Quick Navigation

Report Overview

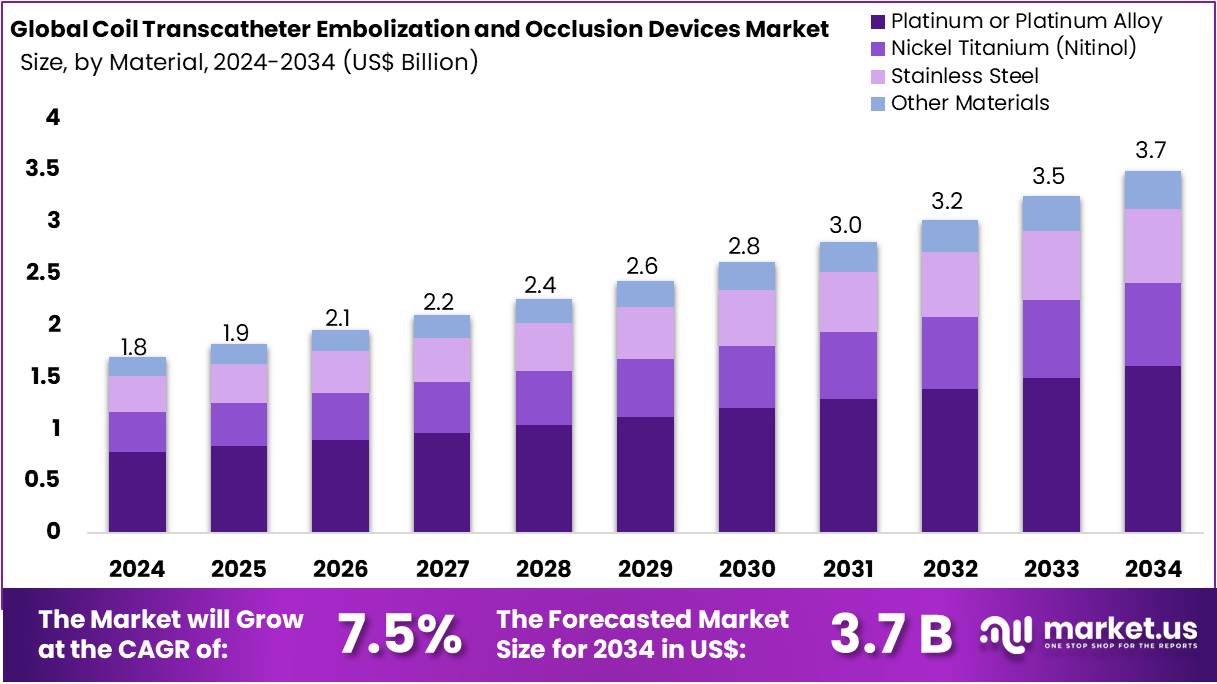

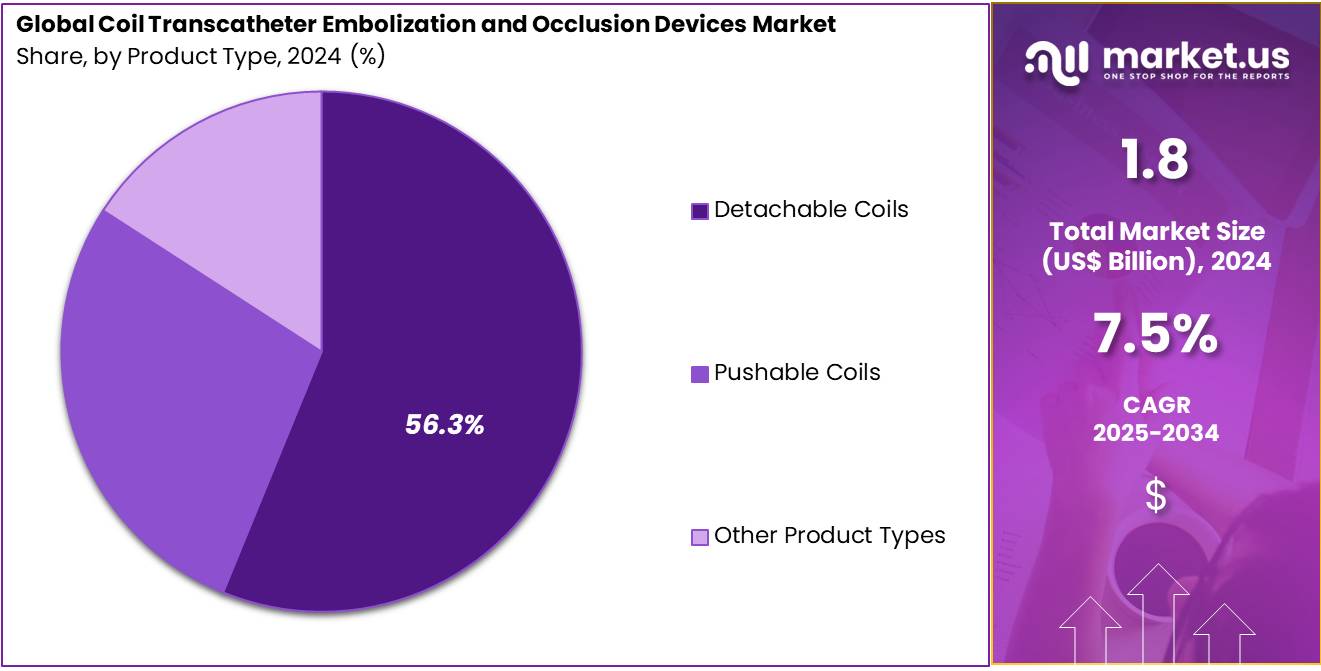

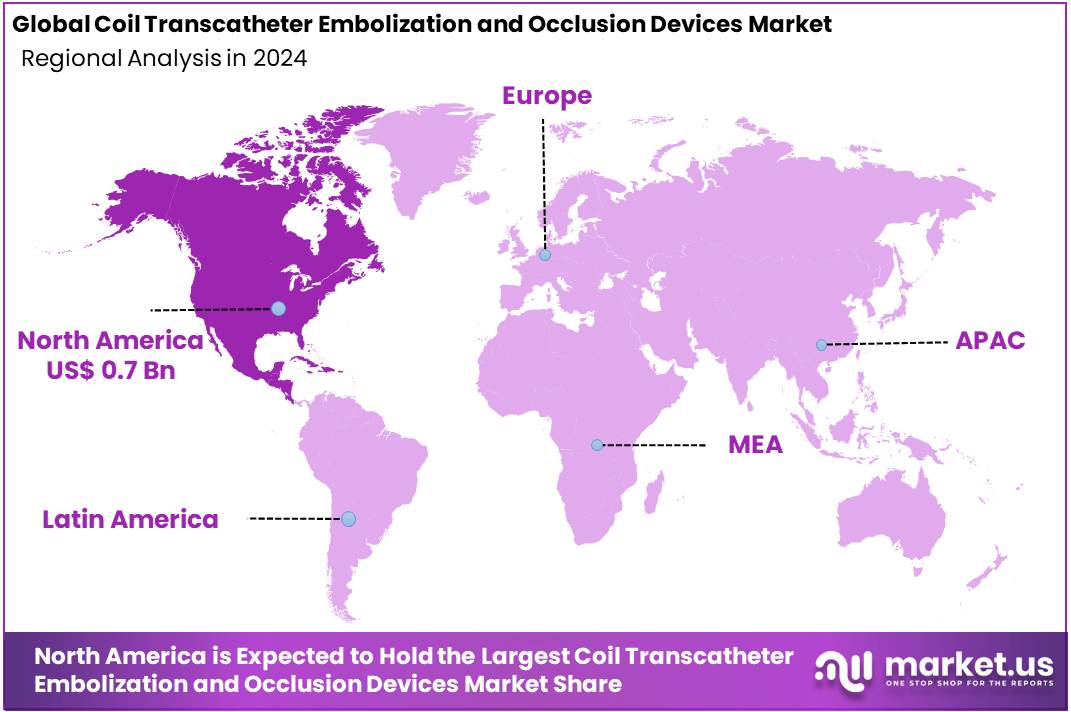

The Global Coil Transcatheter Embolization and Occlusion Devices Market size is expected to be worth around US$ 3.7 Billion by 2034, from US$ 1.8 Billion in 2024, growing at a CAGR of 7.5% during the forecast period from 2025 to 2034. North America held a dominant market position, capturing more than a 43% share and holds US$ 0.7 Billion market value for the year.

The coil transcatheter embolization and occlusion devices market is driven by the increasing prevalence of vascular diseases, cancer, including aneurysms, arteriovenous malformations, and gastrointestinal bleeding, which require effective minimally invasive treatments. Technological advancements in embolization devices, such as the development of micro-coils with improved precision and biocompatibility, are enhancing procedural efficiency and patient outcomes.

The rising adoption of interventional radiology over traditional surgery is contributing to market growth, as these devices offer reduced recovery times and lower risk of complications. Moreover, growing healthcare investments in developing regions and the rising demand for outpatient procedures further fuel market expansion.

However, challenges such as high device costs, limited reimbursement policies, and the need for specialized training for medical professionals may hinder widespread adoption. Despite these barriers, the market is expected to continue evolving, with key players focusing on product innovations and strategic partnerships to maintain competitiveness in the growing global market.

- According to a report by the National Institutes of Health (NIH), lung cancer ranks as the most commonly diagnosed cancer worldwide, with over 1.35 million new cases reported annually. Additionally, data from the Cleveland Clinic indicates that around 76,000 people in the United States are diagnosed with malignant kidney tumors each year. Meanwhile, the National Library of Medicine (NLM) estimates that over 250 million individuals globally are living with unruptured aneurysms. To mitigate the risk of these aneurysms rupturing, transcatheter embolization devices are commonly utilized to block blood flow to the affected areas.

Key Takeaways

- The coil transcatheter embolization and occlusion devices market was valued at USD 1.8 billion in 2024 and is anticipated to register substantial growth of USD 3.7 billion by 2034, with 7.5% CAGR.

- In 2024, the detachable coils segment took the lead in the global market, securing 56.3% of the total revenue share.

- The hemorrhage control segment took the lead in the global market, securing 23.6% of the total revenue share.

- The platinum or platinum alloy segment took the lead in the global market, securing 43.4% of the total revenue share.

- The hospitals segment took the lead in the global market, securing 56.9% of the total revenue share.

- North America maintained its leading position in the global market with a share of over 43% of the total revenue.

Product Type Analysis

Based on product type the market is fragmented into detachable coils, pushable coils, and other product types. Amongst these, detachable coils segment dominated the coil transcatheter embolization and occlusion devices market capturing a significant market share of 56.3% in 2024. The detachable coils segment has dominated the coil transcatheter embolization and occlusion devices market due to their superior precision and flexibility in treating a wide range of vascular conditions.

Detachable coils allow for better control during the embolization procedure, enabling physicians to adjust the placement of the coil within the target vessel, reducing the risk of complications. These coils are particularly effective in the treatment of aneurysms, arteriovenous malformations, and gastrointestinal bleeding, where precise occlusion is crucial for patient safety.

Additionally, advancements in coil design, such as improved biocompatibility and reduced coil migration, have further enhanced the popularity of detachable coils in clinical practice. The ability to detach the coil from the delivery catheter allows for a more secure and customizable treatment, which has contributed to their increased adoption. This segment is expected to continue leading the market as it offers enhanced procedural outcomes, patient safety, and improved overall performance compared to other embolization devices.

Procedure Type Analysis

The market is fragmented by procedure type into hemorrhage control, vascular occlusion, aneurysm treatment, tumor embolization, and other procedure types. Hemorrhage control dominated the coil transcatheter embolization and occlusion devices market capturing a significant market share of 23.6% in 2024 due to the increasing need for effective management of severe bleeding, particularly in trauma cases and surgical interventions.

Coil embolization is a highly effective treatment for controlling hemorrhages, as it allows for precise occlusion of blood vessels, thereby stopping bleeding rapidly and reducing the risk of further complications. This technique is especially crucial in treating patients with gastrointestinal bleeding, traumatic injuries, and certain types of vascular malformations.

The ability of coil embolization to provide a minimally invasive solution, with fewer risks and faster recovery times compared to traditional surgical methods, has driven its widespread adoption in clinical settings. Moreover, advancements in coil design and materials have improved the effectiveness and safety of hemorrhage control procedures. As the demand for less invasive and highly efficient treatment options continues to rise, hemorrhage control remains a dominant application in the coil embolization market.

Material Analysis

The market is fragmented by material into platinum or platinum alloy, nickel titanium (nitinol), stainless steel, and other materials. Platinum or platinum alloy dominated the coil transcatheter embolization and occlusion devices market capturing a significant market share of 43.4% in 2024. Platinum coils, and those made with platinum alloys, offer superior performance in terms of mechanical strength, making them ideal for precise placement and securing occlusion in blood vessels. These materials are also highly resistant to corrosion, ensuring long-term safety and durability within the body.

Furthermore, platinum’s radiopaque nature allows for better visualization during the procedure, enhancing the accuracy of coil placement, which is critical in treating complex vascular conditions such as aneurysms and arteriovenous malformations. The ease with which platinum coils conform to the shape of the vessel enhances their efficacy in achieving complete occlusion, making them a preferred choice among medical professionals. As a result, platinum and platinum alloys continue to dominate the market for coil embolization devices.

End-User Analysis

The market is fragmented by end-user into hospitals, ambulatory surgical centers (ASCs), specialty clinics, and research and academic institutes. Hospitals dominated the coil transcatheter embolization and occlusion devices market capturing a significant market share of 56.9% in 2024. Hospitals are the primary setting for interventional radiology procedures, where coil embolization devices are commonly used to treat a wide range of conditions such as aneurysms, arteriovenous malformations, and gastrointestinal bleeding.

The presence of specialized medical professionals, including interventional radiologists and surgeons, who are trained in these advanced techniques, further reinforces hospitals as the leading end-users of these devices. Additionally, hospitals are equipped with the necessary infrastructure, such as imaging systems and catheterization labs, to perform these procedures safely and effectively. The growing preference for minimally invasive procedures, which hospitals typically offer, has further fuelled the adoption of coil embolization devices, making hospitals the dominant segment in the market.

Key Segments Analysis

By Product Type

- Detachable Coils

- Pushable Coils

- Other Product Types

By Procedure Type

- Hemorrhage Control

- Vascular Occlusion

- Aneurysm Treatment

- Tumor Embolization

- Other Procedure Types

By Material

- Platinum or Platinum Alloy

- Nickel Titanium (Nitinol)

- Stainless Steel

- Other Materials

By End-User

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Specialty Clinics

- Research and Academic Institutes

Drivers

Increasing Incidence of Vascular Diseases

The coil transcatheter embolization and occlusion devices market is primarily driven by the increasing incidence of vascular diseases, including aneurysms, arteriovenous malformations, and gastrointestinal bleeding, which require embolization procedures for effective treatment. The rising preference for minimally invasive procedures, which offer shorter recovery times and fewer complications compared to traditional surgery, is another key factor driving market growth.

Technological advancements, such as the development of micro-coils, which are more precise and have enhanced biocompatibility, have further improved treatment outcomes. Additionally, the growing adoption of interventional radiology and the expanding healthcare infrastructure in emerging economies are contributing to the market’s expansion. Increased awareness about the benefits of these devices and a focus on improving patient care are also supporting the demand for coil embolization and occlusion devices globally.

Restraints

High Cost of Devices

The high cost of these devices, which limits their accessibility, particularly in price-sensitive markets and among low-income populations. Additionally, the need for specialized training and expertise for medical professionals to effectively use these devices can be a barrier, particularly in developing regions where healthcare personnel might not be adequately trained in interventional procedures. Limited reimbursement options for these procedures in some countries further restricts the widespread adoption of coil embolization devices.

Furthermore, complications associated with long-term device placement and the risk of device migration or failure can impact the overall acceptance of these devices. These factors, combined with regulatory hurdles in certain regions, may hinder market growth. These devices, particularly detachable platinum coils, are expensive, often costing between US$ 500 to US$ 3,000 per unit, and multiple coils are required for a single procedure.

Opportunities

Technological Advancements and Innovations

The coil transcatheter embolization and occlusion devices market offers significant growth opportunities, particularly driven by technological advancements and innovations. The development of next-generation embolization devices with enhanced materials, greater biocompatibility, and better precision is expected to further expand the market. There is also an opportunity to tap into the emerging economies, where improving healthcare infrastructure and increasing access to medical treatments are fostering greater demand for these devices.

Additionally, the growing trend of outpatient and minimally invasive procedures offers an opportunity for manufacturers to expand their product lines and increase their market reach. Collaborations and partnerships between medical device companies and healthcare institutions to improve device accessibility, training, and awareness could significantly enhance market growth. The increasing focus on personalized medicine, with tailored embolization solutions for specific conditions, also presents a promising opportunity for market players.

Impact of Macroeconomic Factors / Geopolitical Factors

Macroeconomic and geopolitical factors play a significant role in shaping the growth and dynamics of the coil transcatheter embolization and occlusion devices market. Economic conditions, such as global economic growth rates, inflation, and healthcare spending, directly impact the demand for medical devices. In times of economic downturn or recession, healthcare budgets in both developed and developing countries may face cuts, leading to restricted access to advanced medical treatments, including coil embolization devices.

Conversely, economic stability and rising disposable incomes in emerging economies increase the affordability and accessibility of such devices, driving market expansion. Geopolitical factors, such as trade policies, tariffs, and international relations, can also affect the supply chain for medical devices. Tensions or instability in key manufacturing countries may lead to disruptions in the production or distribution of these devices, causing delays and price fluctuations.

Additionally, regulatory differences across countries and regions can influence market entry strategies, with companies having to navigate complex approval processes and compliance standards, which can delay product launches and impact profitability. Political stability and the prioritization of healthcare infrastructure in certain regions can positively influence the adoption of interventional medical devices, while instability may deter investments and slow market growth in affected areas.

Trends

The coil transcatheter embolization and occlusion devices market is experiencing several key trends that are shaping its growth and innovation. One notable trend is the increasing shift towards minimally invasive procedures, driven by the demand for reduced recovery times, lower risk of complications, and better patient outcomes. This trend is pushing the development of more advanced embolization devices, such as micro-coils and bioabsorbable coils, that offer enhanced precision and biocompatibility.

Another significant trend is the rise in the adoption of interventional radiology over traditional surgical methods, which is further accelerating the use of embolization devices in various treatments, including aneurysms and arteriovenous malformations. Additionally, the market is witnessing growing interest in personalized medicine, with customized embolization treatments being developed to address the specific needs of patients.

The use of 3D printing and imaging technologies is also emerging, enabling more accurate device placement and improved clinical outcomes. Another key trend is the increasing focus on expanding market access in emerging economies, driven by rising healthcare infrastructure and growing awareness of advanced treatment options. Furthermore, several industry players are engaging in strategic partnerships, mergers, and acquisitions to strengthen their product portfolios and expand their geographic reach, fueling market competition and innovation.

Regional Analysis

North America emerged as the leading region in the market, accounting for over 43% of the total market share. This dominance corresponds to an estimated market value of approximately USD 0.7 billion for the year. The North American market for coil transcatheter embolization and occlusion devices is experiencing significant growth, driven by factors such as increasing healthcare expenditure, advancements in medical technologies, and a growing preference for minimally invasive procedures.

The region’s well-established healthcare infrastructure, along with a high incidence of vascular diseases such as aneurysms, arteriovenous malformations, and gastrointestinal bleeding, is fueling the demand for advanced embolization devices.

Additionally, the increasing adoption of interventional radiology over traditional surgical procedures in the United States and Canada has contributed to the market’s expansion, as these devices offer better outcomes, shorter recovery times, and fewer complications. Technological advancements in embolization devices, such as micro-coils with improved precision, enhanced biocompatibility, and reduced risk of migration, are further driving the demand.

Furthermore, the availability of reimbursement policies for these treatments in North America is another key factor supporting market growth. The presence of leading manufacturers and continuous innovation in the product offerings are also creating competitive dynamics that benefit patients. The rising awareness among healthcare professionals and patients about the effectiveness and safety of coil embolization procedures is contributing to the widespread adoption of these devices. These factors, combined with an aging population, are expected to continue driving the North American coil transcatheter embolization and occlusion devices market forward.

Key Players Analysis

The coil transcatheter embolization and occlusion devices market is characterized by intense competition, with several major companies driving innovation and growth. Prominent industry leaders such as Boston Scientific Corporation, Terumo Corporation, Abbott Laboratories, and Medtronic hold significant market shares by offering advanced solutions for various medical conditions, including aneurysms, arteriovenous malformations, and gastrointestinal bleeding.

These companies prioritize research and development efforts to introduce next-generation devices, including micro-coils, bioabsorbable coils, and precision-focused embolization systems designed to enhance biocompatibility and minimize complications. Additionally, strategic initiatives such as mergers, acquisitions, and collaborations are widely employed to expand product offerings and strengthen global market presence.

Top Key Players in the Cell Therapy Market

- Johnson and Johnson

- Medtronic Plc

- Stryker Corporation

- Cook Medical

- Terumo Medical Corporation

- B. Braun Interventional Systems Inc.

- Abbott Laboratories.

- Boston Scientific Corporation

- Merit Medical Systems

- Pfizer, Inc.

Recent Developments

- In December 2022, Abbott launched the Navitor Transcatheter Aortic Valve Implantation (TAVI) system in India, aimed at treating patients with severe aortic stenosis who are at high or extreme surgical risk. The company is advancing TAVI (also known as TAVR, or transcatheter aortic valve replacement) procedures through innovations like the Navitor valve design. TAVI serves as an alternative to traditional surgical aortic valve replacement, offering significant benefits by alleviating symptoms and extending the lives of patients suffering from this condition.

- In June 2024, a study published in the Journal of Interventional Radiology (JVIR) explored the potential of utilizing artificial intelligence (AI) to guide and enhance the precision of transcatheter embolization (TE) operations. This highlights the growing integration of AI into medical technologies, further improving procedural accuracy and patient outcomes.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 1.8 billion |

| Forecast Revenue (2034) | US$ 3.7 billion |

| CAGR (2025-2034) | 7.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Detachable Coils, Pushable Coils, and Other Product Types), By Procedure Type (Hemorrhage Control, Vascular Occlusion, Aneurysm Treatment, Tumor Embolization, and Other Procedure Types), By Material (Platinum or Platinum Alloy, Nickel Titanium (Nitinol), Stainless Steel, and Other Materials), By End-User (Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Clinics, and Research and Academic Institutes) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Johnson and Johnson, Medtronic Plc, Stryker Corporation, Cook Medical, Terumo Medical Corporation, B. Braun Interventional Systems Inc., Abbott Laboratories., Boston Scientific Corporation, Merit Medical Systems, and Pfizer, Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |