Quick Navigation

Report Overview

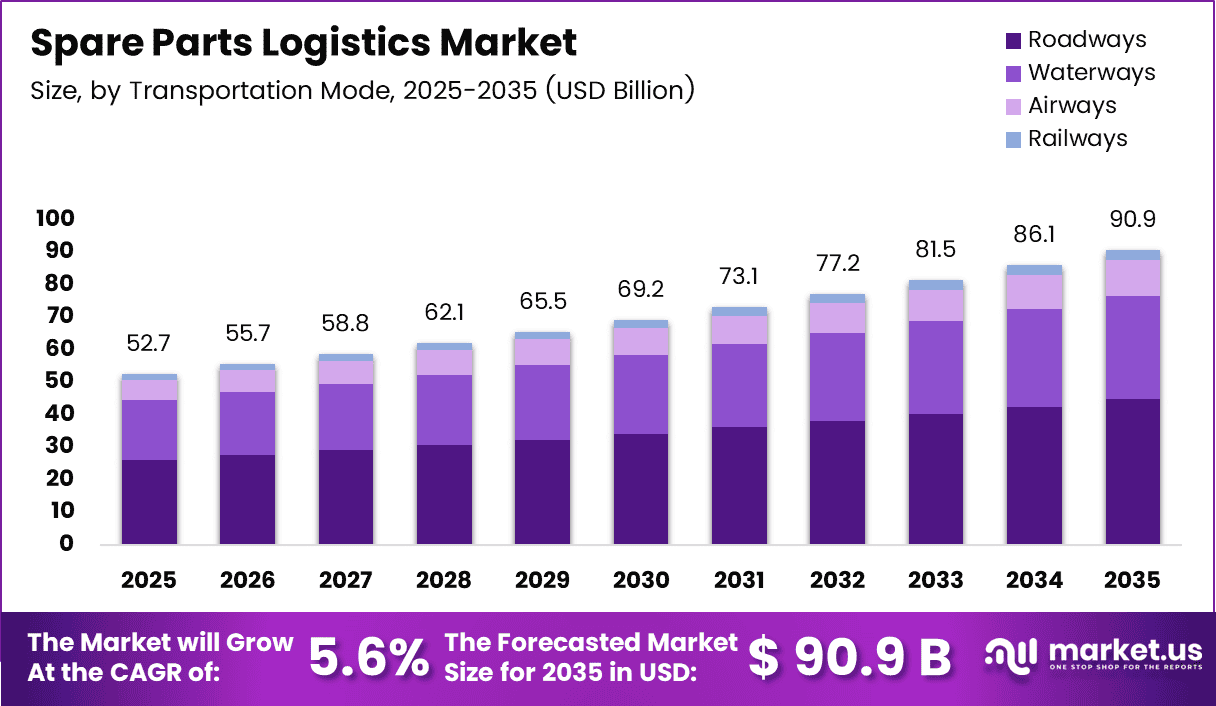

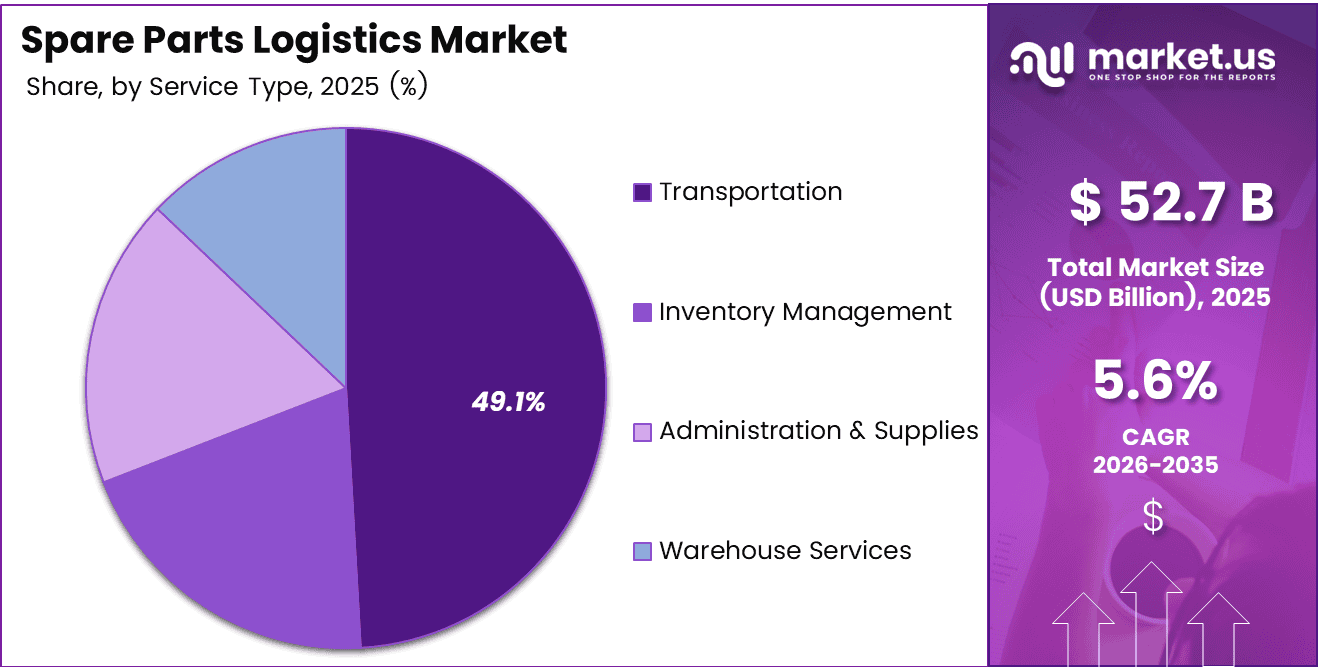

Global Spare Parts Logistics Market size is expected to be worth around USD 90.9 Billion by 2035 from USD 52.7 Billion in 2025, growing at a CAGR of 5.6% during the forecast period 2026 to 2035.

The spare parts logistics market encompasses comprehensive supply chain solutions for automotive components distribution. This sector manages transportation, warehousing, inventory control, and delivery of replacement parts to manufacturers, dealerships, and repair facilities. These specialized logistics services ensure timely availability of critical components across global networks.

Modern spare parts logistics combines advanced technology with traditional distribution methods. Companies utilize sophisticated tracking systems, automated warehousing, and multi-modal transportation networks to optimize delivery efficiency. The integration of digital platforms enables real-time inventory visibility and demand forecasting capabilities.

The market experiences robust growth driven by expanding automotive production and increasing vehicle parc worldwide. Moreover, the shift toward just-in-time delivery models and e-commerce channels accelerates demand for agile logistics solutions. Rising vehicle complexity and technological advancement in automobiles further amplify spare parts requirements.

Automotive manufacturers and aftermarket suppliers increasingly prioritize efficient parts distribution networks. Consequently, logistics providers invest heavily in warehouse automation, last-mile delivery optimization, and digital transformation initiatives. These investments enhance operational efficiency while reducing delivery times and overall costs.

Government initiatives promoting automotive industry development support market expansion. Additionally, regulatory standards for vehicle maintenance and safety compliance drive consistent demand for genuine replacement parts. Environmental regulations also encourage adoption of sustainable logistics practices and fuel-efficient transportation modes.

The emergence of electric vehicles creates new opportunities in specialized component logistics. Furthermore, growing emphasis on predictive maintenance and connected vehicle technologies transforms traditional parts distribution models. These trends require logistics providers to develop capabilities in handling sensitive electronic components.

According to Parts Express B.V., the company handles over 1 million shipments annually with 49% processed during day operations and 42% through night distribution services. According to Yusen Logistics, the company operates more than 680 locations across 47 countries with over 2.9 million square meters of warehouse space globally.

Key Takeaways

- Global Spare Parts Logistics Market valued at USD 52.7 Billion in 2025, projected to reach USD 90.9 Billion by 2035

- Market growing at a CAGR of 5.6% during the forecast period 2026-2035

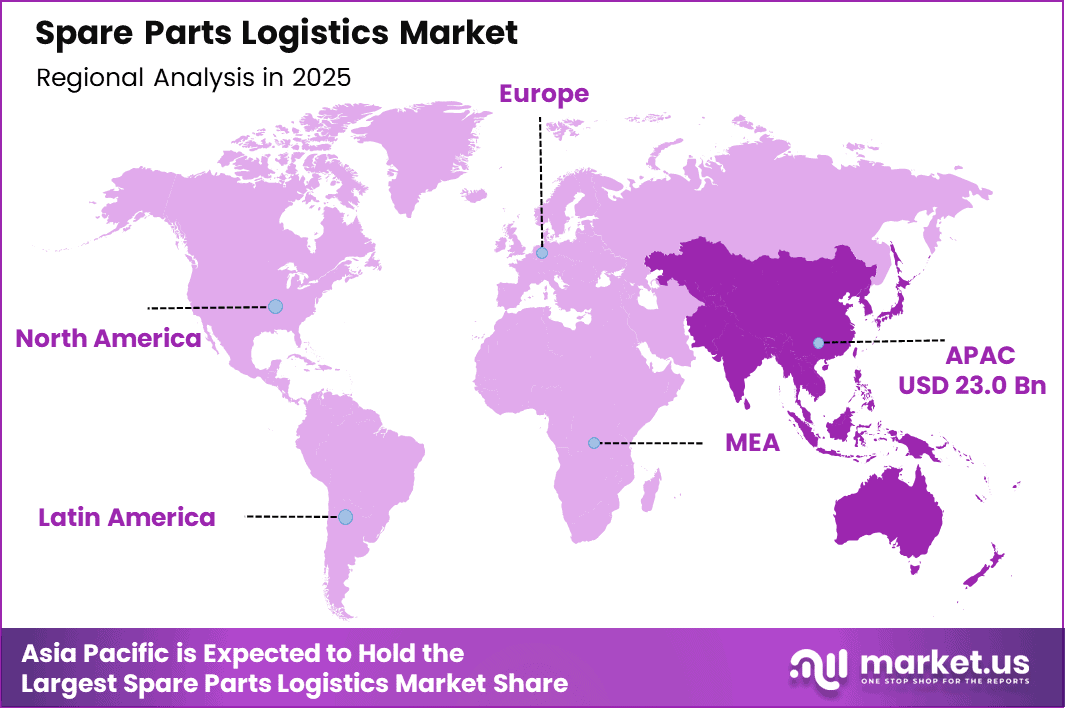

- Asia Pacific dominates with 43.80% market share, valued at USD 23.0 Billion

- Roadways transportation mode leads with 49.4% market share

- Transportation service type holds dominant position with 49.1% share

- Hatchback/Sedan vehicle type accounts for 37.8% of market

- Aftermarket Parts segment dominates end-use category with 66.7% share

- Powertrain Components lead spare parts type segment with 21.5% market share

Transportation Mode Analysis

Roadways dominates with 49.4% due to flexibility and last-mile delivery efficiency.

In 2025, ‘Roadways‘ held a dominant market position in the ‘Transportation Mode’ segment of Spare Parts Logistics Market, with a 49.4% share. Road transportation offers unmatched flexibility for distributing automotive parts across diverse geographic locations. The extensive network of highways and local roads enables direct delivery to remote service centers and dealerships efficiently.

Airways transportation provides critical support for urgent and high-value spare parts delivery requirements. Air freight ensures rapid international shipping of time-sensitive components, particularly for production line support and critical repairs. However, higher costs limit its application to premium and emergency shipments where speed justifies the expense.

Railways offer cost-effective solutions for bulk spare parts movement across long distances within continental regions. Rail transport provides reliable scheduling and lower environmental impact compared to road alternatives. This mode particularly suits large-volume shipments between major distribution centers and regional warehouses.

Waterways handle international spare parts logistics for non-urgent bulk shipments between continents. Maritime transportation delivers the most economical solution for large-volume imports and exports of automotive components. Despite longer transit times, sea freight remains essential for global supply chain operations.

Service Type Analysis

Transportation dominates with 49.1% due to critical role in parts distribution networks.

In 2025, ‘Transportation‘ held a dominant market position in the ‘Service Type’ segment of Spare Parts Logistics Market, with a 49.1% share. Transportation services form the backbone of spare parts distribution, ensuring timely delivery from manufacturers to end users. Multi-modal transportation solutions optimize cost efficiency while maintaining delivery speed requirements.

Warehouse Services provide essential storage, handling, and inventory management for automotive components across distribution networks. Modern warehouses utilize automation and robotics to enhance picking accuracy and processing speed. These facilities serve as strategic nodes ensuring parts availability and enabling rapid order fulfillment.

Inventory Management services optimize stock levels across global distribution networks using advanced analytics and forecasting tools. Real-time visibility systems track parts movement and availability throughout the supply chain. Effective inventory management reduces holding costs while preventing stockouts of critical components.

Administration & Supplies encompass documentation, customs clearance, quality control, and packaging services supporting logistics operations. These administrative functions ensure regulatory compliance and maintain data accuracy across international shipments. Proper administration streamlines processes and reduces delays in cross-border parts movement.

Vehicle Type Analysis

Hatchback/Sedan dominates with 37.8% due to high market penetration and volume.

In 2025, Hatchback/Sedan held a dominant market position in the Vehicle Type segment of Spare Parts Logistics Market, with a 37.8% share. Passenger cars represent the largest vehicle segment globally, generating substantial demand for replacement parts and maintenance components. The mature aftermarket for sedans and hatchbacks ensures consistent logistics requirements.

SUVs demonstrate rapid growth in spare parts logistics driven by increasing consumer preference for sport utility vehicles worldwide. The expanding SUV market creates rising demand for specialized components and larger parts inventory requirements. Premium SUV segments particularly drive demand for expedited delivery services.

LCVs (Light Commercial Vehicles) require dedicated logistics support for fleet maintenance and commercial operations. Business users prioritize minimal downtime, necessitating efficient parts distribution networks and reliable inventory availability. The growth of e-commerce and last-mile delivery services amplifies LCV parts demand.

HCVs (Heavy Commercial Vehicles) demand specialized logistics handling for large components and time-critical delivery to minimize fleet downtime. Transportation and logistics companies maintain extensive parts inventories to support their vehicle fleets. The commercial nature of HCV operations emphasizes cost-effective and reliable parts supply chains.

End-use Analysis

Aftermarket Parts dominates with 66.7% due to ongoing maintenance and replacement demand.

In 2025, ‘Aftermarket Parts‘ held a dominant market position in the ‘End-use’ segment of Spare Parts Logistics Market, with a 66.7% share. The aftermarket generates continuous demand from vehicle owners, independent repair shops, and service centers requiring replacement components. Growing vehicle age and extended ownership periods amplify aftermarket parts consumption and distribution requirements.

OEM Parts serve original equipment manufacturers for production lines and authorized service networks requiring genuine components. OEM logistics emphasize quality assurance, precise inventory management, and just-in-time delivery to manufacturing facilities. Although smaller in volume than aftermarket, OEM parts typically command premium pricing and stricter quality standards.

Spare Parts Type Analysis

Powertrain Components dominates with 21.5% due to critical functionality and replacement frequency.

In 2025, ‘Powertrain Components‘ held a dominant market position in the ‘Spare Parts Type’ segment of Spare Parts Logistics Market, with a 21.5% share. Engine components, transmission parts, and drivetrain elements require frequent replacement due to wear and performance degradation. These critical components demand reliable logistics networks ensuring rapid availability to minimize vehicle downtime.

Body & Structural Parts include panels, bumpers, doors, and chassis components requiring careful handling and specialized packaging during transportation. Collision repairs and cosmetic maintenance generate steady demand for these parts across aftermarket channels. The fragile nature of body parts necessitates specialized logistics handling to prevent damage.

Brake System Parts represent safety-critical components with consistent replacement cycles driven by regulatory inspections and wear patterns. Brake pads, rotors, calipers, and hydraulic components require reliable distribution networks ensuring widespread availability. The safety-critical nature of brake parts emphasizes quality assurance throughout the logistics chain.

Suspension & Steering components experience wear from road conditions and driving patterns, generating regular replacement demand. Shocks, struts, control arms, and steering assemblies require precise handling during storage and transportation. Regional road conditions significantly influence replacement frequencies and logistics demand patterns.

Engine & Cooling parts include radiators, water pumps, thermostats, and engine management components essential for vehicle operation. These parts require temperature-controlled storage and careful handling to maintain quality and performance specifications. The complexity of modern engines drives increasing diversity in component requirements.

Exhaust System components face corrosion and thermal stress, necessitating periodic replacement throughout vehicle lifecycle. Mufflers, catalytic converters, and exhaust pipes require specialized packaging to prevent damage during transportation. Environmental regulations increasingly influence exhaust component specifications and replacement patterns.

Wheels & Accessories encompass rims, tires, wheel bearings, and decorative components serving both functional and aesthetic purposes. Seasonal tire changes and wheel customization drive consistent logistics demand across diverse geographic markets. The bulky nature of wheels requires efficient storage and transportation solutions.

Others category includes electrical components, lighting systems, interior parts, and miscellaneous accessories supporting vehicle functionality and comfort. The growing complexity of modern vehicles expands the range of electronic and specialized components. These diverse parts require flexible logistics solutions accommodating varying sizes, weights, and handling requirements.

Key Market Segments

Transportation Mode

- Roadways

- Airways

- Railways

- Waterways

Service Type

- Transportation

- Warehouse Services

- Inventory Management

- Administration & Supplies

Vehicle Type

- Hatchback/Sedan

- SUVs

- LCVs

- HCVs

End-use

- Aftermarket Parts

- OEM Parts

Spare Parts Type

- Powertrain Components

- Body & Structural Parts

- Brake System Parts

- Suspension & Steering

- Engine & Cooling

- Exhaust System

- Wheels & Accessories

- Others

Drivers

Persistent Range Anxiety and Infrastructure Gaps Drive Extended-Range Electric Vehicle Demand

Persistent range anxiety among consumers continues limiting full battery-electric vehicle adoption despite advancing battery technologies. Many drivers remain concerned about running out of charge during long journeys or in areas with limited charging infrastructure. Consequently, range-extender equipped vehicles offer psychological comfort and practical solutions for diverse driving scenarios.

Insufficient fast-charging infrastructure in emerging and semi-urban markets constrains pure electric vehicle viability in many regions. Rural areas and developing economies lack comprehensive charging networks necessary for convenient long-distance travel. Therefore, range-extender technologies bridge the gap between conventional vehicles and full electrification during the infrastructure development phase.

Growing OEM focus on transitional electrification technologies reflects manufacturer recognition of consumer concerns and market realities. Range-extended electric vehicles provide viable pathways for automakers to meet emissions regulations while addressing consumer needs. Additionally, demand for extended driving range in commercial and fleet electric vehicles drives adoption where operational reliability remains paramount.

Restraints

Advancing Battery Technology and System Complexity Limit Range-Extender Market Growth

Rising preference for long-range battery EVs with rapid charging capabilities challenges range-extender vehicle market potential. Modern electric vehicles increasingly offer ranges exceeding 400 kilometers on single charges, reducing range anxiety concerns significantly. Fast-charging technology advancements enable 80% battery replenishment within 30 minutes at high-power charging stations.

Improved battery energy density and cost reductions make pure electric vehicles increasingly competitive without range-extender complexity. Consumers recognize that adding combustion engines increases maintenance requirements and reduces the environmental benefits of electrification. Moreover, simplified pure-electric architectures align better with long-term sustainability goals and zero-emission mandates.

Higher system complexity and integration costs versus pure BEV platforms present significant economic challenges for range-extender adoption. Manufacturers must develop and integrate both electric and combustion powertrains, increasing engineering costs and component expenses. This dual-system approach complicates vehicle design, adds weight, and potentially reduces overall efficiency compared to dedicated electric platforms.

Growth Factors

Expanding Applications and Government Support Accelerate Range-Extender Market Development

Expansion of range-extender adoption in pickup trucks, SUVs, and off-road EVs creates substantial growth opportunities. These vehicle segments require extended range and high load capacity where pure battery solutions remain challenging. Consequently, range-extender technology provides practical electrification pathways for demanding applications and recreational vehicles.

Increasing government support for hybrid and transitional EV powertrains encourages manufacturer investment in range-extender technologies. Regulatory frameworks in various regions recognize range-extended vehicles as stepping stones toward full electrification. Financial incentives and favorable emissions classifications make these vehicles attractive to both manufacturers and consumers.

Technological advancements in compact, low-emission range-extender engines improve system efficiency and reduce environmental impact. Modern range-extender units deliver better fuel economy and lower emissions than previous generations. Furthermore, strong growth potential in regions with underdeveloped EV charging networks ensures sustained demand in emerging markets and rural areas.

Emerging Trends

Advanced Technologies and Alternative Fuels Transform Range-Extender Powertrain Development

Development of hydrogen-ready and alternative-fuel range-extender engines represents significant technological evolution in the segment. Manufacturers explore sustainable fuel options including hydrogen combustion and synthetic fuels to reduce carbon footprints. These innovations align range-extender technology with long-term environmental sustainability objectives while maintaining operational flexibility.

Integration of intelligent energy management and AI-based control systems optimizes power delivery and efficiency in range-extended vehicles. Advanced algorithms predict driving patterns, terrain, and traffic conditions to maximize electric operation and minimize combustion engine usage. Therefore, smart energy management enhances fuel economy while improving overall driving experience and performance.

Rising use of modular and scalable range-extender powertrain architectures enables flexible application across diverse vehicle platforms. Manufacturers develop standardized range-extender modules adaptable to multiple vehicle types and sizes with minimal redesign. Additionally, strategic investments and joint ventures focused on EREV powertrain platforms accelerate technology development and market commercialization efforts.

Regional Analysis

Asia Pacific Dominates the Spare Parts Logistics Market with a Market Share of 43.80%, Valued at USD 23.0 Billion

Asia Pacific leads the global spare parts logistics market driven by massive automotive production volumes and expanding vehicle ownership. The region hosts major manufacturing hubs in China, Japan, South Korea, and India, generating substantial parts distribution requirements. Moreover, growing middle-class populations and increasing vehicle sales create sustained demand for aftermarket components and logistics services.

North America Spare Parts Logistics Market Trends

North America demonstrates mature spare parts logistics infrastructure with advanced warehouse automation and distribution networks. The region benefits from established automotive industry presence and sophisticated supply chain management systems. Additionally, strong e-commerce growth and consumer preference for rapid delivery accelerate logistics innovation and investment.

Europe Spare Parts Logistics Market Trends

Europe maintains highly developed spare parts logistics operations supported by stringent quality standards and regulatory frameworks. The region emphasizes sustainable transportation methods and efficient cross-border distribution across European Union member states. Furthermore, premium automotive segments and aging vehicle fleets drive consistent demand for specialized logistics services.

Latin America Spare Parts Logistics Market Trends

Latin America experiences growing spare parts logistics demand fueled by increasing vehicle ownership and developing automotive manufacturing sectors. Infrastructure improvements and economic development support market expansion across Brazil, Mexico, and other key economies. However, logistical challenges related to geography and infrastructure quality require innovative distribution solutions.

Middle East & Africa Spare Parts Logistics Market Trends

Middle East & Africa shows emerging potential in spare parts logistics driven by automotive market growth and infrastructure development initiatives. The region faces unique challenges including vast distances, varying infrastructure quality, and diverse regulatory environments. Nevertheless, increasing vehicle imports and growing aftermarket sectors create opportunities for logistics service expansion.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Kuehne Nagel stands as a global leader in spare parts logistics, offering comprehensive supply chain solutions across multiple continents. The company leverages advanced technology platforms and extensive network infrastructure to optimize automotive parts distribution. Their specialized automotive logistics division provides tailored solutions for manufacturers, dealers, and aftermarket suppliers, ensuring efficient inventory management and rapid delivery capabilities.

DHL Supply Chain delivers integrated logistics services for automotive spare parts through its worldwide network and sophisticated warehouse automation systems. The company combines traditional distribution excellence with digital innovation to enhance supply chain visibility and operational efficiency. DHL’s automotive-focused solutions address complex requirements including time-critical deliveries, reverse logistics, and multi-tier distribution network management for global clients.

XPO Logistics provides technology-driven spare parts logistics solutions emphasizing last-mile delivery optimization and warehouse automation capabilities. The company invests heavily in digital platforms enabling real-time tracking, predictive analytics, and seamless integration with customer systems. XPO’s automotive logistics expertise encompasses aftermarket distribution, OEM support, and specialized handling for sensitive electronic components in modern vehicles.

CEVA Logistics offers end-to-end automotive logistics services including spare parts warehousing, transportation, and value-added services across global markets. The company maintains strategic partnerships with major automotive manufacturers and aftermarket distributors, providing customized logistics solutions. CEVA’s focus on operational excellence and continuous improvement drives efficiency gains while supporting customer growth objectives in competitive markets.

Key players

- Kuehne Nagel

- DHL Supply Chain

- XPO Logistics

- CEVA Logistics

- Rhenus Logistics

- Dachser

- UPS Supply Chain Solutions

- DB Schenker

- Yusen Logistics

- Geodis

Recent Developments

- May 2024 – Yusen Logistics (Benelux) B.V. successfully completed the acquisition of Parts Express B.V., marking a strategic expansion in European automotive logistics capabilities. This acquisition strengthens Yusen’s position in spare parts distribution across the Benelux region and enhances service offerings for automotive clients.

- February 2024 – AIT Worldwide Logistics acquired Global Transport Solutions Group, expanding its automotive logistics footprint and enhancing specialized transportation capabilities. This strategic move enables AIT to offer comprehensive spare parts logistics solutions across broader geographic markets with improved service integration.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 52.7 Billion |

| Forecast Revenue (2035) | USD 90.9 Billion |

| CAGR (2026-2035) | 5.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | Transportation Mode (Roadways, Airways, Railways, Waterways), Service Type (Transportation, Warehouse Services, Inventory Management, Administration & Supplies), Vehicle Type (Hatchback/Sedan, SUVs, LCVs, HCVs), End-use (Aftermarket Parts, OEM Parts), Spare Parts Type (Powertrain Components, Body & Structural Parts, Brake System Parts, Suspension & Steering, Engine & Cooling, Exhaust System, Wheels & Accessories, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Kuehne Nagel, DHL Supply Chain, XPO Logistics, CEVA Logistics, Rhenus Logistics, Dachser, UPS Supply Chain Solutions, DB Schenker, Yusen Logistics, Geodis |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |