Global Smart Motors Market Size, Share, Growth Analysis By Component (Motor, Variable Speed Drive, Intelligent Motor Control Center), By Product (24V, 18V, 36V, 48.24V), By Application (Automotive, Aerospace and Defense, Oil and Gas, Metal and Mining, Water and Wastewater Treatment, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2025-2034

- Published date: Sep 2025

- Report ID: 159697

- Number of Pages: 286

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

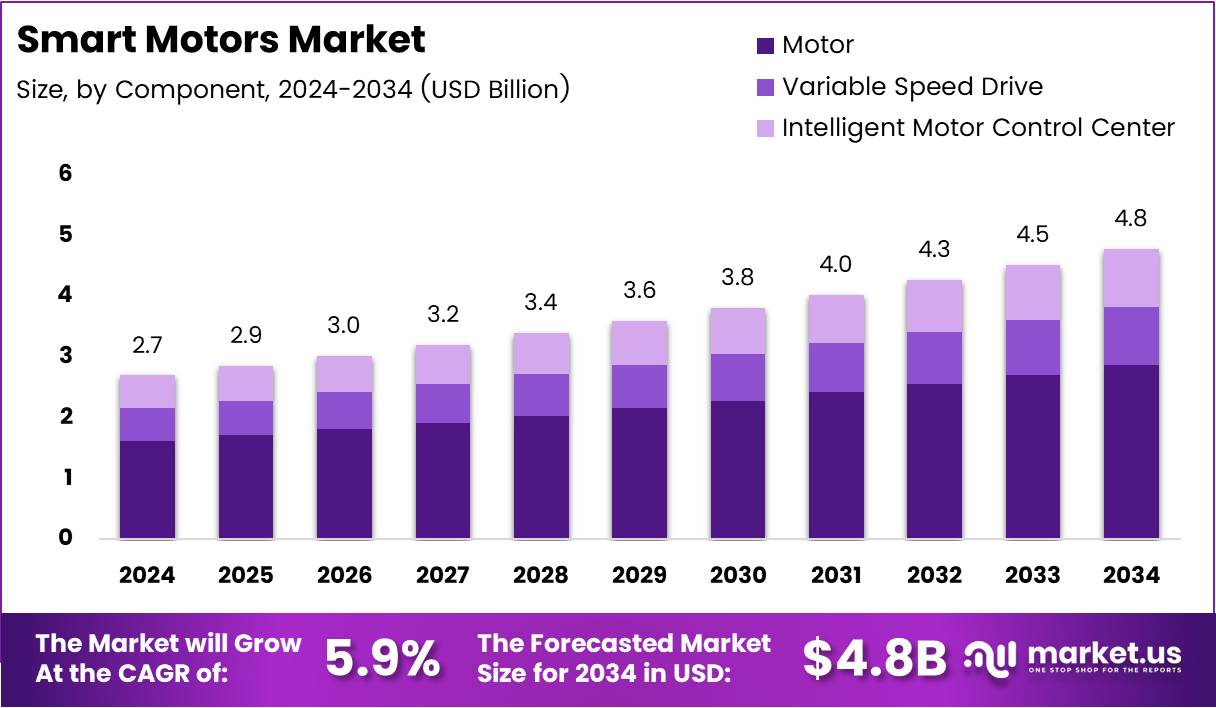

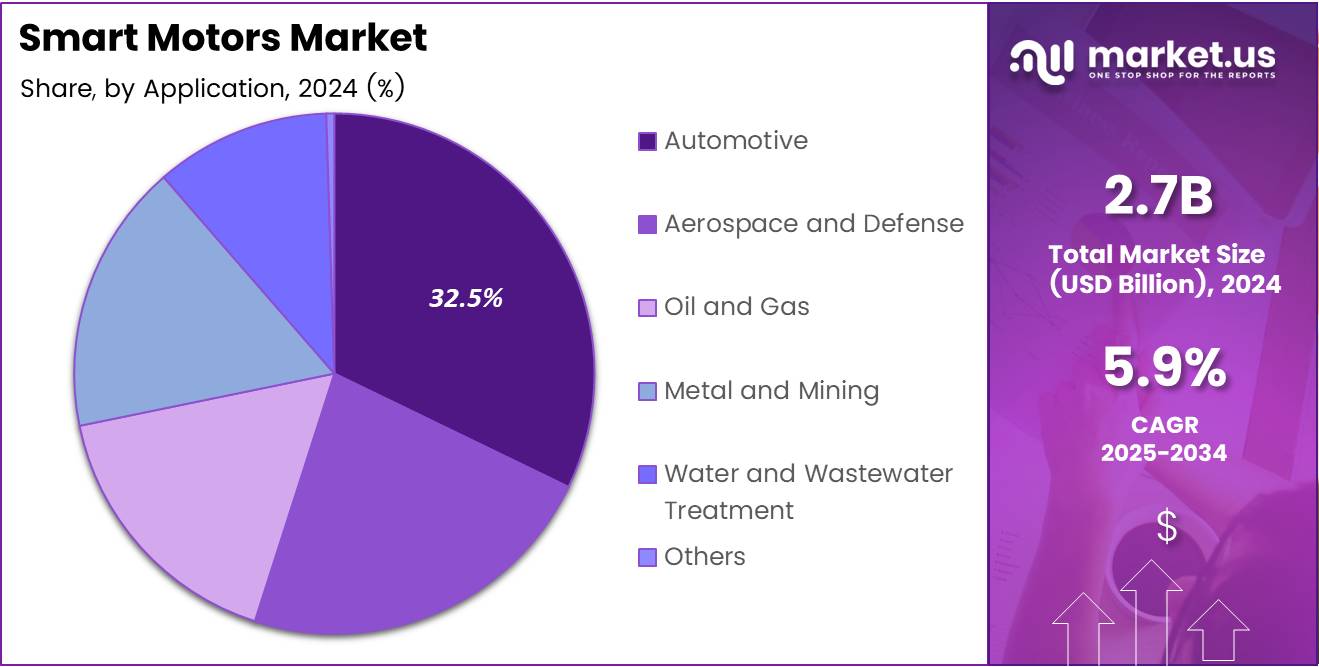

The Global Smart Motors Market size is expected to be worth around USD 4.8 Billion by 2034, from USD 2.7 Billion in 2024, growing at a CAGR of 5.9% during the forecast period from 2025 to 2034.

The Smart Motors Market is expanding rapidly due to the increasing demand for automation and energy-efficient solutions across industries. These motors are integrated with sensors, controllers, and communication interfaces to optimize performance. As industries focus on improving efficiency, the adoption of smart motors in manufacturing, automotive, and robotics is projected to grow significantly in the coming years.

Government regulations promoting energy efficiency are accelerating the growth of the smart motors market. Several governments are introducing initiatives aimed at reducing energy consumption and carbon footprints, such as offering tax incentives for businesses adopting energy-saving technologies. These regulations have led to increased investment in sustainable motor technologies, including smart motors, which contribute to these goals.

The growth opportunities in the smart motors market are substantial. Industries like automotive, aerospace, and HVAC systems are increasingly relying on smart motors to enhance performance and reduce operational costs. Moreover, the integration of the Industrial Internet of Things (IIoT) and smart grid technology in smart motors is opening up new applications. These technologies enable real-time monitoring and predictive maintenance, improving uptime and operational efficiency.

Investments from key players in the market are also driving innovation. Companies are focusing on developing next-generation smart motors that offer higher energy efficiency and greater integration with AI-based systems. As a result, the smart motors market is expected to witness sustained growth, driven by technological advancements and increased adoption across a wide range of sectors.

With the rise of automation, smart motors are anticipated to play a pivotal role in transforming industries. They provide significant advantages, including reduced downtime, better efficiency, and improved overall performance. As a result, they are expected to become a critical component in manufacturing and automation solutions, which further bolsters the market’s potential.

Key Takeaways

- The Global Smart Motors Market is expected to be worth USD 4.8 Billion by 2034, growing at a CAGR of 5.9% from 2025 to 2034.

- Motor holds a dominant position in the By Component Analysis segment, with a 45.9% share in 2024.

- 24V is the dominant product type in the market, accounting for 36.3% of the share in 2024.

- Automotive is the leading application segment, holding a 32.5% share in 2024, driven by the rise of electric vehicles.

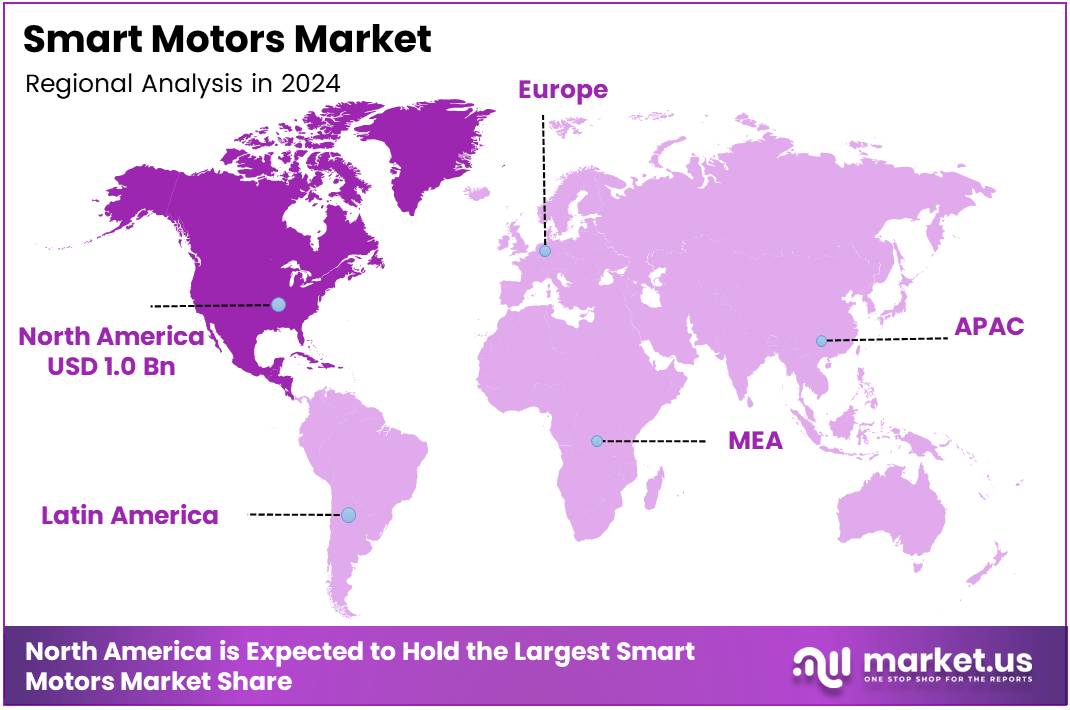

- North America holds a dominant market share of 37.8%, valued at USD 1.0 Billion in 2024.

By Component Analysis

Motor dominates with 45.9% due to its widespread usage in various applications, offering reliability and high performance.

In 2024, Motor held a dominant market position in the By Component Analysis segment of Smart Motors Market, with a 45.9% share. This high market share is attributed to the widespread use of motors in a variety of applications, including industrial automation, automotive, and home appliances, offering efficiency and durability. Motor components are essential in converting electrical energy into mechanical motion, making them a key component in various systems.

Variable Speed Drives play an important role in controlling motor speed and ensuring energy efficiency. However, they represent a smaller portion of the market in comparison to motors, contributing to the versatility of smart motor systems. These drives allow for precise speed control and energy savings, which makes them suitable for diverse industries.

Intelligent Motor Control Centers (IMCC) are also crucial for optimizing motor operations, especially in industrial settings. These systems provide centralized control and protection for electric motors, enhancing operational safety and reducing downtime. Despite their advanced functionality, IMCC systems have a smaller market share compared to motors and variable speed drives.

By Product Analysis

24V dominates with 36.3% due to its compact size and energy efficiency, making it a popular choice for various applications.

In 2024, 24V held a dominant market position in the By Product Analysis segment of Smart Motors Market, with a 36.3% share. The widespread use of 24V systems is driven by their energy efficiency and ability to power smaller, more compact devices. This voltage range is ideal for automotive, robotics, and consumer electronics, contributing to its market dominance.

18V products cater to applications requiring lower power, but they occupy a smaller share of the market. These products are commonly found in power tools and small appliances, where less power is needed. The lower cost of 18V systems also makes them attractive in specific use cases.

36V products are used in medium-sized applications, offering a balance between power and efficiency. While these systems provide more power than 24V, they are less widely adopted due to their higher energy consumption and larger form factor. They are primarily found in electric vehicles and industrial applications.

48V systems cater to high-power applications, such as electric vehicles and heavy machinery, but their adoption remains limited due to their larger size and higher energy requirements. These systems are gaining traction in electric vehicle markets, where higher efficiency and power are necessary for longer ranges.

By Application Analysis

Automotive dominates with 32.5% due to the growing demand for electric vehicles and smart mobility solutions.

In 2024, Automotive held a dominant market position in the By Application Analysis segment of Smart Motors Market, with a 32.5% share. The increasing adoption of electric vehicles (EVs) and smart mobility solutions drives the demand for smart motors in the automotive sector. These motors are essential for powering electric drivetrains and ensuring energy efficiency, aligning with the global push for sustainable transportation.

Aerospace and Defense applications utilize smart motors for precision control in aircraft systems, drones, and defense technologies. While the market share is smaller compared to automotive, the demand for highly reliable and advanced motor systems in these industries is steadily growing.

Oil and Gas applications require smart motors for automation and control in challenging environments. These motors enhance operational efficiency in drilling rigs, pipelines, and production systems. However, the segments share remains lower compared to automotive due to the specialized nature of the applications.

Metal and Mining industries rely on smart motors for automation and machinery control, where heavy-duty motors are required for operating large mining equipment. The demand for these motors is stable, but it accounts for a smaller share than automotive, driven by industry-specific requirements.

Water and Wastewater Treatment applications use smart motors for pump systems and filtration processes. These motors help reduce energy consumption and increase the operational efficiency of water treatment plants. The segment has a relatively smaller market share compared to automotive, but it is expected to grow with increasing demand for sustainable water management systems.

Other industries, such as agriculture and HVAC, also utilize smart motors for various applications. These sectors contribute to the growth of the smart motor market but hold a smaller portion of the overall market share compared to the dominant automotive segment.

Key Market Segments

By Component

- Motor

- Variable Speed Drive

- Intelligent Motor Control Center

By Product

- 24V

- 18V

- 36V

- 48.24V

By Application

- Automotive

- Aerospace and Defense

- Oil and Gas

- Metal and Mining

- Water and Wastewater Treatment

- Others

Drivers

Surge in Demand for Energy-Efficient Solutions Drives Market Growth

The smart motors market is experiencing significant momentum due to several key factors shaping industry demand. Energy efficiency has become a top priority for businesses looking to reduce operational costs and meet environmental regulations. Smart motors offer superior energy management capabilities compared to traditional motors, helping companies achieve substantial cost savings on electricity bills.

Automation and robotics advancements are revolutionizing manufacturing processes across industries. Smart motors provide precise control and real-time monitoring capabilities that are essential for modern automated systems. These motors can adjust their performance based on load requirements, making them ideal for robotic applications.

The electric vehicle revolution is creating unprecedented demand for intelligent motor systems. Smart motors in EVs offer better battery management, regenerative braking, and enhanced performance monitoring. As governments worldwide promote electric mobility, this segment continues to expand rapidly.

Industrial automation needs are growing as companies seek to improve productivity and reduce human error. Smart motors integrate seamlessly with control systems, providing operators with detailed performance data and enabling predictive maintenance. This connectivity helps prevent unexpected downtime and extends equipment lifespan, making them attractive investments for industrial facilities.

Restraints

Limited Availability of Skilled Workforce Restrains Market Expansion

Despite strong growth drivers, the smart motors market faces several challenges that could limit its expansion potential. The shortage of skilled technicians and engineers familiar with smart motor technology represents a significant barrier for many companies considering adoption.

Technical limitations in certain motor types continue to pose challenges for widespread implementation. Some smart motor designs struggle with high-temperature environments or heavy-duty applications, limiting their use in specific industries. These performance constraints require ongoing research and development to overcome.

The lack of standardization across different smart motor designs creates compatibility issues for manufacturers and end-users. Without universal standards, companies face difficulties integrating smart motors from different suppliers into their existing systems. This fragmentation increases costs and complexity for businesses looking to upgrade their equipment.

Installation and maintenance of smart motors require specialized knowledge that many traditional electricians may not possess. This skills gap forces companies to invest in additional training or hire expensive specialists, adding to the total cost of ownership. The complexity of programming and configuring these advanced systems can also deter smaller businesses from making the transition from conventional motors.

Growth Factors

Expansion of Smart Cities and Infrastructure Projects Creates Growth Opportunities

The smart motors market presents numerous growth opportunities driven by emerging technological trends and infrastructure developments. Smart city initiatives worldwide are creating substantial demand for intelligent motor systems in applications ranging from traffic management to building automation.

Renewable energy installations require sophisticated motor control systems for wind turbines, solar tracking systems, and energy storage solutions. Smart motors play a crucial role in optimizing energy generation and distribution, making them essential components in the transition to clean energy. This sector offers tremendous growth potential as governments increase renewable energy investments.

Internet of Things (IoT) and connectivity advancements are expanding the capabilities of smart motors beyond traditional applications. Enhanced wireless communication enables remote monitoring, predictive analytics, and cloud-based control systems. These technological improvements make smart motors more attractive to businesses seeking digital transformation.

The healthcare and medical equipment sector represents an emerging opportunity for smart motor manufacturers. Precision medical devices, robotic surgery systems, and automated laboratory equipment require highly accurate and reliable motor control. As healthcare technology advances, demand for specialized smart motors in medical applications continues to grow, offering manufacturers access to high-value market segments with stringent quality requirements.

Emerging Trends

Integration with AI and Machine Learning for Predictive Maintenance Shapes Market Trends

Current trends in the smart motors market reflect the industry’s evolution toward more intelligent and sustainable solutions. Artificial intelligence and machine learning integration is transforming how smart motors operate and maintain themselves. These technologies enable predictive maintenance capabilities that can identify potential failures before they occur, significantly reducing downtime costs.

Consumer electronics manufacturers are increasingly incorporating smart motors into household appliances, power tools, and personal devices. This trend is driving demand for smaller, more efficient motor designs that can operate quietly while providing precise control. The consumer market’s emphasis on user experience is pushing innovation in motor technology.

Sustainability concerns are shaping product development priorities across the industry. Manufacturers are focusing on eco-friendly motor solutions that use recyclable materials, consume less energy, and have longer operational lifespans. This environmental focus aligns with corporate sustainability goals and regulatory requirements.

The shift toward wireless and remote-controlled motor systems reflects changing user preferences and technological capabilities. Wireless connectivity eliminates the need for complex wiring installations while enabling advanced features like smartphone control and cloud-based monitoring. This trend is particularly strong in building automation and industrial IoT applications where flexibility and ease of installation are paramount.

Regional Analysis

North America Dominates the Smart Motors Market with a Market Share of 37.8%, Valued at USD 1.0 Billion

North America holds a dominant position in the Smart Motors Market with a 37.8% share, valued at USD 1.0 Billion. The market growth in this region is primarily driven by increasing demand for automation in various industrial sectors and the rapid adoption of electric vehicles. Strong investments in smart infrastructure and government incentives further fuel market expansion.

Europe Smart Motors Market Trends

Europe holds a significant share in the Smart Motors Market, driven by stringent energy efficiency regulations and the growing demand for automation in manufacturing. The region’s emphasis on green technologies and sustainability further accelerates the adoption of energy-efficient smart motors, contributing to its market growth.

Asia Pacific Smart Motors Market Trends

Asia Pacific is witnessing rapid growth in the Smart Motors Market due to strong industrialization, particularly in countries like China and India. The region is expected to continue expanding due to the increasing adoption of electric vehicles and automation in manufacturing sectors. Government support for smart technologies plays a crucial role in the market’s development.

Middle East and Africa Smart Motors Market Trends

The Middle East and Africa market for smart motors is expanding, though at a slower pace compared to other regions. Rising investments in industrial automation and energy-efficient solutions in countries like Saudi Arabia and the UAE are expected to contribute to market growth in the coming years. The region’s focus on sustainability is also aiding adoption.

Latin America Smart Motors Market Trends

Latin America’s Smart Motors Market is anticipated to grow steadily, driven by increasing industrialization and technological advancements. While the region’s market share remains relatively small, the rise in demand for energy-efficient solutions and government policies supporting innovation is expected to drive future growth.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Smart Motors Company Insights

In 2024, ABB Ltd continues to maintain a strong foothold in the global Smart Motors market, driven by its diverse portfolio of industrial automation solutions. The company is well-positioned to capitalize on the increasing demand for energy-efficient and high-performance motor solutions across various sectors, including robotics and manufacturing automation.

Dunkermotoren GmbH specializes in brushless DC motors and integrated drive systems, playing a crucial role in sectors requiring precise and reliable motion control. The company is expected to experience steady growth, driven by innovations in compact and energy-efficient solutions suited for robotics, medical devices, and industrial automation.

Fuji Electric Co., Ltd. is another key player gaining momentum in the Smart Motors market with its cutting-edge motor drive systems. Fuji Electric’s focus on integrating advanced technologies such as IoT into motor systems allows it to offer solutions that not only enhance efficiency but also support predictive maintenance, which is increasingly important in the industrial automation space.

General Electric (GE) remains a major contender in the smart motor landscape, leveraging its strong presence in both the industrial and power sectors. GE’s emphasis on digital solutions, particularly its industrial IoT platform, positions the company to provide smart motor solutions that are highly efficient, customizable, and aligned with industry 4.0 trends. This is expected to further strengthen GE’s market position in the coming years.

Top Key Players in the Market

- ABB Ltd

- Dunkermotoren GmbH

- Fuji Electric Co., Ltd.

- General Electric

- Moog, Inc.

- Nidec Corporation

- RobotShop Inc.

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

Recent Developments

- In Jul 2025, Matter Motors plans to raise $200 million to fuel its expansion efforts, with aspirations for a public listing in the next 3-4 years.

- In Sep 2025, Blue Energy Motors secured USD 30 million in funding from investors Nikhil Kamath and Omnitex Industries to further its growth.

- In May 2025, Euler Motors successfully raised Rs 6.38 billion in funding, with a key investment from Hero to support its operational scale-up.

Report Scope

Report Features Description Market Value (2024) USD 2.7 Billion Forecast Revenue (2034) USD 4.8 Billion CAGR (2025-2034) 5.9% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Component (Motor, Variable Speed Drive, Intelligent Motor Control Center), By Product (24V, 18V, 36V, 48.24V), By Application (Automotive, Aerospace and Defense, Oil and Gas, Metal and Mining, Water and Wastewater Treatment, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape ABB Ltd, Dunkermotoren GmbH, Fuji Electric Co., Ltd., General Electric, Moog, Inc., Nidec Corporation, RobotShop Inc., Rockwell Automation Inc., Schneider Electric SE, Siemens AG Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- ABB Ltd

- Dunkermotoren GmbH

- Fuji Electric Co., Ltd.

- General Electric

- Moog, Inc.

- Nidec Corporation

- RobotShop Inc.

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

Our Clients

- 159697

- Sep 2025