Quick Navigation

Report Overview

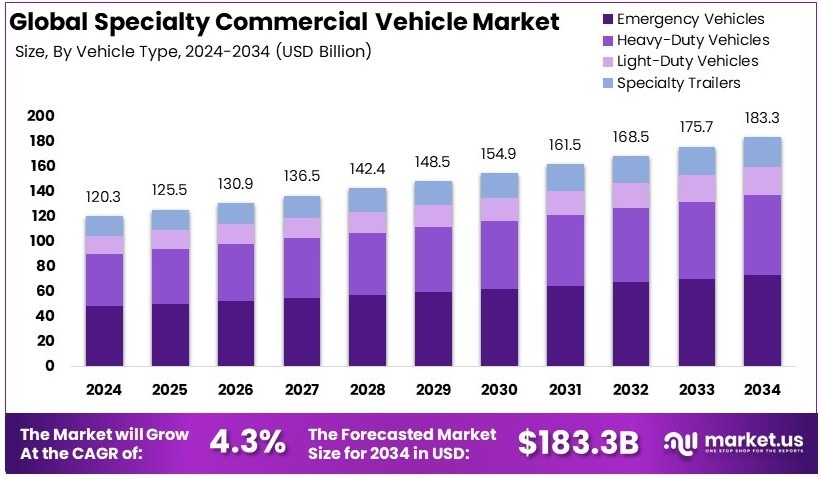

The Global Specialty Commercial Vehicle Market size is expected to be worth around USD 183.3 Billion by 2034, from USD 120.3 Billion in 2024, growing at a CAGR of 4.3% during the forecast period from 2025 to 2034.

A specialty commercial vehicle is designed for specific tasks not covered by standard commercial vehicles. It can be modified for unique industries, such as firefighting, construction, or medical services. These vehicles often include custom features tailored to specialized operations. They are built to meet distinct functional requirements in various sectors.

The specialty commercial vehicle market involves the design, production, and sale of customized vehicles for niche applications. It serves industries with unique transportation or operational needs. The market features manufacturers creating tailored solutions. This sector supports businesses looking for vehicles that meet specific performance, safety, and regulatory requirements.

Specialty commercial vehicles are crucial for maintaining essential services. For instance, the European Union boasts over 3,000 utility companies that rely on these vehicles for infrastructure tasks. The European Automobile Manufacturers Association (ACEA) tracks the use of these specialized vehicles, highlighting their critical role across various sectors.

The demand for specialty vehicles like fire trucks and ambulances is increasing. In the U.S., there are over 29,000 fire departments, each equipped with vehicles that meet the National Fire Protection Association (NFPA) standards. Similarly, in India, the 461,312 road accidents in 2022 underline the urgent need for well-equipped ambulances, driving demand in the emergency vehicle segment.

Government regulations significantly influence the specialty vehicle market. Standards set by organizations like the NFPA ensure that vehicles not only meet operational efficiencies but also adhere to safety requirements.

This regulatory environment supports market growth by ensuring that vehicles are both effective in their roles and safe for operators and the public, illustrating the local and broader impacts of these regulations on the specialty vehicle industry.

Key Takeaways

- The Specialty Commercial Vehicle Market was valued at USD 120.3 Billion in 2024, and is expected to reach USD 183.3 Billion by 2034, with a CAGR of 4.3%.

- In 2024, Emergency Vehicles dominate the vehicle type segment with 52%, reflecting their crucial role in specialized commercial operations.

- In 2024, Diesel leads the fuel type segment with 64%, demonstrating its prevalence in commercial vehicle powertrains.

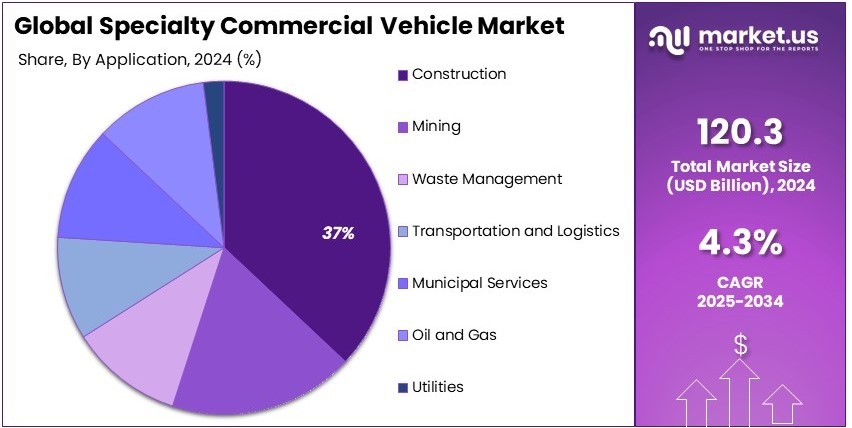

- In 2024, Construction dominates the application segment with 37%, underscoring its significant impact on vehicle demand.

- In 2024, Dump Trucks dominate the body style segment with 45%, reflecting their widespread use in heavy-duty transport.

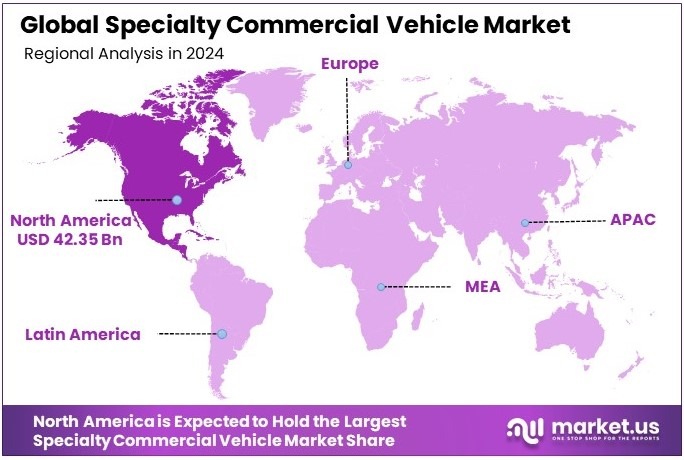

- In 2024, North America leads the regional market with 35.2% and a value of USD 42.35 Bn, highlighting its market prominence.

Vehicle Type Analysis

Emergency Vehicles dominate with 52% due to their critical role in safety and rapid response services.

The Specialty Commercial Vehicle Market is broadly categorized by the type of vehicle, focusing on specialized functions tailored to specific operational needs. Among these, Emergency Vehicles hold a dominant market share of 52%. This prominence is driven by their essential role in providing rapid response and rescue services, which are critical for public safety and emergency management.

Other vehicle types in this segment include Heavy-Duty Vehicles, Light-Duty Vehicles, and Specialty Trailers. Heavy-Duty Vehicles are indispensable in industries requiring substantial material handling capacities, whereas Light-Duty Vehicles are preferred for their versatility and efficiency in urban environments.

Specialty Trailers are crucial for transporting unique or oversized loads, contributing significantly to sectors like construction and large-scale event logistics.

Fuel Type Analysis

Diesel dominates with 64% due to its efficiency and reliability in heavy-duty applications.

In the Specialty Commercial Vehicle Market, Fuel Types play a significant role in defining vehicle performance and environmental impact. Diesel engines, known for their efficiency and long-lasting reliability, dominate the market with a 64% share, particularly valued in heavy-duty vehicles for their robust power and endurance.

Other key fuel types include Gasoline, Electric, and Hybrid. Gasoline is commonly used in lighter commercial vehicles due to its availability and cost-effectiveness.

Electric vehicles are gaining traction due to their lower emissions and reduced operational costs, making them increasingly popular in urban and regulated environments. Hybrid vehicles offer a balance between traditional and electric powertrains, providing a reduced environmental impact while maintaining performance.

Application Analysis

Construction dominates with 37% due to the heavy reliance on specialized vehicles for project efficiency and effectiveness.

Segmenting the market by Application, Construction leads with a 37% market share. The demand in this segment is driven by the construction industry’s heavy reliance on specialized vehicles that enhance project efficiency and operational capabilities, such as dump trucks and concrete mixers.

Additional applications include Mining, Waste Management, Transportation and Logistics, Municipal Services, Oil and Gas, and Utilities. Each of these sectors depends on specialty vehicles tailored to their specific operational needs, like mining requiring rugged vehicles for material extraction and waste management utilizing specialized trucks for collection and recycling processes.

Body Style Analysis

Dump Trucks dominate with 45% due to their essential role in construction and mining operations.

In terms of Body Style within the Specialty Commercial Vehicle Market, Dump Trucks hold the largest share at 45%, underscored by their crucial role in construction and mining operations. These vehicles are designed to handle heavy loads and rugged terrain, making them indispensable for transporting materials such as dirt, rocks, and debris.

Other significant body styles include Cutaway Vans, Chassis Cabs, Box Trucks, Refrigerated Trucks, and Concrete Mixers. Cutaway Vans and Chassis Cabs are versatile and can be customized for various service-related tasks, while Box Trucks are fundamental for freight and logistics operations.

Refrigerated Trucks play a critical role in transporting perishable goods, ensuring items remain at optimal temperatures. Concrete Mixers are vital in construction, providing consistent and ready-to-use concrete mix at worksites.

Key Market Segments

By Vehicle Type

- Heavy-Duty Vehicles

- Light-Duty Vehicles

- Emergency Vehicles

- Specialty Trailers

By Fuel Type

- Diesel

- Gasoline

- Electric

- Hybrid

By Application

- Construction

- Mining

- Waste Management

- Transportation and Logistics

- Municipal Services

- Oil and Gas

- Utilities

By Body Style

- Cutaway Vans

- Chassis Cabs

- Box Trucks

- Refrigerated Trucks

- Dump Trucks

- Concrete Mixers

Driving Factors

Multiple Factors Drive Market Growth

The Specialty Commercial Vehicle Market is expanding due to a mix of influential factors. Increasing demand for customized solutions in niche industries drives many manufacturers to tailor vehicles for specific tasks.

Growth of e-commerce has boosted the need for specialized logistics and delivery vehicles that can handle diverse products. Expanding construction and infrastructure development activities create more opportunities for vehicles designed for rugged conditions and heavy loads.

Rising adoption of electric specialty vehicles supports sustainability goals while reducing long-term operating costs. These factors work together to propel market growth.

For example, a construction firm may require a custom electric truck designed to transport heavy equipment on rough terrain. As demand for such tailored solutions rises, manufacturers invest more in innovation and specialized production. The focus on e-commerce logistics further pushes companies to design vehicles optimized for speed and efficiency in urban environments.

Restraining Factors

Economic and Regulatory Challenges Restrain Market Growth

The Specialty Commercial Vehicle Market faces several challenges that can restrain progress. Fluctuating raw material prices impact vehicle manufacturing costs and profit margins. This uncertainty can slow investment in new projects.

Limited availability of a skilled workforce for customization poses another challenge. Companies struggle to find technicians who can meet specialized production needs. Challenges in meeting stringent emission norms and regulations add further complexity.

Adapting designs to comply with environmental standards often requires significant R&D and investment. Dependence on economic stability for industrial demand also restrains growth. During downturns, fewer industries invest in new vehicles, reducing market demand.

These issues create a challenging environment for market players. For instance, a spike in steel prices could raise vehicle costs, affecting pricing and sales. Shortages of skilled labor slow down customization processes, delaying orders. Stricter emission laws may force companies to redesign vehicles, increasing development time and expenses. Economic instability can lead to reduced spending on new vehicles, further slowing growth.

Growth Opportunities

Innovation Provides Opportunities

Innovation opens up significant opportunities in the Specialty Commercial Vehicle Market. Development of advanced hybrid and electric powertrains offers cleaner and more efficient vehicles that appeal to eco-conscious industries.

Rising demand for autonomous specialty vehicles in industrial applications provides a niche for high-tech solutions that improve safety and efficiency. Increasing focus on lightweight materials for efficiency reduces fuel consumption and enhances performance.

Opportunities in emerging markets with growing industrialization further expand the customer base. For example, a manufacturer might develop a hybrid vehicle using lightweight composites for a booming construction market in Asia.

The combination of powertrain innovation, autonomy, and material science drives new product offerings. This not only meets regulatory standards but also satisfies customer needs for efficiency and sustainability. Companies that invest in these areas can gain a competitive edge, tapping into new revenue streams and market segments.

Emerging Trends

Smart Trends Are Latest Trending Factor

The Specialty Commercial Vehicle Market is witnessing exciting trends that shape its future. Growth of subscription-based models for vehicle services is emerging as a new business model. Customers prefer flexible leasing options and maintenance packages that reduce upfront costs.

Increasing focus on modular design for versatile applications allows vehicles to be easily adapted for different tasks, improving efficiency and reducing downtime. Development of hydrogen-powered specialty vehicles is on the rise as companies seek alternative fuels to meet sustainability goals.

Integration of augmented reality in vehicle maintenance and training offers innovative ways to improve service speed and accuracy. For instance, mechanics using AR glasses can access step-by-step repair instructions in real-time.

These trends highlight a shift toward flexibility, sustainability, and high-tech solutions. Subscription models and modular designs offer cost savings and adaptability. Hydrogen power reduces emissions while AR enhances maintenance practices.

Regional Analysis

North America Dominates with 35.2% Market Share

North America commands the Specialty Commercial Vehicle Market with a 35.2% share, equating to USD 42.35 billion. This leading position is driven by diverse industrial demands, a strong emphasis on regulatory compliance, and substantial investments in infrastructure and utility sectors.

The region’s dominance is supported by a robust manufacturing base and advanced technological capabilities, enabling the production and customization of specialty vehicles across various industries. Additionally, strong economic growth and extensive logistics networks contribute to the high demand for specialized commercial vehicles.

Looking ahead, North America’s influence in the global Specialty Commercial Vehicle Market is expected to remain strong. Continuous technological innovations and an increasing focus on sustainability are likely to drive further growth in the market, reinforcing the region’s leadership position.

Regional Mentions:

- Europe: Europe maintains a significant presence in the Specialty Commercial Vehicle Market, with a focus on environmental sustainability and safety. The market is supported by stringent regulations that drive the demand for eco-friendly and technologically advanced vehicles.

- Asia Pacific: Asia Pacific is experiencing robust growth in the Specialty Commercial Vehicle Market due to rapid industrialization and infrastructure development. The region benefits from a large manufacturing base and increasing governmental focus on transportation and logistics.

- Middle East & Africa: The Middle East and Africa are expanding their market share in the specialty vehicle sector, driven by investments in construction and mining industries. The region’s strategic focus on diversifying economies also supports the growth of specialized commercial vehicles.

- Latin America: Latin America’s Specialty Commercial Vehicle Market is gradually growing, influenced by urbanization and industrial activities. Increased investments in infrastructure projects across the region are prompting higher demand for specialized vehicles.

Key Regions and Countries Covered in the Report

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Landscape

In the Specialty Commercial Vehicle Market, the leading companies include Oshkosh Corporation, AB Volvo, Daimler AG, and MAN Truck & Bus SE. These firms are influential in the industry due to their innovative vehicle solutions, strong global presence, and significant investment in research and development.

Oshkosh Corporation is renowned for its production of specialty vehicles, including defense, fire, and emergency vehicles. Their focus on durability and advanced safety features makes them a top choice for demanding environments and critical missions.

AB Volvo is known for its high-performance trucks and construction equipment. Volvo’s commitment to sustainability and safety, along with its robust global service network, ensures it remains a leader in providing vehicles that meet a variety of specialized industrial needs.

Daimler AG, with its Mercedes-Benz trucks, sets standards in high-end specialty commercial vehicles used in logistics, construction, and transportation. Daimler’s emphasis on technological innovation and high-quality engineering drives its strong market position.

MAN Truck & Bus SE offers a range of heavy-duty and utility vehicles that are pivotal in industries such as construction, municipal services, and logistics. MAN’s focus on fuel efficiency and reduced emissions, coupled with advanced driver assistance systems, underscores its commitment to market-leading vehicle solutions.

These companies shape the Specialty Commercial Vehicle Market by advancing vehicle technology and expanding their product lines to include environmentally friendly and technologically sophisticated options. Their continued growth and adaptation to market needs help set the pace for industry standards and innovations, ensuring their dominant positions in the market.

Major Companies in the Market

- Oshkosh Corporation

- AB Volvo

- Daimler AG

- MAN Truck & Bus SE

- Hino Motors, Ltd.

- Isuzu Motors Limited

- PACCAR Inc.

- Navistar International Corporation

- Tata Motors

- Ashok Leyland

- Rosenbauer International AG

- Iveco S.p.A.

- Scania AB

Recent Developments

- REV Group and Bus Manufacturing Exit: On January 2024, REV Group announced its decision to exit the bus manufacturing business. It sold its Collins school bus brand to Forest River for $303 million and its ENC transit bus division to Rivaz Inc. for $52 million.

- Oshkosh Corporation and AUSA Center SA: On May 2024, Oshkosh Corporation acquired AUSA Center SA, a manufacturer of compact all-terrain industrial vehicles. This acquisition aims to expand Oshkosh’s product portfolio in the construction and municipal sectors.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 120.3 Billion |

| Forecast Revenue (2034) | USD 183.3 Billion |

| CAGR (2025-2034) | 4.3% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Vehicle Type (Heavy-Duty Vehicles, Light-Duty Vehicles, Emergency Vehicles, Specialty Trailers), By Fuel Type (Diesel, Gasoline, Electric, Hybrid), By Application (Construction, Mining, Waste Management, Transportation and Logistics, Municipal Services, Oil and Gas, Utilities), By Body Style (Cutaway Vans, Chassis Cabs, Box Trucks, Refrigerated Trucks, Dump Trucks, Concrete Mixers) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Oshkosh Corporation, AB Volvo, Daimler AG, MAN Truck & Bus SE, Hino Motors, Ltd., Isuzu Motors Limited, PACCAR Inc., Navistar International Corporation, Tata Motors, Ashok Leyland, Rosenbauer International AG, Iveco S.p.A., Scania AB |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |