Quick Navigation

- Report Overview

- Key Takeaways

- Analysts’ Viewpoint

- U.S. Market Forecast Expansion

- By Type Analysis

- By Product Type Analysis

- By Propulsion System Analysis

- By Application Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Player Analysis

- Recent Developments

- Report Scope

Report Overview

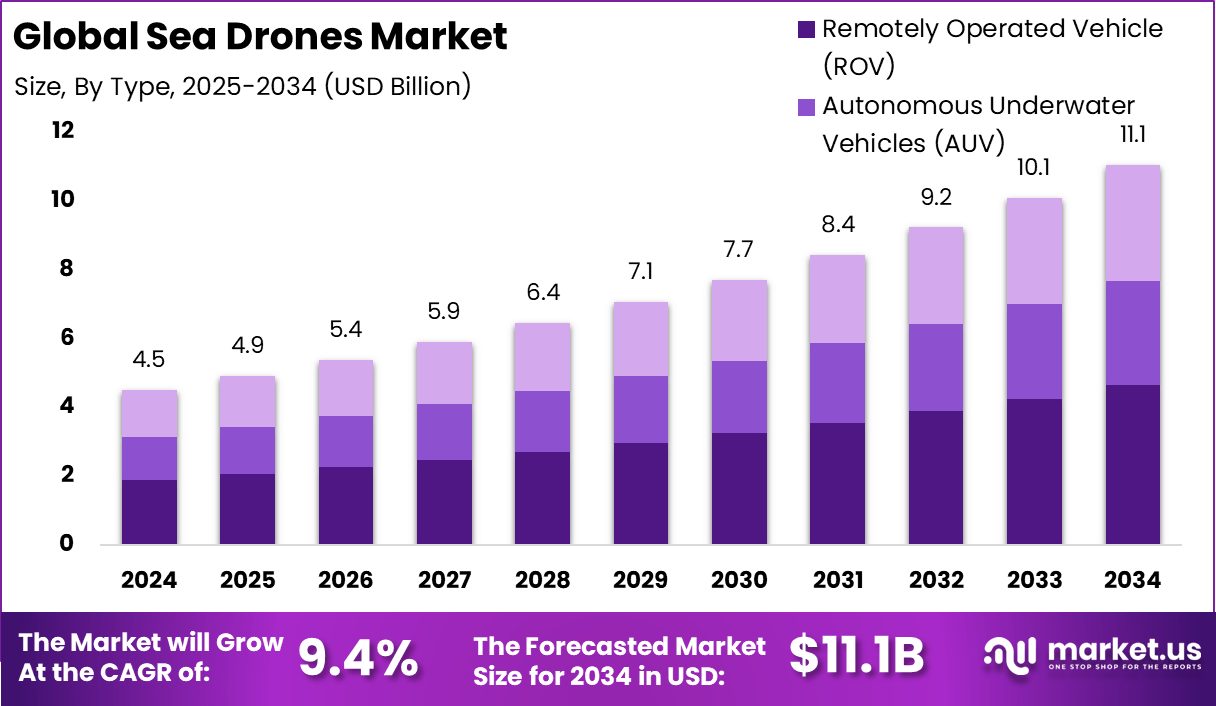

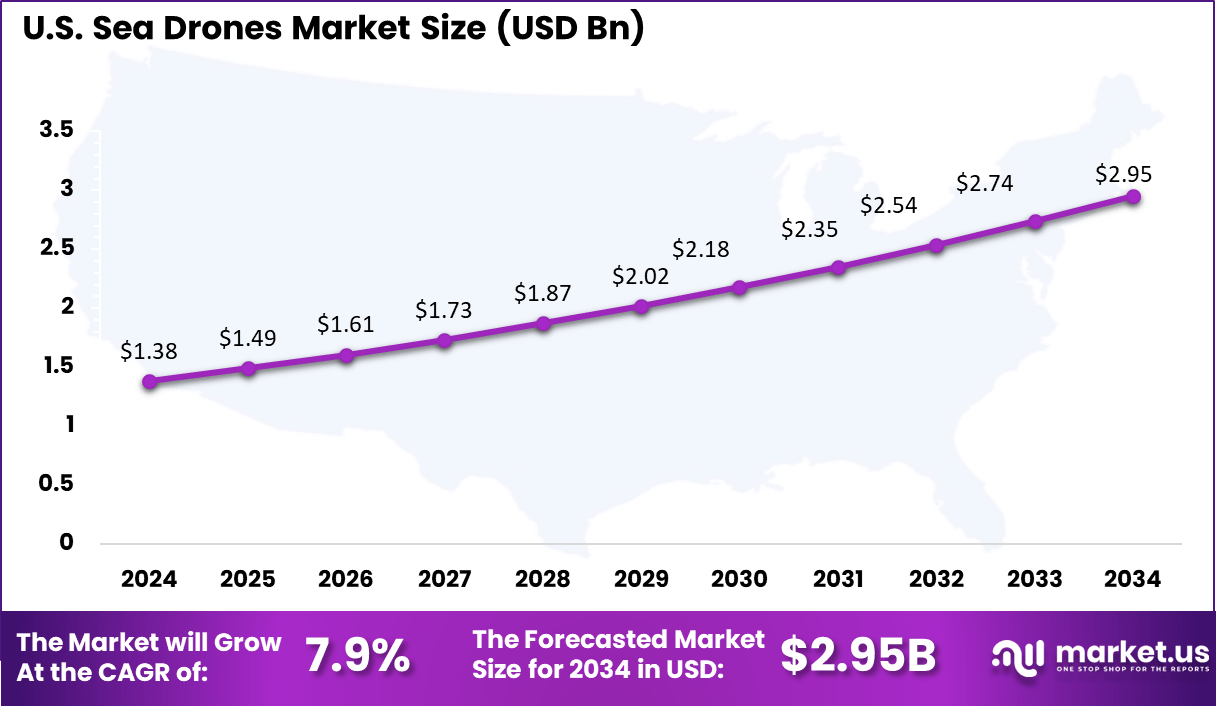

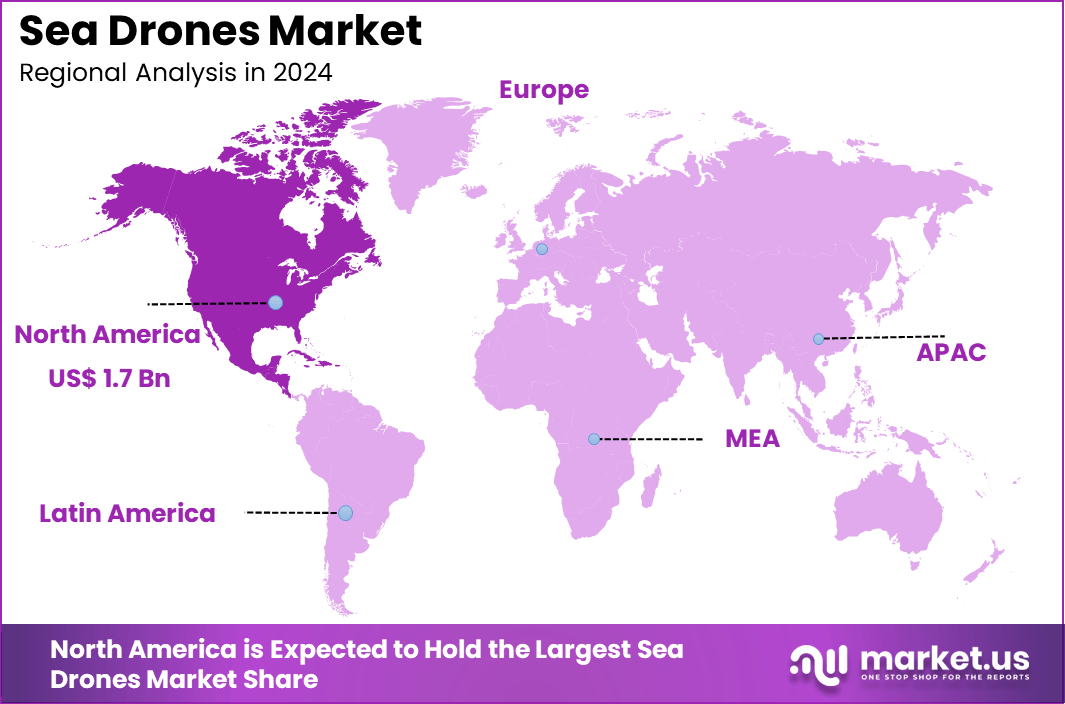

The Global Sea Drones Market size is expected to be worth around USD 11.1 Billion By 2034, from USD 4.5 billion in 2024, growing at a CAGR of 9.4% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 38.4% share, holding USD 1.7 Billion revenue. In 2024, the U.S. Sea Drones market was valued at USD 1.38 billion. The market is growing at a CAGR of 7.9%.

Sea drones, encompassing both unmanned surface vessels (USVs) and unmanned underwater vehicles (UUVs), have emerged as pivotal assets in modern maritime operations. These autonomous systems are designed to perform tasks ranging from surveillance and reconnaissance to environmental monitoring and infrastructure inspection.

Key factors propelling the demand for sea drones include heightened maritime security concerns, the necessity for efficient offshore infrastructure inspection, and the pursuit of cost-effective methods for oceanographic research. The versatility of sea drones enables their deployment in various applications, such as border patrol, disaster response, and undersea exploration, thereby broadening their appeal across multiple industries.

Technological advancements are central to the increasing adoption of sea drones. Innovations in battery technology, sensor integration, and autonomous navigation have significantly improved the endurance, reliability, and functionality of these systems.

For instance, the development of AI-driven data analysis allows for real-time decision-making and adaptive mission planning, enhancing operational efficiency. Additionally, improvements in communication systems facilitate better coordination between unmanned and manned assets, enabling more complex and collaborative missions.

The adoption of sea drones is motivated by several compelling reasons. Primarily, they offer a safer alternative to manned missions in high-risk environments, such as mine detection or deep-sea exploration. Their deployment reduces the need for human exposure to dangerous conditions, thereby minimizing potential casualties.

Key Takeaways

- The Global Sea Drones Market is set for strong long-term growth. Valued at USD 4.5 billion in 2024, the market is expected to reach USD 11.1 billion by 2034, expanding at a steady CAGR of 9.4%.

- In terms of regional dominance, North America led the market in 2024, accounting for over 38.4% share, with revenue touching USD 1.7 billion.

- The U.S. market alone was valued at USD 1.38 billion in 2024, with a projected growth rate of 7.9% CAGR. Growing geopolitical concerns and the need for smarter naval operations are fueling domestic demand for sea drones across both military and civil sectors.

- From a technology perspective, the Remotely Operated Vehicle (ROV) segment held a clear edge, capturing 42.8% of the global market in 2024.

- In terms of size classification, Small and Medium sea drones took the lead with over 34.7% share. Their ease of deployment and suitability for coastal and tactical operations make them increasingly attractive to both government and private players.

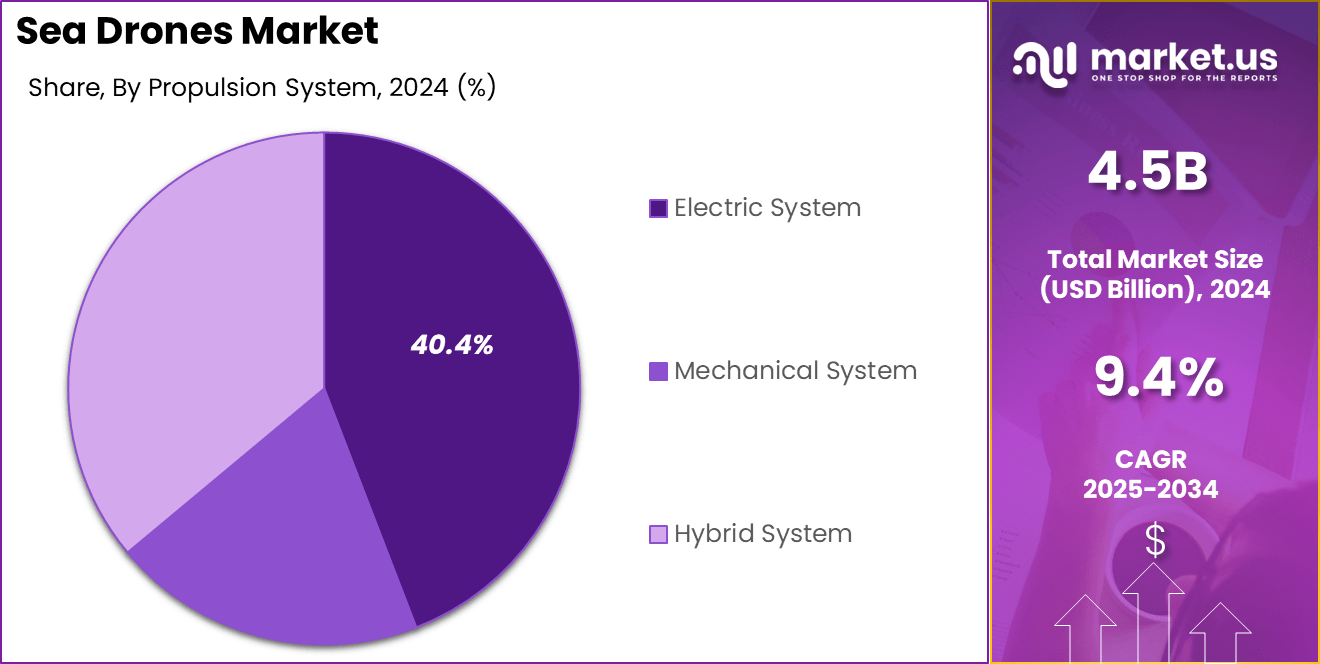

- On the power source front, the Electric System segment dominated the market with a 40.4% share. The shift toward electric propulsion is driven by quieter operations, lower emissions, and longer mission endurance, especially in surveillance use cases.

- The Defense and Security segment remained the largest application vertical, capturing 38.9% of the global share in 2024.

Analysts’ Viewpoint

The sea drones market presents significant investment opportunities due to its wide-ranging applications across defense and commercial sectors. Defense agencies are boosting spending on unmanned maritime systems to strengthen surveillance and security operations. At the same time, commercial investments are rising in areas such as offshore oil exploration, undersea cable inspection, and environmental monitoring.

The convergence of technological innovation and market demand presents a fertile ground for investors seeking growth in the maritime domain. Businesses stand to gain significant benefits from integrating sea drones into their operations. These systems offer enhanced data collection capabilities, enabling more informed decision-making processes.

In industries like shipping and offshore energy, sea drones facilitate predictive maintenance by providing detailed inspections of hulls and subsea structures, thereby preventing costly failures. Additionally, their use in environmental assessments supports compliance with regulatory standards and promotes sustainable practices.

The regulatory environment for sea drones is evolving to accommodate the rapid advancement of unmanned maritime technologies. International maritime organizations and national authorities are developing frameworks to ensure the safe and responsible operation of sea drones. These regulations address aspects such as collision avoidance, communication protocols, and data security.

U.S. Market Forecast Expansion

The US Sea Drones Market is valued at approximately USD 1.38 Billion in 2024 and is predicted to increase from USD 1.49 Billion in 2025 to approximately USD 2.95 Billion by 2034, projected at a CAGR of 7.9% from 2025 to 2034.

In 2024, North America held a dominant market position in the global sea drones market, capturing more than 38.4% of the total share and generating revenue of approximately USD 1.7 billion. This regional leadership is largely driven by high defense spending, especially by the U.S. Navy, which has actively adopted unmanned maritime systems for surveillance, reconnaissance, mine detection, and anti-submarine operations.

The focus on modernizing naval fleets with autonomous and remotely operated underwater vehicles has placed North America at the forefront of sea drone adoption. Additionally, the growing use of sea drones in offshore oil and gas inspections, underwater infrastructure monitoring, and environmental research across U.S. and Canadian waters has further fueled market demand.

The region’s dominance is further reinforced by a mature ecosystem of defense contractors and marine technology startups, which collectively drive product innovation and speed up commercialization cycles. As maritime security and ocean intelligence become critical national priorities, North America is expected to maintain its leadership in the sea drone market over the forecast period.

By Type Analysis

In 2024, the Remotely Operated Vehicle (ROV) segment held a dominant position in the global sea drones market, capturing more than a 42.8% share. This leadership is primarily attributed to the extensive utilization of ROVs in offshore oil and gas operations, where they are indispensable for tasks such as subsea infrastructure inspection, maintenance, and repair.

The capability of ROVs to perform complex underwater operations in deepwater and ultra-deepwater environments has solidified their prominence in the market. The dominance of the ROV segment is further reinforced by their critical role in various applications beyond the energy sector. In defense, ROVs are employed for mine countermeasures, surveillance, and reconnaissance missions.

According to Cleaner Seas, remotely operated vehicles (ROVs) are proving to be a cost-effective solution for the aquaculture industry. It has been reported that inspection costs can be reduced by up to 40% when ROVs are deployed for routine underwater monitoring in fish farms. This reduction is largely due to the elimination of the need for divers and the automation of detailed visual inspections in deep or hazardous zones.

Environmental monitoring and scientific research also benefit from ROVs’ ability to collect high-resolution data and samples from challenging underwater terrains. The integration of advanced technologies, such as high-definition cameras, sonar systems, and robotic arms, has enhanced the operational efficiency and versatility of ROVs, making them a preferred choice for diverse underwater missions.

The sustained investment in ROV technology, coupled with their proven reliability in harsh underwater conditions, underscores their continued dominance in the sea drones market. As industries increasingly seek robust and precise underwater solutions, the demand for ROVs is expected to remain strong, maintaining their leading position in the market.

By Product Type Analysis

In 2024, the Small and Medium segment held a dominant position in the global sea drones market, capturing more than a 34.7% share. This dominance is attributed to the segment’s versatility and cost-effectiveness, making these drones suitable for a wide range of applications, including environmental monitoring, underwater inspections, and defense operations.

Their compact size allows for easier deployment and maneuverability in various underwater environments, enhancing their appeal across multiple industries. The leading position of the Small and Medium segment is further reinforced by technological advancements that have improved their operational capabilities.

These drones now feature enhanced battery life, high-resolution imaging systems, and advanced navigation technologies, enabling more efficient and precise underwater tasks. Moreover, their affordability compared to larger work-class drones makes them an attractive option for organizations with budget constraints, thereby broadening their adoption in both commercial and research sectors.

By Propulsion System Analysis

In 2024, the Electric System segment held a dominant position in the global sea drones market, capturing more than a 40.4% share. This leadership is primarily attributed to the superior energy efficiency of electric propulsion systems compared to traditional mechanical systems.

Electric systems convert a larger portion of energy from the power source into thrust, resulting in longer mission durations and reduced operational costs. These advantages have made electric propulsion the preferred choice for various applications, including environmental monitoring, underwater inspections, and defense operations.

The dominance of the Electric System segment is further reinforced by technological advancements that have enhanced the performance and reliability of electric propulsion in underwater environments. Innovations in battery technology have led to increased energy density, allowing for extended operational ranges and endurance.

Additionally, electric propulsion systems offer quieter operation, which is crucial for applications requiring stealth, such as military surveillance and marine life observation. The integration of advanced control systems and sensors has also improved maneuverability and precision in underwater navigation. These factors collectively contribute to the sustained preference for electric propulsion systems in the sea drones market.

By Application Analysis

In 2024, the Defense and Security segment held a dominant position in the global sea drones market, capturing more than a 38.9% share. This leadership is primarily attributed to the increasing adoption of unmanned maritime systems by military forces worldwide. These systems are employed for various critical applications, including mine detection, anti-submarine warfare, and intelligence, surveillance, and reconnaissance (ISR) missions.

The integration of advanced technologies, such as artificial intelligence and machine learning, has enhanced the capabilities of sea drones, enabling them to operate autonomously and efficiently in complex maritime environments. The dominance of the Defense and Security segment is further reinforced by significant investments from major defense organizations.

For instance, the U.S. Navy has been actively developing and deploying unmanned underwater vehicles (UUVs) like the Knifefish for mine countermeasure operations . Similarly, other nations are investing in sea drone technologies to bolster their maritime security and defense capabilities. The strategic importance of securing maritime borders and critical infrastructure has led to a sustained demand for advanced sea drones in defense applications.

Key Market Segments

By Type

- Remotely Operated Vehicle (ROV)

- Autonomous Underwater Vehicles (AUV)

- Hybrid Vehicles

By Product Type

- Micro

- Small and Medium

- Light Work-Class

- Heavy Work-Class

By Propulsion System

- Electric System

- Mechanical System

- Hybrid System

By Application

- Defense and Security

- Scientific Research

- Commercial Exploration

- Others

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Rising Global Defense Investments Fueling Sea Drone Adoption

In 2024, the global sea drones market is experiencing significant growth, primarily driven by increased defense spending worldwide. Countries are investing heavily in unmanned maritime systems to enhance their naval capabilities.

For instance, the U.S. Navy has been actively developing and deploying unmanned underwater vehicles (UUVs) like the Knifefish for mine countermeasure operations. Similarly, other nations are investing in sea drone technologies to bolster their maritime security and defense capabilities.

The strategic importance of securing maritime borders and critical infrastructure has led to a sustained demand for advanced sea drones in defense applications. These drones offer capabilities such as surveillance, reconnaissance, and mine detection, which are crucial for modern naval operations.

Restraint

High Costs and Maintenance Requirements Limiting Adoption

Despite the promising growth of the sea drones market, high initial costs and ongoing maintenance requirements pose significant challenges to widespread adoption. The development and deployment of advanced sea drones involve substantial financial investments, which can be prohibitive for smaller organizations and developing nations.

Additionally, the complexity of these systems necessitates regular maintenance and specialized technical expertise, further increasing operational costs. The high costs associated with sea drones are not limited to their acquisition.

Operational expenses, including training personnel, maintaining equipment, and ensuring compliance with regulatory standards, add to the financial burden. These factors can deter potential users, particularly in sectors with limited budgets, such as academic research institutions and small-scale commercial enterprises.

Opportunity

Expanding Applications in Offshore Energy Exploration

The offshore energy sector presents significant growth opportunities for the sea drones market. As the demand for renewable energy sources, such as offshore wind farms, continues to rise, the need for efficient and cost-effective methods of exploration and maintenance becomes increasingly important. Sea drones offer a viable solution by providing detailed seabed mapping, infrastructure inspection, and environmental monitoring capabilities.

Companies like XOcean are leveraging sea drones to conduct seabed surveys for offshore wind projects, reducing the need for manned vessels and minimizing environmental impact . These drones can operate autonomously for extended periods, collecting high-resolution data essential for the planning and maintenance of offshore energy installations. Their ability to access hard-to-reach areas and perform tasks in challenging conditions makes them invaluable assets in the offshore energy industry.

Challenge

Navigating Complex Regulatory Landscapes

One of the primary challenges facing the sea drones market is the complex and evolving regulatory environment governing their operation. Regulations vary significantly across different jurisdictions, creating uncertainty for manufacturers and operators. Compliance with diverse legal frameworks, including maritime laws, environmental regulations, and safety standards, can be cumbersome and time-consuming .

The lack of standardized international regulations for sea drones complicates cross-border operations and hinders the development of global best practices. Operators must navigate a patchwork of rules, which can lead to delays in deployment and increased operational costs. Additionally, concerns over data privacy, security, and potential environmental impacts have prompted stricter regulatory scrutiny, further challenging the industry’s growth.

To overcome these challenges, stakeholders in the sea drones market must engage with regulatory bodies to advocate for clear and consistent policies. Collaborative efforts to establish international standards and guidelines can facilitate smoother operations and promote the responsible use of sea drones. Addressing regulatory hurdles is crucial to unlocking the full potential of sea drones and ensuring their integration into various maritime sectors.

Growth Factors

Advancements in Technology and Expanding Applications

The sea drones market is experiencing significant growth, driven by technological advancements and expanding applications across various sectors. Innovations in drone technology, such as improved sensors, artificial intelligence capabilities, and enhanced battery life, are expanding the operational capabilities of marine drones.

In the defense sector, countries are increasingly investing in unmanned maritime systems to enhance their naval capabilities. For instance, the U.S. Navy has been actively developing and deploying unmanned underwater vehicles (UUVs) like the Knifefish for mine countermeasure operations . Similarly, other nations are investing in sea drone technologies to bolster their maritime security and defense capabilities.

The commercial sector is also witnessing increased adoption of sea drones. Companies like XOcean are leveraging sea drones to conduct seabed surveys for offshore wind projects, reducing the need for manned vessels and minimizing environmental impact . These drones can operate autonomously for extended periods, collecting high-resolution data essential for the planning and maintenance of offshore energy installations.

Furthermore, the integration of sea drones into offshore energy operations not only enhances efficiency but also contributes to safety by reducing the reliance on human divers for inspection tasks. As the global focus on sustainable energy intensifies, the adoption of sea drones in offshore energy exploration is expected to accelerate, offering substantial market growth potential.

Emerging Trends

Integration of AI and Autonomous Operations

One of the most significant emerging trends in the sea drones market is the integration of artificial intelligence (AI) and autonomous operations. Advancements in AI and machine learning are enabling sea drones to perform complex tasks with minimal human intervention, enhancing their efficiency and effectiveness in various applications.

In the defense sector, AI-powered sea drones are being developed for intelligence, surveillance, and reconnaissance (ISR) missions. These drones can autonomously navigate and monitor maritime environments, providing real-time data and insights to military forces. For example, the U.S. Navy’s Manta Ray drone is designed to hibernate on the sea floor for extended periods without refueling, enabling long-duration missions with minimal human oversight.

In the commercial sector, AI integration is enhancing the capabilities of sea drones in applications such as offshore energy exploration and environmental monitoring. AI-powered drones can analyze vast amounts of data collected during missions, identifying patterns and anomalies that may indicate potential issues or opportunities. This capability allows for more informed decision-making and proactive maintenance, reducing downtime and operational costs.

Business Benefits

Cost Efficiency and Enhanced Safety

The adoption of sea drones offers significant business benefits, particularly in terms of cost efficiency and enhanced safety. These advantages are driving the increasing use of sea drones across various industries, including defense, offshore energy, and environmental monitoring.

One of the primary benefits of sea drones is their ability to reduce operational costs. Traditional maritime operations often require significant resources, including manned vessels, fuel, and personnel. Sea drones, on the other hand, can operate autonomously for extended periods, reducing the need for human intervention and associated costs.

For example, companies like Saildrone are developing autonomous robotic boats powered by solar and wind energy, capable of operating for over a year without maintenance. In addition to cost savings, sea drones enhance safety by performing tasks in hazardous or challenging environments. In the offshore energy sector, sea drones can conduct inspections and maintenance of underwater infrastructure, reducing the need for human divers and minimizing the risk of accidents.

Key Player Analysis

The sea drones market has witnessed significant growth, driven by advancements in technology and increasing demand for maritime surveillance and exploration. Among the leading companies in this sector, Boeing, ECA Group, and Saab Seaeye have made notable strides through acquisitions, product innovations, and strategic partnerships.

Boeing has solidified its position in the sea drones market through strategic acquisitions and product development. In 2016, Boeing acquired Liquid Robotics, a company specializing in wave and solar-powered unmanned surface vehicles (USVs), enhancing its capabilities in persistent ocean surveillance. Further expanding its portfolio, Boeing developed the Orca Extra-Large Unmanned Undersea Vehicle (XLUUV) for the U.S. Navy.

ECA Group, a French company, has been at the forefront of developing autonomous underwater vehicles (AUVs) and remotely operated vehicles (ROVs) for both civilian and military applications. The company has focused on integrating advanced technologies into its products, such as the A18D AUV, which is designed for deep-sea exploration and can operate at depths of up to 3,000 meters.

Saab Seaeye, a subsidiary of the Swedish aerospace and defense company Saab Group, specializes in electric ROVs for various underwater tasks. The company has introduced innovative products like the Sabertooth, a hybrid AUV/ROV capable of autonomous inspection and intervention tasks. This vehicle can operate in both tethered and untethered modes, providing flexibility for complex underwater operations.

Top Key Players in the Market

- ATLAS ELEKTRONIK GmbH (thyssenkrupp AG)

- Blueye Robotics

- Deep Ocean Engineering Inc.

- Deep Trekker Inc. (Halma plc)

- General Dynamics Corporation

- iBubble

- Kongsberg Gruppen ASA

- Lockheed Martin Corporation

- Oceaneering International Inc.

- Saab Seaeye Limited (Saab AB)

- Teledyne Marine (Teledyne Technologies Incorporated)

- The Boeing Company

- Other Players

Recent Developments

- In April 2025, ATLAS ELEKTRONIK UK partnered with BMT to enhance autonomous maritime navigation using BMT’s SEAS testbed. Additionally, the company is involved in the SeaCat project, with the first drone delivery scheduled for 2024 and subsequent deliveries in 2025.

- In February 2025, Kongsberg Discovery delivered the HUGIN Superior AUV prototype to the US Navy for a large undersea drone project. Additionally, in January 2025, Kongsberg acquired Naxys Technologies AS, enhancing its capabilities in underwater environmental monitoring.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 4.5 Bn |

| Forecast Revenue (2034) | USD 11.1 Bn |

| CAGR (2025-2034) | 9.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Type (Remotely Operated Vehicle (ROV), Autonomous Underwater Vehicles (AUV), Hybrid Vehicles), By Product Type (Micro, Small and Medium, Light Work-Class, Heavy Work-Class), By Propulsion System (Electric System, Mechanical System, Hybrid System), By Application (Defense and Security, Scientific Research, Commercial Exploration, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | ATLAS ELEKTRONIK GmbH (thyssenkrupp AG), Blueye Robotics, Deep Ocean Engineering Inc., Deep Trekker Inc. (Halma plc), General Dynamics Corporation, iBubble, Kongsberg Gruppen ASA, Lockheed Martin Corporation, Oceaneering International Inc., Saab Seaeye Limited (Saab AB), Teledyne Marine (Teledyne Technologies Incorporated), The Boeing Company, Other Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |