Quick Navigation

Report Overview

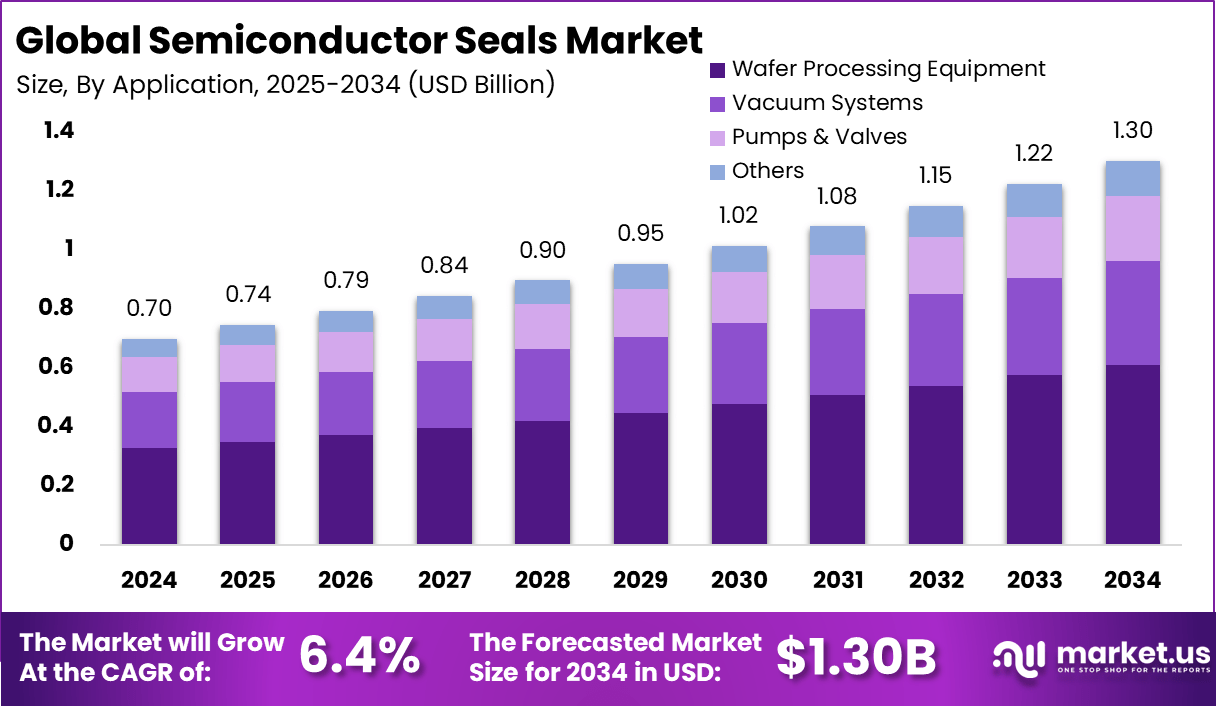

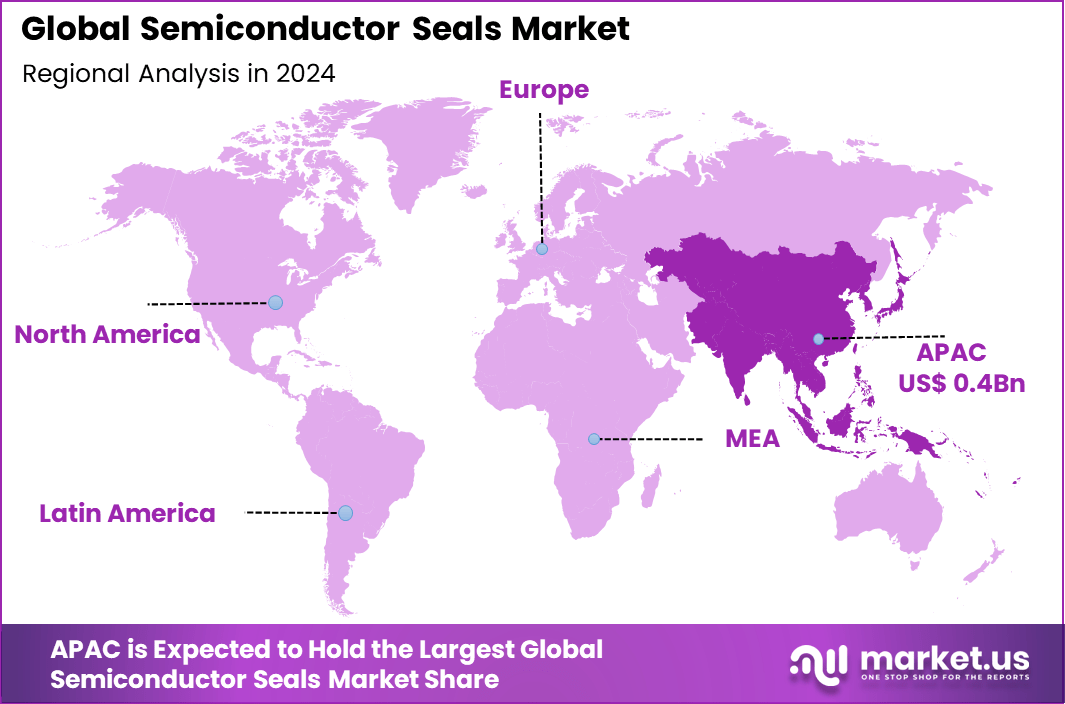

The Global Semiconductor Seals Market size is expected to be worth around USD 1.30 Billion By 2034, from USD 0.70 billion in 2024, growing at a CAGR of 6.4% during the forecast period from 2025 to 2034. In 2024, APAC held a dominant market position, capturing more than a 68% share, holding USD 0.4 Billion revenue.

Semiconductor seals are highly specialized sealing components used in semiconductor fabrication processes to prevent contamination, chemical leakage, and material loss. These seals are made from advanced materials like perfluoroelastomers (FFKM), fluoroelastomers (FKM), and polytetrafluoroethylene (PTFE), which can endure extreme conditions such as high heat, reactive plasma, and aggressive chemicals. They are installed in equipment like etching systems, deposition chambers, and chemical delivery systems.

The semiconductor seals market is witnessing strong growth, driven by increasing semiconductor production and expansion of fabrication facilities across Asia-Pacific, North America, and parts of Europe. Demand continues to rise from key application areas including wafer etching, deposition, ion implantation, and cleaning. The market is evolving with innovations in high-purity materials and next-generation sealing solutions that support advanced lithography and process nodes.

According to Market.us analysis, The Semiconductor Market reached a value of USD 530 Billion in 2023, and it is projected to grow steadily, reaching nearly USD 996 Billion by 2033. This growth is expected at a CAGR of 6.5% over the forecast period from 2024 to 2033. In 2023, Asia-Pacific emerged as the leading region, accounting for over 63.91% market share, supported by strong manufacturing hubs in countries like China, South Korea, and Taiwan.

The Global Semiconductor Materials Market was valued at USD 52.4 Billion in 2023 and is expected to expand to approximately USD 95.6 Billion by 2033, registering a CAGR of 6.2% between 2024 and 2033. This growth is driven by increasing consumption of wafers, photomasks, and CMP slurries in advanced fabrication processes.

The growth of this market can be attributed to rising demand for microelectronics, electric vehicles, 5G devices, and high-performance computing. Increasing complexity in semiconductor device architecture and a shift towards smaller node sizes are pushing the need for precision-engineered, chemically resistant, and high-temperature-tolerant sealing solutions.

Surging demand for semiconductors used in automotive, cloud computing, and IoT applications is creating pressure on chip manufacturers to increase capacity. This is directly boosting the need for dependable sealing systems that can operate under cleanroom standards. O-rings and gaskets made from fluorinated polymers are seeing increased orders due to their reliability and long service life in aggressive plasma environments.

Key Takeaways

- The Global Semiconductor Seals Market is forecasted to reach USD 1.30 Billion by 2034, up from USD 0.70 Billion in 2024.

- The market is set to expand at a steady CAGR of 6.4% from 2025 to 2034.

- In 2024, the Asia-Pacific (APAC) region led the global market with a 68% share, generating USD 0.4 Billion in revenue.

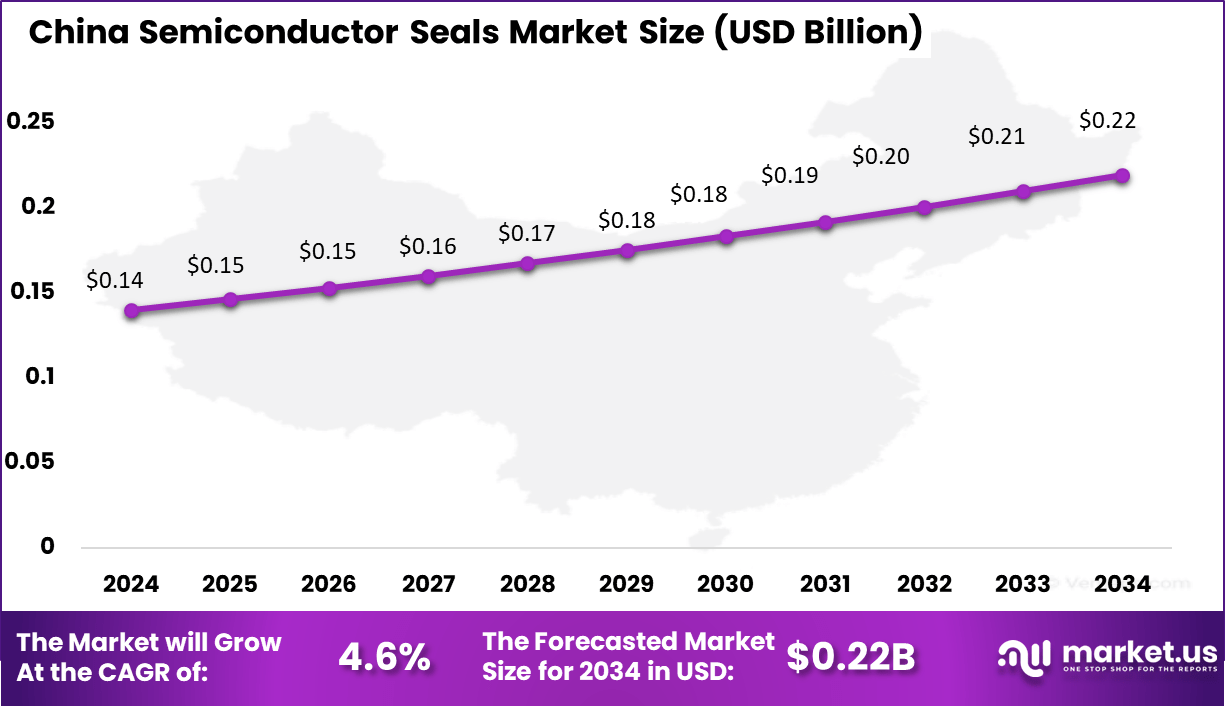

- China contributed USD 0.14 Billion in 2024 and is projected to grow at a CAGR of 4.6%.

- By material type, Fluoropolymer Seals (PTFE, PFA, FKM) accounted for the largest share at 58% in 2024.

- Within applications, Wafer Processing Equipment represented the leading segment with a 47% share.

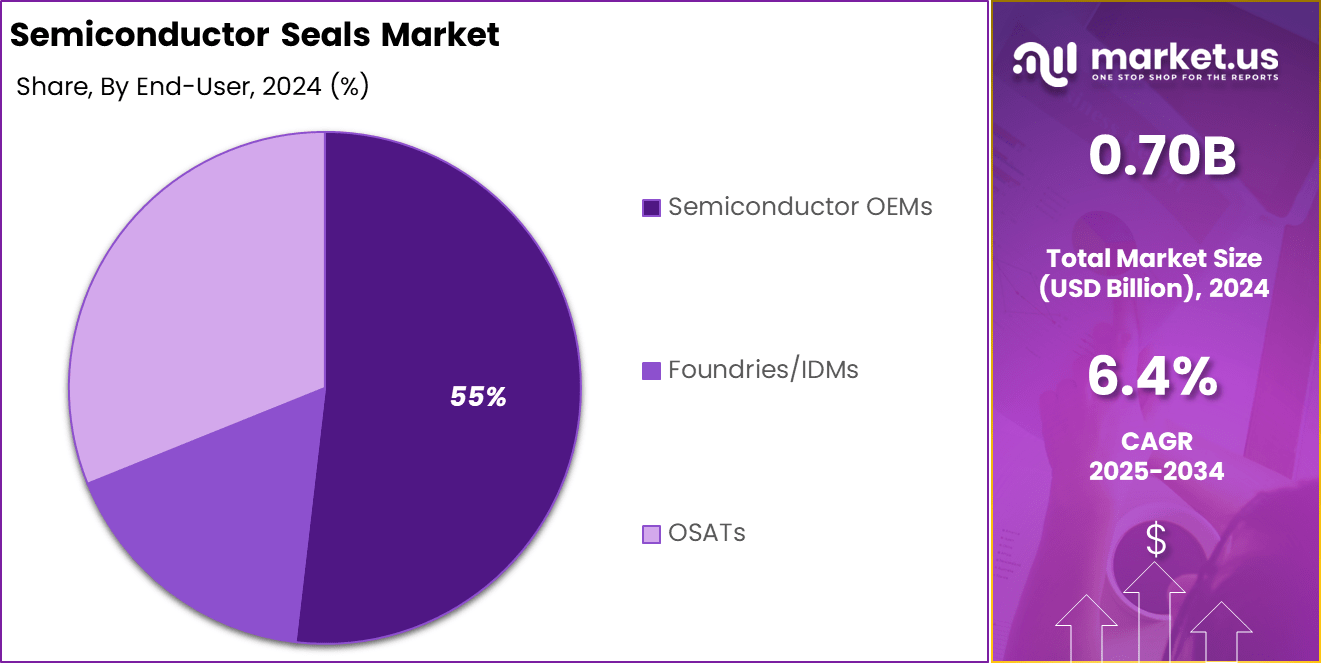

- Among end-users, Semiconductor OEMs held a dominant 55% share, reflecting their high consumption of critical sealing components.

Analysts’ Viewpoint

Advanced lithography technologies such as EUV, and the use of high-aspect-ratio etching and 3D NAND processes, are significantly increasing the performance expectations for semiconductor seals. Modern seal designs must provide low particle generation, high chemical inertness, and minimal outgassing to meet these evolving process requirements.

Investment opportunities are emerging in the development of novel seal materials, particularly PFAS-free elastomers in response to environmental regulations. Additionally, companies that innovate in plasma-resistant sealing technology and offer modular, customized sealing solutions are well-positioned to gain a competitive edge in this increasingly specialized market.

The regulatory landscape is becoming stricter, particularly in Europe and North America, with increasing focus on cleanroom certification, chemical safety, and environmental sustainability. Restrictions on hazardous materials and global initiatives to phase out PFAS-based compounds are reshaping material innovation in the sealing industry.

China Market Expansion

The China Semiconductor Seals Market is valued at approximately USD 0.14 Billion in 2024 and is predicted to increase from USD 0.18 Billion in 2029 to approximately USD 0.22 Billion by 2034, projected at a CAGR of 4.6% from 2025 to 2034.

In 2024, Asia-Pacific held a dominant market position, capturing more than a 68% share, with total revenue reaching approximately USD 0.4 Billion. This leadership can be strongly attributed to the region’s expanding semiconductor manufacturing base, especially in countries like China, South Korea, Taiwan, and Japan.

These nations have heavily invested in advanced chip production facilities, resulting in continuous demand for high-performance sealing solutions that can withstand the harsh environments inside wafer fabrication and packaging equipment.

The growing presence of local and global semiconductor fabs has created a robust and recurring demand for seals that ensure contamination control, thermal stability, and chemical resistance, making the region critical to the global supply chain.

By Material Type Analysis

In 2024, Fluoropolymer Seals (PTFE, PFA, FKM) segment held a dominant market position, capturing more than a 58 % share. This leadership is attributed to their exceptional chemical resistance, thermal stability, and non-stick properties, which are vital in high-purity semiconductor environments.

Materials such as PTFE, PFA, and FKM can resist aggressive etchants, solvents, and extreme temperatures without degrading, making them essential in demanding fabrication processes. Their low particle generation and non-contaminating nature support advanced node manufacturing, causing this material class to command the majority of demand.

The dominance of fluoropolymer seals is further strengthened by their wide application across critical semiconductor processes, including CVD, PVD, etching, and cleaning. PTFE’s hydrophobic and inert nature ensures minimal interaction with process chemicals, while PFA adds improved moldability and mechanical strength. FKM offers a reliable balance of temperature performance and cost efficiency, making it the go-to choice for many OEMs.

By Application Analysis

In 2024, Wafer Processing Equipment segment held a dominant market position, capturing more than a 47 % share of the semiconductor seals market. This leadership is underpinned by the intensive demand for high-purity seals within wafer fabrication tools – such as etchers, chemical vapor deposition systems, plasma chambers, and ion implanters – where maintaining contamination-free environments is vital.

Each piece of wafer equipment relies heavily on seals to prevent microscopic contamination; even slight leaks can result in costly yield losses. As a result, wafer processing continues to be the primary application area for advanced sealing technology.

The segment’s dominance in 2024 is further driven by ongoing expansion of wafer fabs worldwide, particularly across Asia-Pacific and North America, which is fueling orders for cutting-edge wafer process systems. These systems require seals capable of withstanding extreme conditions – high vacuum, elevated temperature, plasma exposure, and harsh chemical cleaning cycles.

The substantial investment in tool precision and reliability promotes the adoption of top-tier seal materials, reinforcing wafer processing’s leading role. The narrow tolerances and high volume requirements inherent to wafer manufacturing ensure that this application segment remains the key growth driver for seal manufacturers.

By End-User Analysis

In 2024, Semiconductor OEMs segment held a dominant market position, capturing more than a 55 % share of the semiconductor seals market. This leading role is attributed to OEMs’ responsibility for integrating sealing solutions directly into semiconductor fabrication and assembly tools. These manufacturers prioritize seals that adhere to the highest standards of cleanliness, chemical compatibility, and mechanical reliability to ensure consistent equipment uptime and optimal chip yields.

Because OEM tool designs demand precise engineering and long-term performance under extreme process conditions, they commission high‑specification seals touting the latest materials and advanced manufacturing techniques – traits that reinforce their dominant market share. The substantial footprint of OEMs in the market is further supported by global fab expansion and recurring investments in next‑generation manufacturing platforms.

As fabs adopt EUV lithography, advanced packaging, and heterogeneous integration, OEMs increasingly require tailored sealing solutions to maintain vacuum integrity, withstand harsh plasmas, and prevent wafer-level contamination. These stringent engineering demands compel OEMs to collaborate closely with seal manufacturers, fostering innovation and customization that smaller end‑users such as foundries and OSATs cannot match.

Key Market Segments

By Material Type

- Fluoropolymer Seals (PTFE, PFA, FKM)

- Elastomer Seals (FFKM, EPDM, Silicone)

- Metal Seals (Stainless Steel, Copper)

- Ceramic & Hybrid Seals

By Application

- Wafer Processing Equipment

- Vacuum Systems

- Pumps & Valves

- Others

By End-User

- Semiconductor OEMs

- Foundries/IDMs

- OSATs

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Market Dynamics

| Category | Description |

|---|---|

| Emerging Trend | Custom-engineered FFKM with integrated production monitoring enhances seal reliability and contamination control. |

| Driver | Rising complexity in semiconductor processes and global fab expansion demand advanced sealing solutions. |

| Restraint | High cost of specialty elastomers and precision manufacturing constrains usage to high-end fabs. |

| Opportunity | Sustainable seal materials and new process-specific applications (EUV, heterogeneous integration) offer expansion potential. |

| Challenge | Supply chain fragility and material-cost competition require strong resilience and innovation. |

Key Player Analysis

DuPont de Nemours has strengthened its position in semiconductor sealing by launching its latest Kalrez® perfluoroelastomer components at SEMICON Southeast Asia in May 2025. These new products – such as bonded door seals – offer reduced leaks, part generation, and maintenance downtime, enhancing fab efficiency and sustainability.

Greene Tweed & Co. has proactively addressed past material shortages by expanding its global supply chain and ramping production of Chemraz® FFKM seals. The company restored lead times for semiconductor customers by building raw-material stockpiles, diversifying sourcing, and adding capacity – particularly with a new Korean facility slated for mid‑2025.

Parker Hannifin, Valqua, Trelleborg, Daikin, MNE, Precision Polymer Engineering, EnPro, Saint‑Gobain, Bal Seal Engineering, Technetics, John Crane, and other key players have advanced their semiconductor seal portfolios through strategic mergers, targeted acquisitions, or niche product launches in 2025.

Top Key Players Covered

- DuPont de Nemours

- Greene Tweed & Co., Ltd.

- PARKER HANNIFIN CORP

- Valqua Ltd.

- Trelleborg SE

- Daikin Industries, Ltd.

- MNE Co., Ltd.

- Precision Polymer Engineering Limited

- EnPro Industries, Inc.

- Saint-Gobin

- Bal Seal Engineering

- Technetics Group

- John Crane

- Other Key Players

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 0.70 Bn |

| Forecast Revenue (2034) | USD 1.30 Bn |

| CAGR (2025-2034) | 6.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Material Type (Fluoropolymer Seals (PTFE, PFA, FKM), Elastomer Seals (FFKM, EPDM, Silicone), Metal Seals (Stainless Steel, Copper), Ceramic & Hybrid Seals), By Application (Wafer Processing Equipment, Vacuum Systems, Pumps & Valves, Others), By End-User (Semiconductor OEMs, Foundries/IDMs, OSATs) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | DuPont de Nemours, Greene Tweed & Co., Ltd., PARKER HANNIFIN CORP, Valqua Ltd., Trelleborg SE, Daikin Industries, Ltd., MNE Co., Ltd., Precision Polymer Engineering Limited, EnPro Industries, Inc., Saint-Gobin, Bal Seal Engineering, Technetics Group, John Crane, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |