in Switzerland is characterized by the presence of several key players contributing to its competitive landscape. Prominent companies operating in this sector include Boston Scientific Corporation, Medtronic plc, Stryker Corporation, Terumo Corporation, and Abbott Laboratories.

These industry leaders are recognized for their extensive product portfolios and commitment to advancing minimally invasive procedures. Their contributions significantly influence the development and adoption of coil transcatheter embolization and occlusion devices globally.

Top Key Players

- Johnson and Johnson

- Medtronic Plc

- Stryker Corporation

- Cook Medical

- Terumo Medical Corporation

- B. Braun Interventional Systems Inc.

- Abbott Laboratories.

- Boston Scientific Corporation

- Merit Medical Systems

- Pfizer, Inc.

Recent Developments

- In December 2023, Stryker has unveiled the 510k clearance of the Target Tetra Detachable Coil, the newest addition of its highly successful Target platform. This innovative coil features a unique tetrahedral shape and customized softness levels, with a specific focus on addressing small aneurysms.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 37.0 million |

| Forecast Revenue (2034) | US$ 81.6 million |

| CAGR (2025-2034) | 8.1% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Detachable Coils, Pushable Coils, and Other Product Types), By Procedure Type (Hemorrhage Control, Vascular Occlusion, Aneurysm Treatment, Tumor Embolization, and Other Procedure Types), By Material (Platinum or Platinum Alloy, Nickel Titanium (Nitinol), Stainless Steel, and Other Materials), By End-User (Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Clinics, and Research and Academic Institutes) |

| Regional Analysis | Johnson and Johnson, Medtronic Plc, Stryker Corporation, Cook Medical, Terumo Medical Corporation, B. Braun Interventional Systems Inc., Abbott Laboratories., Boston Scientific Corporation, Merit Medical Systems, and Pfizer, Inc. |

| Competitive Landscape | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |