Quick Navigation

- Report Overview

- Key Takeaways

- US Tariff Impact Analysis

- U.S. Market Size

- Applications of Military Semiconductors

- Component Analysis

- Application Analysis

- Technology Analysis

- End-User Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Emerging Trends

- Business Benefits

- Key Player Analysis

- Top Opportunities for Players

- Recent Developments

- Report Scope

Report Overview

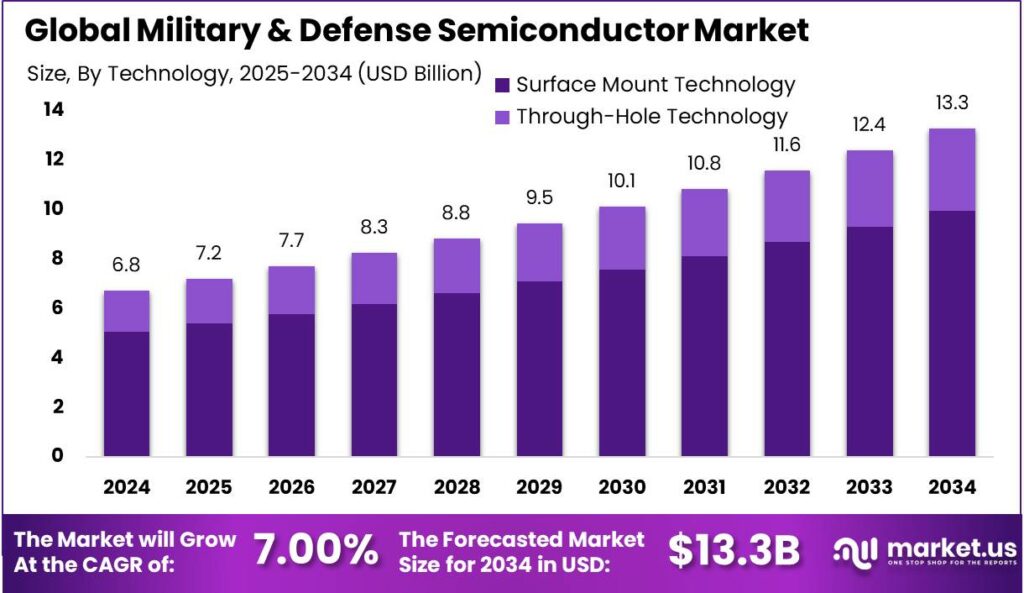

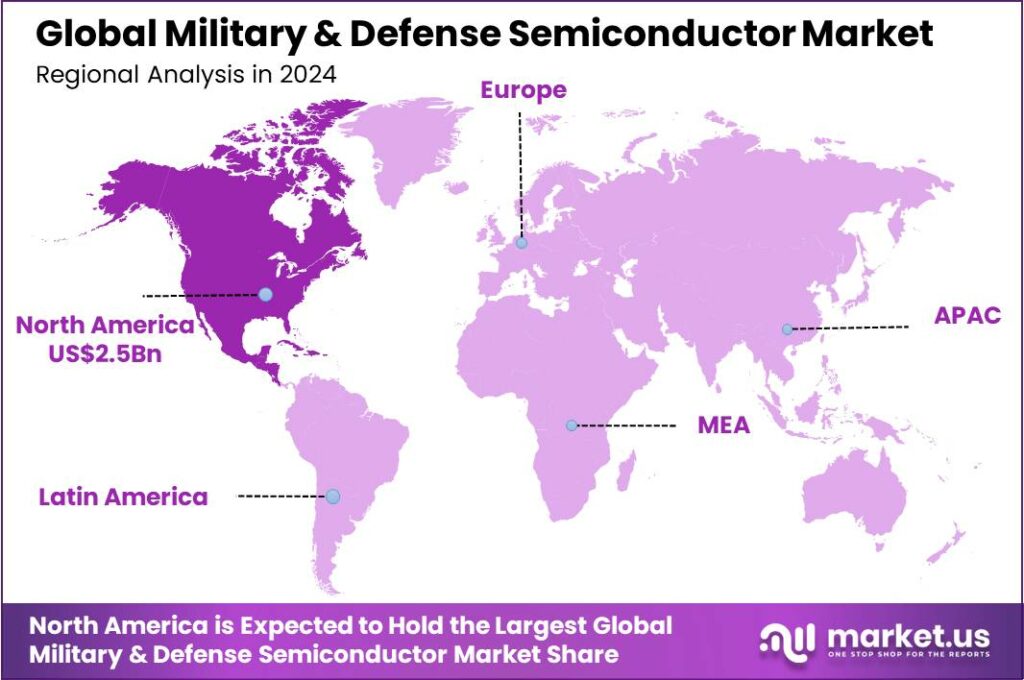

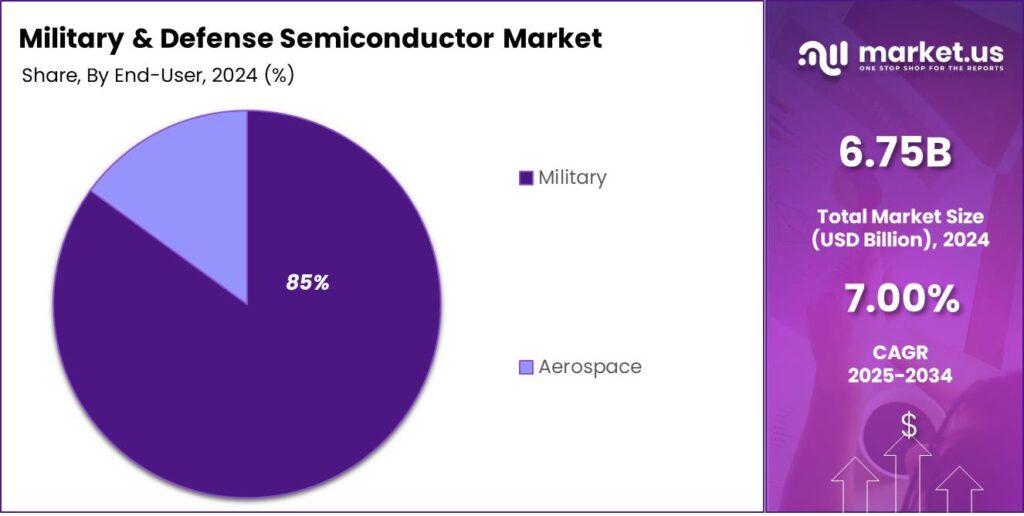

The Global Military & Defense Semiconductor Market size is expected to be worth around USD 13.3 Billion By 2034, from USD 6.75 Billion in 2024, growing at a CAGR of 7.00% during the forecast period from 2025 to 2034. North America was the largest market for Military & Defense Semiconductors in 2024, accounting for more than 38% of the market, with revenues amounting to USD 2.5 billion.

The military and defense semiconductor market refers to the specialized segment of the semiconductor industry dedicated to producing highly reliable, rugged, and secure chips suited to the stringent requirements of defense applications. These chips form the backbone of advanced weapon systems, secure communications, satellite infrastructure, UAVs, electronic warfare, and an array of mission-critical military electronics.

One of the strongest forces propelling this market forward is the ongoing modernization of military forces globally. Defense agencies are constantly pressured to maintain superiority through advanced technology, and semiconductors lie at the heart of this mission. Another major driver is the growing demand for secure and resilient communications networks vital for effective battlefield awareness and rapid, coordinated responses.

Scope and Forecast

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 6.8 Bn |

| Forecast Revenue (2034) | USD 13.3 Bn |

| CAGR (2025-2034) | 7.0% |

| Largest Segment | Military segment [85%] |

| Largest Market | North America [38% Market Share] |

| Largest Country | U.S. [2.4 Billion Market Revenue] |

The demand for military and defense semiconductors is rising sharply, driven by the push for next-generation capabilities. There is a notable preference for chips that function reliably in extreme temperatures, high-radiation zones, and rapidly changing environments. The urgency around secure and resilient communication networks, as well as the increasing use of unmanned systems and autonomous vehicles, creates extra pressure for chips that are both high-performance and energy-efficient.

According to Market.us, The global semiconductor market has displayed substantial growth, with its valuation expected to increase significantly from USD 530 billion in 2023 to approximately USD 996 billion by 2033, reflecting a healthy compound annual growth rate (CAGR) of 6.5% during the forecast period from 2024 to 2033. The growth is driven by rising demand in sectors like automotive, consumer electronics, and industrial automation, which rely on advanced semiconductor technologies.

The Semiconductor Industry Association (SIA) reported a notable surge in sales during the third quarter of 2024, with the market reaching USD 166.0 billion, marking a remarkable 23.2% year-on-year increase. This performance further reflects a 10.7% growth over the preceding quarter of the same year. The sales momentum continued into September 2024, with a total of USD 55.3 billion, a 4.1% increase compared to USD 53.1 billion in August

Key Takeaways

- The Global Military & Defense Semiconductor Market size is projected to reach USD 13.3 Billion by 2034, growing from USD 6.75 Billion in 2024, with a CAGR of 7.00% during the forecast period from 2025 to 2034.

- In 2024, the Microprocessors & Microcontrollers segment dominated the Military & Defense Semiconductor market, capturing more than 28% of the total market share.

- The Radar & Surveillance Systems segment also held a dominant position in 2024, accounting for over 27% of the market share.

- Surface Mount Technology (SMT) led the Military & Defense Semiconductor market in 2024, capturing more than 75% of the market share.

- In 2024, the Military segment of the Military & Defense Semiconductor Market held a dominant position, commanding over 85% of the market share.

- North America was the largest market for Military & Defense Semiconductors in 2024, accounting for more than 38% of the market, with revenues amounting to USD 2.5 billion.

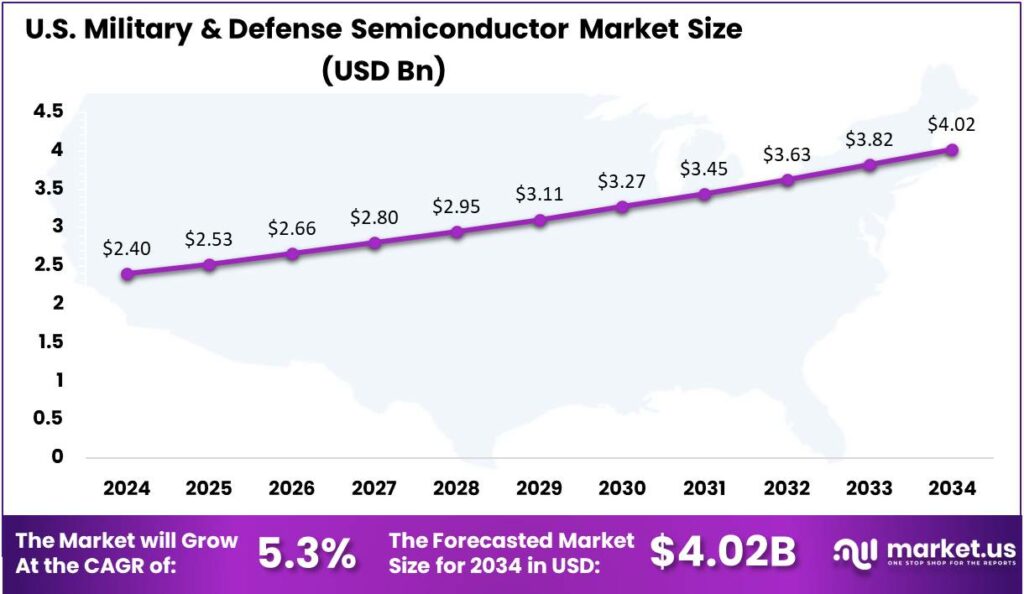

- The U.S. Military & Defense Semiconductor Market was valued at USD 2.4 billion in 2024, with a projected CAGR of 5.3% over the forecast period.

US Tariff Impact Analysis

The new tariffs imposed by U.S. President Donald Trump could indeed have significant financial repercussions for U.S. semiconductor equipment manufacturers. According to industry calculations, these tariffs may cost the sector more than $1 billion annually. This impact stems from the increased costs of imported components and materials which are crucial for manufacturing semiconductor equipment.

The impact of the U.S. 25% tariff on semiconductors is multifaceted and significant, affecting various aspects of the electronics supply chain, consumer prices, and global trade dynamics.

- Cost Increase and Consumer Impact: The imposition of a 25% tariff on semiconductors, particularly from major manufacturing hubs like Taiwan, South Korea, and China, is expected to significantly increase the costs of these critical components. Companies such as Apple, NVIDIA, and Tesla that rely heavily on these imports for their products will face increased production costs.

- Supply Chain Disruptions: The tariffs are prompting companies to reconsider their global supply chain strategies. There is a push towards diversifying supply sources or increasing domestic production to mitigate the risks posed by these tariffs. However, transitioning supply chains is complex and time-consuming, especially in semiconductor manufacturing, which involves sophisticated and costly facilities

- Geopolitical and Trade Implications: The tariffs have strained trade relations, particularly with Asia where the bulk of semiconductor manufacturing is located. This may lead to a geopolitical reshuffling as countries like Taiwan and South Korea, significant players in the semiconductor industry, reassess their trade strategies with the U.S. Additionally, other nations may strengthen their semiconductor collaborations, potentially isolating the U.S. from certain global supply chains.

- Impact on U.S. Manufacturing and Innovation: While the tariffs are intended to boost domestic semiconductor production and reduce reliance on foreign chips, the actual capacity to scale up U.S. manufacturing to meet current demands is limited. Most advanced semiconductor production still occurs overseas, and establishing competitive manufacturing facilities in the U.S. requires substantial investment and time

- Broader Economic Impact: The broader economic repercussions are considerable, extending beyond electronics to impact sectors like automotive and consumer goods, where semiconductors are increasingly crucial. The cost increase due to tariffs is expected to ripple through these industries, potentially leading to higher prices and reduced consumer spending.

U.S. Market Size

The U.S. Military & Defense Semiconductor Market experienced a valuation of USD 2.4 billion in the year 2024. This market is projected to grow at a compound annual growth rate (CAGR) of 5.3% over the forecast period. The steady growth is driven by rising demand for advanced electronics in military communication, weaponry, and surveillance systems.

Several factors drive this growth, notably the technological advancements in semiconductor manufacturing which improve the performance and reliability of military equipment. The U.S. Department of Defense continues to invest heavily in upgrading its defense capabilities, which includes incorporating state-of-the-art semiconductors that enhance the functionality of critical defense systems.

The market’s expansion is also supported by the development of next-generation semiconductor technologies such as silicon carbide (SiC) and gallium nitride (GaN). These materials, valued for their heat resistance and efficiency, are well-suited for harsh military environments. As the technology matures, they are expected to drive market growth by enabling more powerful and dependable military electronics that meet strict defense standards.

In 2024, North America held a dominant market position in the Military & Defense Semiconductor market, capturing more than a 38% share, with revenues amounting to USD 2.5 billion. This leadership can primarily be attributed to the substantial investments made by the United States government in defense capabilities and the presence of major defense contractors and technology firms specializing in advanced semiconductor technology.

Furthermore, North America benefits from a well-established technological infrastructure and robust R&D ecosystems that foster innovation in semiconductor design and manufacturing. These factors contribute to the development of sophisticated military applications, including smart weaponry, radar systems, and communication devices, all of which require specialized semiconductor solutions.

The ongoing research collaborations between defense agencies and technology companies in the region further strengthen its market leadership by speeding up the introduction of innovative semiconductor technologies into the military domain. The strategic governmental policies aimed at maintaining technological superiority over other nations also play a crucial role.

Initiatives that support local semiconductor manufacturing to reduce reliance on foreign electronic components in critical defense technology further propel the market’s growth in North America. Rising global tensions are heightening the focus on reliable, advanced military infrastructure, driving sustained investment and growth in the region’s Military & Defense Semiconductor market.

Applications of Military Semiconductors

- Communication Systems: Semiconductors power advanced radios, satellite communications, and network infrastructure, enabling fast, secure, and reliable data transmission essential for battlefield coordination and command control.

- Radar Systems: They are used in high-frequency amplifiers and signal processors for radar, allowing accurate detection, tracking of targets, and enhanced situational awareness even in difficult weather conditions.

- Navigation Systems: Semiconductor-based sensors and microcontrollers support precise navigation for airborne, underwater, and space applications, including GPS and inertial navigation systems.

- Electronic Warfare: Semiconductors enable electronic countermeasures that disrupt enemy communication and radar, providing a tactical advantage in electronic warfare environments.

- Missile Guidance: Semiconductor sensors and processors calculate trajectories and guide missiles with high accuracy toward targets.

Component Analysis

In 2024, the Microprocessors & Microcontrollers segment held a dominant market position within the Military & Defense Semiconductor market, capturing more than a 28% share. This leadership can be attributed to their crucial role in processing and controlling operations across a wide range of military equipment, from advanced communication systems to control units in weapon systems.

Field-Programmable Gate Arrays (FPGAs) also represent a significant component of the market, valued for their flexibility and adaptability. FPGAs are extensively used in military applications due to their ability to be reprogrammed in the field, catering to specific needs and missions without the need for complete hardware redesigns.

Application-Specific Integrated Circuits (ASICs) are tailored to meet specific application requirements, ensuring optimal performance and reliability in bespoke military applications. Their use in surveillance systems, encrypted communications, and guided missiles is vital due to their enhanced processing capabilities and resistance to harsh environments and potential security threats.

Memory Chips and RF Semiconductors are crucial components Memory Chips ensure durable data storage in extreme conditions, while RF Semiconductors enable radar, communication, and electronic warfare systems. Both are vital for mission success, ensuring data integrity and secure communication across platforms.

Application Analysis

In 2024, the Radar & Surveillance Systems segment held a dominant market position, capturing more than a 27% share. This leadership can be attributed to the increasing global emphasis on enhancing national security and airspace monitoring capabilities.

The rise in geopolitical tensions and the need for advanced border surveillance have significantly driven investments in radar and surveillance technologies. These systems heavily rely on sophisticated semiconductors to improve detection accuracy and real-time data processing, thereby boosting the demand for high-performance semiconductor components.

Electronic Warfare (EW) and jamming systems are vital to modern defense, aiming to disrupt enemy communications and radar. The growing demand for semiconductors in this field is driven by the need for advanced signal processing and jamming resistance. Innovations in semiconductor tech have led to more compact, efficient systems, fueling rapid growth in this strategic defense segment.

Military Communication Systems are essential for command and control, relying on secure, high-speed semiconductor devices. As communication tech advances, the need for reliable, robust systems grows, driving demand for semiconductors that ensure secure, uninterrupted data transmission in challenging environments.

Technology Analysis

In 2024, Surface Mount Technology (SMT) held a dominant market position in the Military & Defense Semiconductor market, capturing more than a 75% share. SMT leads due to its advantages in size reduction, reliability, and manufacturing efficiency. By mounting components directly onto PCBs, it enables more compact, lightweight, and energy-efficient electronic devices.

Additionally, SMT supports the trend toward miniaturization in defense electronics. As technology advances, the demand grows for smaller, more powerful components. SMT enables compact designs without compromising performance, making it ideal for drones, portable communication devices, and wearable tech, while enhancing system functionality and integration.

SMT technology enhances production speed and offers higher circuit speeds, which are essential in defense operations for faster and more reliable military communication and control systems. The ability to rapidly produce large volumes of PCBs with high precision and reduced error rates contributes to its widespread adoption in the military sector.

The integration of SMT in semiconductor manufacturing supports cost-effective production while maintaining high quality. By reducing drilling and assembly steps, SMT cuts costs, making it a preferred choice for defense electronics where budget efficiency and strict quality standards are essential.

End-User Analysis

In 2024, the Military segment of the Military & Defense Semiconductor Market held a dominant market position, capturing more than an 85% share. This significant market share can be attributed to several key factors that underscore the critical role semiconductors play in modern military applications.

The increasing complexity and sophistication of military equipment drive the demand for advanced semiconductors. Modern warfare and defense systems rely heavily on electronic systems for communication, navigation, and weaponry. Semiconductors serve as the backbone for these technologies, enabling enhanced capabilities in radar, surveillance, and unmanned systems.

The global drive for military modernization has expanded semiconductor applications, from secure communications to missile guidance. These systems rely on high-performance, durable components, making reliable, high-quality semiconductors essential for demanding military environments.

Furthermore, the trend of military automation and the use of artificial intelligence (AI) in defense strategies have propelled the use of semiconductors. AI applications require substantial processing power, which is provided by semiconductors. As militaries invest in AI for data analysis, decision-making, and autonomous operations, the reliance on semiconductor technology has grown exponentially.

Key Market Segments

By Component

- Microprocessors & Microcontrollers

- Field-Programmable Gate Arrays (FPGAs)

- Application-Specific Integrated Circuits (ASICs)

- Memory Chips

- RF Semiconductors

- Others

By Application

- Radar & Surveillance Systems

- Electronic Warfare (EW) & Jamming Systems

- Military Communication Systems

- Unmanned Systems (UAVs, UGVs, UUVs)

- Space & Satellite Defense Systems

- Cybersecurity & Secure Computing

- Missile Guidance & Navigation

By Technology

- Surface Mount Technology

- Through-Hole Technology

By End-User

- Military

- Aerospace

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Rising Demand for Advanced Military Electronics

The military and defense semiconductor market is rapidly growing due to rising demand for advanced electronics in modern warfare. Evolving defense strategies are driving the need for cutting-edge technologies like radar, communications, navigation, and electronic warfare systems.

Semiconductors are essential in modern defense tech, enabling better performance, miniaturization, and energy efficiency. The rise of AI, IoT, and data analytics in military operations boosts demand for high-performance chips, supporting real-time processing, autonomy, and enhanced battlefield awareness.

Modernizing military equipment like UAVs and missile systems depends on advanced semiconductors for enhanced capabilities. Ongoing R&D investments by defense agencies and industry players highlight their strategic role in national security, driving continued market growth.

Restraint

Stringent Regulatory Environment

One significant restraint in the military and defense semiconductor market is the stringent regulatory environment governing defense technologies. Compliance with various national and international regulations, such as export control laws and security standards, poses challenges for semiconductor manufacturers.

These regulations are designed to prevent the proliferation of sensitive technologies and ensure that critical components do not fall into the hands of adversaries. Navigating compliance requirements, export restrictions, and strict military-grade testing can be costly and time-consuming for semiconductor companies.

These regulatory demands limit market access, increase operational costs, and slow innovation. While crucial for national security, they also pose significant barriers to growth in the military and defense semiconductor market.

Opportunity

Collaborative International Initiatives

The military and defense semiconductor market offers growth opportunities through international collaborations. Initiatives like the U.S.–India iCET highlight joint efforts to advance semiconductor manufacturing and develop critical emerging technologies.

As part of the iCET initiative, the U.S. and India plan to build semiconductor fabs in India to support national security. These plants will produce silicon carbide, infrared, and gallium nitride chips key components for high-voltage power electronics, advanced communications, and military-grade sensors.

The collaboration involves creating design hubs, testing centers, and centers of excellence, backed by U.S. investments and tech transfers. These efforts strengthen the supply chain, boost self-reliance, and enhance resilience to geopolitical risks, unlocking new growth opportunities in the military and defense semiconductor sector.

Challenge

Supply Chain Vulnerabilities

The military and defense semiconductor market faces significant challenges due to supply chain vulnerabilities.The global semiconductor supply chain is complex and concentrated in specific regions, making it vulnerable to disruptions.

Natural disasters, geopolitical tensions, and pandemics can significantly affect the availability of critical semiconductor components. Reliance on a few suppliers for military-grade semiconductors creates risks of shortages and delays, while the semiconductor industry’s cyclical nature leads to inventory imbalances and production bottlenecks.

These issues are critical for defense, where timely components are vital for mission readiness. Efforts to diversify suppliers, invest in domestic manufacturing, and improve supply chain transparency aim to address these challenges, but building a resilient supply chain remains complex.

Emerging Trends

The military and defense sectors are transforming with advancements in semiconductor technology, particularly the integration of nanoscale semiconductors. These enable the development of compact, energy-efficient devices essential for applications like UAVs and portable communication systems, boosting operational efficiency and mobility.

Flexible electronics represent another emerging trend, allowing for the creation of adaptable and lightweight military equipment. This flexibility is particularly beneficial for wearable technologies and foldable communication devices, providing soldiers with enhanced situational awareness and communication capabilities.

Quantum computing is poised to revolutionize defense systems by offering unprecedented processing power. This advancement enables real-time data analysis and decision-making, essential in complex combat scenarios. The integration of quantum technologies into defense applications further highlights the strategic importance of semiconductors in gaining a competitive edge.

Business Benefits

The evolution of semiconductor technology in defense creates significant business opportunities. Growing demand for advanced semiconductors fuels expansion in the defense electronics market, prompting increased R&D investments. Semiconductor companies can capitalize on this by developing innovative solutions tailored to defense needs.

The strategic importance of semiconductors has led to significant government investments aimed at strengthening domestic manufacturing capabilities. For instance, the U.S. Department of Defense has allocated substantial funds to enhance microelectronics production, fostering a robust supply chain and reducing reliance on foreign sources.

The integration of semiconductors in defense systems also promotes the development of dual-use technologies, which have applications in both military and civilian sectors. This versatility opens avenues for businesses to diversify their product offerings and tap into various industries, including telecommunications, aerospace, and automotive.

Key Player Analysis

Semiconductors are key components in various defense applications, including radar systems, communication devices, avionics, and missile guidance systems.

Northrop Grumman is a significant player in the defense semiconductor industry. Known for its advanced electronics and aerospace technologies, Northrop Grumman designs and manufactures critical systems that rely heavily on semiconductors. The company’s expertise in defense electronics, cybersecurity, and space systems makes it a key contributor to the military semiconductor market.

Raytheon Technologies is a global leader in defense and aerospace technologies, providing cutting-edge solutions to military forces around the world. Raytheon is a key player in the semiconductor space, providing components for missile defense, communications, and radar systems. The company focuses on innovation, developing semiconductors that endure extreme conditions and offer superior performance in critical defense applications.

Lockheed Martin Corporation is a dominant force in the defense sector and a major player in military semiconductor solutions. The company is known for its work on fighter jets, missile systems, and other high-tech defense equipment that require advanced semiconductor technologies. Lockheed Martin’s semiconductors are crucial to the functionality of various military systems, including avionics and radar technologies.

Top Key Players in the Market

- Northrop Grumman Corporation

- Raytheon Technologies Corporation

- Lockheed Martin Corporation

- BAE Systems

- Intel Corporation

- NXP Semiconductors

- Analog Devices, Inc. (ADI)

- Microchip Technology Inc.

- Xilinx (AMD)

- Infineon Technologies

- Texas Instruments (TI)

- STMicroelectronics

- Qorvo Inc.

- Teledyne Technologies Inc.

- Other Key Players

Top Opportunities for Players

The Military & Defense Semiconductor market presents numerous opportunities for growth and innovation.

- Artificial Intelligence and Machine Learning Integration: The incorporation of AI and ML technologies into military systems represents a significant opportunity. Advanced defense technologies rely on specialized semiconductor chips to process large amounts of data, essential for autonomous systems, surveillance, and decision-making. The growing use of AI in defense is fueling demand for semiconductor solutions that boost operational capabilities.

- Advancements in Communication Technologies: The military’s need for advanced communication technologies is expanding, driven by the requirements for secure, reliable, and rapid data transmission. This includes the development of semiconductors that can support 5G and other high-speed communication protocols, which are crucial for modern military communications and tactical operations.

- Miniaturization of Electronics: There is a growing demand for smaller, more power-efficient semiconductor components that can be integrated into a variety of portable military devices. This trend towards miniaturization supports the development of compact and efficient devices crucial for modern warfare, where mobility and the integration of multiple functions into single devices are vital.

- Radiation-Hardened and High-Reliability Semiconductors: The development of radiation-hardened semiconductors is critical, particularly for space and nuclear applications. High-reliability semiconductors, designed to endure extreme environments, are crucial for critical defense operations. With the rise of military space missions and nuclear deterrence technologies, the demand for these specialized semiconductors is growing.

- Increased Government Spending on Defense: Global increases in defense budgets are enabling the adoption of cutting-edge technologies in the military sector. This financial backing is essential for driving the development and integration of advanced semiconductor technologies in military and defense systems, thereby creating a robust market demand.

Recent Developments

- In October 2024, Raytheon, an RTX business, won a three-year, two-phase contract from DARPA to develop ultra-wide bandgap semiconductors (UWBGS). These semiconductors, using diamond and aluminum nitride materials, aim to enhance power delivery and thermal management in sensors and electronic applications.

- In July 2024, Lockheed Martin partnered with GlobalFoundries to strengthen the U.S. semiconductor supply chain. This collaboration aims to enhance domestic production capabilities for defense applications.

Report Scope

| Report Features | Description |

|---|---|

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Component (Microprocessors & Microcontrollers, Field-Programmable Gate Arrays (FPGAs), Application-Specific Integrated Circuits (ASICs), Memory Chips, RF Semiconductors, Others), By Application (Radar & Surveillance Systems, Electronic Warfare (EW) & Jamming Systems, Military Communication Systems, Unmanned Systems (UAVs, UGVs, UUVs), Space & Satellite Defense Systems, Cybersecurity & Secure Computing, Missile Guidance & Navigation), By Technology (Surface Mount Technology, Through-Hole Technology), By End-User (Military, Aerospace) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Northrop Grumman Corporation, Raytheon Technologies Corporation, Lockheed Martin Corporation, BAE Systems, Intel Corporation, NXP Semiconductors, Analog Devices, Inc. (ADI), Microchip Technology Inc., Xilinx (AMD), Infineon Technologies, Texas Instruments (TI), STMicroelectronics, Qorvo Inc., Teledyne Technologies Inc., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |